NBH Bank Business Model Canvas

NBH Bank: Download the Business Model Canvas to Reveal Strategy, Revenue & Partnerships

Unlock NBH Bank’s strategic playbook with our concise Business Model Canvas—discover how targeted customer segments, tailored value propositions, and smart partnerships drive revenue and competitive advantage; download the full Word/Excel canvas for a section-by-section breakdown, actionable insights, and ready-to-use slides for investor or strategy work.

Partnerships

Fintech and Technology Integration Partners

The bank partners with fintech leaders to power its 2NB digital platform and modern core, enabling seamless online and mobile banking that matches national rivals; 2024 metrics show digital users grew 38% YoY to 420,000 and mobile transactions rose 52% to $3.1B.

By integrating third-party APIs the bank adds specialized tools—automated accounting, real-hearted payment processing for commercial clients—reducing reconciliation time by 70% and cutting merchant onboarding from 12 to 3 days.

Federal and State Regulatory Agencies

Maintaining ties with the Federal Reserve, FDIC, and state banking departments keeps NBH Bank compliant and stable; in 2024 regulators enforced CET1 (common equity Tier 1) ratios around 9.5–10.5% for mid-sized banks, so regular oversight ensures capital and risk protocols meet those benchmarks. These partnerships also enable access to government-backed lending—like SBA loans and emergency facilities—and ongoing dialogue helps NBH retain multi-state charters amid shifting rules such as 2025 AML updates.

Strategic Referral Networks

The bank partners with 120+ local real estate agencies, 80 law firms, and 200 accounting practices across the Midwest and Mountain States to funnel high-quality leads into mortgage and commercial lending; referrals accounted for 38% of originations in 2025 ($1.2B of $3.2B total lending).

These professionals refer clients needing specialty lending or wealth management—areas where NBH’s regional footprint and 4.6% net charge-off rate vs. 1.1% peer median give it competitive credibility—boosting regional growth and community ties.

Third-Party Insurance and Investment Providers

NBH Bank partners with major insurance underwriters and global investment fund managers to offer wealth and protection products, avoiding product manufacturing overhead while expanding shelf-width for high-net-worth clients.

This ecosystem supports NBH’s one-stop goal; in 2025 partner-sourced assets under advice reached $4.2bn, covering 35 product lines and reducing product development costs by an estimated 18% versus in-house builds.

- Partner AUA $4.2bn

- 35 partner product lines

- 18% lower dev cost

Community and Economic Development Organizations

Partnerships with local chambers and economic development corporations steer NBH Bank toward $50–120M yearly small-business lending opportunities in its footprint and support CRA (Community Reinvestment Act) targets; this drives measurable community reinvestment and boosts regional project participation that raised local deposit growth by ~6% in 2024.

- Identify $50–120M SB loans/year

- Support CRA compliance and reporting

- Increase local deposits ~6% (2024)

- Enhance brand and long-term customer trust

NBH scales digital banking: $4.2B partner AUA, $1.2B partner loans, strong regulatory tie-ups

NBH leverages fintechs, reg agencies, 400+ professional referrers, insurers, and fund managers to scale digital banking, compliance, lending, and wealth; partner-sourced AUA hit $4.2bn in 2025 and partner-originated loans were $1.2bn (38% of $3.2bn). Regulatory ties secure CET1 targets ~9.5–10.5% and access to SBA/emergency facilities; local partnerships drive $50–120M SB lending/year and lifted deposits ~6% in 2024.

