New Gold Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

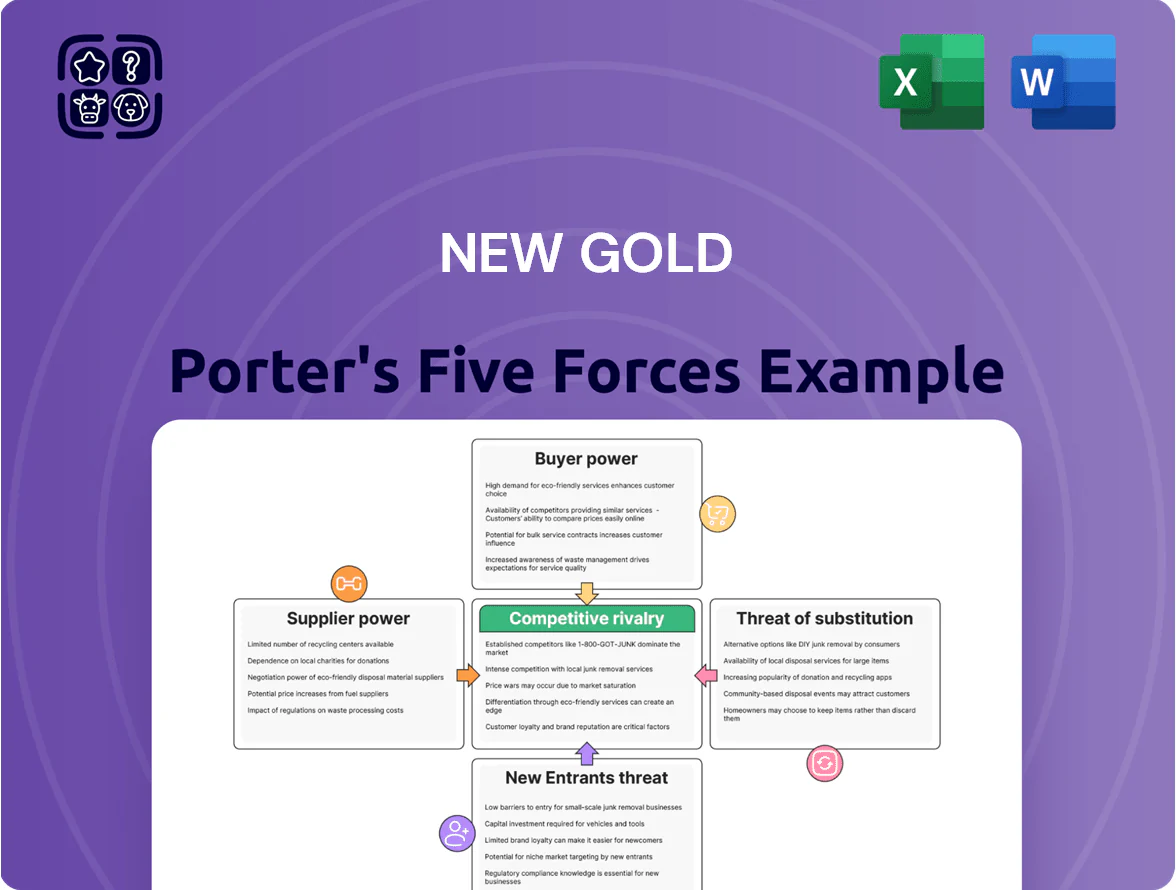

New Gold faces strong supplier and regulatory pressures, moderate buyer power, limited substitutes, and cyclical rivalry that together shape its competitive profile; this snapshot highlights key threats and strategic levers but only scratches the surface.

Suppliers Bargaining Power

Specialized Mining Equipment and OEM Reliance

New Gold depends on a few global OEMs for heavy and underground fleets, concentrating supplier power—switching cost for a 100‑unit fleet runs into tens of millions USD and multi‑year retraining; OEMs often charge 20–30% premium for proprietary parts. Maintenance contracts tied to OEM diagnostics accounted for ~12–18% of operating costs at comparable mid‑tier mines in 2024, raising vendor leverage over uptime and repair timelines.

Skilled Labor Market in Canada

As a Canada-focused operator, New Gold competes for a shrinking pool of skilled miners and trades; Canada saw a 2024 shortfall of ~11,000 mining workers, raising labour scarcity at sites like New Afton.

