Nefab AB Porter's Five Forces Analysis

From Overview to Strategy Blueprint

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nefab AB’s competitive dynamics, market pressures, and strategic advantages in detail.

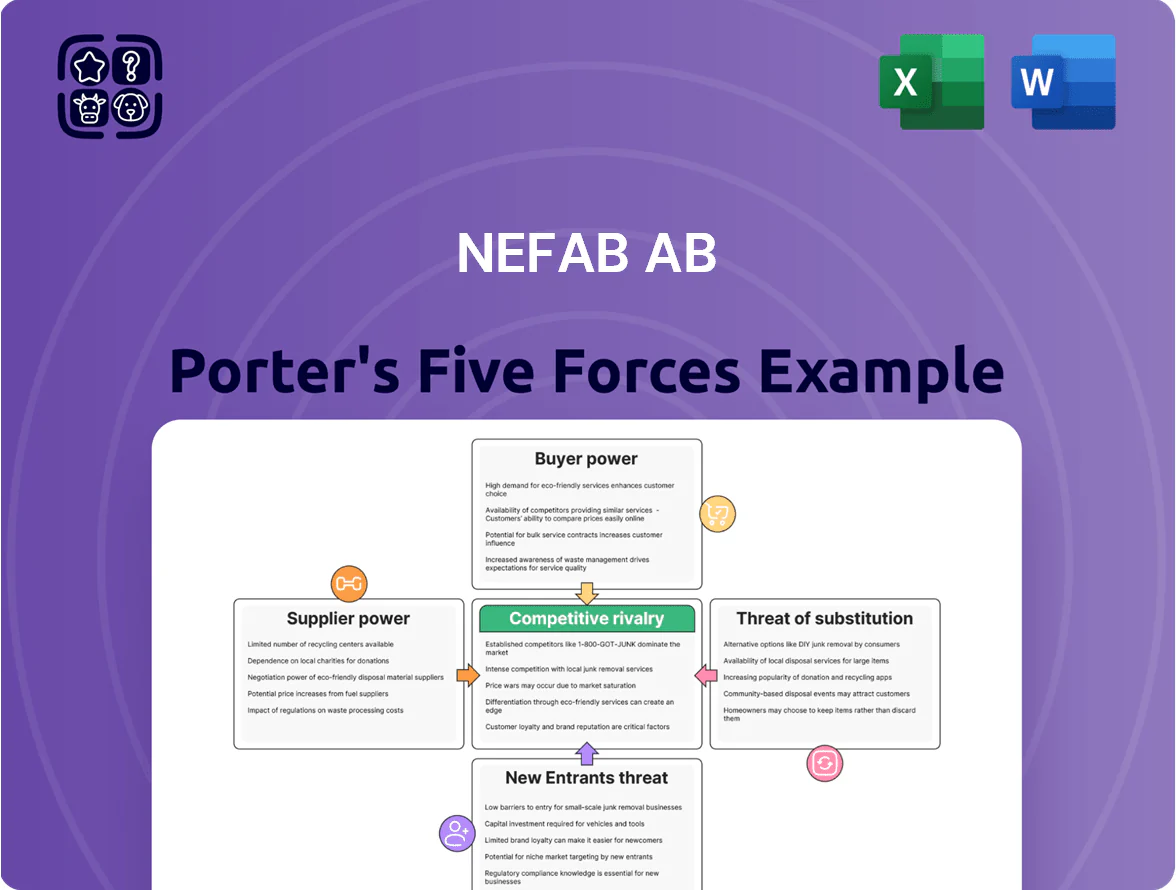

Suppliers Bargaining Power

Raw material price volatility for multi-material inputs

Nefab uses wood, steel, foam and plastics; global commodity volatility pushed input costs up ~12% YoY by end-2025, lifting COGS pressure across packaging lines.

The multi-material mix lowers single-supplier risk, but specialized foam and engineered plastics makers kept price premiums of 5–8% during 2025 supply shocks.

Overall supplier bargaining power is moderate: diversified sourcing helps, yet concentrated specialist suppliers retain leverage in disruption periods.

Geographic concentration of specialized component providers

Certain high-tech packaging components and specialized foams come from few global suppliers, boosting supplier bargaining power; industry data shows top 5 foam suppliers control ~60% of specialty foam capacity (2024). Nefab must tightly manage supplier relationships to secure quality and uptime across ~30 global production sites. Its scale yields volume discounts—estimated savings 5–10%—but strict technical specs keep the qualified vendor pool small.

Impact of sustainability and ESG compliance on sourcing

As of 2025, Nefab’s push to cut emissions forces procurement from suppliers meeting strict carbon and ethical standards, shrinking the pool to certified providers; FSC-certified wood and recycled plastics now form >40% of Nefab’s sustainable material purchases.

