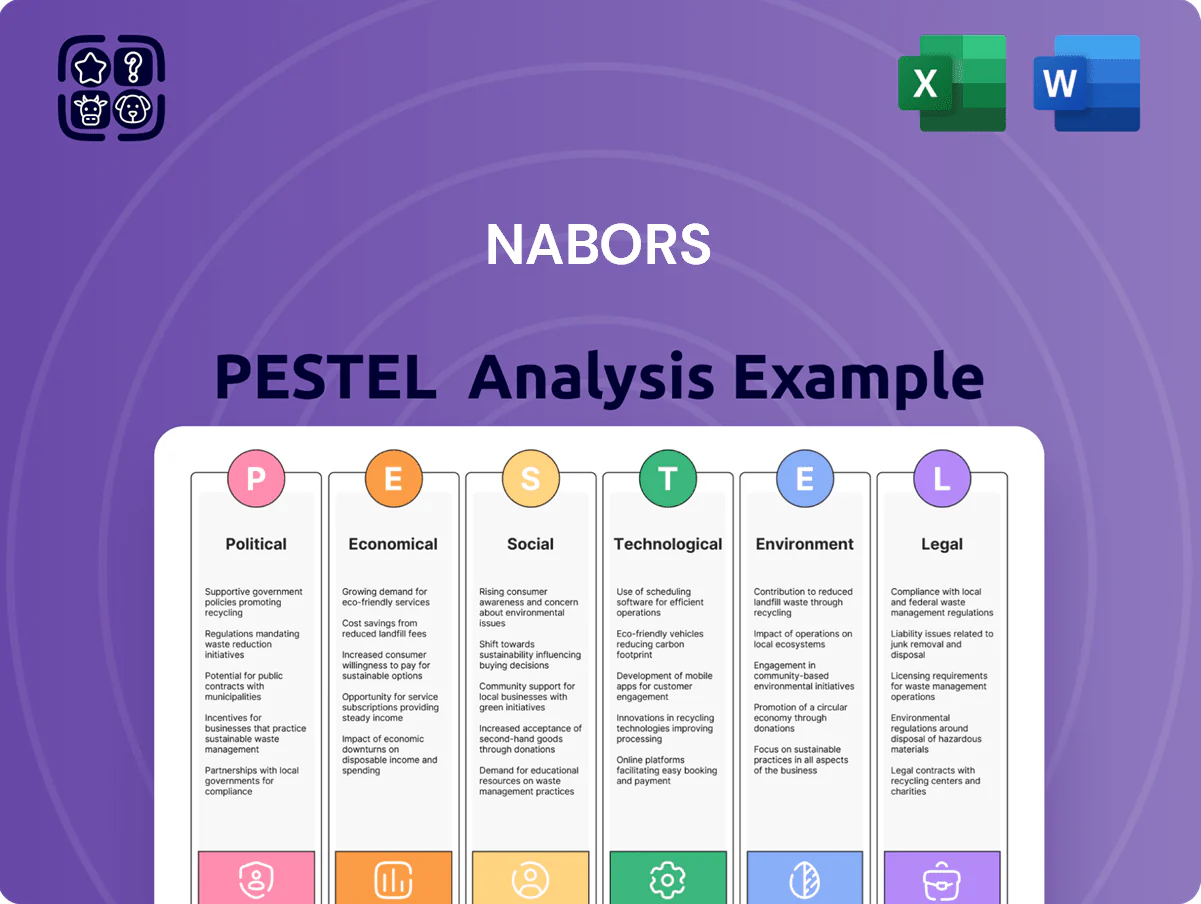

Nabors PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis of Nabors reveals how political shifts, energy-market cycles, and technological advances are reshaping its competitive edge—perfect for investors and strategists who need concise, actionable intelligence. Purchase the full report to access detailed regulatory risk maps, economic scenarios, and innovation levers you can use immediately to inform decisions and pitchbooks.

