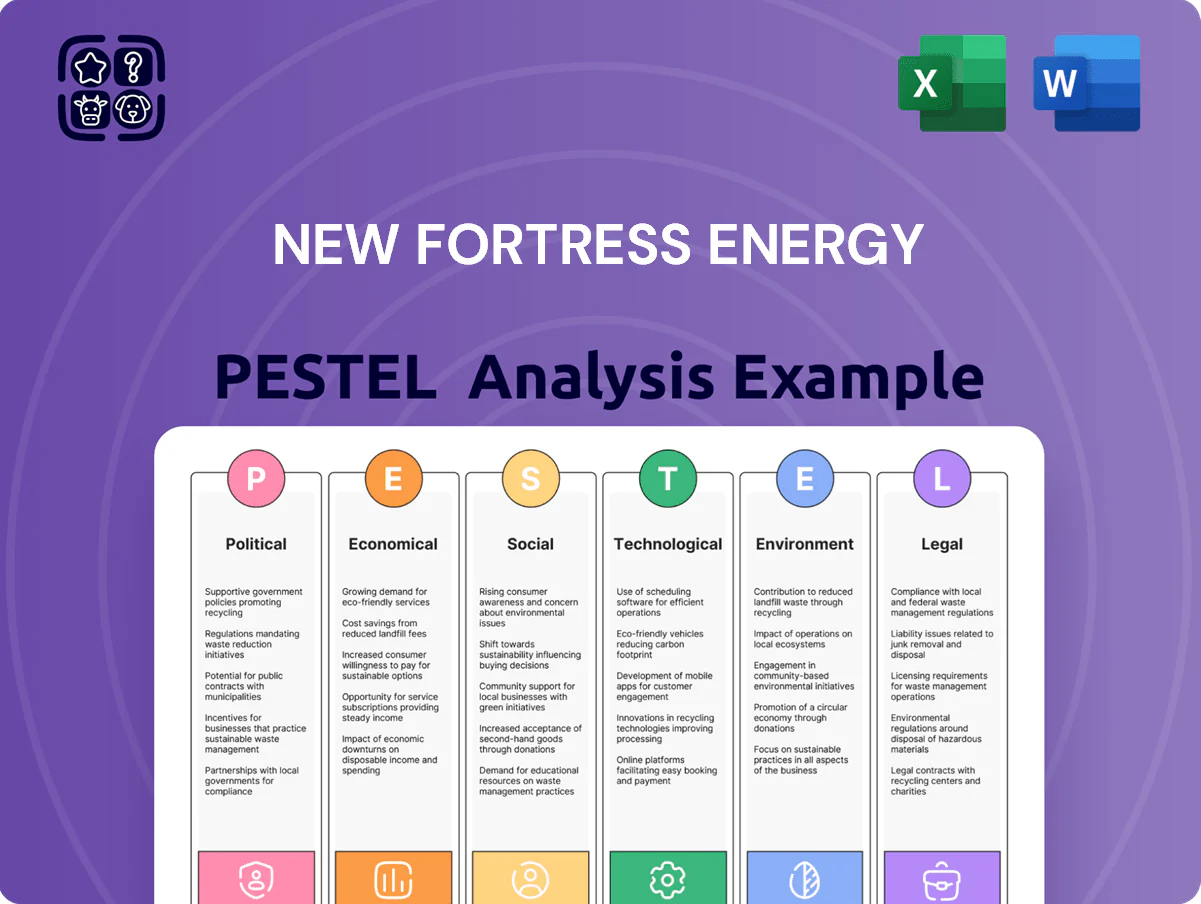

New Fortress Energy PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock how political, economic, and environmental trends are reshaping New Fortress Energy’s strategy with our concise PESTLE snapshot—perfect for investors and strategists who need fast, actionable context; buy the full analysis for the complete data, risk scoring, and tailored recommendations to inform your next move.

Political factors

Geopolitical Energy Security Priorities

Geopolitical energy-security priorities are boosting LNG infrastructure demand as countries shift from pipeline dependence; global LNG trade grew 7% in 2024 to ~410 million tonnes, underscoring LNG’s role as a flexible alternative to volatile pipeline supplies.

Governments in Europe and Southeast Asia are partnering with private firms like New Fortress Energy—which reported 2024 adjusted EBITDA of $485 million—to secure long-term resilience through FSRU and onshore terminal contracts.

This political climate supports NFE’s expansion of terminals and integrated power solutions across continents, aligned with its 2024 target to double deployed capacity by 2027 through multi-year offtake and project agreements.

