NAPEC PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic trends, and technological advances are shaping NAPEC’s strategic outlook—our concise PESTLE snapshot highlights key external forces and practical implications for investors and strategists; purchase the full analysis for the complete, editable report and actionable recommendations to inform your next move.

Political factors

Government Infrastructure Stimulus

Federal funding in Canada and the United States continues to prioritize grid modernization, with the US Inflation Reduction Act and IIJA directing over US$200 billion to energy infrastructure through 2026 and Canada committing CAD 20 billion to grid and clean energy projects; these mandates create a steady pipeline of long-term contracts for infrastructure providers like NRB. Policy shifts toward domestic energy independence—reflected in a projected 15% increase in T&D investment 2024–2028—further solidify demand for robust transmission and distribution networks.

Cross-Border Trade Relations

Trade agreements like USMCA enable cross-border movement of specialized labor and equipment crucial for NRB projects, with USMCA content rules supporting $1.2tn in 2023 US-Canada-Mexico trade; tariffs or protectionist moves—e.g., 2018-21 steel/aluminum tariffs that raised US import prices by ~25%—would materially raise capital costs for large utility projects; stable US-Canada ties reduce delays and lower logistics costs for North American energy builds.

Energy Transition Policy

Legislative pushes toward decarbonization require grid upgrades to integrate renewables; global investment in power grids reached about $430bn in 2024, with transmission spending up 12% year-on-year, signaling major capital needs.

Political Net Zero 2050 commitments are driving expanded substation capacity and high-voltage lines—IEA estimates cumulative transmission additions of ~1.5–2.0 million km by 2050 to meet targets.

NRB stands to benefit as utilities allocate capital to resilience; US utility capex for T&D hit $95bn in 2024, creating procurement and project pipelines where NRB can capture incremental revenue.

Public-Private Partnerships

The rise of P3 models for public lighting and traffic systems is unlocking revenue for contractors; global P3 investment in infrastructure reached about $200bn in 2024, with smart-city projects representing ~12% of that, boosting recurring service contracts.

Political backing for outsourcing municipal maintenance lets firms secure 10–20 year service agreements with indexed payments, improving cash flow visibility and reducing public capex burdens.

Performance-based incentives—often 5–15% of contract value—tie payments to uptime, energy savings and response times, aligning contractor profits with municipal efficiency targets.

- Global P3 infra: ~$200bn (2024)

- Smart-city share: ~12%

- Contract terms: 10–20 years

- Incentive share: 5–15% of contract value

Regulatory Oversight Stability

Regulatory Oversight Stability: Stable energy boards across the US, Canada and Mexico—covering markets that attracted over US$120 billion in energy infrastructure investment in 2024—create predictability for capital deployment; however, shifts in political leadership have led to median permit delays rising from 9 to 14 months in jurisdictions with regulatory turnover, slowing project approvals and environmental assessments.

Consistent policy frameworks are critical for NRB planning multi-year deployments, given that 78% of planned North American grid and renewables projects through 2026 require multi-jurisdictional permits.

- US$120B+ energy infrastructure investment in North America (2024)

- Median permit delays: 9 → 14 months with regulatory shifts

- 78% of projects through 2026 need multi-jurisdictional permits

Fed & Canada funding sparks US$95B T&D boom amid longer permits, rising P3 deals

Political support for grid modernization and decarbonization (US$200B+ federal US funding to 2026; CAD20B Canada) drives steady T&D demand; US utility T&D capex hit US$95B (2024). Trade stability (USMCA) lowers logistics risk while historical tariffs raised input costs ~25%. P3s and outsourcing expand multi‑year contracts (10–20y) with 5–15% performance incentives; permit delays rise 9→14 months with regulatory turnover.

