North American Title Co. Porter's Five Forces Analysis

Don't Miss the Bigger Picture

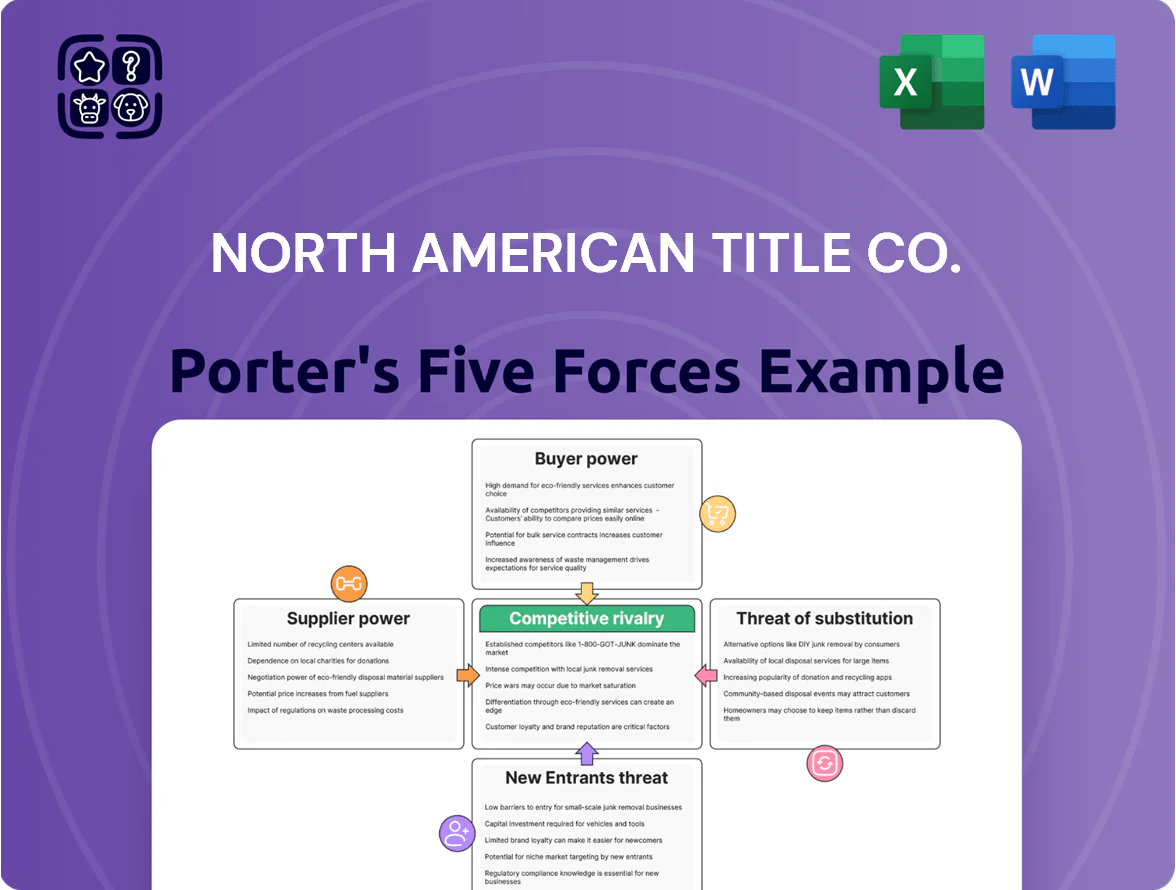

Suppliers Bargaining Power

Specialized Real Estate Data Providers

Title insurers like North American Title Co. depend on third-party aggregators for property records, tax rolls, and lien history; these data costs account for roughly 3–5% of underwriting expense lines for mid‑size underwriters in 2024–25.

By late 2025, five major providers control ~70% of U.S. parcel and lien datasets, boosting pricing power and annual subscription increases of 6–12%, pressuring margins.

NATIC must keep subscriptions to ensure search accuracy and avoid a 20–40% rise in manual search time and related fraud risk.

