New Fortress Energy Porter's Five Forces Analysis

Don't Miss the Bigger Picture

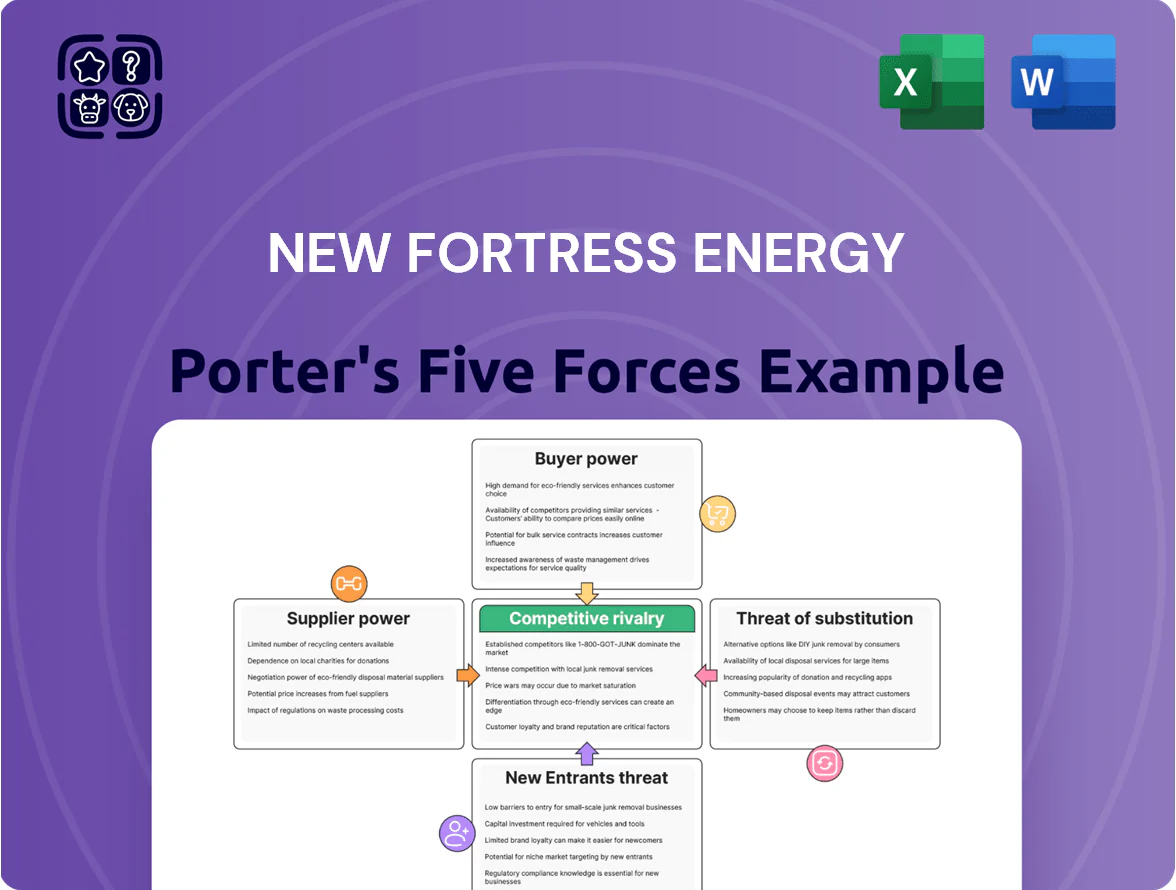

New Fortress Energy faces intense supplier bargaining, regulatory headwinds, and moderate buyer power as it scales LNG infrastructure, while competitive rivalry and substitute threats from renewables shape margins and growth prospects; this snapshot highlights key pressures but omits force-by-force ratings and visuals—unlock the full Porter's Five Forces Analysis to get detailed ratings, strategic implications, and actionable insights tailored for investment or strategic planning.

Suppliers Bargaining Power

Concentration of Upstream LNG Liquefaction

The global LNG liquefaction market is highly concentrated: the top 10 producers control about 65% of capacity and top 5 exporters (Qatar, Australia, US, Russia, Malaysia) set prices in tight markets, giving suppliers leverage during peaks. New Fortress Energy depends on these upstream sellers for feedstock to run its ~2.5 GW of downstream capacity and regas hubs, so supplier price moves hit margins directly. As of Dec 2025, supply risks from geopolitics (Russia/Ukraine, Middle East) keep spot LNG premiums ~30% above 2021 averages, boosting supplier bargaining power.