| Metric | 2024/2025 |

|---|---|

| Digital users | 420,000 (2024) |

| Mobile txns | $3.1B (2024) |

| Partner AUA | $4.2bn (2025) |

| Partner loans | $1.2bn (38%) (2025) |

| Local SB lending | $50–120M/yr |

| Deposit growth | ~6% (2024) |

What is included in the product

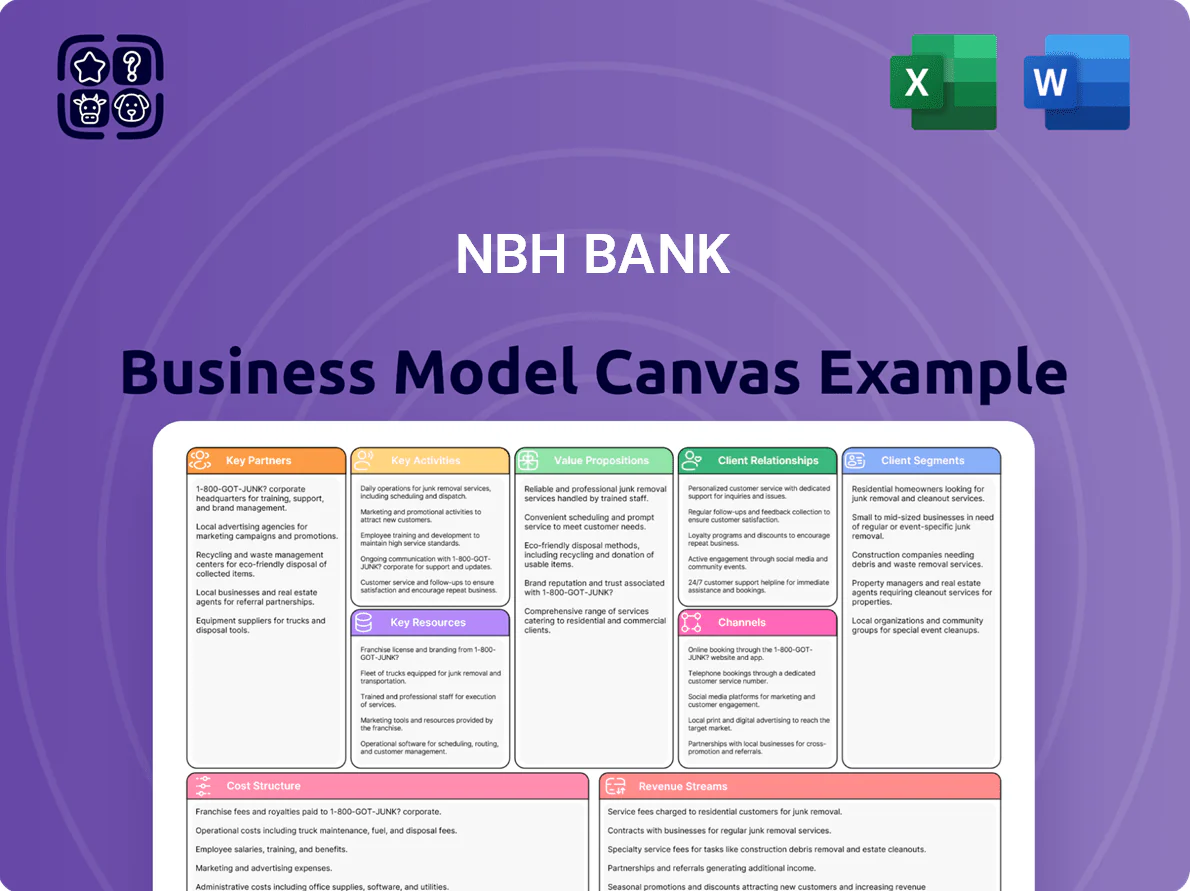

A concise, pre-written Business Model Canvas for NBH Bank outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and customer relationships—aligned to real-world banking operations and strategic plans.

High-level view of NBH Bank’s business model with editable cells to quickly pinpoint revenue drivers, cost centers, and risk exposures for faster strategic decisions.

Activities

Commercial and Personal Lending Operations

NBH Bank concentrates on originating, underwriting, and servicing a diverse loan book—commercial, industrial, and residential real estate—conducting rigorous credit analysis and stress testing; as of 2025 the bank’s loan portfolio stood at $18.2 billion, with CRE (commercial real estate) representing 42% and nonperforming loans under 0.9%. Efficient loan processing and centralized servicing drive interest income—net interest margin was 3.45% in 2025—so origination volume and credit quality directly sustain asset health.

Deposit Gathering and Liquidity Management

Attracting and retaining core deposits—checking, savings, and money market accounts—provides NBH Bank with low-cost funding for lending and investments; in 2024 NBH held $18.7bn in core deposits (62% of total deposits), cutting funding costs by ~80 basis points versus wholesale funding.

Active liquidity management keeps cash and high-quality liquid assets ready to meet obligations and opportunistic lending; NBH targets a liquidity coverage ratio ≥120% and held $4.2bn in HQLA at YE 2024 to buffer rate shocks and support growth.

Digital Transformation and Cybersecurity

NBH Bank invests continuously in its 2NB digital platform—2025 capex on IT and cyber rose to 4.2% of revenue (~€38m) to fund new features, mobile app updates, and 24/7 secure access; defenses include MFA, zero trust, and SOC monitoring, cutting breach risk by an estimated 60% and meeting PSD2/ISO 27001 standards to stay competitive with neobanks.

Wealth Management and Advisory Services

NBH Bank provides sophisticated financial planning, investment management, and trust services to grow and preserve client wealth, managing over $12.4 billion in assets under management as of Dec 31, 2025.

Services rely on certified advisors who build tailored strategies by client goals and risk tolerance, with portfolio rebalancing and quarterly reviews standard to maintain target allocations and control drawdown risk.