US LNG Export Regulatory Landscape

As of late 2025, US LNG export regulation remains pivotal after 2023–25 policy shifts tightened terminal permitting; DOE approvals for non-FTA exports rose 18% YoY while FERC completed environmental reviews for 6 major projects affecting capacity.

New Fortress Energy must align with evolving DOE and FERC requirements across its offshore FLNG and onshore regas and liquefaction assets to avoid permit delays that could defer revenue recognition tied to contracts worth roughly $2.3 billion.

US political stability influences feedstock access and pipeline flows—domestic gas production of ~105 bcfd in 2024 underpins export volumes, so regulatory uncertainty can compress margins and disrupt the LNG supply chain to international offtakers.

Emerging Market Government Relations

International Trade Policy and Sanctions

Global trade dynamics and sanctions reshape New Fortress Energy's competitive position; 2024 saw 12 major energy-related sanctions globally, increasing demand for flexible LNG delivery alternatives that NFE's ship-borne terminals address.

Ship-to-ship and FSRU solutions let countries circumvent pipeline constraints and port chokepoints, supporting NFE's 2024 throughput growth of ~18% year-over-year, yet exposure to trade wars could raise LNG freight costs by 10–25%.

Trade agreements easing cross-border energy tech and fuel flows are vital to sustain NFE's low-cost model; tariff reductions and streamlined customs correlate with lower delivered cost per MMBtu, improving project IRRs.

- 12 energy sanctions in 2024 increased demand for mobile LNG

- NFE throughput +18% y/y in 2024

- Trade wars can lift freight costs 10–25%

- Favorable trade deals lower delivered cost per MMBtu and boost IRR

Energy Transition Subsidies and Incentives

Political moves toward decarbonization have increased subsidies for cleaner-burning fuels versus coal; in 2024 the EU and G20 members expanded fuel-switch incentives, improving economics for LNG-fired projects.

New Fortress Energy leverages these incentives to market natural gas as the bridge fuel in developing markets, citing project-level subsidy boosts that lower levelized fuel costs by up to 10–15% in targeted jurisdictions.

Green financing and government-backed loan guarantees—over $20 billion in energy transition facilities announced by multilateral banks in 2024–2025—support NFE’s CAPEX plans through 2025, reducing financing costs and enabling faster build-out.

- 2024–25 multilateral green facilities > $20bn

- Project LCOE reduction from subsidies ~10–15%

- NFE positions LNG as primary bridge fuel in developing markets

- Government guarantees lower CAPEX financing costs through 2025

LNG surge boosts FSRU demand as sanctions, policy shifts threaten $2.3B projects

Geopolitical shifts favor LNG; global trade rose 7% in 2024 to ~410 mt, boosting demand for NFE’s FSRU and mobile solutions as throughput grew ~18% y/y.

US DOE/FERC permitting, 2024–25 export policy tightening, and 12 energy sanctions in 2024 raise regulatory and trade risks that can increase freight costs 10–25% and delay projects tied to ~$2.3bn international assets.

Government subsidies, green finance (> $20bn 2024–25) and tariff changes (Brazil 2024 tariff reviews, Jamaica rate adjustments) impact margins, lowering LCOE 10–15% where applied.

| Metric | 2024–25 |

|---|---|

| Global LNG trade | ~410 mt (+7%) |

| NFE throughput | +18% y/y |

| Sanctions | 12 energy sanctions |

| Green facilities | > $20bn |

| Intl assets at risk | ~$2.3bn |

What is included in the product

Explores how macro-environmental forces uniquely impact New Fortress Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current market trends and regional regulatory dynamics.

A concise, shareable New Fortress Energy PESTLE snapshot that’s visually segmented for quick interpretation, usable in presentations or strategy sessions to align teams, add contextual notes, and streamline discussion of external risks and market positioning.

Economic factors

Interest Rate Environment and Debt Servicing

New Fortress Energy operates a capital-intensive model financed largely by debt—total long-term debt was about $6.1 billion as of Q4 2025—making refinancing risk-sensitive to interest rate moves.

As central banks normalize policy through 2025, any rise in global benchmark rates would increase NFE’s interest expense and could raise weighted-average borrowing costs above its 2024 effective rate near mid-single digits.

Higher borrowing costs would compress EBIT margins and may delay deployment of LNG terminals and power projects in new markets, slowing capacity growth targets tied to annual contracted volumes.

