Nabors Porter's Five Forces Analysis

From Overview to Strategy Blueprint

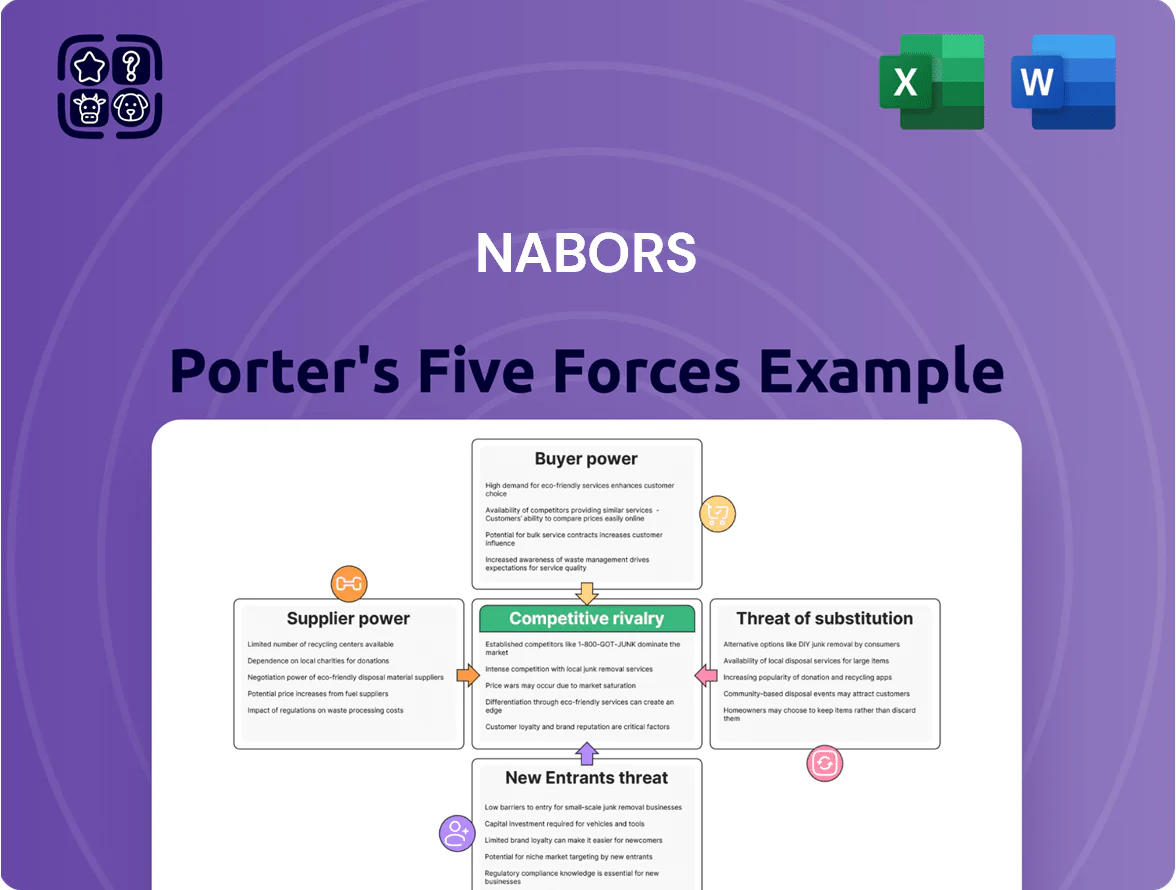

Nabors operates in a capital‑intensive, cyclical drilling market where supplier consolidation and high switching costs give suppliers moderate power, while strong buyers and industry incumbents keep competitive rivalry intense and barriers to entry high.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nabors’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Technology and Component Vendors

As Nabors ramps automation and robotics, dependence on niche vendors of high-end sensors and specialized software rises, giving suppliers leverage over pricing and delivery; these inputs are critical to Nabors’ high-margin digital services that drove 18% of services revenue in 2024.

By end-2025, global shortages pushed edge AI accelerator prices up ~35% year-over-year and lead times to 26+ weeks, further strengthening supplier bargaining power and raising Nabors’ capex risk.

Steel and Raw Material Manufacturers

Steel and alloy inputs for Nabors consume large volumes—global steel prices rose ~18% in 2023 and specialty alloy premiums can add 10–25% to base costs, so suppliers hold moderate power. Product commoditization limits pricing power, but strict specs for deep-well and Arctic drilling shrink the vendor pool to a few qualified mills. Nabors must lock long-term contracts and use hedges; a 10% steel price shock can cut rig margins by 2–4 percentage points. Maintain close supplier ties to avoid cost overruns during demand spikes.

Skilled Technical Labor Market

The oilfield services sector struggles to attract and keep petroleum engineers and software developers, who function as suppliers of specialized human capital and exert high bargaining power in automated drilling operations.

