National Grid PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political regulation, decarbonization mandates, and technological innovation are reshaping National Grid’s strategy and risk profile; our concise PESTLE highlights the forces that matter and how to act on them—buy the full analysis to access the complete, actionable breakdown and ready-to-use insights.

Political factors

UK Net Zero Policy Alignment

The UK commitment to a carbon-neutral power system by 2030 forces National Grid to fast-track network reinforcement and connection delivery, with BEIS forecasting 70–100 GW of offshore wind capacity by 2030 and National Grid ESO estimating c.£60–100bn grid investment to 2050.

US Federal and State Regulation

Operations in New York and Massachusetts are driven by the Climate Leadership and Community Protection Act and the 2050 Decarbonization Roadmap, and by Massachusetts’ 2030 goal to cut emissions 50% versus 1990 levels, forcing National Grid to plan for large-scale electrification and DER integration.

Federal incentives from the Inflation Reduction Act have unlocked up to $369 billion in clean energy tax credits and grant programs through 2031, increasing subsidies available for grid modernization projects that National Grid can tap for battery, transmission and resilience investments.

Shifts in federal politics can alter FERC priorities and the pace of interstate transmission permitting; recent FERC reform proposals and faster permitting pilots aim to shorten siting timelines that historically delayed multi-state projects by years, affecting project ROI and capital allocation.

Energy Security and Sovereignty

Geopolitical tensions have pushed energy security to the top of government agendas, prompting National Grid to reinforce domestic supply chains after UK gas storage fell to under 2% capacity in 2024; the high-voltage transmission network is now treated as a critical resilience asset, drawing stricter political scrutiny over foreign ownership and prompting policy moves—UK announced a £4bn resilience fund in 2025—to diversify supplies via interconnectors, now totaling 6 GW planned by 2027.

Planning Reform and Permitting

Political efforts to streamline the UK planning system are critical for National Grid to overcome historical bottlenecks that delayed projects by an average of 18–24 months; proposed reforms target cutting judicial review times and shortening local consultation windows for major infrastructure like pylon lines.

The success of National Grid’s £30bn 2024–2029 capital investment plan hinges on political will to reform land-use laws, with estimates suggesting reforms could accelerate project delivery by 20–30% and reduce holding costs tied to delays.

- Average project delays: 18–24 months

- CapEx 2024–2029: £30bn

- Potential delivery acceleration: 20–30%

- Reform focus: shorten judicial reviews & local consultations

Transatlantic Trade and Relations

As a major investor in the UK and US, National Grid is exposed to shifts in transatlantic trade relations; in 2024 UK-US goods trade totaled about £150bn, and tariffs or supply‑chain barriers on transformers or semiconductors could raise procurement costs for grid projects.

Changes to trade agreements affect cross‑border equipment sourcing and could add percentage points to capex on multi‑billion pound projects—National Grid reported £13.8bn capex guidance for 2024–25—while political stability sustains investor confidence for long‑dated financing.

- UK‑US trade ~£150bn (2024)

- National Grid capex guidance £13.8bn (2024–25)

- Tariff or regulatory shifts can increase equipment costs and financing risk

Policy Pushes £30bn National Grid Capex to Meet UK/US Clean‑Energy Targets

Political drivers—UK 2030 carbon-neutral target, BEIS 70–100 GW offshore by 2030, UK £4bn resilience fund (2025), US IRA $369bn credits (through 2031), FERC permitting reforms, UK‑US trade ~£150bn (2024)—force National Grid to accelerate £30bn (2024–29) capex; reforms could cut delivery times 20–30% vs historical 18–24 month delays.