Global LNG Price Volatility

The economic viability of New Fortress Energy’s integrated model hinges on spreads between Henry Hub (US ~$2.50–3.50/MMBtu in 2024–2025) and international spot LNG prices (Asia/Japan Korea Marker peaked near $18/MMBtu in 2024), driving arbitrage opportunities. Global demand swings—Asia industrial activity and 2024–25 cold winters in Europe—have pushed spot volatility, impacting supply margins. NFE offsets exposure with long-term hedges and contracts, supporting stable downstream pricing and protecting EBITDA against spot shocks.

Emerging Market Currency Risk

With roughly 60% of New Fortress Energy’s 2024 revenue tied to emerging markets, currency volatility—like the 15–30% devaluations seen in parts of Latin America since 2022—raises material risks as local currencies weaken vs the US dollar.

Devaluations increase the local-currency cost of imported LNG for utilities, contributing to payment delays and elevated receivable days observed in some markets in 2023–2025.

To mitigate this, NFE often uses US dollar-linked pricing and dollar-denominated contracts, preserving margins despite host-country macro shocks and limiting FX translation exposure.

Infrastructure Development Costs

The cost of specialized labor, steel, and advanced cryogenic equipment materially affects ROI for new regasification and liquefaction units; steel prices averaged about $1,100/ton in 2024, raising CAPEX estimates by mid-single digits versus 2022.

Inflationary pressures on construction materials through 2025 pushed NFE to adopt tighter project management and scale its proprietary Fast LNG modules, reducing per-MW build costs by an estimated 8–12% in recent projects.

Economic efficiency in the build-out phase remains a primary determinant of NFE’s ability to offer competitive power prices, with optimized CAPEX targeting sub-$600/kW for select integrated plants based on 2024–2025 project data.

- 2024 steel: ~$1,100/ton; CAPEX +mid-single digits

- Fast LNG cut per-MW build cost ~8–12%

- Targeted CAPEX benchmark: < $600/kW (2024–25 projects)

Growth in Industrial Energy Demand

The expansion of industrial manufacturing and hyperscale data centers in Southeast Asia, Africa and Latin America drives strong demand for baseload power; global data center energy use reached about 205 TWh in 2023 and is projected to grow ~4% annually through 2025, strengthening NFE’s market opportunity.

New Fortress Energy focuses on regions where electricity access and reliability gaps—over 600 million without reliable power in 2024—constrain growth, supplying LNG-powered infrastructure to unlock industrialization and exports.

This rising industrial energy demand underpins NFE’s long-term revenue forecasts and supports market share gains, with LNG-to-power projects contributing materially to contracted EBITDA in 2024–25.

- 205 TWh global data center use (2023), ~4% CAGR to 2025

- 600+ million without reliable power (2024)

- NFE LNG projects key driver of contracted EBITDA 2024–25

High debt, FX & LNG spread risk; cost cuts target sub-$600/kW

Debt-heavy capital structure (~$6.1B LT debt Q4 2025) raises refinancing/interest-rate sensitivity; rising global rates through 2025 could lift borrowing costs above 2024 mid-single digits and compress EBIT margins.

FX volatility in emerging markets (15–30% devaluations since 2022) and spot LNG spreads (Henry Hub ~$2.5–3.5/MMBtu vs JKM up to ~$18/MMBtu in 2024) drive revenue/margin risk; dollar contracts and hedges mitigate exposure.

Higher steel (~$1,100/ton in 2024) and inflation raised CAPEX mid-single digits; Fast LNG reduced per-MW build cost ~8–12%, targeting sub-$600/kW on select 2024–25 projects.

| Metric | Value/Period |

|---|---|

| LT Debt | $6.1B (Q4 2025) |

| Henry Hub / JKM | $2.5–3.5 / ~ $18 (2024) |

| Steel price | $1,100/ton (2024) |

| Fast LNG savings | 8–12% per-MW |

| Target CAPEX | < $600/kW (2024–25) |

Preview the Actual Deliverable

New Fortress Energy PESTLE Analysis

The preview shown here is the exact New Fortress Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and insights visible are identical to the downloadable file you’ll get upon checkout, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock how political, economic, and environmental trends are reshaping New Fortress Energy’s strategy with our concise PESTLE snapshot—perfect for investors and strategists who need fast, actionable context; buy the full analysis for the complete data, risk scoring, and tailored recommendations to inform your next move.

Political factors

Geopolitical Energy Security Priorities

Geopolitical energy-security priorities are boosting LNG infrastructure demand as countries shift from pipeline dependence; global LNG trade grew 7% in 2024 to ~410 million tonnes, underscoring LNG’s role as a flexible alternative to volatile pipeline supplies.