Those certified suppliers charge premiums—typically 5–15% higher—because certification is required for Nefab’s Scope 3 targets and for meeting major clients’ ESG specs, raising input costs and supplier bargaining power.

Logistics and energy cost dependencies

Suppliers of timber and steel pass volatile energy and transport costs to manufacturers; European energy price spikes in 2022 raised steel input costs by ~30% year-over-year, squeezing margins for packagers like Nefab AB (SE: NEFAB) in 2022–24.

Nefab’s global inbound network is sensitive to regional fuel prices and policies—diesel averages varied 20–35% between major regions in 2024—creating indirect supplier power as logistics costs act like a fixed margin floor.

- Timber/steel cost rise ~30% (2022 YoY)

- Diesel price spread 20–35% across regions (2024)

- Logistics as fixed margin constraint on gross margin

Switching costs between specialized material vendors

Switching specialized-material suppliers requires 8–16 weeks for validation, testing, and QA, so Nefab AB (STO: NEFAB) faces long lead times that hamper quick vendor changes.

In healthcare and telecom, where packaging failure rates must stay below 0.1%, Nefab risks product integrity and regulatory issues if it swaps vendors, raising supplier leverage.

This technical dependency lets incumbent suppliers demand longer contracts and price premiums; typical supplier contract lengths in 2024 averaged 24–36 months with 3–7% annual price escalators in engineered packaging.

- Validation lead time: 8–16 weeks

- Failure-rate tolerance: <0.1% in target sectors

- Typical contract: 24–36 months

- Common price escalator: 3–7% p.a.

Moderate supplier power: specialty premiums, long contracts, 8–16wk switches

Supplier power: moderate—diversified materials cut single-supplier risk, but specialty foam/plastics and certified suppliers hold leverage, causing 5–15% premiums and 8–16 week switching. Volume scale gives Nefab ~5–10% discounts, yet tight specs and long contracts (24–36 months, 3–7% escalators) keep bargaining power elevated during disruptions.

| Metric | Value |

|---|---|

| Input cost rise (2025 YoY) | ~12% |

| Specialty supplier market share | Top‑5 foam 60% (2024) |

| Certified material share | >40% (2025) |

| Switch lead time | 8–16 weeks |

| Typical contract | 24–36 months |

What is included in the product

Tailored Porter's Five Forces analysis for Nefab AB uncovering competitive drivers, supplier and buyer power, entry barriers, substitution risks, and strategic levers to protect margins and market position—fully editable for reports and presentations.

A concise Porter's Five Forces snapshot for Nefab AB—quickly identify supplier, buyer, rivalry, entrant, and substitute pressures to streamline strategic choices.

Customers Bargaining Power

Concentration of large multinational industrial clients

Nefab serves major telecom, energy and automotive firms where the top 10 customers account for roughly 55–65% of revenue, giving buyers strong price leverage and the ability to demand bespoke solutions.

These sophisticated clients push for higher service levels and customization, raising Nefab’s per-order costs while limiting price increases; gross margins in packaging fell ~120–180 bps for suppliers facing such demand in 2024.

By late 2025, large customers increasingly contract integrated logistics-plus-packaging deals—analysts estimate this shifts ~30% of spend to logistics partners, squeezing standalone packaging margins further.

Demand for total cost of ownership reductions

Customers now demand partners that cut total cost of ownership (TCO) via smarter packaging design; 68% of global manufacturers surveyed in 2024 said packaging redesign reduced logistics costs by at least 10%.

Nefab’s offering centers on TCO reduction through engineered packaging and reusable solutions, so buyers expect ongoing efficiency gains and price pass‑backs.

That expectation forces Nefab to innovate continually—R&D and pilot projects must sustain double‑digit annual savings to defend pricing and supply‑chain positioning.

Low switching costs for standardized packaging products

While Nefab’s custom-engineered packaging keeps clients sticky, standardized components face high buyer power because switching costs are low; buyers can replace basic wooden crates or corrugated boxes within weeks. In 2024 packaging commoditization saw prices fall ~3–5% in Europe, so Nefab must stay price-competitive or lose volume. That pressure pushes investment into engineering services and value-added logistics; in 2023 Nefab reported 18% of revenue from engineered solutions, helping protect margins.

Transparency in sustainability and carbon reporting

Industrial buyers now demand detailed Life Cycle Analysis (LCA) for Scope 3 reporting; 72% of procurement teams in manufacturing say supplier sustainability data is critical to sourcing decisions (2024 Deloitte Global CPO Survey).

Buyers can force transparency across packaging flows and will switch suppliers if Nefab’s environmental data lags competitors; 38% of firms shifted suppliers in 2023 citing better carbon performance.

If Nefab cannot supply verified LCA and third-party carbon footprints, contract loss risk rises as green alternatives gain price parity.

