NAURA Technology GroupLtd Business Model Canvas

NAURA Technology: Compact Business Model Canvas for Investors & Strategists

Unlock NAURA Technology GroupLtd’s strategic playbook with a concise Business Model Canvas that maps value propositions, key partners, revenue streams, and growth levers—ideal for investors and strategists seeking actionable insight.

Partnerships

Strategic Semiconductor Foundries

NAURA partners with major Chinese foundries such as SMIC ( Semiconductor Manufacturing International Corp.) and Hua Hong (Shanghai Huahong Group) to test etch and deposition tools in production lines; in 2024 these collaborations covered validation on nodes down to 28nm and comprised >40% of NAURA’s domestic equipment validation hours.

Aligning roadmaps with foundries ensures NAURA’s hardware meets node specs and yields: joint pilot runs in 2023–2024 drove a 12% tool throughput improvement and supported foundry scale-up that contributed to NAURA’s 2024 China revenues of RMB 1.2bn tied to front-end equipment sales.

Government and State Investment Vehicles

NAURA benefits from close ties with the China Integrated Circuit Industry Investment Fund and state-backed vehicles that supplied an estimated CNY 3.2 billion in equity and project financing through 2024, enabling 20% capacity expansion and funding R&D programs that cut wafer defect rates by 15%.

Specialized Component Suppliers

NAURA relies on a network of high-precision component manufacturers for vacuum-system and plasma-generator parts; in 2024 about 62% of its equipment BOM value came from five key suppliers, so stable contracts cut lead-time volatility that averaged 14 weeks without them. Collaborative co-design reduces rework rates by ~18% and helps meet strict specs for 3nm–5nm microelectronics tools.

Academic and Research Institutions

Joint ventures and research agreements with top universities and the Chinese Academy of Sciences drive NAURA’s materials and physics R&D, yielding ~18 patents/year (2024) and cutting thin-film defect rates by ~22% in pilot runs.

These ties supply a steady hiring funnel—~30% of new engineers (2024) came from partner labs—and help commercialize IP that contributed ~7% of NAURA Technology GroupLtd’s 2024 revenue.

- ~18 patents/year (2024)

- 22% defect-rate reduction in thin-film pilots

- 30% of 2024 engineering hires from partners

- 7% of 2024 revenue from commercialized IP

New Energy and Battery Partners

Collaborations with top lithium-ion battery makers and solar-cell producers let NAURA adapt vacuum and coating tools for energy storage and PV, addressing a market where global battery manufacturing capacity hit ~3 TWh and solar PV installations reached 420 GW in 2024.

These partners share production specs and demand forecasts, guiding equipment R&D and helping NAURA reduce semiconductor cyclicality by tapping high-growth segments—battery and PV revenues grew ~18% and 25% in 2024 respectively.

- Access to 3 TWh battery capacity (2024)

- 420 GW global PV additions (2024)

- Battery/PV sector revenue growth ~18%/25% (2024)

- Enables specialized vacuum/coating product lines

- Reduces semiconductor cyclicality risk

NAURA partnerships fuel 2024: RMB1.2bn sales, CNY3.2bn funding, +40% validation

NAURA’s key partnerships with SMIC, Hua Hong, state funds, top suppliers, universities, and battery/PV firms drove validation hours >40%, supported RMB 1.2bn 2024 China front‑end sales, ~CNY 3.2bn financing, 18 patents/year, 22% thin‑film defect cut, 30% new engineers, and 7% revenue from IP; battery/PV lines grew ~18%/25% in 2024.

