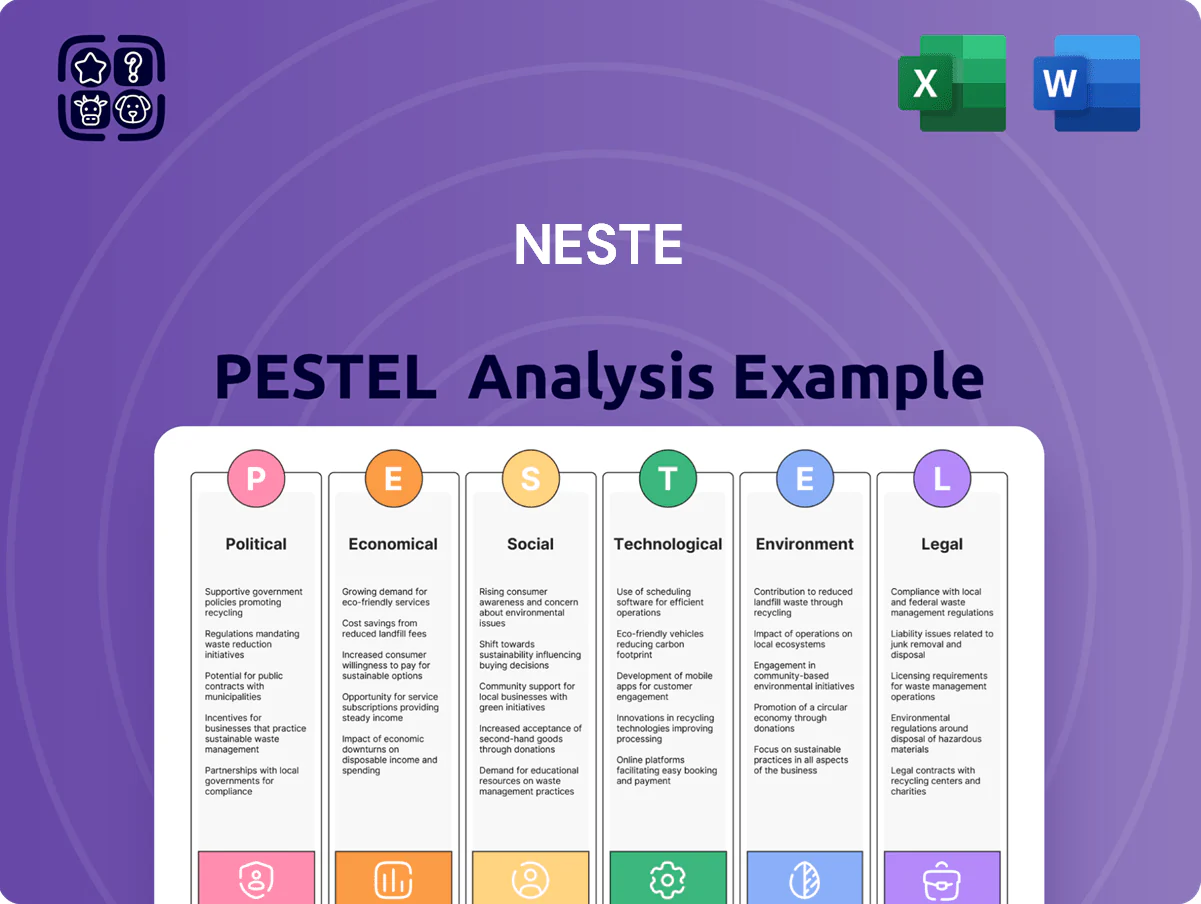

Neste PESTLE Analysis

Skip the Research. Get the Strategy.

Navigate Neste’s future with our concise PESTLE snapshot—spot regulatory pressures, economic drivers, and tech trends shaping its renewable fuels leadership. Perfect for investors and strategists, this ready-to-use briefing highlights risks and opportunity areas. Purchase the full PESTLE to unlock detailed, actionable insights and editable files for immediate strategic use.

Political factors

EU Regulatory Frameworks

The ReFuelEU Aviation and FuelEU Maritime mandates, due end-2025, create predictable demand for Neste's renewable jet and marine fuels; EU targets foresee 2% SAF by 2025 rising to 5% by 2030 for aviation and increasing GHG reduction obligations for maritime, supporting Neste’s €5.7bn 2024 revenue from renewable products.