Governments in Europe and Southeast Asia are partnering with private firms like New Fortress Energy—which reported 2024 adjusted EBITDA of $485 million—to secure long-term resilience through FSRU and onshore terminal contracts.

This political climate supports NFE’s expansion of terminals and integrated power solutions across continents, aligned with its 2024 target to double deployed capacity by 2027 through multi-year offtake and project agreements.

US LNG Export Regulatory Landscape

As of late 2025, US LNG export regulation remains pivotal after 2023–25 policy shifts tightened terminal permitting; DOE approvals for non-FTA exports rose 18% YoY while FERC completed environmental reviews for 6 major projects affecting capacity.

New Fortress Energy must align with evolving DOE and FERC requirements across its offshore FLNG and onshore regas and liquefaction assets to avoid permit delays that could defer revenue recognition tied to contracts worth roughly $2.3 billion.

US political stability influences feedstock access and pipeline flows—domestic gas production of ~105 bcfd in 2024 underpins export volumes, so regulatory uncertainty can compress margins and disrupt the LNG supply chain to international offtakers.

Emerging Market Government Relations

International Trade Policy and Sanctions

Global trade dynamics and sanctions reshape New Fortress Energy's competitive position; 2024 saw 12 major energy-related sanctions globally, increasing demand for flexible LNG delivery alternatives that NFE's ship-borne terminals address.

Ship-to-ship and FSRU solutions let countries circumvent pipeline constraints and port chokepoints, supporting NFE's 2024 throughput growth of ~18% year-over-year, yet exposure to trade wars could raise LNG freight costs by 10–25%.

Trade agreements easing cross-border energy tech and fuel flows are vital to sustain NFE's low-cost model; tariff reductions and streamlined customs correlate with lower delivered cost per MMBtu, improving project IRRs.

- 12 energy sanctions in 2024 increased demand for mobile LNG

- NFE throughput +18% y/y in 2024

- Trade wars can lift freight costs 10–25%

- Favorable trade deals lower delivered cost per MMBtu and boost IRR

Energy Transition Subsidies and Incentives

Political moves toward decarbonization have increased subsidies for cleaner-burning fuels versus coal; in 2024 the EU and G20 members expanded fuel-switch incentives, improving economics for LNG-fired projects.

New Fortress Energy leverages these incentives to market natural gas as the bridge fuel in developing markets, citing project-level subsidy boosts that lower levelized fuel costs by up to 10–15% in targeted jurisdictions.

Green financing and government-backed loan guarantees—over $20 billion in energy transition facilities announced by multilateral banks in 2024–2025—support NFE’s CAPEX plans through 2025, reducing financing costs and enabling faster build-out.

- 2024–25 multilateral green facilities > $20bn

- Project LCOE reduction from subsidies ~10–15%

- NFE positions LNG as primary bridge fuel in developing markets

- Government guarantees lower CAPEX financing costs through 2025

LNG surge boosts FSRU demand as sanctions, policy shifts threaten $2.3B projects

Geopolitical shifts favor LNG; global trade rose 7% in 2024 to ~410 mt, boosting demand for NFE’s FSRU and mobile solutions as throughput grew ~18% y/y.

US DOE/FERC permitting, 2024–25 export policy tightening, and 12 energy sanctions in 2024 raise regulatory and trade risks that can increase freight costs 10–25% and delay projects tied to ~$2.3bn international assets.

Government subsidies, green finance (> $20bn 2024–25) and tariff changes (Brazil 2024 tariff reviews, Jamaica rate adjustments) impact margins, lowering LCOE 10–15% where applied.

| Metric | 2024–25 |

|---|---|

| Global LNG trade | ~410 mt (+7%) |

| NFE throughput | +18% y/y |

| Sanctions | 12 energy sanctions |

| Green facilities | > $20bn |

| Intl assets at risk | ~$2.3bn |

What is included in the product

Explores how macro-environmental forces uniquely impact New Fortress Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current market trends and regional regulatory dynamics.

A concise, shareable New Fortress Energy PESTLE snapshot that’s visually segmented for quick interpretation, usable in presentations or strategy sessions to align teams, add contextual notes, and streamline discussion of external risks and market positioning.

Economic factors

Interest Rate Environment and Debt Servicing

New Fortress Energy operates a capital-intensive model financed largely by debt—total long-term debt was about $6.1 billion as of Q4 2025—making refinancing risk-sensitive to interest rate moves.