- 72% of procurement teams require supplier sustainability data

- 38% of firms switched suppliers for better carbon performance (2023)

- Verified LCA and third-party audits now a buying prerequisite

- Failure to match peers raises contract-loss and churn risk

Integration into customer digital supply chains

Large industrial customers now link ERP and inventory systems to packaging suppliers for just-in-time delivery, creating digital lock-in that raises switching costs and boosts customer bargaining power.

Such integrations force Nefab AB to offer seamless APIs and real-time data sharing; 2024 surveys show 62% of manufacturers rank supplier data transparency as a top retention factor.

Failing to match these digital interfaces risks losing high-value accounts that demand operational visibility and reduced lead times.

- Digital lock-in raises switching costs

- 62% of manufacturers value supplier data transparency (2024)

- APIs and real-time sharing are retention basics

Concentrated buyers squeeze margins, drive customization, and force sustainability shifts

Buyers hold high leverage: top 10 clients = ~55–65% revenue, push customization and TCO cuts, pressuring margins (packaging margins down ~120–180 bps for suppliers in 2024). Digital/ERP integrations raise switching costs but buyers still replace commoditized items (prices fell ~3–5% Europe 2024). Sustainability and verified LCA now buying musts (72% require data; 38% switched suppliers 2023).

| Metric | Value |

|---|---|

| Top-10 share | 55–65% |

| Margin pressure | -120–180 bps (2024) |

| Price fall (EU) | -3–5% (2024) |

| Require sustainability data | 72% (2024) |

| Switched for carbon | 38% (2023) |

Preview the Actual Deliverable

Nefab AB Porter's Five Forces Analysis

This preview shows the exact Nefab AB Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is the same fully formatted, professionally written file included with your purchase, ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nefab AB’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility for multi-material inputs

Nefab uses wood, steel, foam and plastics; global commodity volatility pushed input costs up ~12% YoY by end-2025, lifting COGS pressure across packaging lines.

The multi-material mix lowers single-supplier risk, but specialized foam and engineered plastics makers kept price premiums of 5–8% during 2025 supply shocks.

Overall supplier bargaining power is moderate: diversified sourcing helps, yet concentrated specialist suppliers retain leverage in disruption periods.

Geographic concentration of specialized component providers

Certain high-tech packaging components and specialized foams come from few global suppliers, boosting supplier bargaining power; industry data shows top 5 foam suppliers control ~60% of specialty foam capacity (2024). Nefab must tightly manage supplier relationships to secure quality and uptime across ~30 global production sites. Its scale yields volume discounts—estimated savings 5–10%—but strict technical specs keep the qualified vendor pool small.

Impact of sustainability and ESG compliance on sourcing

As of 2025, Nefab’s push to cut emissions forces procurement from suppliers meeting strict carbon and ethical standards, shrinking the pool to certified providers; FSC-certified wood and recycled plastics now form >40% of Nefab’s sustainable material purchases.

Those certified suppliers charge premiums—typically 5–15% higher—because certification is required for Nefab’s Scope 3 targets and for meeting major clients’ ESG specs, raising input costs and supplier bargaining power.

Logistics and energy cost dependencies

Suppliers of timber and steel pass volatile energy and transport costs to manufacturers; European energy price spikes in 2022 raised steel input costs by ~30% year-over-year, squeezing margins for packagers like Nefab AB (SE: NEFAB) in 2022–24.

Nefab’s global inbound network is sensitive to regional fuel prices and policies—diesel averages varied 20–35% between major regions in 2024—creating indirect supplier power as logistics costs act like a fixed margin floor.

- Timber/steel cost rise ~30% (2022 YoY)

- Diesel price spread 20–35% across regions (2024)

- Logistics as fixed margin constraint on gross margin

Switching costs between specialized material vendors

Switching specialized-material suppliers requires 8–16 weeks for validation, testing, and QA, so Nefab AB (STO: NEFAB) faces long lead times that hamper quick vendor changes.

In healthcare and telecom, where packaging failure rates must stay below 0.1%, Nefab risks product integrity and regulatory issues if it swaps vendors, raising supplier leverage.

This technical dependency lets incumbent suppliers demand longer contracts and price premiums; typical supplier contract lengths in 2024 averaged 24–36 months with 3–7% annual price escalators in engineered packaging.

- Validation lead time: 8–16 weeks

- Failure-rate tolerance: <0.1% in target sectors

- Typical contract: 24–36 months

- Common price escalator: 3–7% p.a.