United States Policy Stability

The Inflation Reduction Act’s production and SAF tax credits have underpinned Neste’s North American expansion, supporting planned 2024–2025 capacity additions tied to roughly $1.5–2.0 billion in project investment and expected incremental revenues; IRS guidance through 2025 secures these incentives. Political shifts could inject uncertainty, but existing credits for sustainable aviation fuel and renewable diesel bolster Neste’s competitive position versus petro-refiners. Bipartisan emphasis on energy independence and domestic fuel production—reflected in 2024 congressional appropriations and DOE funding—remains a stabilizing political factor for U.S. operations.

Geopolitical Supply Chain Security

Ongoing geopolitical tensions in Eastern Europe and the Middle East have tightened energy supply chains and constrained certain feedstock flows, contributing to a 12% year-on-year increase in feedstock logistics costs for refiners in 2024; Neste has diversified sourcing across Europe, North America and Southeast Asia to reduce exposure, sourcing over 30% of renewable feedstocks outside traditional regions by late 2025.

Finnish Government Stakeholder Influence

As 39.3% state-owned (2025), Neste's strategy is tightly tied to Finland's push for carbon neutrality by 2035, aligning its renewable fuels and circular solutions with national targets while exposing it to political oversight and policy shifts.

This anchoring secures Neste as a pillar of Finland's industrial policy—2024 renewable product sales €8.6bn—forcing trade-offs between commercial returns and public climate objectives.

- State ownership 39.3% (2025)

- Carbon neutrality target 2035

- Renewable sales €8.6bn (2024)

- High public/political scrutiny

Global Trade Barriers and Feedstock Protectionism

Neste faces rising export restrictions on waste and residue feedstocks like used cooking oil, as countries protect domestic renewable industries; Indonesia, for example, introduced export levies in 2022 and tightened controls that affected global supplies.

These measures constrain low-cost raw material access, pressuring Neste’s margins given feedstock costs represented roughly 60–70% of renewable diesel production costs in 2024.

Maintaining diplomatic engagement and trade advocacy through 2026 is critical for Neste to secure cross-border feedstock flows and mitigate supply shocks.

- Indonesia export controls since 2022 reduced UCO exports by an estimated 20–30% in 2023–24

- Feedstock costs ≈60–70% of renewable diesel production cost (2024)

- Neste needs active trade diplomacy to protect global sourcing into 2026

Neste poised for SAF growth as EU/US policies boost demand despite rising feedstock costs

EU mandates (ReFuelEU, FuelEU) and US IRA credits drive demand and investment for Neste’s SAF and renewable fuels; state ownership 39.3% (2025) aligns company with Finland’s 2035 carbon neutrality target; feedstock export controls (eg. Indonesia since 2022) and geopolitical tensions raised feedstock logistics costs ~12% YoY (2024) and feedstock share 60–70% of production cost.

| Indicator | Value |

|---|---|

| State ownership (2025) | 39.3% |

| Renewable sales (2024) | €8.6bn |

| Feedstock share of cost (2024) | 60–70% |

| Feedstock logistics cost change (2024) | +12% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect Neste across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

Summarized PESTLE insights for Neste, neatly organized by category to ease meeting prep and enable quick insertion into presentations or strategy packs.

Economic factors

Feedstock Price Volatility

The cost of waste and residue feedstocks remained Neste's key economic variable at end-2025, with used cooking oil and animal fats prices up ~18% year-on-year, pushing input costs higher and compressing margins. Competition from oil majors and chemical firms increased demand for limited 2025 feedstock volumes, contributing to price volatility and a 12% rise in feedstock sourcing expenses. Neste's advanced sourcing network and pre-treatment tech reduced yield losses, supporting a 3-4 percentage point improvement in processing efficiency and helping protect EBITDA against raw-material swings.

Sustainable Aviation Fuel Market Expansion

Interest Rates and Capital Expenditure

The elevated global policy rates at end-2025—ECB depo 3.75%, US Fed funds 5.25%—raise borrowing costs for Neste, increasing weighted average cost of capital for its refinery and renewable hydrogen projects. Higher interest expense necessitates disciplined capital allocation and net debt/EBITDA targets; Neste reported net debt/EBITDA ~0.6x in 2024, supporting financing flexibility. Planned capacity ramps in Singapore and Rotterdam, expected to reach full operation in 2025–26, are projected to lift EBITDA margins and deliver multi-year ROI that offsets higher financing costs.

Fossil Fuel Price Parity

The price of crude oil strongly affects demand for Neste’s renewable diesel and SAF; Brent averaged about 95 USD/bbl in 2024, making renewables more competitive and boosting Neste’s margins and volumes.

When oil drops—as in 2020–21 shocks or sub‑$60 USD/bbl periods—renewables need stronger carbon pricing or mandates; EU ETS carbon prices around 90–100 EUR/t in 2024 partially offset this.