| Metric | Value (2024/2025) |

|---|---|

| US federal energy funding | US$200B+ |

| Canada grid commits | CAD20B |

| US T&D capex | US$95B |

| P3 infra | ~US$200B |

| Permit delays (median) | 9 → 14 months |

What is included in the product

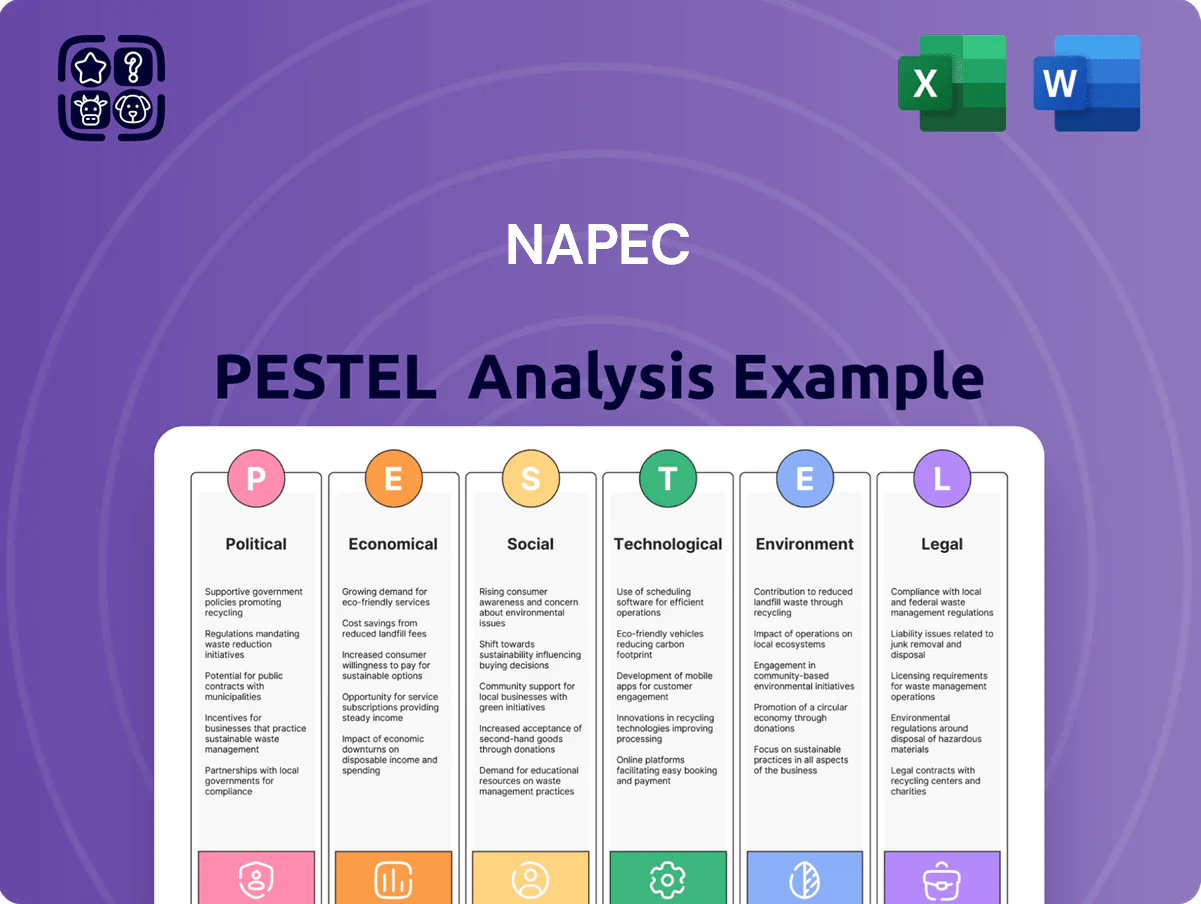

Explores how external macro-environmental factors uniquely affect the NAPEC across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

A concise, visually segmented NAPEC PESTLE summary that relieves meeting prep burden by offering an easily shareable, editable snapshot for presentations, planning sessions, and cross-team alignment.

Economic factors

Interest Rate Environment

As of late 2025, global policy rates stabilized after 2023–24 hikes, with US Fed funds near 5.25% and ECB deposit at 3.75%, lowering average corporate borrowing costs by ~120 bps vs peak; this reduces WACC for capital-intensive projects, spurring utilities to fast-track expansions and boosting NRB service demand potentially by 8–12% y/y. Conversely, sustained high rates continue to risk delays and compress margins on fixed-price contracts.