| Metric | 2024 |

|---|---|

| Validation hours from foundry partners | >40% |

| China front‑end revenue | RMB 1.2bn |

| State funding | CNY 3.2bn |

| Patents/year | ~18 |

| Thin‑film defect reduction | 22% |

| New engineers from partners | 30% |

| Revenue from IP | 7% |

| Battery revenue growth | ~18% |

| PV revenue growth | ~25% |

What is included in the product

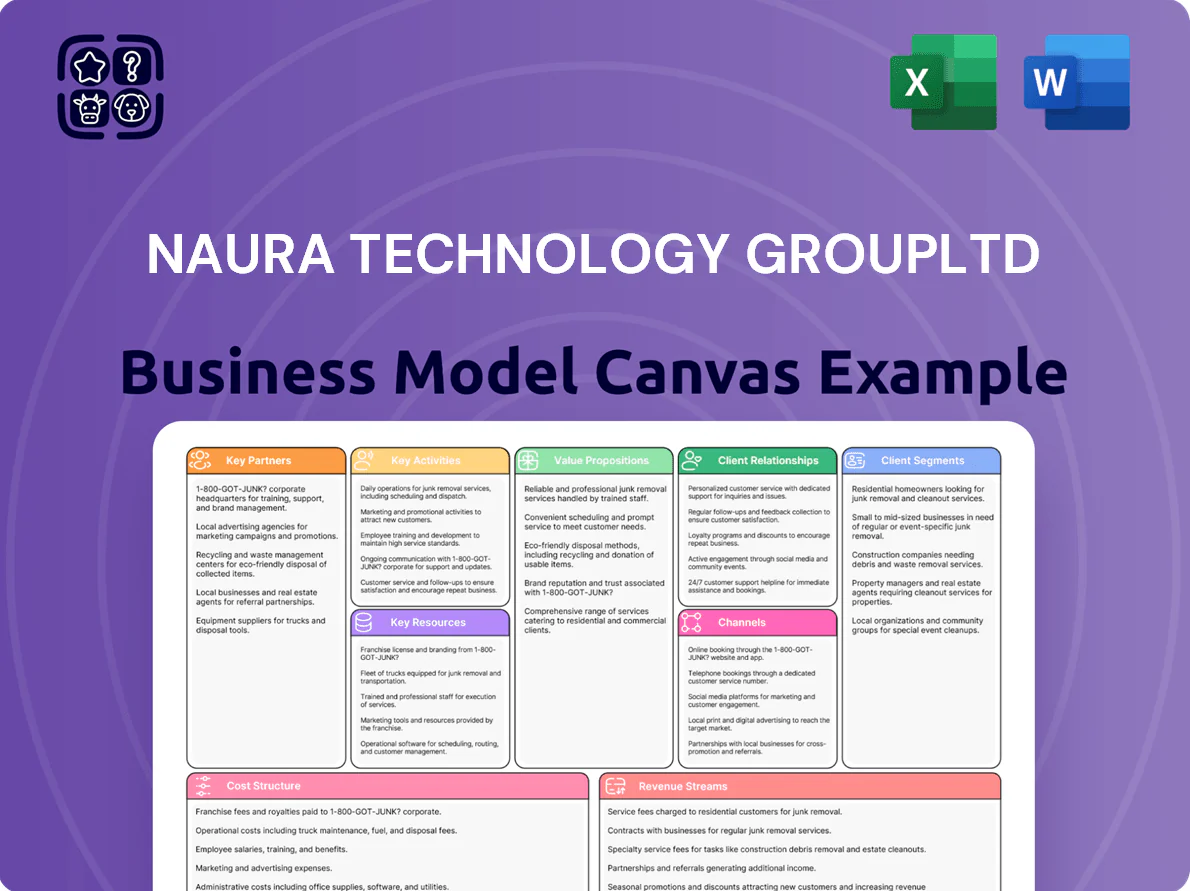

A concise, pre-crafted Business Model Canvas for NAURA Technology Group Ltd outlining customer segments, channels, value propositions, key activities, partners, resources, cost structure, and revenue streams, reflecting its semiconductor and equipment-focused operations and strategic priorities for investors and analysts.

High-level view of NAURA Technology Group Ltd’s business model with editable cells, enabling teams to quickly pinpoint R&D, manufacturing, and customer-segmentation pain points for faster decision-making.

