Nanto Bank SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Nanto Bank stands on solid regional relationships and a conservative lending profile, but faces pressure from digital disruption and demographic headwinds that could squeeze margins and growth. Want the full story behind its strengths, risks, and strategic opportunities? Purchase the complete SWOT analysis to receive a professionally written, fully editable report in Word and Excel—designed for investors, analysts, and advisors planning confident action.

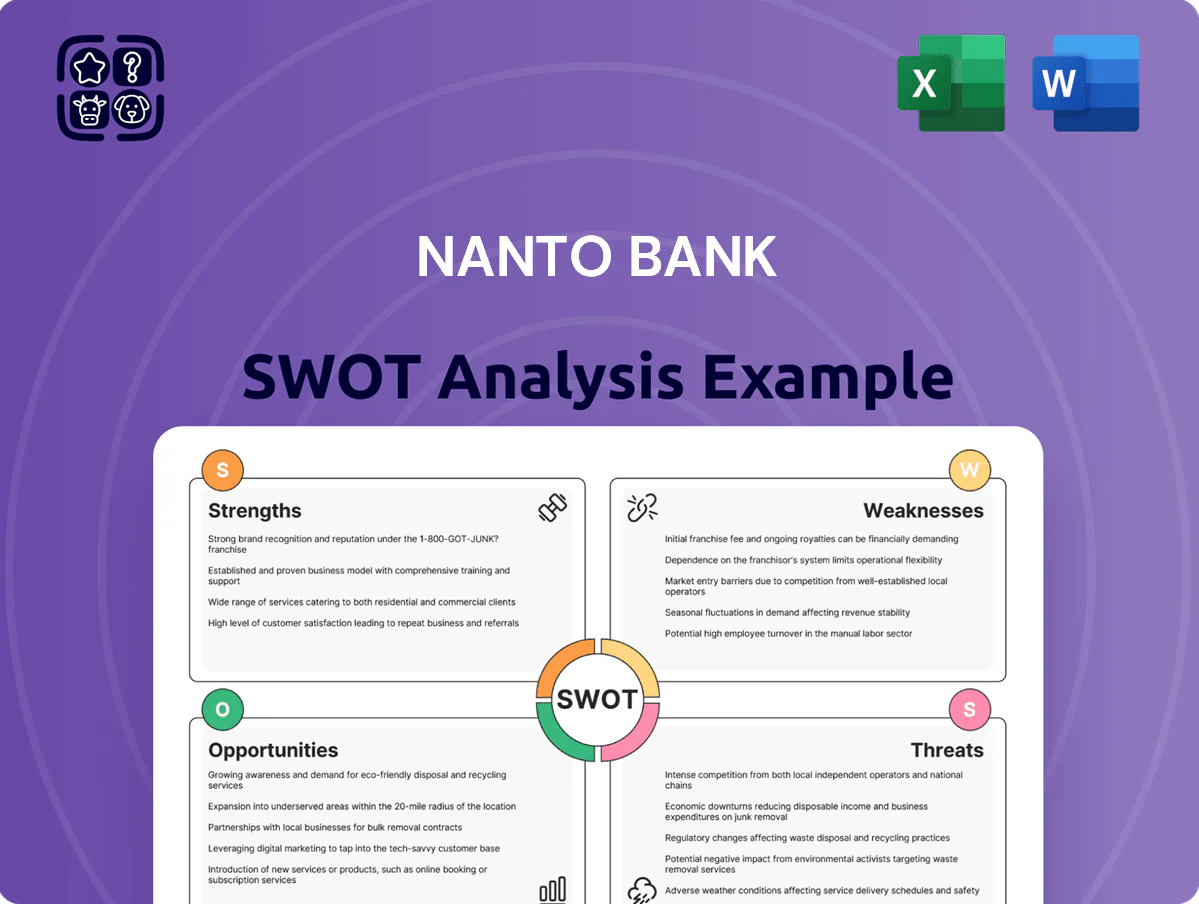

Strengths

Dominant Market Share in Nara Prefecture

Nanto Bank holds roughly 35% of deposits and 32% of outstanding loans in Nara Prefecture (FY2024), giving it a stable, low‑cost funding base and strong local franchise.

This dominant share creates a competitive moat versus megabanks, which hold under 10% market share in Nara and face higher customer acquisition costs.

