Nanogate Porter's Five Forces Analysis

Don't Miss the Bigger Picture

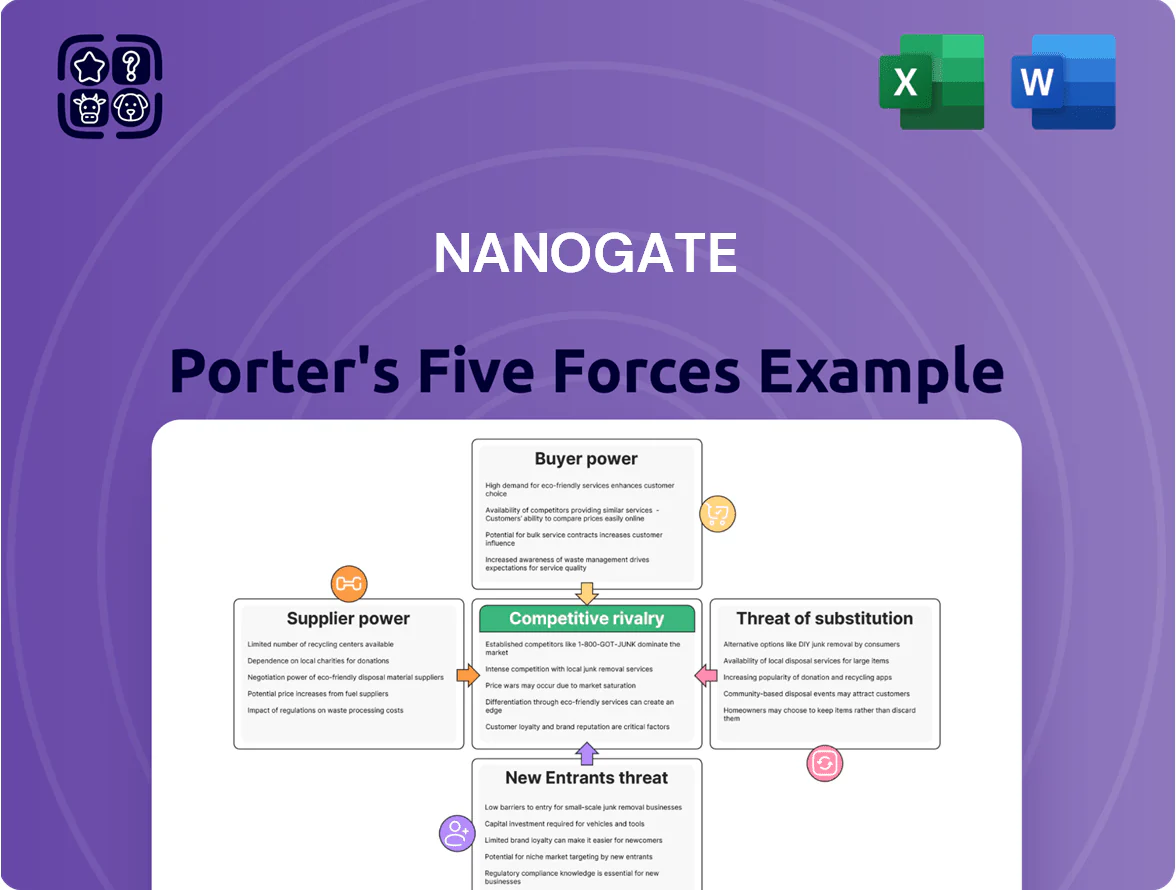

Nanogate faces moderate supplier power due to specialized inputs, while buyer concentration and price sensitivity heighten competitive pressure; substitutes and tech disruption pose emerging threats, and barriers to entry are medium given capital and know-how requirements.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nanogate’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Chemical and Raw Material Providers

The production of high-performance surfaces depends on niche chemical compounds and high-purity polymers from a small set of global suppliers, giving them strong leverage over Techniplas Nano Tec SE; about 60–70% of specialty monomers supply is concentrated among five firms as of 2025. Disruptions or a 10–20% price swing in these inputs would raise manufacturing costs materially, so Techniplas must keep strategic long-term contracts and dual sourcing to secure quality and availability.