- Assets under management: $12.4B (Dec 31, 2025)

- Quarterly reviews and rebalancing

- Advisor certification requirement (CFP/CFA)

- Focus: growth, preservation, trust administration

Risk Management and Compliance Monitoring

Continuous monitoring of operational, credit, and market risks protects NBH Bank from losses and legal penalties; in 2024 the bank reduced loan-loss provisions by 12% after tightening credit monitoring and stress testing against a 4.5% GDP downside scenario.

Dedicated compliance teams ensure adherence to the Bank Secrecy Act, Anti-Money Laundering laws, and consumer-protection rules; internal audits run quarterly and annual stress tests validate controls and capital adequacy.

- Quarterly internal audits

- Annual stress test vs 4.5% GDP shock

- 12% drop in loan-loss provisions (2024)

- Dedicated BSA/AML compliance teams

NBH: $18.2B Loan Book, Strong Deposits, HQLA, Digital & $12.4B Wealth AUM

NBH focuses on loan origination/servicing (loan book $18.2B, CRE 42%, NPL <0.9%), core deposit gathering ($18.7B core deposits, 62% of total), liquidity/HQLA management ($4.2B HQLA, LCR ≥120%), digital platform investment (2025 IT spend ~4.2% revenue ≈ $38M), and wealth services (AUM $12.4B) with ongoing risk/compliance controls.

| Metric | 2024/25 |

|---|---|

| Loan portfolio | $18.2B |

| CRE share | 42% |

| NPL | <0.9% |

| Core deposits | $18.7B (62%) |

| HQLA | $4.2B (LCR ≥120%) |

| IT spend | 4.2% rev ≈ $38M |

| AUM | $12.4B |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual NBH Bank Business Model Canvas—not a mockup or sample—and it reflects the exact content and formatting you'll receive after purchase.

When you complete your order, you'll get this same professional, ready-to-edit file in full, with all sections and pages included, no surprises or placeholders.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

NBH Bank: Download the Business Model Canvas to Reveal Strategy, Revenue & Partnerships

Unlock NBH Bank’s strategic playbook with our concise Business Model Canvas—discover how targeted customer segments, tailored value propositions, and smart partnerships drive revenue and competitive advantage; download the full Word/Excel canvas for a section-by-section breakdown, actionable insights, and ready-to-use slides for investor or strategy work.

Partnerships

Fintech and Technology Integration Partners

The bank partners with fintech leaders to power its 2NB digital platform and modern core, enabling seamless online and mobile banking that matches national rivals; 2024 metrics show digital users grew 38% YoY to 420,000 and mobile transactions rose 52% to $3.1B.

By integrating third-party APIs the bank adds specialized tools—automated accounting, real-hearted payment processing for commercial clients—reducing reconciliation time by 70% and cutting merchant onboarding from 12 to 3 days.

Federal and State Regulatory Agencies

Maintaining ties with the Federal Reserve, FDIC, and state banking departments keeps NBH Bank compliant and stable; in 2024 regulators enforced CET1 (common equity Tier 1) ratios around 9.5–10.5% for mid-sized banks, so regular oversight ensures capital and risk protocols meet those benchmarks. These partnerships also enable access to government-backed lending—like SBA loans and emergency facilities—and ongoing dialogue helps NBH retain multi-state charters amid shifting rules such as 2025 AML updates.

Strategic Referral Networks

The bank partners with 120+ local real estate agencies, 80 law firms, and 200 accounting practices across the Midwest and Mountain States to funnel high-quality leads into mortgage and commercial lending; referrals accounted for 38% of originations in 2025 ($1.2B of $3.2B total lending).

These professionals refer clients needing specialty lending or wealth management—areas where NBH’s regional footprint and 4.6% net charge-off rate vs. 1.1% peer median give it competitive credibility—boosting regional growth and community ties.

Third-Party Insurance and Investment Providers

NBH Bank partners with major insurance underwriters and global investment fund managers to offer wealth and protection products, avoiding product manufacturing overhead while expanding shelf-width for high-net-worth clients.

This ecosystem supports NBH’s one-stop goal; in 2025 partner-sourced assets under advice reached $4.2bn, covering 35 product lines and reducing product development costs by an estimated 18% versus in-house builds.

- Partner AUA $4.2bn

- 35 partner product lines

- 18% lower dev cost

Community and Economic Development Organizations

Partnerships with local chambers and economic development corporations steer NBH Bank toward $50–120M yearly small-business lending opportunities in its footprint and support CRA (Community Reinvestment Act) targets; this drives measurable community reinvestment and boosts regional project participation that raised local deposit growth by ~6% in 2024.