Political factors

Geopolitical instability in energy regions

Nabors' global operations face heightened risk from geopolitical instability in energy regions; in 2024 over 40% of global drilling activity was influenced by Middle East and Eastern Europe tensions, which can delay supply chains and drilling schedules for the company.

Turbulence in those regions contributed to Brent crude price swings of 18% in 2024, directly affecting demand for Nabors' advanced rig services and revenue visibility.

Management must navigate shifting alliances and conflict risks that in 2025 threaten physical assets and personnel, with insurers raising premiums by roughly 12% for operations in high-risk zones.

Energy security and trade policies

Governments prioritizing domestic energy security are offering incentives—US IRA tax credits and Canadian provincial drilling credits—boosting land-rig demand; US onshore rig count rose to 862 in Feb 2025, supporting Nabors' contracts.

Tariff shifts on drilling equipment and steel affect maintenance costs: US steel tariffs raised domestic plate prices ~15% in 2024, increasing lift‑boat and rig refurbishment expenses for Nabors.

North American energy independence keeps demand local for high-spec land rigs: Permian Basin activity accounted for ~45% of US rig demand in 2024, favoring Nabors’ modern fleet.

International sanctions and export controls

Nabors must navigate sanctions from jurisdictions like the US, EU and UK that in 2024 covered over 40 countries; these regimes restrict export of drilling automation and software, limiting access to high-growth markets such as parts of Africa and the Middle East where oil services spending grew ~6% in 2024. Non-compliance risks fines—US penalties often exceed $1M per violation and reach billions in aggregate—and material reputational damage affecting contract wins.

Government energy transition incentives

- 2024: ~$4.8B federal carbon capture allocations; geothermal IRA incentives ~$1–2B/yr

- Nabors expanding tech/services into CCUS and geothermal

- Revenue growth tied to legislative funding and timely appropriations

Taxation and royalty adjustments

Changes in corporate tax rates or royalty structures where Nabors operates can swing drilling project NPV by 5–20%; for example, a 5 percentage-point royalty hike in Mexico in 2024 raised production costs for operators by ~12% seasonally.

Host governments adjust taxes/royalties to shore up revenue or push cleaner extraction—Norway’s tax changes in 2023 increased marginal tax burdens on oilfield services, tightening operator CAPEX plans.

Investors track legislative shifts closely since tax/royalty moves directly affect customers’ CAPEX; a 2024 industry survey showed 68% of operators delayed rigs procurement after tax/royalty proposals.

- NPV impact: 5–20%

- 2024 example: Mexico royalty hike → ~12% production cost rise

- 2023 Norway tax changes tightened CAPEX

- 2024 survey: 68% of operators delayed rig purchases

Policy cashbacks and Permian resilience reshape rig demand, tipping Nabors to CCUS/geothermal

Geopolitical instability and sanctions in 2024–25 disrupted supply chains and raised insurance/tariff costs, while US/Canada incentives and Permian strength supported land‑rig demand; tax/royalty shifts altered project NPVs by ~5–20%, with policy funding (e.g., ~$4.8B CCUS, $1–2B geothermal) key to Nabors’ CCUS/geothermal pivot.

| Metric | 2024–25 |

|---|---|

| Brent volatility | 18% |

| US onshore rig count (Feb 2025) | 862 |

| Permian share | 45% |

| CCUS funding | $4.8B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Nabors across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by data, trend analysis, and forward-looking insights to support scenario planning and strategy design.

Condensed PESTLE insights tailored for Nabors, enabling quick risk assessment and strategic alignment during meetings or presentations.

Economic factors

Fluctuating global commodity prices

The demand for Nabors' drilling services tracks oil and gas prices; Brent averaged about 95 USD/bbl in 2024, supporting higher rig activity and boosting average U.S. land rig dayrates to roughly 25–30k USD/day in late 2024–2025, improving utilization. When prices plunged in 2020, rigs were idled and contracts cut; similar volatility risks remain as a sharp price drop would rapidly create surplus idle fleets and margin pressure.