Technological Equipment Manufacturers

The small pool of high-tech firms that make thin-film and nanotech production equipment gives suppliers strong bargaining power; global semiconductor tool makers saw 18% revenue growth in 2024, concentrating R&D and pricing power. Techniplas relies on these vendors for support and hardware advances, and typical equipment units cost $2–10 million each, with annual service contracts of 5–10% of purchase price. Supplier-driven upgrades can force multimillion-euro capital expenditures and months of retraining, raising operational risk and capex volatility for Nanogate.

Energy and Utility Dependency

Operating Nanogate’s cleanrooms and advanced plants consumes large, steady power — in 2025 European industrial electricity averaged about €0.18–0.22/kWh, so energy is a material cost driver for chemical and plastic processing and squeezes margins.

Limited ability to switch suppliers or rapid onsite generation gives utilities indirect bargaining power; 60–80% uptime dependency raises risk.

To counter price swings Nanogate must invest in efficiency and onsite renewables—CAPEX payback often 3–7 years based on current €/kWh levels.

Intellectual Property and Licensing Partners

Specialized surface additives and processes often rely on third-party patents; patent holders can impose licensing fees or restrict tech transfer, raising supplier power. Techniplas must invest in internal R&D—it spent €24m on R&D in 2024—to reduce dependency and protect margins. Renegotiating licenses or developing alternatives can take 12–36 months and cost millions, delaying product launches. This creates a steady risk to time-to-market and cost control.

- Patent fees raise COGS and limit margins

- €24m R&D in 2024 lowers external reliance

- Alternatives take 12–36 months, multi‑million cost

- License terms can block or slow technology transfer

Labor Market for Specialized Scientists

The supply of specialized material scientists and nanotech experts holds high bargaining power for Nanogate, as global demand in automotive and aerospace rose ~8% CAGR 2019–2024, driving competition for talent.

Techniplas must match market pay—median materials scientist salary €75k–€95k in Germany 2024—and offer strong R&D settings to retain staff; scarcity lets employees push for higher pay and benefits, pressuring operational budgets.

- High bargaining power due to scarcity

- 8% CAGR demand (2019–2024)

- Median Germany salary €75k–€95k (2024)

- Increases operational payroll pressure

Supplier concentration risks: 10–20% input swings, €m capex; Techniplas spent €24m R&D

Suppliers hold strong bargaining power due to concentrated specialty-chemical and thin-film equipment markets, patent licensing and energy dependence, making Nanogate vulnerable to 10–20% input-price swings and multi‑million capex for mandatory upgrades; Techniplas spent €24m on R&D in 2024 to reduce this risk.

| Metric | 2024/25 |

|---|---|

| Top-5 share specialty monomers | 60–70% |

| Equipment unit cost | €2–10m |

| Service contract | 5–10% p.a. |

| EU industrial power | €0.18–0.22/kWh |

| Techniplas R&D | €24m (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Nanogate that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic implications for pricing and profitability.

One-sheet Porter's Five Forces for Nanogate—clear force ratings and concise insights to speed strategic decisions and communicate risk to stakeholders.

Customers Bargaining Power

Concentration of Automotive OEMs

The customer base for high-performance plastic components is dominated by a few global OEMs (Toyota, Volkswagen, Stellantis, Hyundai-Kia), which in 2024 accounted for roughly 45% of global light-vehicle production, giving them strong bargaining power.

These OEMs place platform-level orders in volumes often exceeding millions of units, pressuring suppliers for annual price reductions of 1–3% and continuous efficiency gains.

Losing one major OEM contract can cut a supplier’s revenue by 20–40% depending on portfolio concentration, so Nanogate must prioritize cost competitiveness and customer retention.