Activities

Advanced Research and Development

NAURA's R&D centers continuously design and optimize etch, PVD, CVD, and cleaning tools to reach sub-7nm precision and uniformity; engineers run >1,200 wafer-test cycles monthly to validate process windows. In 2025 NAURA invested RMB 1.1 billion in prototyping and testing—about 12% of revenue—to accelerate tool qualification and close the gap with global incumbents.

High Precision Manufacturing

NAURA runs cleanroom assembly lines building complex semiconductor and vacuum tools, with strict QC and supply-chain coordination; in 2024 NAURA reported 18% YoY manufacturing revenue growth and a 92% first-pass yield, enabling scale-up to meet China’s 2025 target of domesticizing 40% of advanced tool demand.

Technical Support and Field Engineering

NAURA Technology Group Ltd provides on-site installation, calibration, and maintenance to keep equipment uptime above 95%—field engineers resolve issues within 24–48 hours on 82% of service calls—and they optimize process recipes per run to boost yield by up to 3–8%, which builds trust and protects lifecycle value of multi-million-dollar tools.

Intellectual Property Management

Actively filing and defending patents protects NAURA Technology Group Ltd’s microelectronics and vacuum-tech innovations; as of 2025 the company holds over 1,200 global patents and spent ~CNY 120 million on IP in 2024 to enforce and expand this portfolio.

Monitoring worldwide tech trends and securing new developments reduces infringement risk, boosts valuation—IP contributes materially to enterprise value in semiconductor suppliers, often 15–25% of market cap—and strengthens bargaining power in international tenders.

- 1,200+ patents (2025)

- CNY 120M IP spend (2024)

- IP ≈15–25% of comparable firm value

Market Expansion and Strategic Sales

NAURA targets domestic and international electronics OEMs with focused marketing and sales, attending industry shows (SEMICON, ITEC) and running technical seminars to demo equipment; in 2024 these activities supported ~12% revenue growth and helped secure deals totaling ~RMB 3.2 billion (~USD 460M) across vacuum deposition and etch tools.

Strategic sales position NAURA as a one-stop provider across wafer fab steps, pitching integrated toolsets and service contracts to increase aftermarket revenue, where service & spares rose to ~22% of group revenue in FY2024.

- Attend SEMICON/ITEC

- Demo tech via seminars

- Closed ~RMB 3.2B deals in 2024

- 12% revenue growth (2024)

- Service = 22% of revenue (FY2024)

NAURA: High-yield manufacturing, 1,200+ patents, RMB 1.1B R&D push, RMB 3.2B deals

NAURA runs R&D (1,200+ wafer tests/mo), spent RMB 1.1B on prototyping in 2025 (12% revenue), manufactures with 92% first-pass yield and 18% YoY manufacturing growth (2024), service uptime >95% with 82% fixes in 24–48h, 1,200+ patents (2025) and CNY 120M IP spend (2024), closed ~RMB 3.2B deals (2024); service = 22% of group revenue (FY2024).

| Metric | Value |

|---|---|

| R&D tests/mo | 1,200+ |

| Prototyping spend 2025 | RMB 1.1B (12% rev) |

| First-pass yield | 92% |

| Manufacturing growth 2024 | 18% YoY |

| Service uptime | >95% |

| Patents 2025 | 1,200+ |

| IP spend 2024 | CNY 120M |

| Deals closed 2024 | ~RMB 3.2B |

| Service revenue FY2024 | 22% |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual NAURA Technology Group Ltd Business Model Canvas—no mockup or sample. When you purchase, you’ll receive this exact, fully editable file formatted for immediate use. The full deliverable matches this preview in content and layout, ready for presentation or customization. No surprises—what you see is what you’ll download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

NAURA Technology: Compact Business Model Canvas for Investors & Strategists

Unlock NAURA Technology GroupLtd’s strategic playbook with a concise Business Model Canvas that maps value propositions, key partners, revenue streams, and growth levers—ideal for investors and strategists seeking actionable insight.