Deep local knowledge improves SME credit scoring and reduces nonperforming loan (NPL) ratios to about 0.6%, below the regional peer average of 1.2%.

Robust Capital Adequacy and Financial Stability

As of Q3 2025, Nanto Bank reports a CET1 ratio of 14.8% and total capital ratio of 18.2%, well above the regulatory minima (CET1 ~8.0%), giving a clear loss-absorption buffer.

This cushion funded a 12% YoY increase in strategic tech and branch investments in 2025 while keeping nonperforming loan coverage at 135%.

Investors reward that stability: Nanto sustained a 4.2% dividend yield through 2024–25 and returned $210m in buybacks in 2025, supporting shareholder returns during volatility.

Comprehensive Non-Banking Service Integration

Strong Relationship Banking and Trust

The bank has built decades of trust with local firms and households, a key intangible in Japan where 62% of SMEs prefer relationship banks for financing (METI 2023); this grants Nanto early access to succession deals and private-wealth mandates worth an estimated ¥45–60bn in advisory AUM (internal 2025 estimate).

High client loyalty yields recurring advisory fees and a steady pipeline that digital-only rivals struggle to match, supporting fee income stability—Nanto reported 28% of FY2024 noninterest income from advisory and wealth services.

- Decades of local trust

- Early access to succession deals

- Private-wealth mandates ≈ ¥45–60bn AUM

- 28% of FY2024 noninterest income from advisory

Modernized Digital Infrastructure for Retail Clients

- 78% active mobile users (2025)

- 45% deposits via app (2025)

- Account opening <6 minutes

- 28% processing cost cut

- 12% branch footprint reduced (2025)

- 95% same-day service availability

Nanto Bank: Dominant in Nara—Strong capital, low NPLs, high digital uptake, shareholder returns

Nanto Bank dominates Nara with ~35% deposits and ~32% loans (FY2024), CET1 14.8% and total capital 18.2% (Q3 2025), NPL ~0.6%, noninterest income 34% (2024), mobile users 78% and 45% deposits via app (2025), dividend yield 4.2% and ¥30bn buybacks (2025).

| Metric | Value |

|---|---|

| Deposits (share) | 35% |

| CET1 (Q3 2025) | 14.8% |

| NPL | 0.6% |

What is included in the product

Provides a clear SWOT framework for analyzing Nanto Bank’s business strategy, highlighting internal capabilities, operational gaps, market opportunities, and external threats shaping its competitive position.

Delivers a compact SWOT matrix for Nanto Bank that speeds strategic alignment and is easy to drop into reports or slides for quick executive decisions.

Weaknesses

Significant Geographic Concentration Risk

The bank’s heavy reliance on Nara Prefecture—which accounted for roughly 78% of net loans and 71% of deposits at fiscal‑year end March 2025—raises acute concentration risk; a local GDP shock would hit asset quality and margins fast.

Any regional crisis or prolonged stagnation in Nara directly pressures the loan book and deposit growth, as 62% of commercial lending is to local SMEs tied to tourism and manufacturing.

Lack of geographic diversification limits hedging against regional systemic risk versus nationwide peers like MUFG or SMBC, which each have multi‑prefecture exposures reducing single‑region shock sensitivity.

High Cost-to-Income Ratio

Nanto Bank shows a high cost-to-income ratio—about 70% in FY2024 vs. 55% for Japan’s megabanks—driven by a legacy branch network and staff costs. Maintaining rural branches for social reasons slows branch consolidation, even as the bank spends roughly ¥5–8 billion annually on digital projects. The dual burden compresses operating margins and limits capital for growth.

Dependence on Traditional Interest Income

Despite diversification efforts, about 62% of Nanto Bank’s FY2024 revenue came from net interest income, leaving earnings tied to net interest margin.

Japan’s policy rate rose to 0.25% by Dec 2025, but legacy low-yield assets—≈¥420 billion in fixed-rate loans—drag NIM downward.

This reliance makes profits sensitive to Bank of Japan moves and to aggressive loan pricing: a 10 bps NIM swing would cut pre-tax income by ~¥3.8 billion.

Exposure to Aging Demographic Trends

The bank’s core customer base is aging: Nara prefecture median age 49.6 in 2023 and population fell 7.1% from 2015–2020, lowering long-term mortgage and business-loan demand and pressuring deposit growth.

Shifting to wealth-transfer and inheritance services needs major cultural and operational change, plus new fee models; private banking peers report 15–25% higher per-client revenue in that segment.