As central banks normalize policy through 2025, any rise in global benchmark rates would increase NFE’s interest expense and could raise weighted-average borrowing costs above its 2024 effective rate near mid-single digits.

Higher borrowing costs would compress EBIT margins and may delay deployment of LNG terminals and power projects in new markets, slowing capacity growth targets tied to annual contracted volumes.

Global LNG Price Volatility

The economic viability of New Fortress Energy’s integrated model hinges on spreads between Henry Hub (US ~$2.50–3.50/MMBtu in 2024–2025) and international spot LNG prices (Asia/Japan Korea Marker peaked near $18/MMBtu in 2024), driving arbitrage opportunities. Global demand swings—Asia industrial activity and 2024–25 cold winters in Europe—have pushed spot volatility, impacting supply margins. NFE offsets exposure with long-term hedges and contracts, supporting stable downstream pricing and protecting EBITDA against spot shocks.

Emerging Market Currency Risk

With roughly 60% of New Fortress Energy’s 2024 revenue tied to emerging markets, currency volatility—like the 15–30% devaluations seen in parts of Latin America since 2022—raises material risks as local currencies weaken vs the US dollar.

Devaluations increase the local-currency cost of imported LNG for utilities, contributing to payment delays and elevated receivable days observed in some markets in 2023–2025.

To mitigate this, NFE often uses US dollar-linked pricing and dollar-denominated contracts, preserving margins despite host-country macro shocks and limiting FX translation exposure.

Infrastructure Development Costs

The cost of specialized labor, steel, and advanced cryogenic equipment materially affects ROI for new regasification and liquefaction units; steel prices averaged about $1,100/ton in 2024, raising CAPEX estimates by mid-single digits versus 2022.

Inflationary pressures on construction materials through 2025 pushed NFE to adopt tighter project management and scale its proprietary Fast LNG modules, reducing per-MW build costs by an estimated 8–12% in recent projects.

Economic efficiency in the build-out phase remains a primary determinant of NFE’s ability to offer competitive power prices, with optimized CAPEX targeting sub-$600/kW for select integrated plants based on 2024–2025 project data.

- 2024 steel: ~$1,100/ton; CAPEX +mid-single digits

- Fast LNG cut per-MW build cost ~8–12%

- Targeted CAPEX benchmark: < $600/kW (2024–25 projects)

Growth in Industrial Energy Demand

The expansion of industrial manufacturing and hyperscale data centers in Southeast Asia, Africa and Latin America drives strong demand for baseload power; global data center energy use reached about 205 TWh in 2023 and is projected to grow ~4% annually through 2025, strengthening NFE’s market opportunity.

New Fortress Energy focuses on regions where electricity access and reliability gaps—over 600 million without reliable power in 2024—constrain growth, supplying LNG-powered infrastructure to unlock industrialization and exports.

This rising industrial energy demand underpins NFE’s long-term revenue forecasts and supports market share gains, with LNG-to-power projects contributing materially to contracted EBITDA in 2024–25.

- 205 TWh global data center use (2023), ~4% CAGR to 2025

- 600+ million without reliable power (2024)

- NFE LNG projects key driver of contracted EBITDA 2024–25

High debt, FX & LNG spread risk; cost cuts target sub-$600/kW

Debt-heavy capital structure (~$6.1B LT debt Q4 2025) raises refinancing/interest-rate sensitivity; rising global rates through 2025 could lift borrowing costs above 2024 mid-single digits and compress EBIT margins.

FX volatility in emerging markets (15–30% devaluations since 2022) and spot LNG spreads (Henry Hub ~$2.5–3.5/MMBtu vs JKM up to ~$18/MMBtu in 2024) drive revenue/margin risk; dollar contracts and hedges mitigate exposure.

Higher steel (~$1,100/ton in 2024) and inflation raised CAPEX mid-single digits; Fast LNG reduced per-MW build cost ~8–12%, targeting sub-$600/kW on select 2024–25 projects.

| Metric | Value/Period |

|---|---|

| LT Debt | $6.1B (Q4 2025) |

| Henry Hub / JKM | $2.5–3.5 / ~ $18 (2024) |

| Steel price | $1,100/ton (2024) |

| Fast LNG savings | 8–12% per-MW |

| Target CAPEX | < $600/kW (2024–25) |

Preview the Actual Deliverable

New Fortress Energy PESTLE Analysis

The preview shown here is the exact New Fortress Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and insights visible are identical to the downloadable file you’ll get upon checkout, with no placeholders or surprises.