Labor Market Shortages

The scarcity of skilled electrical workers and specialized engineers is constraining construction capacity, with US Bureau of Labor Statistics data (2024) showing 7.4% vacancy rates in skilled trades and an estimated 18% shortfall for electrical engineers in key regions; wage inflation rose 5.1% YoY in 2024, forcing firms to boost compensation—NRB faces a 6–12% hike in labor costs and must factor these into bid pricing to preserve target margins.

Inflationary Pressure on Materials

Volatility in global commodity markets pushed copper up ~35% and aluminum ~22% from 2020–2023, raising NAPEC’s procurement costs for cables and transformers and increasing prices for specialized electrical components by double digits in 2024.

Persistent inflation (global CPI ~4.5% in 2024) forces stronger supply-chain hedging, just-in-time buffers, and escalation clauses in long-term service contracts to protect margins.

Fuel cost swings—diesel averaging $1.10–1.35/L in 2024 across key markets—increased fleet OPEX by an estimated 8–12%, stressing maintenance budgets and routing efficiency.

Utility Capital Expenditure Trends

Utility CAPEX budgets drive contractor workloads; major North American utilities planned combined transmission and distribution CAPEX of about $150–$170 billion annually in 2024–2025, underpinning multi-year programs for grid expansion and resilience.

Regional GDP growth and a projected 1.2–1.8% rise in electricity demand per annum in some U.S. and Canadian markets through 2026 are prompting investments in capacity, smart grid and reliability upgrades.

NRB performance tracks these investment cycles closely: revenue and backlog for infrastructure contractors typically rise during utility program ramp-ups and decelerate as spend plateaus or shifts to O&M.

- 2024–25 North American utility CAPEX ~ $150–$170B/year

- Electricity demand growth ~1.2–1.8% p.a. to 2026

- NRB revenue/backlog correlated with utility program phases

Currency Exchange Volatility

Operating across Canada and the United States exposes NAPEC to CAD/USD volatility; the loonie moved between 0.72–0.79 USD in 2024, amplifying FX translation risks for revenues earned in USD but consolidated in CAD.

Revenue in USD must offset Canadian-denominated corporate costs, and a 5% adverse move in CAD/USD can cut reported EBIT by several percentage points for cross-border operators.

Active hedging—forwards, options, and natural hedges—reduces P&L volatility; by end-2024, 48% of mid-cap Canadian exporters reported using FX forwards.

- Exposure: CAD/USD swings (0.72–0.79 in 2024)

- Impact: ~5% move can materially reduce reported EBIT

- Mitigation: forwards, options, natural hedges; 48% adoption among mid-cap exporters (2024)

Lower rates boost utility CAPEX and demand, but labor, materials and FX squeeze margins

Lowered policy rates since 2024 trimmed average corporate borrowing costs ~120 bps vs peak, reducing WACC and encouraging utility CAPEX (~$150–$170B/year in 2024–25) that supports 1.2–1.8% p.a. electricity demand growth to 2026 and higher NRB revenues/backlog.

Labor shortages (7.4% skilled trade vacancies, 18% engineer shortfall) and commodity inflation (copper +35%, aluminum +22% since 2020) raised execution costs—labor +6–12% and materials double-digit in 2024—pressuring margins.

CAD/USD volatility (0.72–0.79 in 2024) creates translation risk; a 5% adverse move can cut reported EBIT materially—48% of mid-cap exporters used FX forwards in 2024 to hedge.

| Metric | Value |

|---|---|

| Utility CAPEX (NA 2024–25) | $150–$170B/yr |

| Electricity demand growth | 1.2–1.8% p.a. to 2026 |

| Labor vacancy/engineer shortfall (2024) | 7.4% / 18% |

| Copper / Aluminum change (2020–23) | +35% / +22% |

| CAD/USD range (2024) | 0.72–0.79 |

| Hedging adoption (mid-caps 2024) | 48% |

Full Version Awaits

NAPEC PESTLE Analysis

The preview shown here is the exact NAPEC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic trends, and technological advances are shaping NAPEC’s strategic outlook—our concise PESTLE snapshot highlights key external forces and practical implications for investors and strategists; purchase the full analysis for the complete, editable report and actionable recommendations to inform your next move.