Partnerships

Strategic Semiconductor Foundries

NAURA partners with major Chinese foundries such as SMIC ( Semiconductor Manufacturing International Corp.) and Hua Hong (Shanghai Huahong Group) to test etch and deposition tools in production lines; in 2024 these collaborations covered validation on nodes down to 28nm and comprised >40% of NAURA’s domestic equipment validation hours.

Aligning roadmaps with foundries ensures NAURA’s hardware meets node specs and yields: joint pilot runs in 2023–2024 drove a 12% tool throughput improvement and supported foundry scale-up that contributed to NAURA’s 2024 China revenues of RMB 1.2bn tied to front-end equipment sales.

Government and State Investment Vehicles

NAURA benefits from close ties with the China Integrated Circuit Industry Investment Fund and state-backed vehicles that supplied an estimated CNY 3.2 billion in equity and project financing through 2024, enabling 20% capacity expansion and funding R&D programs that cut wafer defect rates by 15%.

Specialized Component Suppliers

NAURA relies on a network of high-precision component manufacturers for vacuum-system and plasma-generator parts; in 2024 about 62% of its equipment BOM value came from five key suppliers, so stable contracts cut lead-time volatility that averaged 14 weeks without them. Collaborative co-design reduces rework rates by ~18% and helps meet strict specs for 3nm–5nm microelectronics tools.

Academic and Research Institutions

Joint ventures and research agreements with top universities and the Chinese Academy of Sciences drive NAURA’s materials and physics R&D, yielding ~18 patents/year (2024) and cutting thin-film defect rates by ~22% in pilot runs.

These ties supply a steady hiring funnel—~30% of new engineers (2024) came from partner labs—and help commercialize IP that contributed ~7% of NAURA Technology GroupLtd’s 2024 revenue.

- ~18 patents/year (2024)

- 22% defect-rate reduction in thin-film pilots

- 30% of 2024 engineering hires from partners

- 7% of 2024 revenue from commercialized IP

New Energy and Battery Partners

Collaborations with top lithium-ion battery makers and solar-cell producers let NAURA adapt vacuum and coating tools for energy storage and PV, addressing a market where global battery manufacturing capacity hit ~3 TWh and solar PV installations reached 420 GW in 2024.

These partners share production specs and demand forecasts, guiding equipment R&D and helping NAURA reduce semiconductor cyclicality by tapping high-growth segments—battery and PV revenues grew ~18% and 25% in 2024 respectively.

- Access to 3 TWh battery capacity (2024)

- 420 GW global PV additions (2024)

- Battery/PV sector revenue growth ~18%/25% (2024)

- Enables specialized vacuum/coating product lines

- Reduces semiconductor cyclicality risk

NAURA partnerships fuel 2024: RMB1.2bn sales, CNY3.2bn funding, +40% validation

NAURA’s key partnerships with SMIC, Hua Hong, state funds, top suppliers, universities, and battery/PV firms drove validation hours >40%, supported RMB 1.2bn 2024 China front‑end sales, ~CNY 3.2bn financing, 18 patents/year, 22% thin‑film defect cut, 30% new engineers, and 7% revenue from IP; battery/PV lines grew ~18%/25% in 2024.

| Metric | 2024 |

|---|---|

| Validation hours from foundry partners | >40% |

| China front‑end revenue | RMB 1.2bn |

| State funding | CNY 3.2bn |

| Patents/year | ~18 |

| Thin‑film defect reduction | 22% |

| New engineers from partners | 30% |

| Revenue from IP | 7% |

| Battery revenue growth | ~18% |

| PV revenue growth | ~25% |

What is included in the product

A concise, pre-crafted Business Model Canvas for NAURA Technology Group Ltd outlining customer segments, channels, value propositions, key activities, partners, resources, cost structure, and revenue streams, reflecting its semiconductor and equipment-focused operations and strategic priorities for investors and analysts.

