Bank of Ningbo Business Model Canvas

Bank of Ningbo: Actionable Business Model Canvas for Investors & Strategists

Unlock the full strategic blueprint behind Bank of Ningbo’s business model — a concise, actionable Business Model Canvas that maps its value propositions, customer segments, revenue streams, and key partnerships.

Perfect for investors, consultants, and strategists, this downloadable Word/Excel file reveals operational levers, growth opportunities, and risks to help you benchmark or build winning financial strategies.

Partnerships

Strategic Alliance with OCBC Bank

As a major shareholder, OCBC Bank (Singapore) supplies Bank of Ningbo with international risk and wealth-management expertise, backing upgraded credit-risk models and cross-border compliance frameworks used since OCBC took a 12.2% stake in 2016; this raised BIS CET1 planning and reduced nonperforming loans to 1.35% by 2024. The tie lets Bank of Ningbo offer OCBC’s global cash‑management and trade services to clients expanding beyond China, boosting Yangtze River Delta multinational coverage and cross-border fee income.

Local Government and Public Sector Entities

The bank holds long-standing ties with Zhejiang and other provinces, acting as primary fiscal agent for municipal accounts and social security funds—handling over CNY 420 billion in government deposits as of 2025, which supplies low-cost funding and liquidity. These links secure priority lending into state-backed infrastructure and development zones, where Bank of Ningbo underwrote roughly CNY 85 billion in project loans in 2024–2025.

Fintech and Digital Infrastructure Providers

Collaborations with leading tech firms let Bank of Ningbo embed AI and cloud computing into core systems, supporting automated credit scoring that cut default prediction error by ~12% in 2024 and reducing IT latency 30% after a 2023 cloud migration.

Interbank and Financial Institution Networks

Membership in national and international clearing networks (CIPS, CNAPS, SWIFT) enables Bank of Ningbo to process >¥5tn annual payments and optimize liquidity across corridors, reducing settlement times and intraday funding needs.

Partnerships with banks for syndicated loans and interbank lending diversify assets—~¥120bn syndicated exposure in 2024—and support complex investment-banking mandates and institutional capital flows.

- Clearing networks: CIPS, CNAPS, SWIFT

- Payments processed: >¥5tn/year (2024)

- Syndicated exposure: ~¥120bn (2024)

- Use: liquidity mgmt, settlement speed, IB mandates

Supply Chain and Industrial Park Operators

The bank embeds branches and relationship teams inside 120+ industrial parks across Zhejiang, capturing SME panels tied to 30 major anchor manufacturers and originating about CNY 18.5bn in supply-chain loans in 2024, boosting high-quality client access and loan book yield.

These partnerships enable tailored trade finance and inventory financing—average ticket CNY 3.2m—reducing default rates by ~40% versus standalone SME lending.

- 120+ parks covered

- CNY 18.5bn supply-chain loans (2024)

- 30 anchor manufacturers

- Avg ticket CNY 3.2m

- ~40% lower default rate

OCBC & Zhejiang tie-up: Low‑cost liquidity, 1.35% NPLs, >¥5tn clearing & CNY 120bn deals

OCBC (12.2% since 2016) supplies cross‑border cash, risk models and compliance, cutting NPLs to 1.35% by 2024 and lifting CET1 planning; Zhejiang gov’t deposits (~CNY 420bn by 2025) provide low‑cost liquidity and ~CNY 85bn project lending (2024–25). Tech and clearing ties (CIPS/CNAPS/SWIFT) process >¥5tn/yr, support ~¥120bn syndicated exposure and CNY 18.5bn supply‑chain loans (2024).

| Partner | Role | Key metric |

|---|---|---|

| OCBC | Risk, cross‑border services | 12.2% stake; NPL 1.35% (2024) |

| Zhejiang gov’ts | Deposits, project lending | CNY 420bn deposits (2025); CNY 85bn loans |

| Clearing/tech | Payments, IT | >¥5tn/yr; 30% IT latency cut |

| Banks (syndication) | Capital, IB mandates | ~¥120bn syndicated (2024) |

| Industrial parks | SME origination | 120+ parks; CNY 18.5bn supply‑chain (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Bank of Ningbo covering customer segments, value propositions, channels, key activities, resources, partnerships, cost structure and revenue streams, reflecting real-world banking operations and competitive advantages; ideal for presentations, investor discussions and strategic decision-making with SWOT-linked insights and polished, analyst-ready narrative.