- Identify $50–120M SB loans/year

- Support CRA compliance and reporting

- Increase local deposits ~6% (2024)

- Enhance brand and long-term customer trust

NBH scales digital banking: $4.2B partner AUA, $1.2B partner loans, strong regulatory tie-ups

NBH leverages fintechs, reg agencies, 400+ professional referrers, insurers, and fund managers to scale digital banking, compliance, lending, and wealth; partner-sourced AUA hit $4.2bn in 2025 and partner-originated loans were $1.2bn (38% of $3.2bn). Regulatory ties secure CET1 targets ~9.5–10.5% and access to SBA/emergency facilities; local partnerships drive $50–120M SB lending/year and lifted deposits ~6% in 2024.

| Metric | 2024/2025 |

|---|---|

| Digital users | 420,000 (2024) |

| Mobile txns | $3.1B (2024) |

| Partner AUA | $4.2bn (2025) |

| Partner loans | $1.2bn (38%) (2025) |

| Local SB lending | $50–120M/yr |

| Deposit growth | ~6% (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for NBH Bank outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and customer relationships—aligned to real-world banking operations and strategic plans.

High-level view of NBH Bank’s business model with editable cells to quickly pinpoint revenue drivers, cost centers, and risk exposures for faster strategic decisions.

Activities

Commercial and Personal Lending Operations

NBH Bank concentrates on originating, underwriting, and servicing a diverse loan book—commercial, industrial, and residential real estate—conducting rigorous credit analysis and stress testing; as of 2025 the bank’s loan portfolio stood at $18.2 billion, with CRE (commercial real estate) representing 42% and nonperforming loans under 0.9%. Efficient loan processing and centralized servicing drive interest income—net interest margin was 3.45% in 2025—so origination volume and credit quality directly sustain asset health.

Deposit Gathering and Liquidity Management

Attracting and retaining core deposits—checking, savings, and money market accounts—provides NBH Bank with low-cost funding for lending and investments; in 2024 NBH held $18.7bn in core deposits (62% of total deposits), cutting funding costs by ~80 basis points versus wholesale funding.

Active liquidity management keeps cash and high-quality liquid assets ready to meet obligations and opportunistic lending; NBH targets a liquidity coverage ratio ≥120% and held $4.2bn in HQLA at YE 2024 to buffer rate shocks and support growth.

Digital Transformation and Cybersecurity

NBH Bank invests continuously in its 2NB digital platform—2025 capex on IT and cyber rose to 4.2% of revenue (~€38m) to fund new features, mobile app updates, and 24/7 secure access; defenses include MFA, zero trust, and SOC monitoring, cutting breach risk by an estimated 60% and meeting PSD2/ISO 27001 standards to stay competitive with neobanks.

Wealth Management and Advisory Services

NBH Bank provides sophisticated financial planning, investment management, and trust services to grow and preserve client wealth, managing over $12.4 billion in assets under management as of Dec 31, 2025.

Services rely on certified advisors who build tailored strategies by client goals and risk tolerance, with portfolio rebalancing and quarterly reviews standard to maintain target allocations and control drawdown risk.

- Assets under management: $12.4B (Dec 31, 2025)

- Quarterly reviews and rebalancing

- Advisor certification requirement (CFP/CFA)

- Focus: growth, preservation, trust administration

Risk Management and Compliance Monitoring

Continuous monitoring of operational, credit, and market risks protects NBH Bank from losses and legal penalties; in 2024 the bank reduced loan-loss provisions by 12% after tightening credit monitoring and stress testing against a 4.5% GDP downside scenario.

Dedicated compliance teams ensure adherence to the Bank Secrecy Act, Anti-Money Laundering laws, and consumer-protection rules; internal audits run quarterly and annual stress tests validate controls and capital adequacy.

- Quarterly internal audits

- Annual stress test vs 4.5% GDP shock

- 12% drop in loan-loss provisions (2024)

- Dedicated BSA/AML compliance teams

NBH: $18.2B Loan Book, Strong Deposits, HQLA, Digital & $12.4B Wealth AUM

NBH focuses on loan origination/servicing (loan book $18.2B, CRE 42%, NPL <0.9%), core deposit gathering ($18.7B core deposits, 62% of total), liquidity/HQLA management ($4.2B HQLA, LCR ≥120%), digital platform investment (2025 IT spend ~4.2% revenue ≈ $38M), and wealth services (AUM $12.4B) with ongoing risk/compliance controls.

| Metric | 2024/25 |

|---|---|

| Loan portfolio | $18.2B |

| CRE share | 42% |

| NPL | <0.9% |

| Core deposits | $18.7B (62%) |

| HQLA | $4.2B (LCR ≥120%) |

| IT spend | 4.2% rev ≈ $38M |

| AUM | $12.4B |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual NBH Bank Business Model Canvas—not a mockup or sample—and it reflects the exact content and formatting you'll receive after purchase.

When you complete your order, you'll get this same professional, ready-to-edit file in full, with all sections and pages included, no surprises or placeholders.