| Metric | Value |

|---|---|

| UK offshore target | 70–100 GW by 2030 |

| Resilience fund | £4bn (2025) |

| IRA credits | $369bn to 2031 |

| NG capex | £30bn (2024–29) |

| Avg delays | 18–24 months |

What is included in the product

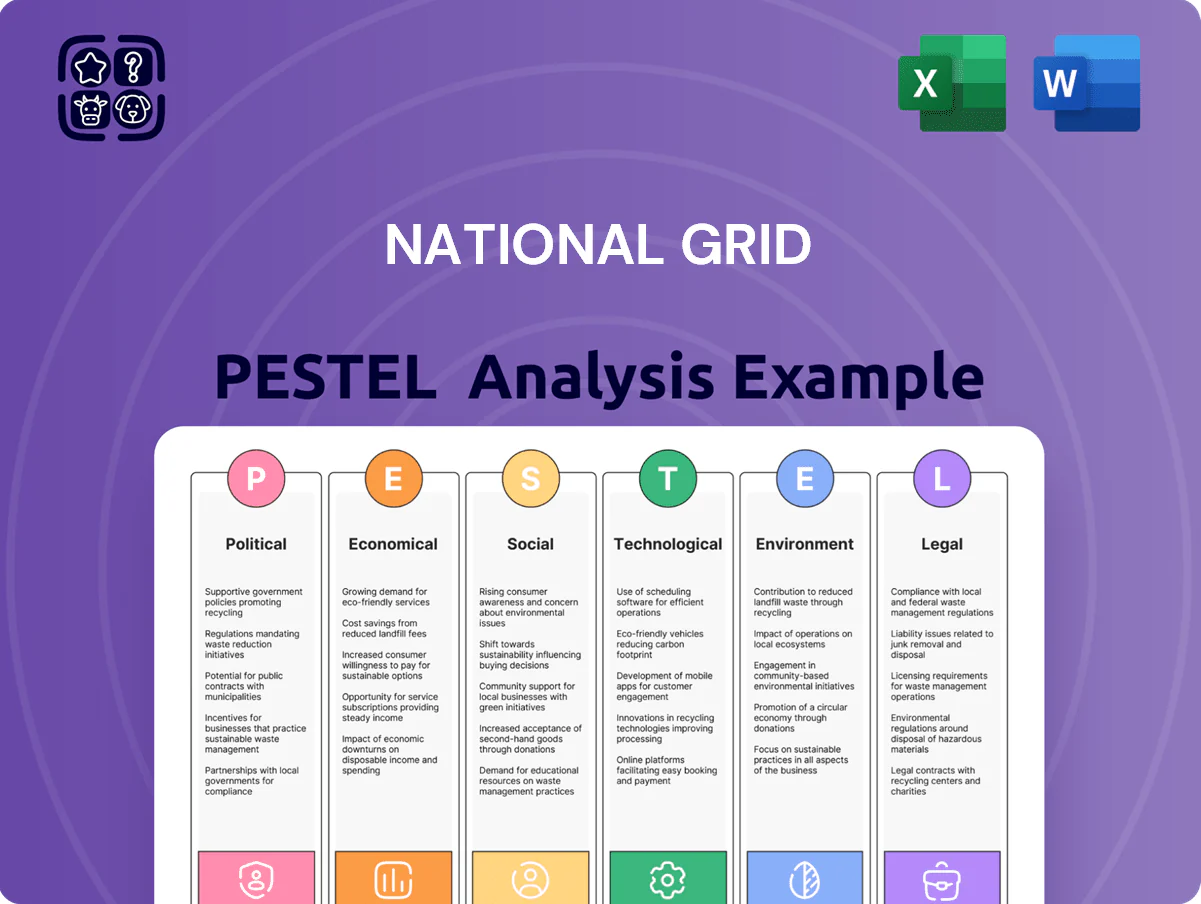

Explores how external macro-environmental factors uniquely affect National Grid across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and regulatory trends to highlight risks and opportunities.

A concise National Grid PESTLE summary that distills regulatory, technological, and environmental risks into an easy-to-share slide or meeting note, enabling rapid team alignment and focused discussion on external threats and strategic positioning.

Economic factors

Interest Rate Environment

High interest rates raise National Grid’s debt servicing costs across ~£40–45bn gross debt (2024), squeezing free cash flow for its ~£17bn five‑year capital program; a 100bp rise can add several hundred million pounds in annual interest expense.

Inflationary Impact on Supply Chains

Persistent inflation has driven copper prices up ~35% and steel up ~20% from 2020–2024, increasing National Grid's input costs for expansion projects; specialized electrical component prices rose ~12% in 2023–24, squeezing margins. Regulated revenue caps limit immediate pass-through of these spikes, exposing the company to margin erosion. Contractor and labor inflation—wage growth averaging 6–8% annually through 2024—remains a key risk for project delivery and margins into 2025.

Regulatory Price Control Frameworks

The RIIO-2 price control (2021–2026) caps allowed returns for UK networks, tying National Grid Electricity Transmission’s revenue to Ofgem-set efficiency targets; missing 2023 benchmarks can reduce returns vs a regulatory equity allowed post-tax real cost of capital ~3.8% used in determinations. In the US, state rate cases set allowed revenues, making 2024 capex recovery and outperforming efficiency targets critical to National Grid’s 2025 guidance of adjusted EBITDA ~£4.9bn.

Energy Market Volatility

While National Grid mainly transmits and distributes energy, volatility in wholesale gas and power raised UK balancing costs to about £3.4bn in 2022–23 and pushed US customer arrears up 35% in some states by 2023, increasing operational expense and credit risk.

Surges in global gas prices (European TTF up ~150% in 2021–22) force National Grid to deploy advanced hedging and liquidity measures to stabilize cash flows and limit exposure.