High interest rate environment

As a capital-intensive operator, Nabors is highly sensitive to borrowing costs needed for rig upgrades and R&D; with US Fed rates at 5.25–5.50% in late 2024, sustained high rates raise financing costs. Higher rates increase the burden of servicing Nabors’ roughly $3.1bn debt (2024) and can push back investments in next-gen automated rigs. Analysts focus on Nabors’ interest coverage (EBITDA/interest ≈ 3.2x in 2024) and debt maturities to gauge resilience in tight credit markets.

Inflationary pressure on operating costs

Rising costs for steel, drilling equipment and skilled rig crews have pressured margins; global steel prices averaged about 1,050 USD/ton in 2024, up roughly 12% year-on-year, increasing capital and maintenance spend for Nabors.

Nabors faces difficulty passing costs to customers as 2024 average US onshore dayrates rose ~8–10%, risking competitiveness if dayrates lag input inflation.

Persistent 2023–24 inflation (US CPI ~3.4% in 2024) makes supply chain resilience and strategic procurement—longer contracts, vendor diversification, hedging—critical to protect EBITDA.

Currency exchange rate volatility

With roughly 40% of Nabors Holdings’ 2024 revenue derived from international operations, USD volatility against CAD, MXN and Middle Eastern currencies materially affects reported earnings; a 5% USD appreciation in 2024 reduced consolidated revenue by an estimated 2–3% on translation effects.

Currency devaluations in emerging markets—e.g., a 12% MXN decline in 2023–24—eroded local clients’ purchasing power and complicated repatriation of profits due to capital controls and higher conversion costs.

Nabors employs currency hedges, forwards and selective natural hedging across its geographic footprint; management reported hedging coverage of approximately 60% of anticipated FX exposure for 2025 during its 2024 investor update.

- ~40% 2024 revenue international

- 5% USD appreciation → ~2–3% revenue translation hit

- 12% MXN decline 2023–24 reduced local purchasing power

- ~60% hedging coverage for 2025 FX exposure

Global capital expenditure cycles

The energy sector's capex cycles drive demand for drilling tech; global upstream capex fell about 8% to $430 billion in 2024 after 2023’s recovery, pressuring timing and scale for Nabors' investments.

Nabors must synchronize growth with majors and independents—Top 10 IOC/independent capex plans account for roughly 45% of 2025 upstream spend—shifting strategy toward service contracts tied to customer budgets.

During downturns Nabors pivots to efficiency and market-share defense; focusing on utilization, cost reduction, and aftermarket services helped peers sustain ~70–80% rig utilization in weak phases.

- Global upstream capex ~ $430B (2024)

- Top customers represent ~45% of 2025 upstream spend

- Peer rig utilization ~70–80% in downturns

Nabors faces tight margins as oil rallies but rates, debt and input costs bite

Oil prices (Brent ~95 USD/bbl in 2024) lifted rig dayrates to ~25–30k USD/day, aiding utilization; however price volatility can quickly idle fleets. High US rates (5.25–5.50% late 2024) raise financing costs for Nabors’ ~$3.1bn debt and capex, with interest coverage ≈3.2x. Input inflation (steel ~$1,050/ton in 2024) and FX swings (USD +5% → −2–3% rev translation) compress margins.

| Metric | 2024/2025 Value |

|---|---|

| Brent | ~95 USD/bbl |

| U.S. land dayrate | ~25–30k USD/day |

| Debt | ~3.1bn USD |

| Fed rate | 5.25–5.50% |

| Steel | ~1,050 USD/ton |

| USD appreciation impact | 5% → −2–3% rev |

Full Version Awaits

Nabors PESTLE Analysis

The preview shown here is the exact Nabors PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis of Nabors reveals how political shifts, energy-market cycles, and technological advances are reshaping its competitive edge—perfect for investors and strategists who need concise, actionable intelligence. Purchase the full report to access detailed regulatory risk maps, economic scenarios, and innovation levers you can use immediately to inform decisions and pitchbooks.