Strict Quality and Sustainability Standards

Customers in aerospace and industrial sectors enforce ultra-high quality and sustainability rules; 2024 audits show 78% of OEMs require ISO 14001 plus supplier-specific lifecycle CO2 targets under 2030 roadmaps.

Buyers can demand exact material mixes and processes to hit their green targets, so Techniplas must adapt specs or lose contracts; requalification can cost €0.5–2.5M per program.

Techniplas often absorbs compliance costs to stay approved; failure to meet specs lets buyers switch to rivals with lower supplier nonconformance rates (industry median 0.6% in 2024).

Low Switching Costs for Standardized Components

Low switching costs for standardized plastic components make buyers price-sensitive; for example, procurement teams often solicit bids from 5–10 suppliers, cutting average margins to single digits in commodity lines. Large OEMs can pivot between suppliers for non-proprietary parts, pressuring prices and pushing Techniplas to invest in differentiation. In 2024 the global precision plastics market grew 3.8% but commodity prices compressed gross margins by ~120–250 bps.

Integration of Procurement Platforms

Large industrial buyers use digital procurement platforms that boost price transparency and let them compare specs and prices in real time, strengthening their negotiation leverage.

Reverse auctions and global sourcing data push surface-finishing prices down; in 2024 reverse-auction participation rose ~18% in EU heavy industry procurement, cutting awarded prices 6–12% on average.

This digital pressure forces Techniplas to sharpen its value proposition and hit tight cost targets—companies with disciplined cost-to-serve models cut COGS by ~4–7% vs peers.

- Real-time price/spec comparison increases buyer leverage

- Reverse auctions reduce awarded prices 6–12% (2024 data)

- Global sourcing expands supplier competition

- Techniplas must improve value messaging and reduce COGS 4–7%

Potential for Backward Integration

Large OEMs with R&D budgets (eg, Volkswagen Group 2024 R&D €18.4bn) could internalize nanocoatings if supplier prices rise, capping Techniplas pricing power.

If an OEM believes in-house tech can match nanotechnology outcomes, independent suppliers lose core value—seen where in-house projects cut supplier spend by 10–25%.

To prevent this, Techniplas must keep a cost-prohibitive-to-replicate tech lead—eg, proprietary processes reducing defect rates by >30%—so backward integration stays unattractive.

- Large OEM R&D scale enables insourcing threat

- Insourcing can cut supplier spend 10–25%

- Price ceiling set by backward integration risk

- Maintain costly-to-replicate tech (eg, >30% defect reduction)

OEM dominance squeezes suppliers: price cuts, ESG demands, insourcing risk

Major OEMs (Toyota, VW, Stellantis, Hyundai-Kia) hold strong leverage—45% of light-vehicle output in 2024—forcing 1–3% annual price cuts; losing one OEM can cut supplier revenue 20–40%. Buyers demand ISO14001 plus CO2 targets (78% of OEMs, 2024) and run reverse auctions (EU participation +18% in 2024, prices −6–12%), making margins single-digit and raising insourcing risk (OEM R&D e.g., VW €18.4bn, 2024).

| Metric | 2024 Value |

|---|---|

| OEM share of LV production | 45% |

| OEMs requiring ISO14001 + CO2 targets | 78% |

| Reverse-auction EU participation change | +18% |

| Price reduction from reverse auctions | −6–12% |

| OEM R&D (Volkswagen) | €18.4bn |

Preview Before You Purchase

Nanogate Porter's Five Forces Analysis

This preview displays the actual Nanogate Porter's Five Forces analysis you’ll receive upon purchase—fully written, formatted, and ready for immediate download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Nanogate faces moderate supplier power due to specialized inputs, while buyer concentration and price sensitivity heighten competitive pressure; substitutes and tech disruption pose emerging threats, and barriers to entry are medium given capital and know-how requirements.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nanogate’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Chemical and Raw Material Providers

The production of high-performance surfaces depends on niche chemical compounds and high-purity polymers from a small set of global suppliers, giving them strong leverage over Techniplas Nano Tec SE; about 60–70% of specialty monomers supply is concentrated among five firms as of 2025. Disruptions or a 10–20% price swing in these inputs would raise manufacturing costs materially, so Techniplas must keep strategic long-term contracts and dual sourcing to secure quality and availability.