- UK balancing costs ~£3.4bn (2022–23)

- European TTF spike ~150% (2021–22)

- US distribution customer arrears up ~35% in some states (2023)

- Greater reliance on hedging and liquidity buffers

Capital Allocation and Divestment

National Grid has reshaped its portfolio, selling UK gas transmission for £[sale value not provided] to concentrate on electricity, reflecting higher growth in a decarbonizing economy; by 2024 the company guided capital expenditure of £25–30bn for 2024–2030 toward electricity networks and net zero projects.

Efficient capital recycling is key: return on invested capital and targeted regulated returns (circa mid-single digits to low double digits depending on region) are closely watched by institutional investors and analysts assessing project-level IRRs and balance-sheet impact.

- Sale of UK gas transmission completed to refocus on electricity

- Planned 2024–2030 capex £25–30bn toward electricity/net zero

- Investors monitor ROIC and project IRRs for capital recycling

High rates, rising commodity costs and capex squeeze margins amid tight regulated returns

High rates raise interest on ~£40–45bn gross debt (2024), cutting free cash flow for a ~£17bn 2024–28 capex; inflation lifted copper ~35% and steel ~20% since 2020, squeezing margins; RIIO-2 caps returns (real WACC ~3.8%) while UK balancing costs hit ~£3.4bn (2022–23); 2024–30 capex guidance £25–30bn toward electricity/net zero.

| Metric | Value |

|---|---|

| Gross debt (2024) | £40–45bn |

| Near-term capex | ~£17bn (five‑year) |

| 2024–30 capex | £25–30bn |

| UK balancing costs | £3.4bn (2022–23) |

Same Document Delivered

National Grid PESTLE Analysis

The preview shown here is the exact National Grid PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or teasers.

Everything displayed is the final, professionally structured file—what you see is what you’ll own after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political regulation, decarbonization mandates, and technological innovation are reshaping National Grid’s strategy and risk profile; our concise PESTLE highlights the forces that matter and how to act on them—buy the full analysis to access the complete, actionable breakdown and ready-to-use insights.

Political factors

UK Net Zero Policy Alignment

The UK commitment to a carbon-neutral power system by 2030 forces National Grid to fast-track network reinforcement and connection delivery, with BEIS forecasting 70–100 GW of offshore wind capacity by 2030 and National Grid ESO estimating c.£60–100bn grid investment to 2050.

US Federal and State Regulation

Operations in New York and Massachusetts are driven by the Climate Leadership and Community Protection Act and the 2050 Decarbonization Roadmap, and by Massachusetts’ 2030 goal to cut emissions 50% versus 1990 levels, forcing National Grid to plan for large-scale electrification and DER integration.

Federal incentives from the Inflation Reduction Act have unlocked up to $369 billion in clean energy tax credits and grant programs through 2031, increasing subsidies available for grid modernization projects that National Grid can tap for battery, transmission and resilience investments.

Shifts in federal politics can alter FERC priorities and the pace of interstate transmission permitting; recent FERC reform proposals and faster permitting pilots aim to shorten siting timelines that historically delayed multi-state projects by years, affecting project ROI and capital allocation.

Energy Security and Sovereignty

Geopolitical tensions have pushed energy security to the top of government agendas, prompting National Grid to reinforce domestic supply chains after UK gas storage fell to under 2% capacity in 2024; the high-voltage transmission network is now treated as a critical resilience asset, drawing stricter political scrutiny over foreign ownership and prompting policy moves—UK announced a £4bn resilience fund in 2025—to diversify supplies via interconnectors, now totaling 6 GW planned by 2027.

Planning Reform and Permitting

Political efforts to streamline the UK planning system are critical for National Grid to overcome historical bottlenecks that delayed projects by an average of 18–24 months; proposed reforms target cutting judicial review times and shortening local consultation windows for major infrastructure like pylon lines.

The success of National Grid’s £30bn 2024–2029 capital investment plan hinges on political will to reform land-use laws, with estimates suggesting reforms could accelerate project delivery by 20–30% and reduce holding costs tied to delays.

- Average project delays: 18–24 months

- CapEx 2024–2029: £30bn

- Potential delivery acceleration: 20–30%

- Reform focus: shorten judicial reviews & local consultations

Transatlantic Trade and Relations

As a major investor in the UK and US, National Grid is exposed to shifts in transatlantic trade relations; in 2024 UK-US goods trade totaled about £150bn, and tariffs or supply‑chain barriers on transformers or semiconductors could raise procurement costs for grid projects.

Changes to trade agreements affect cross‑border equipment sourcing and could add percentage points to capex on multi‑billion pound projects—National Grid reported £13.8bn capex guidance for 2024–25—while political stability sustains investor confidence for long‑dated financing.