Political factors

Geopolitical instability in energy regions

Nabors' global operations face heightened risk from geopolitical instability in energy regions; in 2024 over 40% of global drilling activity was influenced by Middle East and Eastern Europe tensions, which can delay supply chains and drilling schedules for the company.

Turbulence in those regions contributed to Brent crude price swings of 18% in 2024, directly affecting demand for Nabors' advanced rig services and revenue visibility.

Management must navigate shifting alliances and conflict risks that in 2025 threaten physical assets and personnel, with insurers raising premiums by roughly 12% for operations in high-risk zones.

Energy security and trade policies

Governments prioritizing domestic energy security are offering incentives—US IRA tax credits and Canadian provincial drilling credits—boosting land-rig demand; US onshore rig count rose to 862 in Feb 2025, supporting Nabors' contracts.

Tariff shifts on drilling equipment and steel affect maintenance costs: US steel tariffs raised domestic plate prices ~15% in 2024, increasing lift‑boat and rig refurbishment expenses for Nabors.

North American energy independence keeps demand local for high-spec land rigs: Permian Basin activity accounted for ~45% of US rig demand in 2024, favoring Nabors’ modern fleet.

International sanctions and export controls

Nabors must navigate sanctions from jurisdictions like the US, EU and UK that in 2024 covered over 40 countries; these regimes restrict export of drilling automation and software, limiting access to high-growth markets such as parts of Africa and the Middle East where oil services spending grew ~6% in 2024. Non-compliance risks fines—US penalties often exceed $1M per violation and reach billions in aggregate—and material reputational damage affecting contract wins.

Government energy transition incentives

- 2024: ~$4.8B federal carbon capture allocations; geothermal IRA incentives ~$1–2B/yr

- Nabors expanding tech/services into CCUS and geothermal

- Revenue growth tied to legislative funding and timely appropriations

Taxation and royalty adjustments

Changes in corporate tax rates or royalty structures where Nabors operates can swing drilling project NPV by 5–20%; for example, a 5 percentage-point royalty hike in Mexico in 2024 raised production costs for operators by ~12% seasonally.

Host governments adjust taxes/royalties to shore up revenue or push cleaner extraction—Norway’s tax changes in 2023 increased marginal tax burdens on oilfield services, tightening operator CAPEX plans.

Investors track legislative shifts closely since tax/royalty moves directly affect customers’ CAPEX; a 2024 industry survey showed 68% of operators delayed rigs procurement after tax/royalty proposals.

- NPV impact: 5–20%

- 2024 example: Mexico royalty hike → ~12% production cost rise

- 2023 Norway tax changes tightened CAPEX

- 2024 survey: 68% of operators delayed rig purchases

Policy cashbacks and Permian resilience reshape rig demand, tipping Nabors to CCUS/geothermal

Geopolitical instability and sanctions in 2024–25 disrupted supply chains and raised insurance/tariff costs, while US/Canada incentives and Permian strength supported land‑rig demand; tax/royalty shifts altered project NPVs by ~5–20%, with policy funding (e.g., ~$4.8B CCUS, $1–2B geothermal) key to Nabors’ CCUS/geothermal pivot.

| Metric | 2024–25 |

|---|---|

| Brent volatility | 18% |

| US onshore rig count (Feb 2025) | 862 |

| Permian share | 45% |

| CCUS funding | $4.8B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Nabors across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by data, trend analysis, and forward-looking insights to support scenario planning and strategy design.

Condensed PESTLE insights tailored for Nabors, enabling quick risk assessment and strategic alignment during meetings or presentations.