High-level view of NAURA Technology Group Ltd’s business model with editable cells, enabling teams to quickly pinpoint R&D, manufacturing, and customer-segmentation pain points for faster decision-making.

Activities

Advanced Research and Development

NAURA's R&D centers continuously design and optimize etch, PVD, CVD, and cleaning tools to reach sub-7nm precision and uniformity; engineers run >1,200 wafer-test cycles monthly to validate process windows. In 2025 NAURA invested RMB 1.1 billion in prototyping and testing—about 12% of revenue—to accelerate tool qualification and close the gap with global incumbents.

High Precision Manufacturing

NAURA runs cleanroom assembly lines building complex semiconductor and vacuum tools, with strict QC and supply-chain coordination; in 2024 NAURA reported 18% YoY manufacturing revenue growth and a 92% first-pass yield, enabling scale-up to meet China’s 2025 target of domesticizing 40% of advanced tool demand.

Technical Support and Field Engineering

NAURA Technology Group Ltd provides on-site installation, calibration, and maintenance to keep equipment uptime above 95%—field engineers resolve issues within 24–48 hours on 82% of service calls—and they optimize process recipes per run to boost yield by up to 3–8%, which builds trust and protects lifecycle value of multi-million-dollar tools.

Intellectual Property Management

Actively filing and defending patents protects NAURA Technology Group Ltd’s microelectronics and vacuum-tech innovations; as of 2025 the company holds over 1,200 global patents and spent ~CNY 120 million on IP in 2024 to enforce and expand this portfolio.

Monitoring worldwide tech trends and securing new developments reduces infringement risk, boosts valuation—IP contributes materially to enterprise value in semiconductor suppliers, often 15–25% of market cap—and strengthens bargaining power in international tenders.

- 1,200+ patents (2025)

- CNY 120M IP spend (2024)

- IP ≈15–25% of comparable firm value

Market Expansion and Strategic Sales

NAURA targets domestic and international electronics OEMs with focused marketing and sales, attending industry shows (SEMICON, ITEC) and running technical seminars to demo equipment; in 2024 these activities supported ~12% revenue growth and helped secure deals totaling ~RMB 3.2 billion (~USD 460M) across vacuum deposition and etch tools.

Strategic sales position NAURA as a one-stop provider across wafer fab steps, pitching integrated toolsets and service contracts to increase aftermarket revenue, where service & spares rose to ~22% of group revenue in FY2024.

- Attend SEMICON/ITEC

- Demo tech via seminars

- Closed ~RMB 3.2B deals in 2024

- 12% revenue growth (2024)

- Service = 22% of revenue (FY2024)

NAURA: High-yield manufacturing, 1,200+ patents, RMB 1.1B R&D push, RMB 3.2B deals

NAURA runs R&D (1,200+ wafer tests/mo), spent RMB 1.1B on prototyping in 2025 (12% revenue), manufactures with 92% first-pass yield and 18% YoY manufacturing growth (2024), service uptime >95% with 82% fixes in 24–48h, 1,200+ patents (2025) and CNY 120M IP spend (2024), closed ~RMB 3.2B deals (2024); service = 22% of group revenue (FY2024).

| Metric | Value |

|---|---|

| R&D tests/mo | 1,200+ |

| Prototyping spend 2025 | RMB 1.1B (12% rev) |

| First-pass yield | 92% |

| Manufacturing growth 2024 | 18% YoY |

| Service uptime | >95% |

| Patents 2025 | 1,200+ |

| IP spend 2024 | CNY 120M |

| Deals closed 2024 | ~RMB 3.2B |

| Service revenue FY2024 | 22% |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual NAURA Technology Group Ltd Business Model Canvas—no mockup or sample. When you purchase, you’ll receive this exact, fully editable file formatted for immediate use. The full deliverable matches this preview in content and layout, ready for presentation or customization. No surprises—what you see is what you’ll download.