Independent Agency Distribution Networks

About 70% of US title premiums are sold via independent agencies, so these agents act as suppliers with strong leverage over North American Title Co (NATIC) because they can shift business to other underwriters; in 2024 NATIC reported agency-sourced premiums near $1.2bn, making competitive commission splits (often 40–60% for escrow/title combos) and investments in agent tech—API integrations, e-recording, and portal uptime above 99.5%—critical to retention.

Reinsurance Market Volatility

Title insurers like North American Title Co. (NATIC) use reinsurance to limit exposure on large commercial files; by late 2025 global reinsurers tightened capacity after 2023–24 catastrophe losses, raising average reinsurance premiums ~15–25% and reducing offered limits.

Those higher premiums feed into NATIC’s expense base—for example a 20% reinsurance cost uptick on high-value deals can cut underwriting margin by several hundred basis points on affected books.

Reduced reinsurance availability also forces retention of larger net exposures, increasing volatility in NATIC’s loss ratio and pressuring capital and pricing flexibility.

Legal and Underwriting Talent

The title industry needs specialized legal pros and senior underwriters to spot complex defects; median US title examiner pay rose 8.4% to about $83,000 in 2024, tightening supply.

Shortage of skilled financial-services labor has pushed demands for higher pay and benefits—turnover for specialty underwriting roles hit ~18% in 2024, raising recruiting costs. NATIC must boost retention spending to protect exam quality and limit claim risk.

- Median title examiner pay ≈ $83,000 (2024)

- Pay growth +8.4% YoY (2023–24)

- Specialty underwriting turnover ~18% (2024)

- Retention investment needed to reduce claim exposure

Cybersecurity and Tech Infrastructure Providers

As closings go digital, NATIC depends heavily on cloud and cybersecurity vendors; Gartner reported cloud security spending in North America rose 18% in 2024 to $28.6B, raising supplier leverage.

These providers protect mortgage data and uptime; a 24-hour outage can cost lenders millions and erode trust, so vendor disruptions or price hikes directly hit NATIC’s margins and reputation.

- 2024 cloud security spend NA: $28.6B

- 18% year-over-year growth (Gartner 2024)

- Single-day outage losses: millions

Concentrated suppliers squeeze NATIC: rising data, reinsurer, agency, labor costs

Suppliers (data vendors, agencies, reinsurers, skilled examiners, cloud/security firms) exert strong bargaining power over NATIC via concentrated data providers (~5 firms = ~70% market, 6–12% annual price hikes), agency channel leverage (agency-sourced premiums ~$1.2bn, 40–60% commission ranges), reinsurance cost rises (+15–25% by 2025), and rising labor/pay (median examiner pay $83k, +8.4% YoY).

| Supplier | Key stat (2024–25) |

|---|---|

| Data vendors | 5 firms ≈70% market; +6–12% prices |

| Agencies | $1.2bn agency premiums; 40–60% commissions |

| Reinsurers | +15–25% premiums (2023–25) |

| Labor | Examiner pay $83k; +8.4% YoY |

| Cloud/security | NA spend $28.6B; +18% YoY |

What is included in the product

Tailored exclusively for North American Title Co., this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier leverage, entry barriers, substitute risks, and disruptive threats shaping the company’s pricing power and profitability.

A concise, one-sheet Porter’s Five Forces for North American Title Co.—quickly highlights competitive pressures and regulatory risks to speed strategic decisions.

Customers Bargaining Power

Institutional Lender Requirements

Mortgage lenders drive roughly 85% of US title insurance demand because they require policies to protect real-estate collateral; in 2024 mortgage originations were ~$2.5 trillion, anchoring title volume. Large national banks set tight tech and compliance standards—APIs, ALTA Best Practices, and KYC/AML checks—forcing title firms to invest millions in integration; failing to meet specs can drop NATIC from approved provider lists and cost substantial referral revenue.

Real Estate Agent Influence

Real estate agents in U.S. residential deals often steer clients: 65% of buyers use an agent referral for title services, concentrating premium dollars toward recommended firms. This gives agents high bargaining power over North American Title Co. (NATIC), affecting deal volume and average revenue per order (U.S. title industry median revenue per residential closing ≈ $1,200 in 2024). NATIC must invest in fast turnaround, co-branded marketing, and agent retention programs to secure referrals.