High-level view of Bank of Ningbo’s business model with editable cells, condensing retail, corporate, and digital banking strategies into a clean one-page snapshot for quick boardroom review and collaborative adaptation.

Activities

Credit Risk Assessment and Management

Bank of Ningbo conducts rigorous credit analysis, keeping its 2024 year-end non-performing loan (NPL) ratio at 0.88%, well below the 1.5% sector average, which supports lower pricing for top-tier borrowers.

Continuous borrower monitoring uses big data models processing transaction, payment and POS feeds; early-warning alerts cut 90-day default emergence by an estimated 35% in 2024, anchoring portfolio stability.

Digital Banking and Technology Innovation

Bank of Ningbo prioritizes a resilient mobile and online banking ecosystem, with 2025 figures showing digital channels account for 68% of retail transactions and mobile active users up 22% year-over-year to 8.4 million; R&D spend rose 14% in 2024 to CNY 1.2 billion to automate back-office processes and improve UX. Ongoing infrastructure updates cut online latency by 40ms and expanded self-service products to 120 offerings, while security investments reduced fraud losses 28%.

Wealth Management Product Development

Designing and managing a diverse suite of structured products, mutual funds, and insurance-linked offerings helps Bank of Ningbo attract and retain HNW clients, driving fee income—wealth management fees rose 18% in 2024 to RMB 3.6 billion. The bank’s product research team monitors FX, rates, and equities and launched 42 new products in 2024, strengthening its position as a premier regional wealth manager.

Small and Medium Enterprise Lending

Regional Market Expansion and Optimization

Bank of Ningbo: Digital-led growth, low NPLs and RMB3.6bn wealth fees

Bank of Ningbo runs strict credit and SME cash-flow lending, digital-first retail banking, proactive monitoring (2024 NPL 0.88%, SME NPL 1.15%), and expanded wealth/product offerings (wealth fees RMB 3.6bn, 42 new products in 2024) to drive fee income and portfolio stability.