Global Inflationary Pressures

Inflation in 2025 raised Neste’s labor, logistics and energy costs by roughly 6–9% year-on-year, squeezing margins and increasing operating expenses across refineries and supply chains.

Neste accelerated operational excellence and digital transformation projects, targeting a 3–4% cost-to-serve reduction and automated logistics to protect EBITDA.

Efficient global supply-chain management is critical to keep end-product prices competitive for customers across Europe, Asia and North America amid volatile freight and energy prices.

- 2025 labor/logistics/energy inflation: ~6–9%

- Targeted cost-to-serve reduction via digitalization: 3–4%

- Focus regions: Europe, Asia, North America

Neste faces margin squeeze as feedstock costs surge 18% while SAF ramp meets mixed pricing

Key economic drivers for Neste in 2024–25: feedstock costs up ~18% YoY, raising sourcing spend ~12% and pressuring margins; SAF capacity >2.5 Mt with 30–40% long‑term offtake, SAF premium $0.40–0.80/L; Brent ~95 USD/bbl (2024) and EU ETS ~90–100 EUR/t; interest rates higher (ECB 3.75%, Fed 5.25%), net debt/EBITDA ~0.6x; 2025 inflation increased OPEX ~6–9%, targeted cost-to-serve cut 3–4%.

| Metric | 2024–25 |

|---|---|

| Feedstock price change | +18% YoY |

| Feedstock spend | +12% |

| SAF capacity | >2.5 Mt |

| SAF premium | $0.40–0.80/L |

| Brent | ~95 USD/bbl |

| EU ETS | ~90–100 EUR/t |

| Rates (ECB/Fed) | 3.75% / 5.25% |

| Net debt/EBITDA | ~0.6x |

| Inflation impact | +6–9% OPEX |

| Cost-to-serve target | -3–4% |

Full Version Awaits

Neste PESTLE Analysis

The preview shown here is the exact Neste PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Navigate Neste’s future with our concise PESTLE snapshot—spot regulatory pressures, economic drivers, and tech trends shaping its renewable fuels leadership. Perfect for investors and strategists, this ready-to-use briefing highlights risks and opportunity areas. Purchase the full PESTLE to unlock detailed, actionable insights and editable files for immediate strategic use.

Political factors

EU Regulatory Frameworks

The ReFuelEU Aviation and FuelEU Maritime mandates, due end-2025, create predictable demand for Neste's renewable jet and marine fuels; EU targets foresee 2% SAF by 2025 rising to 5% by 2030 for aviation and increasing GHG reduction obligations for maritime, supporting Neste’s €5.7bn 2024 revenue from renewable products.

United States Policy Stability

The Inflation Reduction Act’s production and SAF tax credits have underpinned Neste’s North American expansion, supporting planned 2024–2025 capacity additions tied to roughly $1.5–2.0 billion in project investment and expected incremental revenues; IRS guidance through 2025 secures these incentives. Political shifts could inject uncertainty, but existing credits for sustainable aviation fuel and renewable diesel bolster Neste’s competitive position versus petro-refiners. Bipartisan emphasis on energy independence and domestic fuel production—reflected in 2024 congressional appropriations and DOE funding—remains a stabilizing political factor for U.S. operations.

Geopolitical Supply Chain Security

Ongoing geopolitical tensions in Eastern Europe and the Middle East have tightened energy supply chains and constrained certain feedstock flows, contributing to a 12% year-on-year increase in feedstock logistics costs for refiners in 2024; Neste has diversified sourcing across Europe, North America and Southeast Asia to reduce exposure, sourcing over 30% of renewable feedstocks outside traditional regions by late 2025.

Finnish Government Stakeholder Influence

As 39.3% state-owned (2025), Neste's strategy is tightly tied to Finland's push for carbon neutrality by 2035, aligning its renewable fuels and circular solutions with national targets while exposing it to political oversight and policy shifts.

This anchoring secures Neste as a pillar of Finland's industrial policy—2024 renewable product sales €8.6bn—forcing trade-offs between commercial returns and public climate objectives.

- State ownership 39.3% (2025)

- Carbon neutrality target 2035

- Renewable sales €8.6bn (2024)

- High public/political scrutiny

Global Trade Barriers and Feedstock Protectionism

Neste faces rising export restrictions on waste and residue feedstocks like used cooking oil, as countries protect domestic renewable industries; Indonesia, for example, introduced export levies in 2022 and tightened controls that affected global supplies.

These measures constrain low-cost raw material access, pressuring Neste’s margins given feedstock costs represented roughly 60–70% of renewable diesel production costs in 2024.

Maintaining diplomatic engagement and trade advocacy through 2026 is critical for Neste to secure cross-border feedstock flows and mitigate supply shocks.