Price Sensitivity of Homebuyers

Buyers still must buy title insurance, but 2025’s high-rate mortgage market makes every closing dollar matter: surveys show 62% of US homebuyers compare settlement fees and 48% choose providers on price, so North American Title Co. (NATIC) must keep non-regulated fees competitive—often trimming or bundling services—to protect volume and margin as shoppers hunt savings on $3,000–$7,000 total closing costs.

Corporate Real Estate Developers

- Top 20 developers ≈18% commercial title revenue (2024)

- 50+ annual deals → typical 10–25% discount

- Custom SLAs raise operational cost

- High-frequency deals increase negotiation leverage

Digital Integration Expectations

- 78% US borrowers prefer digital (2024)

- 35% faster processing with digital-first firms (2023)

- 62% willing to pay for speed (2024)

Customers Hold the Levers: Lenders, Agents & Buyers Squeeze NATIC on Price & Tech

Customers (lenders, agents, buyers, developers) exert high bargaining power over North American Title Co. (NATIC): lenders drive ~85% of demand tied to ~$2.5T originations (2024), agents influence ~65% of referrals, 62% of buyers shop fees, and top 20 developers made ~18% of commercial title revenue (2024), forcing discounts (10–25% for 50+ deals) and heavy tech/SLAs investment.

| Metric | Value |

|---|---|

| Lender share of demand | ~85% |

| Mortgage originations (2024) | $2.5T |

| Agent referral influence | ~65% |

| Buyers comparing fees | 62% |

| Top 20 developers revenue | ~18% |

| Discounts for 50+ deals | 10–25% |

Same Document Delivered

North American Title Co. Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for North American Title Co. you’ll receive after purchase—no placeholders or mockups, fully formatted and ready to use.

It’s the complete, final document: instant access to this same file upon payment, suitable for immediate download, presentation, or integration into your reports.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Suppliers Bargaining Power

Specialized Real Estate Data Providers

Title insurers like North American Title Co. depend on third-party aggregators for property records, tax rolls, and lien history; these data costs account for roughly 3–5% of underwriting expense lines for mid‑size underwriters in 2024–25.

By late 2025, five major providers control ~70% of U.S. parcel and lien datasets, boosting pricing power and annual subscription increases of 6–12%, pressuring margins.

NATIC must keep subscriptions to ensure search accuracy and avoid a 20–40% rise in manual search time and related fraud risk.

Independent Agency Distribution Networks

About 70% of US title premiums are sold via independent agencies, so these agents act as suppliers with strong leverage over North American Title Co (NATIC) because they can shift business to other underwriters; in 2024 NATIC reported agency-sourced premiums near $1.2bn, making competitive commission splits (often 40–60% for escrow/title combos) and investments in agent tech—API integrations, e-recording, and portal uptime above 99.5%—critical to retention.

Reinsurance Market Volatility

Title insurers like North American Title Co. (NATIC) use reinsurance to limit exposure on large commercial files; by late 2025 global reinsurers tightened capacity after 2023–24 catastrophe losses, raising average reinsurance premiums ~15–25% and reducing offered limits.

Those higher premiums feed into NATIC’s expense base—for example a 20% reinsurance cost uptick on high-value deals can cut underwriting margin by several hundred basis points on affected books.

Reduced reinsurance availability also forces retention of larger net exposures, increasing volatility in NATIC’s loss ratio and pressuring capital and pricing flexibility.

Legal and Underwriting Talent

The title industry needs specialized legal pros and senior underwriters to spot complex defects; median US title examiner pay rose 8.4% to about $83,000 in 2024, tightening supply.

Shortage of skilled financial-services labor has pushed demands for higher pay and benefits—turnover for specialty underwriting roles hit ~18% in 2024, raising recruiting costs. NATIC must boost retention spending to protect exam quality and limit claim risk.

- Median title examiner pay ≈ $83,000 (2024)

- Pay growth +8.4% YoY (2023–24)

- Specialty underwriting turnover ~18% (2024)

- Retention investment needed to reduce claim exposure

Cybersecurity and Tech Infrastructure Providers

As closings go digital, NATIC depends heavily on cloud and cybersecurity vendors; Gartner reported cloud security spending in North America rose 18% in 2024 to $28.6B, raising supplier leverage.