Technological Equipment Manufacturers

The small pool of high-tech firms that make thin-film and nanotech production equipment gives suppliers strong bargaining power; global semiconductor tool makers saw 18% revenue growth in 2024, concentrating R&D and pricing power. Techniplas relies on these vendors for support and hardware advances, and typical equipment units cost $2–10 million each, with annual service contracts of 5–10% of purchase price. Supplier-driven upgrades can force multimillion-euro capital expenditures and months of retraining, raising operational risk and capex volatility for Nanogate.

Energy and Utility Dependency

Operating Nanogate’s cleanrooms and advanced plants consumes large, steady power — in 2025 European industrial electricity averaged about €0.18–0.22/kWh, so energy is a material cost driver for chemical and plastic processing and squeezes margins.

Limited ability to switch suppliers or rapid onsite generation gives utilities indirect bargaining power; 60–80% uptime dependency raises risk.

To counter price swings Nanogate must invest in efficiency and onsite renewables—CAPEX payback often 3–7 years based on current €/kWh levels.

Intellectual Property and Licensing Partners

Specialized surface additives and processes often rely on third-party patents; patent holders can impose licensing fees or restrict tech transfer, raising supplier power. Techniplas must invest in internal R&D—it spent €24m on R&D in 2024—to reduce dependency and protect margins. Renegotiating licenses or developing alternatives can take 12–36 months and cost millions, delaying product launches. This creates a steady risk to time-to-market and cost control.

- Patent fees raise COGS and limit margins

- €24m R&D in 2024 lowers external reliance

- Alternatives take 12–36 months, multi‑million cost

- License terms can block or slow technology transfer

Labor Market for Specialized Scientists

The supply of specialized material scientists and nanotech experts holds high bargaining power for Nanogate, as global demand in automotive and aerospace rose ~8% CAGR 2019–2024, driving competition for talent.

Techniplas must match market pay—median materials scientist salary €75k–€95k in Germany 2024—and offer strong R&D settings to retain staff; scarcity lets employees push for higher pay and benefits, pressuring operational budgets.

- High bargaining power due to scarcity

- 8% CAGR demand (2019–2024)

- Median Germany salary €75k–€95k (2024)

- Increases operational payroll pressure

Supplier concentration risks: 10–20% input swings, €m capex; Techniplas spent €24m R&D

Suppliers hold strong bargaining power due to concentrated specialty-chemical and thin-film equipment markets, patent licensing and energy dependence, making Nanogate vulnerable to 10–20% input-price swings and multi‑million capex for mandatory upgrades; Techniplas spent €24m on R&D in 2024 to reduce this risk.

| Metric | 2024/25 |

|---|---|

| Top-5 share specialty monomers | 60–70% |

| Equipment unit cost | €2–10m |

| Service contract | 5–10% p.a. |

| EU industrial power | €0.18–0.22/kWh |

| Techniplas R&D | €24m (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Nanogate that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic implications for pricing and profitability.

One-sheet Porter's Five Forces for Nanogate—clear force ratings and concise insights to speed strategic decisions and communicate risk to stakeholders.

Customers Bargaining Power

Concentration of Automotive OEMs

The customer base for high-performance plastic components is dominated by a few global OEMs (Toyota, Volkswagen, Stellantis, Hyundai-Kia), which in 2024 accounted for roughly 45% of global light-vehicle production, giving them strong bargaining power.