- UK‑US trade ~£150bn (2024)

- National Grid capex guidance £13.8bn (2024–25)

- Tariff or regulatory shifts can increase equipment costs and financing risk

Policy Pushes £30bn National Grid Capex to Meet UK/US Clean‑Energy Targets

Political drivers—UK 2030 carbon-neutral target, BEIS 70–100 GW offshore by 2030, UK £4bn resilience fund (2025), US IRA $369bn credits (through 2031), FERC permitting reforms, UK‑US trade ~£150bn (2024)—force National Grid to accelerate £30bn (2024–29) capex; reforms could cut delivery times 20–30% vs historical 18–24 month delays.

| Metric | Value |

|---|---|

| UK offshore target | 70–100 GW by 2030 |

| Resilience fund | £4bn (2025) |

| IRA credits | $369bn to 2031 |

| NG capex | £30bn (2024–29) |

| Avg delays | 18–24 months |

What is included in the product

Explores how external macro-environmental factors uniquely affect National Grid across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and regulatory trends to highlight risks and opportunities.

A concise National Grid PESTLE summary that distills regulatory, technological, and environmental risks into an easy-to-share slide or meeting note, enabling rapid team alignment and focused discussion on external threats and strategic positioning.

Economic factors

Interest Rate Environment

High interest rates raise National Grid’s debt servicing costs across ~£40–45bn gross debt (2024), squeezing free cash flow for its ~£17bn five‑year capital program; a 100bp rise can add several hundred million pounds in annual interest expense.

Inflationary Impact on Supply Chains

Persistent inflation has driven copper prices up ~35% and steel up ~20% from 2020–2024, increasing National Grid's input costs for expansion projects; specialized electrical component prices rose ~12% in 2023–24, squeezing margins. Regulated revenue caps limit immediate pass-through of these spikes, exposing the company to margin erosion. Contractor and labor inflation—wage growth averaging 6–8% annually through 2024—remains a key risk for project delivery and margins into 2025.

Regulatory Price Control Frameworks

The RIIO-2 price control (2021–2026) caps allowed returns for UK networks, tying National Grid Electricity Transmission’s revenue to Ofgem-set efficiency targets; missing 2023 benchmarks can reduce returns vs a regulatory equity allowed post-tax real cost of capital ~3.8% used in determinations. In the US, state rate cases set allowed revenues, making 2024 capex recovery and outperforming efficiency targets critical to National Grid’s 2025 guidance of adjusted EBITDA ~£4.9bn.

Energy Market Volatility

While National Grid mainly transmits and distributes energy, volatility in wholesale gas and power raised UK balancing costs to about £3.4bn in 2022–23 and pushed US customer arrears up 35% in some states by 2023, increasing operational expense and credit risk.

Surges in global gas prices (European TTF up ~150% in 2021–22) force National Grid to deploy advanced hedging and liquidity measures to stabilize cash flows and limit exposure.

- UK balancing costs ~£3.4bn (2022–23)

- European TTF spike ~150% (2021–22)

- US distribution customer arrears up ~35% in some states (2023)

- Greater reliance on hedging and liquidity buffers

Capital Allocation and Divestment

National Grid has reshaped its portfolio, selling UK gas transmission for £[sale value not provided] to concentrate on electricity, reflecting higher growth in a decarbonizing economy; by 2024 the company guided capital expenditure of £25–30bn for 2024–2030 toward electricity networks and net zero projects.

Efficient capital recycling is key: return on invested capital and targeted regulated returns (circa mid-single digits to low double digits depending on region) are closely watched by institutional investors and analysts assessing project-level IRRs and balance-sheet impact.

- Sale of UK gas transmission completed to refocus on electricity

- Planned 2024–2030 capex £25–30bn toward electricity/net zero

- Investors monitor ROIC and project IRRs for capital recycling

High rates, rising commodity costs and capex squeeze margins amid tight regulated returns

High rates raise interest on ~£40–45bn gross debt (2024), cutting free cash flow for a ~£17bn 2024–28 capex; inflation lifted copper ~35% and steel ~20% since 2020, squeezing margins; RIIO-2 caps returns (real WACC ~3.8%) while UK balancing costs hit ~£3.4bn (2022–23); 2024–30 capex guidance £25–30bn toward electricity/net zero.

| Metric | Value |

|---|---|

| Gross debt (2024) | £40–45bn |

| Near-term capex | ~£17bn (five‑year) |

| 2024–30 capex | £25–30bn |

| UK balancing costs | £3.4bn (2022–23) |

Same Document Delivered

National Grid PESTLE Analysis

The preview shown here is the exact National Grid PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or teasers.

Everything displayed is the final, professionally structured file—what you see is what you’ll own after checkout.