By Q4 2025, industry surveys showed a 12–18% wage premium for tech-skilled roles versus general field staff, with attrition rates near 15% annually for engineers, keeping labor costs and project margins pressured.

Proprietary Energy Storage and Power Providers

Nabors depends on a small set of suppliers for large-scale battery systems and natural-gas hybrid engines as it shifts to lower-emission rigs, giving those vendors strong bargaining power.

As ESG rules tightened in 2024–2025, operators accepted equipment premiums—battery packs cost $300–400/kWh in utility-scale deals—making suppliers non‑negotiable in contracts.

The limited number of industrial-scale manufacturers lets suppliers set prices, lead times (6–12 months), and service terms, pressuring Nabors’ margins and capex timing.

- Suppliers concentrated; few capable at scale

- Battery costs ~300–400 USD/kWh (2024–25)

- Lead times 6–12 months raise capex risk

- ESG compliance makes tech indispensable

Logistics and Transport Service Providers

Specialized heavy-haul trucking and international logistics firms are essential for moving Nabors’ rigs and components into remote basins, and delays can cost millions in idle rig time; for example, a two-week delay on a $200k/day contract equals $2.8m lost revenue.

Only a handful of providers hold the scale and safety certifications for oilfield work, so they keep steady bargaining power, pressuring rates and availability across Nabors’ global fleet of ~1,300 rigs (2025).

Rising supplier costs, long lead times and labor premiums squeeze Nabors’ rig margins

Supplier power is high: niche sensors, edge AI chips (+35% price, 26+ week lead times in 2025), batteries $300–400/kWh (2024–25), steel +18% (2023) and alloy premiums 10–25% tighten margins; skilled labor wage premium 12–18% (Q4 2025) and limited logistics providers raise capex and downtime risk for Nabors’ ~1,300 rigs (2025).

| Item | 2023–25 metric |

|---|---|

| Edge AI chips | +35% price, 26+ wk lead |

| Batteries | $300–400/kWh |

| Steel | +18% (2023) |

| Alloy premium | 10–25% |

| Labor premium | 12–18% (Q4 2025) |

| Rigs | ~1,300 (2025) |

What is included in the product

Uncovers Nabors' competitive pressures by analyzing rivalry, supplier and buyer power, threats from new entrants and substitutes, and industry-specific disruptors to inform strategic positioning and pricing.

A concise Nabors Porter’s Five Forces one-sheet that quantifies competitive pressure and highlights where strategic moves reduce risk—ideal for quick board decisions or investor briefs.

Customers Bargaining Power

Concentration of Major E&P Operators

The customer base for Nabors is dominated by a handful of supermajors and national oil companies—BP, Shell, Saudi Aramco, Chevron, and ADNOC—whose combined upstream capex share exceeded 40% of global E&P spending in 2024, giving them huge buy power. They push hard on dayrates and service levels, forcing Nabors into lower margins and shorter contracts; Nabors’ 2024 U.S. onshore revenue per rig fell 8% vs 2021. By 2025 further E&P consolidation reduced potential clients by ~15%, tightening bargaining leverage.

Price Sensitivity to Global Crude Volatility

The demand for Nabors’ drilling and rig services tracks customer capex, which fell ~22% in global E&P budgets in 2020 and remained 10–15% below 2019 levels through 2024, tying spending tightly to Brent crude moves. When Brent drops or swings (Brent ranged $60–90/bbl in 2024), customers can pressure Nabors for steep discounts or cancel with short notice. Nabors often absorbs price and uptime risk to keep contracts, cutting dayrates or offering uptime guarantees to preserve long-term relationships.

Shift Toward Performance-Based Contracting

Modern customers are shifting from day-rate models to performance-based contracts that pay premiums for drilling efficiency and safety; industry data show performance contracts accounted for about 22% of global rig revenues in 2024, up from ~12% in 2019.

For Nabors, this can boost margins when rigs meet digital and mechanical KPIs, but buyers can impose penalties—often 5–15% of contract value—if benchmarks slip.

The model shifts operational risk from oil companies to service providers, increasing buyer control over final payouts and making Nabors’ cash flow more variable tied to measurable outcomes.

Internal Technical Expertise of Clients

Many of Nabors' biggest customers—national oil majors and large independents—had by 2025 built in-house drilling tech and analytics, cutting dependence on contractor software and enabling unbundling of services.

This technical literacy lets buyers cherry-pick rigs, bits, or analytics, lowering the value of bundled services and pressuring margins; major customers reportedly reduced outside services spend by up to 15% in 2023–2024.

As client data capability rises, they can more credibly contest service pricing and push for fee-for-use or performance-based contracts, shrinking contractors' pricing power.