Political factors

Government Infrastructure Stimulus

Federal funding in Canada and the United States continues to prioritize grid modernization, with the US Inflation Reduction Act and IIJA directing over US$200 billion to energy infrastructure through 2026 and Canada committing CAD 20 billion to grid and clean energy projects; these mandates create a steady pipeline of long-term contracts for infrastructure providers like NRB. Policy shifts toward domestic energy independence—reflected in a projected 15% increase in T&D investment 2024–2028—further solidify demand for robust transmission and distribution networks.

Cross-Border Trade Relations

Trade agreements like USMCA enable cross-border movement of specialized labor and equipment crucial for NRB projects, with USMCA content rules supporting $1.2tn in 2023 US-Canada-Mexico trade; tariffs or protectionist moves—e.g., 2018-21 steel/aluminum tariffs that raised US import prices by ~25%—would materially raise capital costs for large utility projects; stable US-Canada ties reduce delays and lower logistics costs for North American energy builds.

Energy Transition Policy

Legislative pushes toward decarbonization require grid upgrades to integrate renewables; global investment in power grids reached about $430bn in 2024, with transmission spending up 12% year-on-year, signaling major capital needs.

Political Net Zero 2050 commitments are driving expanded substation capacity and high-voltage lines—IEA estimates cumulative transmission additions of ~1.5–2.0 million km by 2050 to meet targets.

NRB stands to benefit as utilities allocate capital to resilience; US utility capex for T&D hit $95bn in 2024, creating procurement and project pipelines where NRB can capture incremental revenue.

Public-Private Partnerships

The rise of P3 models for public lighting and traffic systems is unlocking revenue for contractors; global P3 investment in infrastructure reached about $200bn in 2024, with smart-city projects representing ~12% of that, boosting recurring service contracts.

Political backing for outsourcing municipal maintenance lets firms secure 10–20 year service agreements with indexed payments, improving cash flow visibility and reducing public capex burdens.

Performance-based incentives—often 5–15% of contract value—tie payments to uptime, energy savings and response times, aligning contractor profits with municipal efficiency targets.

- Global P3 infra: ~$200bn (2024)

- Smart-city share: ~12%

- Contract terms: 10–20 years

- Incentive share: 5–15% of contract value

Regulatory Oversight Stability

Regulatory Oversight Stability: Stable energy boards across the US, Canada and Mexico—covering markets that attracted over US$120 billion in energy infrastructure investment in 2024—create predictability for capital deployment; however, shifts in political leadership have led to median permit delays rising from 9 to 14 months in jurisdictions with regulatory turnover, slowing project approvals and environmental assessments.

Consistent policy frameworks are critical for NRB planning multi-year deployments, given that 78% of planned North American grid and renewables projects through 2026 require multi-jurisdictional permits.

- US$120B+ energy infrastructure investment in North America (2024)

- Median permit delays: 9 → 14 months with regulatory shifts

- 78% of projects through 2026 need multi-jurisdictional permits

Fed & Canada funding sparks US$95B T&D boom amid longer permits, rising P3 deals

Political support for grid modernization and decarbonization (US$200B+ federal US funding to 2026; CAD20B Canada) drives steady T&D demand; US utility T&D capex hit US$95B (2024). Trade stability (USMCA) lowers logistics risk while historical tariffs raised input costs ~25%. P3s and outsourcing expand multi‑year contracts (10–20y) with 5–15% performance incentives; permit delays rise 9→14 months with regulatory turnover.

| Metric | Value (2024/2025) |

|---|---|

| US federal energy funding | US$200B+ |

| Canada grid commits | CAD20B |

| US T&D capex | US$95B |

| P3 infra | ~US$200B |

| Permit delays (median) | 9 → 14 months |

What is included in the product

Explores how external macro-environmental factors uniquely affect the NAPEC across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

A concise, visually segmented NAPEC PESTLE summary that relieves meeting prep burden by offering an easily shareable, editable snapshot for presentations, planning sessions, and cross-team alignment.

Economic factors

Interest Rate Environment

As of late 2025, global policy rates stabilized after 2023–24 hikes, with US Fed funds near 5.25% and ECB deposit at 3.75%, lowering average corporate borrowing costs by ~120 bps vs peak; this reduces WACC for capital-intensive projects, spurring utilities to fast-track expansions and boosting NRB service demand potentially by 8–12% y/y. Conversely, sustained high rates continue to risk delays and compress margins on fixed-price contracts.