Economic factors

Fluctuating global commodity prices

The demand for Nabors' drilling services tracks oil and gas prices; Brent averaged about 95 USD/bbl in 2024, supporting higher rig activity and boosting average U.S. land rig dayrates to roughly 25–30k USD/day in late 2024–2025, improving utilization. When prices plunged in 2020, rigs were idled and contracts cut; similar volatility risks remain as a sharp price drop would rapidly create surplus idle fleets and margin pressure.

High interest rate environment

As a capital-intensive operator, Nabors is highly sensitive to borrowing costs needed for rig upgrades and R&D; with US Fed rates at 5.25–5.50% in late 2024, sustained high rates raise financing costs. Higher rates increase the burden of servicing Nabors’ roughly $3.1bn debt (2024) and can push back investments in next-gen automated rigs. Analysts focus on Nabors’ interest coverage (EBITDA/interest ≈ 3.2x in 2024) and debt maturities to gauge resilience in tight credit markets.

Inflationary pressure on operating costs

Rising costs for steel, drilling equipment and skilled rig crews have pressured margins; global steel prices averaged about 1,050 USD/ton in 2024, up roughly 12% year-on-year, increasing capital and maintenance spend for Nabors.

Nabors faces difficulty passing costs to customers as 2024 average US onshore dayrates rose ~8–10%, risking competitiveness if dayrates lag input inflation.

Persistent 2023–24 inflation (US CPI ~3.4% in 2024) makes supply chain resilience and strategic procurement—longer contracts, vendor diversification, hedging—critical to protect EBITDA.

Currency exchange rate volatility

With roughly 40% of Nabors Holdings’ 2024 revenue derived from international operations, USD volatility against CAD, MXN and Middle Eastern currencies materially affects reported earnings; a 5% USD appreciation in 2024 reduced consolidated revenue by an estimated 2–3% on translation effects.

Currency devaluations in emerging markets—e.g., a 12% MXN decline in 2023–24—eroded local clients’ purchasing power and complicated repatriation of profits due to capital controls and higher conversion costs.

Nabors employs currency hedges, forwards and selective natural hedging across its geographic footprint; management reported hedging coverage of approximately 60% of anticipated FX exposure for 2025 during its 2024 investor update.

- ~40% 2024 revenue international

- 5% USD appreciation → ~2–3% revenue translation hit

- 12% MXN decline 2023–24 reduced local purchasing power

- ~60% hedging coverage for 2025 FX exposure

Global capital expenditure cycles

The energy sector's capex cycles drive demand for drilling tech; global upstream capex fell about 8% to $430 billion in 2024 after 2023’s recovery, pressuring timing and scale for Nabors' investments.

Nabors must synchronize growth with majors and independents—Top 10 IOC/independent capex plans account for roughly 45% of 2025 upstream spend—shifting strategy toward service contracts tied to customer budgets.

During downturns Nabors pivots to efficiency and market-share defense; focusing on utilization, cost reduction, and aftermarket services helped peers sustain ~70–80% rig utilization in weak phases.

- Global upstream capex ~ $430B (2024)

- Top customers represent ~45% of 2025 upstream spend

- Peer rig utilization ~70–80% in downturns

Nabors faces tight margins as oil rallies but rates, debt and input costs bite

Oil prices (Brent ~95 USD/bbl in 2024) lifted rig dayrates to ~25–30k USD/day, aiding utilization; however price volatility can quickly idle fleets. High US rates (5.25–5.50% late 2024) raise financing costs for Nabors’ ~$3.1bn debt and capex, with interest coverage ≈3.2x. Input inflation (steel ~$1,050/ton in 2024) and FX swings (USD +5% → −2–3% rev translation) compress margins.

| Metric | 2024/2025 Value |

|---|---|

| Brent | ~95 USD/bbl |

| U.S. land dayrate | ~25–30k USD/day |

| Debt | ~3.1bn USD |

| Fed rate | 5.25–5.50% |

| Steel | ~1,050 USD/ton |

| USD appreciation impact | 5% → −2–3% rev |

Full Version Awaits

Nabors PESTLE Analysis

The preview shown here is the exact Nabors PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.