Specialized Maritime and Infrastructure Equipment

Specialized vendors supplying FSRUs and modular liquefiers wield strong bargaining power: about 4–6 global firms control key proprietary designs and account for over 70% of FSRU capacity, making them critical for New Fortress Energy’s Fast LNG projects.

Limited global shipyard capacity—reported at ~60–80 available conversion slots annually in 2024—raises lead times to 12–30 months and can add 10–25% to capex through premiums and schedule risk.

Long-term Supply Contract Dependencies

Fluctuations in Commodity Market Pricing

- Henry Hub 2024 avg: 2.73 USD/MMBtu

- TTF 2024 range: ~16–20 USD/MMBtu

- NFE hedged ~40% of 2025 volumes (Q3 2025)

- Suppliers can reroute volumes to higher-price regions

Regulatory and Environmental Compliance Standards

Suppliers of tech and feedstock face strict methane limits and carbon reporting rules effective end-2025, raising demand for low-emission LNG tech and green hydrogen catalysts; this shifts pricing power to green suppliers and raises their negotiation leverage with New Fortress Energy (NFE).

NFE must secure preferred terms with compliant suppliers to meet 2030 emissions targets and avoid fines—US EPA and EU rules expose noncompliant supply chains to penalties and stranded-asset risk.

- End-2025 methane/carbon reporting deadline

- Premium pricing for low-carbon suppliers

- Higher leverage for green-tech vendors

- Alignment needed to meet 2030 targets and avoid fines

Suppliers dominate LNG pricing; NFE hedges stabilize margins but cap flexibility

Suppliers hold high bargaining power: top 5 exporters control pricing during tight markets, spot LNG premiums ~30% above 2021 (Dec 2025), and limited FSRU/shipyard vendors push capex and lead times; NFE has 60–70% feedstock on LTAs and hedged ~40% of 2025 volumes, which stabilizes margins but limits flexibility against regional price arbitrage.

| Metric | Value |

|---|---|

| Top-5 export share | ~50–60% |

| Spot premium (Dec 2025) | ~+30% vs 2021 |

| Feedstock LTAs | 60–70% |

| 2025 hedged | ~40% |

What is included in the product

Tailored Porter's Five Forces analysis for New Fortress Energy that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—actionable for investors, strategists, and academic use.

A concise Porter's Five Forces one-sheet for New Fortress Energy—instantly highlights competitive pressures, supplier/buyer power, and substitution threats to streamline strategic decisions.

Customers Bargaining Power

Sovereign and Utility Off-take Agreements

Availability of Alternative Energy Sources

Customers in industrial and power sectors can switch to diesel, fuel oil, or renewables; by 2025 utility-scale solar LCOE fell ~35% vs 2015 and onshore wind ~20%, boosting switching leverage.

Declining capex for distributed solar plus battery storage—US residential PV+storage costs down ~25% 2020–2024—lets buyers threaten bypassing gas infrastructure.

That pressure forces New Fortress Energy to keep pipeline and LNG pricing competitive; losing price edge risks customers choosing decentralized green alternatives.

Price Sensitivity in Developing Economies

Operating mainly in developing regions where energy affordability is a hot political issue, New Fortress Energy faces customers who are highly price sensitive; surveys show >60% of households in its Caribbean and West African markets cut consumption when prices rise over 15% (World Bank, 2023).

During the 2022–23 global gas spike, governments pressed for subsidies; regulators limited pass-throughs, so NFE could only recover ~40–60% of fuel-cost increases, squeezing EBITDA margins by an estimated 150–300 basis points in affected contracts.

Contractual Flexibility and Renegotiation Demands

Large industrial buyers of LNG and gas for power—often 50–500 MW plants—push New Fortress Energy for shorter contracts and flexible volumes; in 2024 about 30% of NFE’s commercial portfolio had sub-5‑year terms, raising renegotiation risk.

Customers use scale to extract softer take‑or‑pay terms or early termination clauses, and in 2023 market spot prices swung 40% vs. 2022, fueling demand for agility.

NFE must trade steady cash flow (fixed payments underpinning project finance) against churn: if average contract length falls below 7 years, refinancing spreads could widen by ~150 bps.

- ~30% contracts <5 years (2024)

- 2023–24 spot price swing ~40%

- Refi spread +150 bps if avg term <7 years

Low Switching Costs for Certain Industrial Users

Smaller industrial users face low switching costs versus locked-in power plants, so entry of local LNG resellers can quickly shift demand; in 2024 spot LNG prices fell ~35% in Atlantic markets, making short-term contracts more attractive to buyers.