These OEMs place platform-level orders in volumes often exceeding millions of units, pressuring suppliers for annual price reductions of 1–3% and continuous efficiency gains.

Losing one major OEM contract can cut a supplier’s revenue by 20–40% depending on portfolio concentration, so Nanogate must prioritize cost competitiveness and customer retention.

Strict Quality and Sustainability Standards

Customers in aerospace and industrial sectors enforce ultra-high quality and sustainability rules; 2024 audits show 78% of OEMs require ISO 14001 plus supplier-specific lifecycle CO2 targets under 2030 roadmaps.

Buyers can demand exact material mixes and processes to hit their green targets, so Techniplas must adapt specs or lose contracts; requalification can cost €0.5–2.5M per program.

Techniplas often absorbs compliance costs to stay approved; failure to meet specs lets buyers switch to rivals with lower supplier nonconformance rates (industry median 0.6% in 2024).

Low Switching Costs for Standardized Components

Low switching costs for standardized plastic components make buyers price-sensitive; for example, procurement teams often solicit bids from 5–10 suppliers, cutting average margins to single digits in commodity lines. Large OEMs can pivot between suppliers for non-proprietary parts, pressuring prices and pushing Techniplas to invest in differentiation. In 2024 the global precision plastics market grew 3.8% but commodity prices compressed gross margins by ~120–250 bps.

Integration of Procurement Platforms

Large industrial buyers use digital procurement platforms that boost price transparency and let them compare specs and prices in real time, strengthening their negotiation leverage.

Reverse auctions and global sourcing data push surface-finishing prices down; in 2024 reverse-auction participation rose ~18% in EU heavy industry procurement, cutting awarded prices 6–12% on average.

This digital pressure forces Techniplas to sharpen its value proposition and hit tight cost targets—companies with disciplined cost-to-serve models cut COGS by ~4–7% vs peers.

- Real-time price/spec comparison increases buyer leverage

- Reverse auctions reduce awarded prices 6–12% (2024 data)

- Global sourcing expands supplier competition

- Techniplas must improve value messaging and reduce COGS 4–7%

Potential for Backward Integration

Large OEMs with R&D budgets (eg, Volkswagen Group 2024 R&D €18.4bn) could internalize nanocoatings if supplier prices rise, capping Techniplas pricing power.

If an OEM believes in-house tech can match nanotechnology outcomes, independent suppliers lose core value—seen where in-house projects cut supplier spend by 10–25%.

To prevent this, Techniplas must keep a cost-prohibitive-to-replicate tech lead—eg, proprietary processes reducing defect rates by >30%—so backward integration stays unattractive.

- Large OEM R&D scale enables insourcing threat

- Insourcing can cut supplier spend 10–25%

- Price ceiling set by backward integration risk

- Maintain costly-to-replicate tech (eg, >30% defect reduction)

OEM dominance squeezes suppliers: price cuts, ESG demands, insourcing risk

Major OEMs (Toyota, VW, Stellantis, Hyundai-Kia) hold strong leverage—45% of light-vehicle output in 2024—forcing 1–3% annual price cuts; losing one OEM can cut supplier revenue 20–40%. Buyers demand ISO14001 plus CO2 targets (78% of OEMs, 2024) and run reverse auctions (EU participation +18% in 2024, prices −6–12%), making margins single-digit and raising insourcing risk (OEM R&D e.g., VW €18.4bn, 2024).

| Metric | 2024 Value |

|---|---|

| OEM share of LV production | 45% |

| OEMs requiring ISO14001 + CO2 targets | 78% |

| Reverse-auction EU participation change | +18% |

| Price reduction from reverse auctions | −6–12% |

| OEM R&D (Volkswagen) | €18.4bn |

Preview Before You Purchase

Nanogate Porter's Five Forces Analysis

This preview displays the actual Nanogate Porter's Five Forces analysis you’ll receive upon purchase—fully written, formatted, and ready for immediate download with no placeholders or samples.