- Indonesia export controls since 2022 reduced UCO exports by an estimated 20–30% in 2023–24

- Feedstock costs ≈60–70% of renewable diesel production cost (2024)

- Neste needs active trade diplomacy to protect global sourcing into 2026

Neste poised for SAF growth as EU/US policies boost demand despite rising feedstock costs

EU mandates (ReFuelEU, FuelEU) and US IRA credits drive demand and investment for Neste’s SAF and renewable fuels; state ownership 39.3% (2025) aligns company with Finland’s 2035 carbon neutrality target; feedstock export controls (eg. Indonesia since 2022) and geopolitical tensions raised feedstock logistics costs ~12% YoY (2024) and feedstock share 60–70% of production cost.

| Indicator | Value |

|---|---|

| State ownership (2025) | 39.3% |

| Renewable sales (2024) | €8.6bn |

| Feedstock share of cost (2024) | 60–70% |

| Feedstock logistics cost change (2024) | +12% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect Neste across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

Summarized PESTLE insights for Neste, neatly organized by category to ease meeting prep and enable quick insertion into presentations or strategy packs.

Economic factors

Feedstock Price Volatility

The cost of waste and residue feedstocks remained Neste's key economic variable at end-2025, with used cooking oil and animal fats prices up ~18% year-on-year, pushing input costs higher and compressing margins. Competition from oil majors and chemical firms increased demand for limited 2025 feedstock volumes, contributing to price volatility and a 12% rise in feedstock sourcing expenses. Neste's advanced sourcing network and pre-treatment tech reduced yield losses, supporting a 3-4 percentage point improvement in processing efficiency and helping protect EBITDA against raw-material swings.

Sustainable Aviation Fuel Market Expansion

Interest Rates and Capital Expenditure

The elevated global policy rates at end-2025—ECB depo 3.75%, US Fed funds 5.25%—raise borrowing costs for Neste, increasing weighted average cost of capital for its refinery and renewable hydrogen projects. Higher interest expense necessitates disciplined capital allocation and net debt/EBITDA targets; Neste reported net debt/EBITDA ~0.6x in 2024, supporting financing flexibility. Planned capacity ramps in Singapore and Rotterdam, expected to reach full operation in 2025–26, are projected to lift EBITDA margins and deliver multi-year ROI that offsets higher financing costs.

Fossil Fuel Price Parity

The price of crude oil strongly affects demand for Neste’s renewable diesel and SAF; Brent averaged about 95 USD/bbl in 2024, making renewables more competitive and boosting Neste’s margins and volumes.

When oil drops—as in 2020–21 shocks or sub‑$60 USD/bbl periods—renewables need stronger carbon pricing or mandates; EU ETS carbon prices around 90–100 EUR/t in 2024 partially offset this.

Global Inflationary Pressures

Inflation in 2025 raised Neste’s labor, logistics and energy costs by roughly 6–9% year-on-year, squeezing margins and increasing operating expenses across refineries and supply chains.

Neste accelerated operational excellence and digital transformation projects, targeting a 3–4% cost-to-serve reduction and automated logistics to protect EBITDA.

Efficient global supply-chain management is critical to keep end-product prices competitive for customers across Europe, Asia and North America amid volatile freight and energy prices.

- 2025 labor/logistics/energy inflation: ~6–9%

- Targeted cost-to-serve reduction via digitalization: 3–4%

- Focus regions: Europe, Asia, North America

Neste faces margin squeeze as feedstock costs surge 18% while SAF ramp meets mixed pricing

Key economic drivers for Neste in 2024–25: feedstock costs up ~18% YoY, raising sourcing spend ~12% and pressuring margins; SAF capacity >2.5 Mt with 30–40% long‑term offtake, SAF premium $0.40–0.80/L; Brent ~95 USD/bbl (2024) and EU ETS ~90–100 EUR/t; interest rates higher (ECB 3.75%, Fed 5.25%), net debt/EBITDA ~0.6x; 2025 inflation increased OPEX ~6–9%, targeted cost-to-serve cut 3–4%.

| Metric | 2024–25 |

|---|---|

| Feedstock price change | +18% YoY |

| Feedstock spend | +12% |

| SAF capacity | >2.5 Mt |

| SAF premium | $0.40–0.80/L |

| Brent | ~95 USD/bbl |

| EU ETS | ~90–100 EUR/t |

| Rates (ECB/Fed) | 3.75% / 5.25% |

| Net debt/EBITDA | ~0.6x |

| Inflation impact | +6–9% OPEX |

| Cost-to-serve target | -3–4% |

Full Version Awaits

Neste PESTLE Analysis

The preview shown here is the exact Neste PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.