Labor Market Shortages

The scarcity of skilled electrical workers and specialized engineers is constraining construction capacity, with US Bureau of Labor Statistics data (2024) showing 7.4% vacancy rates in skilled trades and an estimated 18% shortfall for electrical engineers in key regions; wage inflation rose 5.1% YoY in 2024, forcing firms to boost compensation—NRB faces a 6–12% hike in labor costs and must factor these into bid pricing to preserve target margins.

Inflationary Pressure on Materials

Volatility in global commodity markets pushed copper up ~35% and aluminum ~22% from 2020–2023, raising NAPEC’s procurement costs for cables and transformers and increasing prices for specialized electrical components by double digits in 2024.

Persistent inflation (global CPI ~4.5% in 2024) forces stronger supply-chain hedging, just-in-time buffers, and escalation clauses in long-term service contracts to protect margins.

Fuel cost swings—diesel averaging $1.10–1.35/L in 2024 across key markets—increased fleet OPEX by an estimated 8–12%, stressing maintenance budgets and routing efficiency.

Utility Capital Expenditure Trends

Utility CAPEX budgets drive contractor workloads; major North American utilities planned combined transmission and distribution CAPEX of about $150–$170 billion annually in 2024–2025, underpinning multi-year programs for grid expansion and resilience.

Regional GDP growth and a projected 1.2–1.8% rise in electricity demand per annum in some U.S. and Canadian markets through 2026 are prompting investments in capacity, smart grid and reliability upgrades.

NRB performance tracks these investment cycles closely: revenue and backlog for infrastructure contractors typically rise during utility program ramp-ups and decelerate as spend plateaus or shifts to O&M.

- 2024–25 North American utility CAPEX ~ $150–$170B/year

- Electricity demand growth ~1.2–1.8% p.a. to 2026

- NRB revenue/backlog correlated with utility program phases

Currency Exchange Volatility

Operating across Canada and the United States exposes NAPEC to CAD/USD volatility; the loonie moved between 0.72–0.79 USD in 2024, amplifying FX translation risks for revenues earned in USD but consolidated in CAD.

Revenue in USD must offset Canadian-denominated corporate costs, and a 5% adverse move in CAD/USD can cut reported EBIT by several percentage points for cross-border operators.

Active hedging—forwards, options, and natural hedges—reduces P&L volatility; by end-2024, 48% of mid-cap Canadian exporters reported using FX forwards.

- Exposure: CAD/USD swings (0.72–0.79 in 2024)

- Impact: ~5% move can materially reduce reported EBIT

- Mitigation: forwards, options, natural hedges; 48% adoption among mid-cap exporters (2024)

Lower rates boost utility CAPEX and demand, but labor, materials and FX squeeze margins

Lowered policy rates since 2024 trimmed average corporate borrowing costs ~120 bps vs peak, reducing WACC and encouraging utility CAPEX (~$150–$170B/year in 2024–25) that supports 1.2–1.8% p.a. electricity demand growth to 2026 and higher NRB revenues/backlog.

Labor shortages (7.4% skilled trade vacancies, 18% engineer shortfall) and commodity inflation (copper +35%, aluminum +22% since 2020) raised execution costs—labor +6–12% and materials double-digit in 2024—pressuring margins.

CAD/USD volatility (0.72–0.79 in 2024) creates translation risk; a 5% adverse move can cut reported EBIT materially—48% of mid-cap exporters used FX forwards in 2024 to hedge.

| Metric | Value |

|---|---|

| Utility CAPEX (NA 2024–25) | $150–$170B/yr |

| Electricity demand growth | 1.2–1.8% p.a. to 2026 |

| Labor vacancy/engineer shortfall (2024) | 7.4% / 18% |

| Copper / Aluminum change (2020–23) | +35% / +22% |

| CAD/USD range (2024) | 0.72–0.79 |

| Hedging adoption (mid-caps 2024) | 48% |

Full Version Awaits

NAPEC PESTLE Analysis

The preview shown here is the exact NAPEC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.