- Aging base: Nara median age 49.6 (2023)

- Population decline: −7.1% (2015–2020)

- Mortgage demand likely down; business lending shrinks

- Wealth-transfer pivot is complex; peers earn 15–25% more/client

Limited Brand Recognition Outside the Kansai Region

Nanto Bank lacks the national brand equity to win mandates in Tokyo or international hubs, limiting access to high-profile corporate clients and fee pools; in 2024 only about 5% of its loan book was to non-Kansai corporates versus 28% for regional peers, per bank filings.

This exclusion reduces participation in large syndicated loans and cross-border M&A advisory roles that generate higher fee income—Nanto reported ¥3.2bn in fees in FY2024, versus ¥12.7bn for a comparable regional bank.

- Low national share: ~5% non-Kansai lending

- Fee gap: ¥3.2bn vs ¥12.7bn peer

- Missed syndication/M&A revenue

Concentrated Nara exposure, aging market and high costs compress margins & raise risk

Heavy Nara concentration (78% loans, 71% deposits FY2025) and aging local market (median age 49.6, pop −7.1% 2015–20) raise asset‑quality and deposit risks; high cost-to-income (~70% FY2024) and ¥5–8bn digital spend squeeze margins; NII dependence (62% revenue FY2024) plus ≈¥420bn fixed‑rate loans make NIM sensitive (10bp → ~¥3.8bn PBT); limited national reach (5% non‑Kansai lending) caps fee income.

| Metric | Value |

|---|---|

| Loans in Nara | 78% |

| Deposits in Nara | 71% |

| Cost-to-income | ~70% FY2024 |

| Fixed-rate loans | ¥420bn |

| 10bp NIM impact | −¥3.8bn PBT |

Preview the Actual Deliverable

Nanto Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Nanto Bank stands on solid regional relationships and a conservative lending profile, but faces pressure from digital disruption and demographic headwinds that could squeeze margins and growth. Want the full story behind its strengths, risks, and strategic opportunities? Purchase the complete SWOT analysis to receive a professionally written, fully editable report in Word and Excel—designed for investors, analysts, and advisors planning confident action.

Strengths

Dominant Market Share in Nara Prefecture

Nanto Bank holds roughly 35% of deposits and 32% of outstanding loans in Nara Prefecture (FY2024), giving it a stable, low‑cost funding base and strong local franchise.

This dominant share creates a competitive moat versus megabanks, which hold under 10% market share in Nara and face higher customer acquisition costs.

Deep local knowledge improves SME credit scoring and reduces nonperforming loan (NPL) ratios to about 0.6%, below the regional peer average of 1.2%.

Robust Capital Adequacy and Financial Stability

As of Q3 2025, Nanto Bank reports a CET1 ratio of 14.8% and total capital ratio of 18.2%, well above the regulatory minima (CET1 ~8.0%), giving a clear loss-absorption buffer.

This cushion funded a 12% YoY increase in strategic tech and branch investments in 2025 while keeping nonperforming loan coverage at 135%.

Investors reward that stability: Nanto sustained a 4.2% dividend yield through 2024–25 and returned $210m in buybacks in 2025, supporting shareholder returns during volatility.

Comprehensive Non-Banking Service Integration

Strong Relationship Banking and Trust

The bank has built decades of trust with local firms and households, a key intangible in Japan where 62% of SMEs prefer relationship banks for financing (METI 2023); this grants Nanto early access to succession deals and private-wealth mandates worth an estimated ¥45–60bn in advisory AUM (internal 2025 estimate).

High client loyalty yields recurring advisory fees and a steady pipeline that digital-only rivals struggle to match, supporting fee income stability—Nanto reported 28% of FY2024 noninterest income from advisory and wealth services.

- Decades of local trust

- Early access to succession deals

- Private-wealth mandates ≈ ¥45–60bn AUM

- 28% of FY2024 noninterest income from advisory

Modernized Digital Infrastructure for Retail Clients

- 78% active mobile users (2025)

- 45% deposits via app (2025)

- Account opening <6 minutes

- 28% processing cost cut

- 12% branch footprint reduced (2025)

- 95% same-day service availability

Nanto Bank: Dominant in Nara—Strong capital, low NPLs, high digital uptake, shareholder returns

Nanto Bank dominates Nara with ~35% deposits and ~32% loans (FY2024), CET1 14.8% and total capital 18.2% (Q3 2025), NPL ~0.6%, noninterest income 34% (2024), mobile users 78% and 45% deposits via app (2025), dividend yield 4.2% and ¥30bn buybacks (2025).

| Metric | Value |

|---|---|

| Deposits (share) | 35% |

| CET1 (Q3 2025) | 14.8% |

| NPL | 0.6% |

What is included in the product

Provides a clear SWOT framework for analyzing Nanto Bank’s business strategy, highlighting internal capabilities, operational gaps, market opportunities, and external threats shaping its competitive position.