Moderate supplier power: specialty premiums, long contracts, 8–16wk switches

Supplier power: moderate—diversified materials cut single-supplier risk, but specialty foam/plastics and certified suppliers hold leverage, causing 5–15% premiums and 8–16 week switching. Volume scale gives Nefab ~5–10% discounts, yet tight specs and long contracts (24–36 months, 3–7% escalators) keep bargaining power elevated during disruptions.

| Metric | Value |

|---|---|

| Input cost rise (2025 YoY) | ~12% |

| Specialty supplier market share | Top‑5 foam 60% (2024) |

| Certified material share | >40% (2025) |

| Switch lead time | 8–16 weeks |

| Typical contract | 24–36 months |

What is included in the product

Tailored Porter's Five Forces analysis for Nefab AB uncovering competitive drivers, supplier and buyer power, entry barriers, substitution risks, and strategic levers to protect margins and market position—fully editable for reports and presentations.

A concise Porter's Five Forces snapshot for Nefab AB—quickly identify supplier, buyer, rivalry, entrant, and substitute pressures to streamline strategic choices.

Customers Bargaining Power

Concentration of large multinational industrial clients

Nefab serves major telecom, energy and automotive firms where the top 10 customers account for roughly 55–65% of revenue, giving buyers strong price leverage and the ability to demand bespoke solutions.

These sophisticated clients push for higher service levels and customization, raising Nefab’s per-order costs while limiting price increases; gross margins in packaging fell ~120–180 bps for suppliers facing such demand in 2024.

By late 2025, large customers increasingly contract integrated logistics-plus-packaging deals—analysts estimate this shifts ~30% of spend to logistics partners, squeezing standalone packaging margins further.

Demand for total cost of ownership reductions

Customers now demand partners that cut total cost of ownership (TCO) via smarter packaging design; 68% of global manufacturers surveyed in 2024 said packaging redesign reduced logistics costs by at least 10%.

Nefab’s offering centers on TCO reduction through engineered packaging and reusable solutions, so buyers expect ongoing efficiency gains and price pass‑backs.

That expectation forces Nefab to innovate continually—R&D and pilot projects must sustain double‑digit annual savings to defend pricing and supply‑chain positioning.

Low switching costs for standardized packaging products

While Nefab’s custom-engineered packaging keeps clients sticky, standardized components face high buyer power because switching costs are low; buyers can replace basic wooden crates or corrugated boxes within weeks. In 2024 packaging commoditization saw prices fall ~3–5% in Europe, so Nefab must stay price-competitive or lose volume. That pressure pushes investment into engineering services and value-added logistics; in 2023 Nefab reported 18% of revenue from engineered solutions, helping protect margins.

Transparency in sustainability and carbon reporting

Industrial buyers now demand detailed Life Cycle Analysis (LCA) for Scope 3 reporting; 72% of procurement teams in manufacturing say supplier sustainability data is critical to sourcing decisions (2024 Deloitte Global CPO Survey).

Buyers can force transparency across packaging flows and will switch suppliers if Nefab’s environmental data lags competitors; 38% of firms shifted suppliers in 2023 citing better carbon performance.

If Nefab cannot supply verified LCA and third-party carbon footprints, contract loss risk rises as green alternatives gain price parity.

- 72% of procurement teams require supplier sustainability data

- 38% of firms switched suppliers for better carbon performance (2023)

- Verified LCA and third-party audits now a buying prerequisite

- Failure to match peers raises contract-loss and churn risk

Integration into customer digital supply chains

Large industrial customers now link ERP and inventory systems to packaging suppliers for just-in-time delivery, creating digital lock-in that raises switching costs and boosts customer bargaining power.

Such integrations force Nefab AB to offer seamless APIs and real-time data sharing; 2024 surveys show 62% of manufacturers rank supplier data transparency as a top retention factor.

Failing to match these digital interfaces risks losing high-value accounts that demand operational visibility and reduced lead times.

- Digital lock-in raises switching costs

- 62% of manufacturers value supplier data transparency (2024)

- APIs and real-time sharing are retention basics

Concentrated buyers squeeze margins, drive customization, and force sustainability shifts

Buyers hold high leverage: top 10 clients = ~55–65% revenue, push customization and TCO cuts, pressuring margins (packaging margins down ~120–180 bps for suppliers in 2024). Digital/ERP integrations raise switching costs but buyers still replace commoditized items (prices fell ~3–5% Europe 2024). Sustainability and verified LCA now buying musts (72% require data; 38% switched suppliers 2023).

| Metric | Value |

|---|---|

| Top-10 share | 55–65% |

| Margin pressure | -120–180 bps (2024) |

| Price fall (EU) | -3–5% (2024) |

| Require sustainability data | 72% (2024) |

| Switched for carbon | 38% (2023) |

Preview the Actual Deliverable

Nefab AB Porter's Five Forces Analysis

This preview shows the exact Nefab AB Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is the same fully formatted, professionally written file included with your purchase, ready for download and use the moment you buy.