Where New Fortress Energy has initial rigs or regas hubs, competitors could piggyback logistics to undercut rates, strengthening customer leverage; in Puerto Rico and Panama, industrial buyers negotiated 5–10% discounts in 2023–24.

- Low switching costs for small industrials

- Spot price volatility (~35% drop 2024) boosts buyer options

- Local logistics reuse enables competitor offers

- Observed 5–10% negotiated discounts (2023–24)

Sovereign buyers hold 60% of NFE EBITDA—tariff cuts, short contracts, tech shifts raise churn

Sovereign utility buyers drive ~60% of NFE’s 2024 contracted EBITDA, giving them strong price leverage and renegotiation power; tariff reviews in 2024 reduced recoverable fuel pass‑throughs to ~40–60%, cutting EBITDA by ~150–300 bps. Shorter contracts (~30% <5 years) and 2023–24 spot volatility (~40%) raise churn risk; solar/wind LCOE declines (~35% since 2015) and 2020–24 PV+storage cost ↓25% increase switching threats.

| Metric | Value |

|---|---|

| Share of contracted EBITDA (2024) | ~60% |

| Contracts <5 yrs (2024) | ~30% |

| Spot price swing (2023–24) | ~40% |

| Solar LCOE change (2015–2025) | ~-35% |

| PV+storage cost change (2020–24) | ~-25% |

Preview the Actual Deliverable

New Fortress Energy Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for New Fortress Energy you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the full, professionally formatted file—ready for download and use the moment you buy.

You're viewing the final deliverable; once you complete payment, you’ll get instant access to this same analysis, ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

New Fortress Energy faces intense supplier bargaining, regulatory headwinds, and moderate buyer power as it scales LNG infrastructure, while competitive rivalry and substitute threats from renewables shape margins and growth prospects; this snapshot highlights key pressures but omits force-by-force ratings and visuals—unlock the full Porter's Five Forces Analysis to get detailed ratings, strategic implications, and actionable insights tailored for investment or strategic planning.

Suppliers Bargaining Power

Concentration of Upstream LNG Liquefaction

The global LNG liquefaction market is highly concentrated: the top 10 producers control about 65% of capacity and top 5 exporters (Qatar, Australia, US, Russia, Malaysia) set prices in tight markets, giving suppliers leverage during peaks. New Fortress Energy depends on these upstream sellers for feedstock to run its ~2.5 GW of downstream capacity and regas hubs, so supplier price moves hit margins directly. As of Dec 2025, supply risks from geopolitics (Russia/Ukraine, Middle East) keep spot LNG premiums ~30% above 2021 averages, boosting supplier bargaining power.

Specialized Maritime and Infrastructure Equipment

Specialized vendors supplying FSRUs and modular liquefiers wield strong bargaining power: about 4–6 global firms control key proprietary designs and account for over 70% of FSRU capacity, making them critical for New Fortress Energy’s Fast LNG projects.

Limited global shipyard capacity—reported at ~60–80 available conversion slots annually in 2024—raises lead times to 12–30 months and can add 10–25% to capex through premiums and schedule risk.

Long-term Supply Contract Dependencies

Fluctuations in Commodity Market Pricing

- Henry Hub 2024 avg: 2.73 USD/MMBtu

- TTF 2024 range: ~16–20 USD/MMBtu

- NFE hedged ~40% of 2025 volumes (Q3 2025)

- Suppliers can reroute volumes to higher-price regions

Regulatory and Environmental Compliance Standards

Suppliers of tech and feedstock face strict methane limits and carbon reporting rules effective end-2025, raising demand for low-emission LNG tech and green hydrogen catalysts; this shifts pricing power to green suppliers and raises their negotiation leverage with New Fortress Energy (NFE).

NFE must secure preferred terms with compliant suppliers to meet 2030 emissions targets and avoid fines—US EPA and EU rules expose noncompliant supply chains to penalties and stranded-asset risk.