- 2025: top clients with in-house analytics grew to ~40% of spend

- Unbundling cut contractor package value ~10–20%

- Push toward unit pricing and performance fees increased

Low Switching Costs for Standard Rigs

While Nabors offers high-spec automated rigs, many operators still use standard rigs where provider differences are small; in 2024 about 30% of global onshore rigs were lower-spec, making that segment price-sensitive.

Customers can switch easily for lower rates, so these contracts are transactional; spot-day rates for standard rigs fell ~8% YoY in 2024, showing price pressure.

This weak loyalty pushes Nabors to innovate and upsell to automated, higher-margin services to secure stickier revenue.

- ~30% of onshore rigs lower-spec in 2024

- Standard rig rates down ~8% YoY (2024)

- Strategy: upsell to automated, higher-margin services

Big oil buyers squeeze rig margins: dayrate cuts, performance penalties, analytics unbundle

Major customers (BP, Shell, Saudi Aramco, Chevron, ADNOC) control >40% of E&P capex (2024), driving dayrate cuts and shorter contracts; Nabors’ U.S. rig revenue per rig fell 8% vs 2021. Performance contracts rose to ~22% of rig revenues (2024), shifting risk and giving buyers 5–15% penalty leverage. In-house analytics grew to ~40% of client spend by 2025, enabling unbundling and cutting contractor package value ~10–20%.

| Metric | Value |

|---|---|

| Top-client E&P share (2024) | >40% |

| Perf. contract share (2024) | ~22% |

| U.S. revenue/rig change vs 2021 | -8% |

| In-house analytics spend (2025) | ~40% |

| Unbundling impact | -10–20% |

What You See Is What You Get

Nabors Porter's Five Forces Analysis

This preview shows the exact Nabors Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual, professionally written analysis file; once your purchase is complete, you’ll have instant access to this same deliverable.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Nabors operates in a capital‑intensive, cyclical drilling market where supplier consolidation and high switching costs give suppliers moderate power, while strong buyers and industry incumbents keep competitive rivalry intense and barriers to entry high.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nabors’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Technology and Component Vendors

As Nabors ramps automation and robotics, dependence on niche vendors of high-end sensors and specialized software rises, giving suppliers leverage over pricing and delivery; these inputs are critical to Nabors’ high-margin digital services that drove 18% of services revenue in 2024.

By end-2025, global shortages pushed edge AI accelerator prices up ~35% year-over-year and lead times to 26+ weeks, further strengthening supplier bargaining power and raising Nabors’ capex risk.

Steel and Raw Material Manufacturers

Steel and alloy inputs for Nabors consume large volumes—global steel prices rose ~18% in 2023 and specialty alloy premiums can add 10–25% to base costs, so suppliers hold moderate power. Product commoditization limits pricing power, but strict specs for deep-well and Arctic drilling shrink the vendor pool to a few qualified mills. Nabors must lock long-term contracts and use hedges; a 10% steel price shock can cut rig margins by 2–4 percentage points. Maintain close supplier ties to avoid cost overruns during demand spikes.

Skilled Technical Labor Market

The oilfield services sector struggles to attract and keep petroleum engineers and software developers, who function as suppliers of specialized human capital and exert high bargaining power in automated drilling operations.

By Q4 2025, industry surveys showed a 12–18% wage premium for tech-skilled roles versus general field staff, with attrition rates near 15% annually for engineers, keeping labor costs and project margins pressured.

Proprietary Energy Storage and Power Providers

Nabors depends on a small set of suppliers for large-scale battery systems and natural-gas hybrid engines as it shifts to lower-emission rigs, giving those vendors strong bargaining power.

As ESG rules tightened in 2024–2025, operators accepted equipment premiums—battery packs cost $300–400/kWh in utility-scale deals—making suppliers non‑negotiable in contracts.

The limited number of industrial-scale manufacturers lets suppliers set prices, lead times (6–12 months), and service terms, pressuring Nabors’ margins and capex timing.

- Suppliers concentrated; few capable at scale

- Battery costs ~300–400 USD/kWh (2024–25)

- Lead times 6–12 months raise capex risk

- ESG compliance makes tech indispensable

Logistics and Transport Service Providers

Specialized heavy-haul trucking and international logistics firms are essential for moving Nabors’ rigs and components into remote basins, and delays can cost millions in idle rig time; for example, a two-week delay on a $200k/day contract equals $2.8m lost revenue.

Only a handful of providers hold the scale and safety certifications for oilfield work, so they keep steady bargaining power, pressuring rates and availability across Nabors’ global fleet of ~1,300 rigs (2025).