| Metric | 2024 | H1 2025 |

|---|---|---|

| NPL ratio | 0.88% | — |

| SME share | 23% | — |

| SME NPL | 1.15% | — |

| Wealth fees | RMB 3.6bn | — |

| Digital txns | 68% | Mobile users 8.4m |

Delivered as Displayed

Business Model Canvas

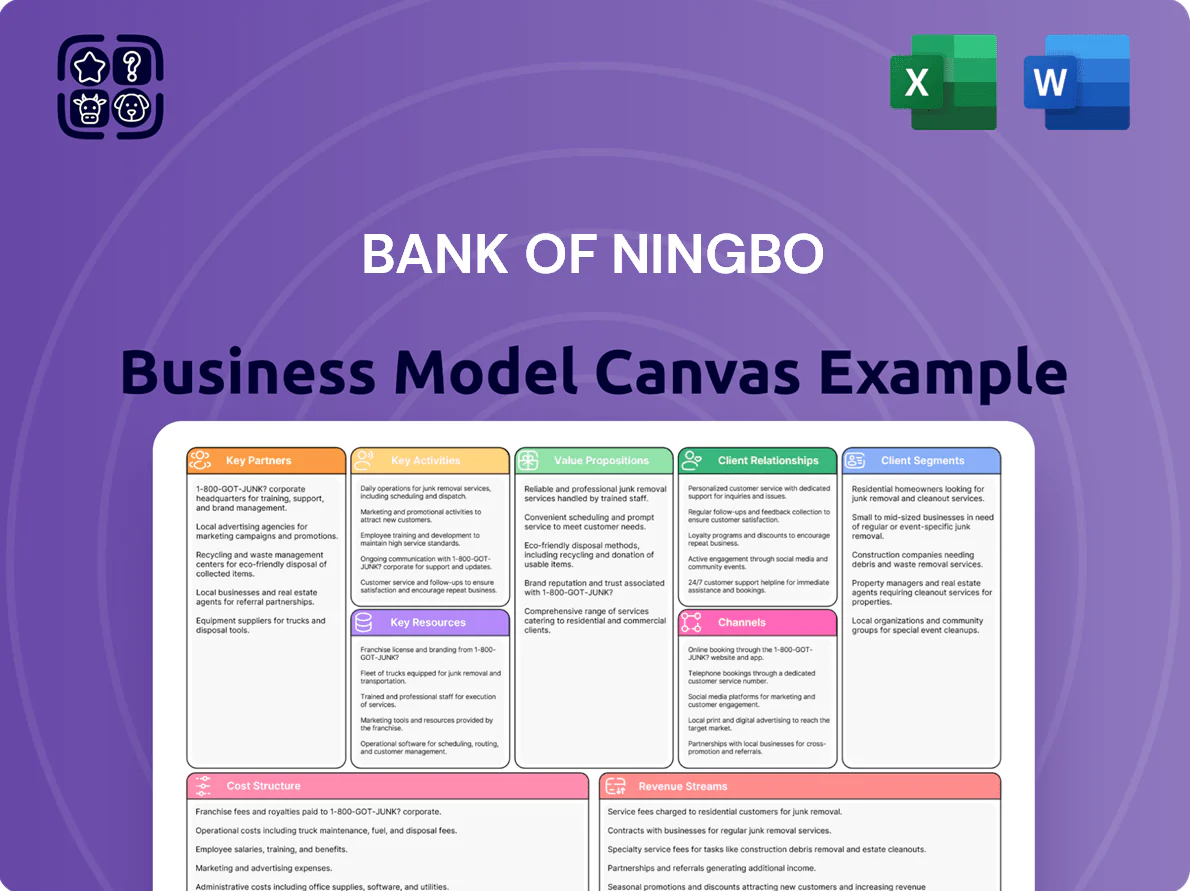

The document you're previewing is the actual Bank of Ningbo Business Model Canvas you will receive—this is not a mockup or sample but a direct snapshot of the final deliverable; upon purchase you’ll download the complete, editable file formatted exactly as shown, ready for presentation, analysis, and implementation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Bank of Ningbo: Actionable Business Model Canvas for Investors & Strategists

Unlock the full strategic blueprint behind Bank of Ningbo’s business model — a concise, actionable Business Model Canvas that maps its value propositions, customer segments, revenue streams, and key partnerships.

Perfect for investors, consultants, and strategists, this downloadable Word/Excel file reveals operational levers, growth opportunities, and risks to help you benchmark or build winning financial strategies.

Partnerships

Strategic Alliance with OCBC Bank

As a major shareholder, OCBC Bank (Singapore) supplies Bank of Ningbo with international risk and wealth-management expertise, backing upgraded credit-risk models and cross-border compliance frameworks used since OCBC took a 12.2% stake in 2016; this raised BIS CET1 planning and reduced nonperforming loans to 1.35% by 2024. The tie lets Bank of Ningbo offer OCBC’s global cash‑management and trade services to clients expanding beyond China, boosting Yangtze River Delta multinational coverage and cross-border fee income.

Local Government and Public Sector Entities

The bank holds long-standing ties with Zhejiang and other provinces, acting as primary fiscal agent for municipal accounts and social security funds—handling over CNY 420 billion in government deposits as of 2025, which supplies low-cost funding and liquidity. These links secure priority lending into state-backed infrastructure and development zones, where Bank of Ningbo underwrote roughly CNY 85 billion in project loans in 2024–2025.

Fintech and Digital Infrastructure Providers

Collaborations with leading tech firms let Bank of Ningbo embed AI and cloud computing into core systems, supporting automated credit scoring that cut default prediction error by ~12% in 2024 and reducing IT latency 30% after a 2023 cloud migration.

Interbank and Financial Institution Networks

Membership in national and international clearing networks (CIPS, CNAPS, SWIFT) enables Bank of Ningbo to process >¥5tn annual payments and optimize liquidity across corridors, reducing settlement times and intraday funding needs.

Partnerships with banks for syndicated loans and interbank lending diversify assets—~¥120bn syndicated exposure in 2024—and support complex investment-banking mandates and institutional capital flows.

- Clearing networks: CIPS, CNAPS, SWIFT

- Payments processed: >¥5tn/year (2024)

- Syndicated exposure: ~¥120bn (2024)

- Use: liquidity mgmt, settlement speed, IB mandates

Supply Chain and Industrial Park Operators

The bank embeds branches and relationship teams inside 120+ industrial parks across Zhejiang, capturing SME panels tied to 30 major anchor manufacturers and originating about CNY 18.5bn in supply-chain loans in 2024, boosting high-quality client access and loan book yield.