These providers protect mortgage data and uptime; a 24-hour outage can cost lenders millions and erode trust, so vendor disruptions or price hikes directly hit NATIC’s margins and reputation.

- 2024 cloud security spend NA: $28.6B

- 18% year-over-year growth (Gartner 2024)

- Single-day outage losses: millions

Concentrated suppliers squeeze NATIC: rising data, reinsurer, agency, labor costs

Suppliers (data vendors, agencies, reinsurers, skilled examiners, cloud/security firms) exert strong bargaining power over NATIC via concentrated data providers (~5 firms = ~70% market, 6–12% annual price hikes), agency channel leverage (agency-sourced premiums ~$1.2bn, 40–60% commission ranges), reinsurance cost rises (+15–25% by 2025), and rising labor/pay (median examiner pay $83k, +8.4% YoY).

| Supplier | Key stat (2024–25) |

|---|---|

| Data vendors | 5 firms ≈70% market; +6–12% prices |

| Agencies | $1.2bn agency premiums; 40–60% commissions |

| Reinsurers | +15–25% premiums (2023–25) |

| Labor | Examiner pay $83k; +8.4% YoY |

| Cloud/security | NA spend $28.6B; +18% YoY |

What is included in the product

Tailored exclusively for North American Title Co., this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier leverage, entry barriers, substitute risks, and disruptive threats shaping the company’s pricing power and profitability.

A concise, one-sheet Porter’s Five Forces for North American Title Co.—quickly highlights competitive pressures and regulatory risks to speed strategic decisions.

Customers Bargaining Power

Institutional Lender Requirements

Mortgage lenders drive roughly 85% of US title insurance demand because they require policies to protect real-estate collateral; in 2024 mortgage originations were ~$2.5 trillion, anchoring title volume. Large national banks set tight tech and compliance standards—APIs, ALTA Best Practices, and KYC/AML checks—forcing title firms to invest millions in integration; failing to meet specs can drop NATIC from approved provider lists and cost substantial referral revenue.

Real Estate Agent Influence

Real estate agents in U.S. residential deals often steer clients: 65% of buyers use an agent referral for title services, concentrating premium dollars toward recommended firms. This gives agents high bargaining power over North American Title Co. (NATIC), affecting deal volume and average revenue per order (U.S. title industry median revenue per residential closing ≈ $1,200 in 2024). NATIC must invest in fast turnaround, co-branded marketing, and agent retention programs to secure referrals.

Price Sensitivity of Homebuyers

Buyers still must buy title insurance, but 2025’s high-rate mortgage market makes every closing dollar matter: surveys show 62% of US homebuyers compare settlement fees and 48% choose providers on price, so North American Title Co. (NATIC) must keep non-regulated fees competitive—often trimming or bundling services—to protect volume and margin as shoppers hunt savings on $3,000–$7,000 total closing costs.

Corporate Real Estate Developers

- Top 20 developers ≈18% commercial title revenue (2024)

- 50+ annual deals → typical 10–25% discount

- Custom SLAs raise operational cost

- High-frequency deals increase negotiation leverage

Digital Integration Expectations

- 78% US borrowers prefer digital (2024)

- 35% faster processing with digital-first firms (2023)

- 62% willing to pay for speed (2024)

Customers Hold the Levers: Lenders, Agents & Buyers Squeeze NATIC on Price & Tech

Customers (lenders, agents, buyers, developers) exert high bargaining power over North American Title Co. (NATIC): lenders drive ~85% of demand tied to ~$2.5T originations (2024), agents influence ~65% of referrals, 62% of buyers shop fees, and top 20 developers made ~18% of commercial title revenue (2024), forcing discounts (10–25% for 50+ deals) and heavy tech/SLAs investment.

| Metric | Value |

|---|---|

| Lender share of demand | ~85% |

| Mortgage originations (2024) | $2.5T |

| Agent referral influence | ~65% |

| Buyers comparing fees | 62% |

| Top 20 developers revenue | ~18% |

| Discounts for 50+ deals | 10–25% |

Same Document Delivered

North American Title Co. Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for North American Title Co. you’ll receive after purchase—no placeholders or mockups, fully formatted and ready to use.

It’s the complete, final document: instant access to this same file upon payment, suitable for immediate download, presentation, or integration into your reports.