Rising supplier costs, long lead times and labor premiums squeeze Nabors’ rig margins

Supplier power is high: niche sensors, edge AI chips (+35% price, 26+ week lead times in 2025), batteries $300–400/kWh (2024–25), steel +18% (2023) and alloy premiums 10–25% tighten margins; skilled labor wage premium 12–18% (Q4 2025) and limited logistics providers raise capex and downtime risk for Nabors’ ~1,300 rigs (2025).

| Item | 2023–25 metric |

|---|---|

| Edge AI chips | +35% price, 26+ wk lead |

| Batteries | $300–400/kWh |

| Steel | +18% (2023) |

| Alloy premium | 10–25% |

| Labor premium | 12–18% (Q4 2025) |

| Rigs | ~1,300 (2025) |

What is included in the product

Uncovers Nabors' competitive pressures by analyzing rivalry, supplier and buyer power, threats from new entrants and substitutes, and industry-specific disruptors to inform strategic positioning and pricing.

A concise Nabors Porter’s Five Forces one-sheet that quantifies competitive pressure and highlights where strategic moves reduce risk—ideal for quick board decisions or investor briefs.

Customers Bargaining Power

Concentration of Major E&P Operators

The customer base for Nabors is dominated by a handful of supermajors and national oil companies—BP, Shell, Saudi Aramco, Chevron, and ADNOC—whose combined upstream capex share exceeded 40% of global E&P spending in 2024, giving them huge buy power. They push hard on dayrates and service levels, forcing Nabors into lower margins and shorter contracts; Nabors’ 2024 U.S. onshore revenue per rig fell 8% vs 2021. By 2025 further E&P consolidation reduced potential clients by ~15%, tightening bargaining leverage.

Price Sensitivity to Global Crude Volatility

The demand for Nabors’ drilling and rig services tracks customer capex, which fell ~22% in global E&P budgets in 2020 and remained 10–15% below 2019 levels through 2024, tying spending tightly to Brent crude moves. When Brent drops or swings (Brent ranged $60–90/bbl in 2024), customers can pressure Nabors for steep discounts or cancel with short notice. Nabors often absorbs price and uptime risk to keep contracts, cutting dayrates or offering uptime guarantees to preserve long-term relationships.

Shift Toward Performance-Based Contracting

Modern customers are shifting from day-rate models to performance-based contracts that pay premiums for drilling efficiency and safety; industry data show performance contracts accounted for about 22% of global rig revenues in 2024, up from ~12% in 2019.

For Nabors, this can boost margins when rigs meet digital and mechanical KPIs, but buyers can impose penalties—often 5–15% of contract value—if benchmarks slip.

The model shifts operational risk from oil companies to service providers, increasing buyer control over final payouts and making Nabors’ cash flow more variable tied to measurable outcomes.

Internal Technical Expertise of Clients

Many of Nabors' biggest customers—national oil majors and large independents—had by 2025 built in-house drilling tech and analytics, cutting dependence on contractor software and enabling unbundling of services.

This technical literacy lets buyers cherry-pick rigs, bits, or analytics, lowering the value of bundled services and pressuring margins; major customers reportedly reduced outside services spend by up to 15% in 2023–2024.

As client data capability rises, they can more credibly contest service pricing and push for fee-for-use or performance-based contracts, shrinking contractors' pricing power.

- 2025: top clients with in-house analytics grew to ~40% of spend

- Unbundling cut contractor package value ~10–20%

- Push toward unit pricing and performance fees increased

Low Switching Costs for Standard Rigs

While Nabors offers high-spec automated rigs, many operators still use standard rigs where provider differences are small; in 2024 about 30% of global onshore rigs were lower-spec, making that segment price-sensitive.

Customers can switch easily for lower rates, so these contracts are transactional; spot-day rates for standard rigs fell ~8% YoY in 2024, showing price pressure.

This weak loyalty pushes Nabors to innovate and upsell to automated, higher-margin services to secure stickier revenue.

- ~30% of onshore rigs lower-spec in 2024

- Standard rig rates down ~8% YoY (2024)

- Strategy: upsell to automated, higher-margin services

Big oil buyers squeeze rig margins: dayrate cuts, performance penalties, analytics unbundle

Major customers (BP, Shell, Saudi Aramco, Chevron, ADNOC) control >40% of E&P capex (2024), driving dayrate cuts and shorter contracts; Nabors’ U.S. rig revenue per rig fell 8% vs 2021. Performance contracts rose to ~22% of rig revenues (2024), shifting risk and giving buyers 5–15% penalty leverage. In-house analytics grew to ~40% of client spend by 2025, enabling unbundling and cutting contractor package value ~10–20%.

| Metric | Value |

|---|---|

| Top-client E&P share (2024) | >40% |

| Perf. contract share (2024) | ~22% |

| U.S. revenue/rig change vs 2021 | -8% |

| In-house analytics spend (2025) | ~40% |

| Unbundling impact | -10–20% |

What You See Is What You Get

Nabors Porter's Five Forces Analysis

This preview shows the exact Nabors Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual, professionally written analysis file; once your purchase is complete, you’ll have instant access to this same deliverable.