These partnerships enable tailored trade finance and inventory financing—average ticket CNY 3.2m—reducing default rates by ~40% versus standalone SME lending.

- 120+ parks covered

- CNY 18.5bn supply-chain loans (2024)

- 30 anchor manufacturers

- Avg ticket CNY 3.2m

- ~40% lower default rate

OCBC & Zhejiang tie-up: Low‑cost liquidity, 1.35% NPLs, >¥5tn clearing & CNY 120bn deals

OCBC (12.2% since 2016) supplies cross‑border cash, risk models and compliance, cutting NPLs to 1.35% by 2024 and lifting CET1 planning; Zhejiang gov’t deposits (~CNY 420bn by 2025) provide low‑cost liquidity and ~CNY 85bn project lending (2024–25). Tech and clearing ties (CIPS/CNAPS/SWIFT) process >¥5tn/yr, support ~¥120bn syndicated exposure and CNY 18.5bn supply‑chain loans (2024).

| Partner | Role | Key metric |

|---|---|---|

| OCBC | Risk, cross‑border services | 12.2% stake; NPL 1.35% (2024) |

| Zhejiang gov’ts | Deposits, project lending | CNY 420bn deposits (2025); CNY 85bn loans |

| Clearing/tech | Payments, IT | >¥5tn/yr; 30% IT latency cut |

| Banks (syndication) | Capital, IB mandates | ~¥120bn syndicated (2024) |

| Industrial parks | SME origination | 120+ parks; CNY 18.5bn supply‑chain (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Bank of Ningbo covering customer segments, value propositions, channels, key activities, resources, partnerships, cost structure and revenue streams, reflecting real-world banking operations and competitive advantages; ideal for presentations, investor discussions and strategic decision-making with SWOT-linked insights and polished, analyst-ready narrative.

High-level view of Bank of Ningbo’s business model with editable cells, condensing retail, corporate, and digital banking strategies into a clean one-page snapshot for quick boardroom review and collaborative adaptation.

Activities

Credit Risk Assessment and Management

Bank of Ningbo conducts rigorous credit analysis, keeping its 2024 year-end non-performing loan (NPL) ratio at 0.88%, well below the 1.5% sector average, which supports lower pricing for top-tier borrowers.

Continuous borrower monitoring uses big data models processing transaction, payment and POS feeds; early-warning alerts cut 90-day default emergence by an estimated 35% in 2024, anchoring portfolio stability.

Digital Banking and Technology Innovation

Bank of Ningbo prioritizes a resilient mobile and online banking ecosystem, with 2025 figures showing digital channels account for 68% of retail transactions and mobile active users up 22% year-over-year to 8.4 million; R&D spend rose 14% in 2024 to CNY 1.2 billion to automate back-office processes and improve UX. Ongoing infrastructure updates cut online latency by 40ms and expanded self-service products to 120 offerings, while security investments reduced fraud losses 28%.

Wealth Management Product Development

Designing and managing a diverse suite of structured products, mutual funds, and insurance-linked offerings helps Bank of Ningbo attract and retain HNW clients, driving fee income—wealth management fees rose 18% in 2024 to RMB 3.6 billion. The bank’s product research team monitors FX, rates, and equities and launched 42 new products in 2024, strengthening its position as a premier regional wealth manager.

Small and Medium Enterprise Lending

Regional Market Expansion and Optimization

Bank of Ningbo: Digital-led growth, low NPLs and RMB3.6bn wealth fees

Bank of Ningbo runs strict credit and SME cash-flow lending, digital-first retail banking, proactive monitoring (2024 NPL 0.88%, SME NPL 1.15%), and expanded wealth/product offerings (wealth fees RMB 3.6bn, 42 new products in 2024) to drive fee income and portfolio stability.

| Metric | 2024 | H1 2025 |

|---|---|---|

| NPL ratio | 0.88% | — |

| SME share | 23% | — |

| SME NPL | 1.15% | — |

| Wealth fees | RMB 3.6bn | — |

| Digital txns | 68% | Mobile users 8.4m |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Bank of Ningbo Business Model Canvas you will receive—this is not a mockup or sample but a direct snapshot of the final deliverable; upon purchase you’ll download the complete, editable file formatted exactly as shown, ready for presentation, analysis, and implementation.