- End-2025 methane/carbon reporting deadline

- Premium pricing for low-carbon suppliers

- Higher leverage for green-tech vendors

- Alignment needed to meet 2030 targets and avoid fines

Suppliers dominate LNG pricing; NFE hedges stabilize margins but cap flexibility

Suppliers hold high bargaining power: top 5 exporters control pricing during tight markets, spot LNG premiums ~30% above 2021 (Dec 2025), and limited FSRU/shipyard vendors push capex and lead times; NFE has 60–70% feedstock on LTAs and hedged ~40% of 2025 volumes, which stabilizes margins but limits flexibility against regional price arbitrage.

| Metric | Value |

|---|---|

| Top-5 export share | ~50–60% |

| Spot premium (Dec 2025) | ~+30% vs 2021 |

| Feedstock LTAs | 60–70% |

| 2025 hedged | ~40% |

What is included in the product

Tailored Porter's Five Forces analysis for New Fortress Energy that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—actionable for investors, strategists, and academic use.

A concise Porter's Five Forces one-sheet for New Fortress Energy—instantly highlights competitive pressures, supplier/buyer power, and substitution threats to streamline strategic decisions.

Customers Bargaining Power

Sovereign and Utility Off-take Agreements

Availability of Alternative Energy Sources

Customers in industrial and power sectors can switch to diesel, fuel oil, or renewables; by 2025 utility-scale solar LCOE fell ~35% vs 2015 and onshore wind ~20%, boosting switching leverage.

Declining capex for distributed solar plus battery storage—US residential PV+storage costs down ~25% 2020–2024—lets buyers threaten bypassing gas infrastructure.

That pressure forces New Fortress Energy to keep pipeline and LNG pricing competitive; losing price edge risks customers choosing decentralized green alternatives.

Price Sensitivity in Developing Economies

Operating mainly in developing regions where energy affordability is a hot political issue, New Fortress Energy faces customers who are highly price sensitive; surveys show >60% of households in its Caribbean and West African markets cut consumption when prices rise over 15% (World Bank, 2023).

During the 2022–23 global gas spike, governments pressed for subsidies; regulators limited pass-throughs, so NFE could only recover ~40–60% of fuel-cost increases, squeezing EBITDA margins by an estimated 150–300 basis points in affected contracts.

Contractual Flexibility and Renegotiation Demands

Large industrial buyers of LNG and gas for power—often 50–500 MW plants—push New Fortress Energy for shorter contracts and flexible volumes; in 2024 about 30% of NFE’s commercial portfolio had sub-5‑year terms, raising renegotiation risk.

Customers use scale to extract softer take‑or‑pay terms or early termination clauses, and in 2023 market spot prices swung 40% vs. 2022, fueling demand for agility.

NFE must trade steady cash flow (fixed payments underpinning project finance) against churn: if average contract length falls below 7 years, refinancing spreads could widen by ~150 bps.

- ~30% contracts <5 years (2024)

- 2023–24 spot price swing ~40%

- Refi spread +150 bps if avg term <7 years

Low Switching Costs for Certain Industrial Users

Smaller industrial users face low switching costs versus locked-in power plants, so entry of local LNG resellers can quickly shift demand; in 2024 spot LNG prices fell ~35% in Atlantic markets, making short-term contracts more attractive to buyers.

Where New Fortress Energy has initial rigs or regas hubs, competitors could piggyback logistics to undercut rates, strengthening customer leverage; in Puerto Rico and Panama, industrial buyers negotiated 5–10% discounts in 2023–24.

- Low switching costs for small industrials

- Spot price volatility (~35% drop 2024) boosts buyer options

- Local logistics reuse enables competitor offers

- Observed 5–10% negotiated discounts (2023–24)

Sovereign buyers hold 60% of NFE EBITDA—tariff cuts, short contracts, tech shifts raise churn

Sovereign utility buyers drive ~60% of NFE’s 2024 contracted EBITDA, giving them strong price leverage and renegotiation power; tariff reviews in 2024 reduced recoverable fuel pass‑throughs to ~40–60%, cutting EBITDA by ~150–300 bps. Shorter contracts (~30% <5 years) and 2023–24 spot volatility (~40%) raise churn risk; solar/wind LCOE declines (~35% since 2015) and 2020–24 PV+storage cost ↓25% increase switching threats.

| Metric | Value |

|---|---|

| Share of contracted EBITDA (2024) | ~60% |

| Contracts <5 yrs (2024) | ~30% |

| Spot price swing (2023–24) | ~40% |

| Solar LCOE change (2015–2025) | ~-35% |

| PV+storage cost change (2020–24) | ~-25% |

Preview the Actual Deliverable

New Fortress Energy Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for New Fortress Energy you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the full, professionally formatted file—ready for download and use the moment you buy.

You're viewing the final deliverable; once you complete payment, you’ll get instant access to this same analysis, ready for immediate use.