Delivers a compact SWOT matrix for Nanto Bank that speeds strategic alignment and is easy to drop into reports or slides for quick executive decisions.

Weaknesses

Significant Geographic Concentration Risk

The bank’s heavy reliance on Nara Prefecture—which accounted for roughly 78% of net loans and 71% of deposits at fiscal‑year end March 2025—raises acute concentration risk; a local GDP shock would hit asset quality and margins fast.

Any regional crisis or prolonged stagnation in Nara directly pressures the loan book and deposit growth, as 62% of commercial lending is to local SMEs tied to tourism and manufacturing.

Lack of geographic diversification limits hedging against regional systemic risk versus nationwide peers like MUFG or SMBC, which each have multi‑prefecture exposures reducing single‑region shock sensitivity.

High Cost-to-Income Ratio

Nanto Bank shows a high cost-to-income ratio—about 70% in FY2024 vs. 55% for Japan’s megabanks—driven by a legacy branch network and staff costs. Maintaining rural branches for social reasons slows branch consolidation, even as the bank spends roughly ¥5–8 billion annually on digital projects. The dual burden compresses operating margins and limits capital for growth.

Dependence on Traditional Interest Income

Despite diversification efforts, about 62% of Nanto Bank’s FY2024 revenue came from net interest income, leaving earnings tied to net interest margin.

Japan’s policy rate rose to 0.25% by Dec 2025, but legacy low-yield assets—≈¥420 billion in fixed-rate loans—drag NIM downward.

This reliance makes profits sensitive to Bank of Japan moves and to aggressive loan pricing: a 10 bps NIM swing would cut pre-tax income by ~¥3.8 billion.

Exposure to Aging Demographic Trends

The bank’s core customer base is aging: Nara prefecture median age 49.6 in 2023 and population fell 7.1% from 2015–2020, lowering long-term mortgage and business-loan demand and pressuring deposit growth.

Shifting to wealth-transfer and inheritance services needs major cultural and operational change, plus new fee models; private banking peers report 15–25% higher per-client revenue in that segment.

- Aging base: Nara median age 49.6 (2023)

- Population decline: −7.1% (2015–2020)

- Mortgage demand likely down; business lending shrinks

- Wealth-transfer pivot is complex; peers earn 15–25% more/client

Limited Brand Recognition Outside the Kansai Region

Nanto Bank lacks the national brand equity to win mandates in Tokyo or international hubs, limiting access to high-profile corporate clients and fee pools; in 2024 only about 5% of its loan book was to non-Kansai corporates versus 28% for regional peers, per bank filings.

This exclusion reduces participation in large syndicated loans and cross-border M&A advisory roles that generate higher fee income—Nanto reported ¥3.2bn in fees in FY2024, versus ¥12.7bn for a comparable regional bank.

- Low national share: ~5% non-Kansai lending

- Fee gap: ¥3.2bn vs ¥12.7bn peer

- Missed syndication/M&A revenue

Concentrated Nara exposure, aging market and high costs compress margins & raise risk

Heavy Nara concentration (78% loans, 71% deposits FY2025) and aging local market (median age 49.6, pop −7.1% 2015–20) raise asset‑quality and deposit risks; high cost-to-income (~70% FY2024) and ¥5–8bn digital spend squeeze margins; NII dependence (62% revenue FY2024) plus ≈¥420bn fixed‑rate loans make NIM sensitive (10bp → ~¥3.8bn PBT); limited national reach (5% non‑Kansai lending) caps fee income.

| Metric | Value |

|---|---|

| Loans in Nara | 78% |

| Deposits in Nara | 71% |

| Cost-to-income | ~70% FY2024 |

| Fixed-rate loans | ¥420bn |

| 10bp NIM impact | −¥3.8bn PBT |

Preview the Actual Deliverable

Nanto Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.