Experienced staff are critical for safety and throughput, so bargaining power is high, forcing New Gold to raise pay; Canadian mining average wages rose 6.2% in 2023–24.

Competition from Tier 1 firms drives retention costs up—labour-related operating expense pressure can exceed 3–5% of site opex annually.

Energy and Fuel Cost Volatility

Mining is energy-heavy: New Gold uses large diesel volumes for haulage and MW-scale electricity for mills, so input costs feed directly into All-In Sustaining Costs (AISC).

As a price-taker to global oil majors and regional utilities, New Gold had diesel costs rise ~28% in 2022–23 and electricity tariffs up to 12% in parts of Ontario and B.C. in 2024, squeezing margins.

Without long-term supply bargaining power, a $10/boe fuel swing can change AISC by ~$10–15/oz gold equivalent at mid-sized mines, raising operational risk.

Consumables and Reagent Supply Chains

Regulatory and ESG Consultancy Services

Regulatory and ESG consultancy firms in Canada now command strong supplier power for New Gold because strict federal and provincial rules (e.g., 2023 Canadian Impact Assessment changes) force use of certified auditors to keep permits and social license; specialized ESG audits cost 20–40% more than general compliance reviews, raising operating costs.

Rising sector-wide ESG reporting demand—GNWT/BC disclosure pushes and ~35% year‑on‑year growth in ESG service fees in 2024—gives these firms pricing leverage and strategic influence over project timelines and capital allocation.

- Essential for permits and social license

- Fees up 20–40% vs general audits

- ESG service demand +35% in 2024

- Influences timelines and capex

Supplier squeeze lifts New Gold AISC: reagent + diesel shocks add US$10–25/oz

Suppliers exert high bargaining power: concentrated OEMs and reagent providers, skilled‑labour scarcity, rising fuel/electricity tariffs, and costly ESG consults push New Gold’s AISC and capex timing; a 20% reagent rise ≈ US$10–25/oz impact; diesel swings alter AISC ~US$10–15/oz.

| Factor | 2024/25 |

|---|---|

| Reagent shock (20%) | US$10–25/oz |

| Diesel swing | US$10–15/oz |

| Labour shortfall (Canada) | ~11,000 workers |

What is included in the product

Tailored Porter's Five Forces analysis for New Gold that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic implications for pricing and profitability.

A concise Porter's Five Forces one-sheet for New Gold—quickly assess supplier, buyer, competitive, entrant, and substitution pressures to speed strategic decisions.

Customers Bargaining Power

Global Commodity Price-Taking

Gold trades as a global commodity with prices set on international markets (LBMA, COMEX); New Gold cannot influence spot prices and sells at prevailing rates—gold averaged 1,950 USD/oz in 2025 YTD through Jan 2026. This lack of pricing power constrains margins for New Gold and all miners, so revenue moves with the London spot price and not company-level production choices.

Standardized Product Quality

The output from New Gold’s operations—gold bullion and copper-gold concentrate—is highly standardized, so buyers face no switching costs and can source from any producer; in 2024 global refined gold supply was ~4,400 tonnes, making individual differentiation negligible. This undifferentiated product raises buyer leverage, letting customers press for spot pricing and tighter payment terms; New Gold reported realized gold prices aligned within 1–2% of LBMA spot in 2024.

Concentration of Smelting and Refining Capacity

Bullion sells easily, but New Afton’s copper-gold concentrates must go to a few specialized smelters; global smelting capacity is highly concentrated—top 10 smelters handle ~60% of copper concentrate throughput in 2024—so these buyers set treatment and refining charges. In 2024 New Gold reported concentrates sales made up about 18% of consolidated revenue, making that revenue stream sensitive to smelter capacity constraints and contract terms.

Low Switching Costs for Buyers

Buyers like bullion banks and refineries face near-zero switching costs, sourcing gold from hundreds of mines and >3,000 tonnes of annual recycled supply; London Bullion Market Association trading volumes averaged ~20,000 tonnes in 2024, so New Gold cannot charge loyalty premiums.

Liquid global markets and spot pricing mean buyers can pick lowest-cost suppliers instantly, preventing New Gold from securing price premiums or long-term captive contracts.

- Buyers: bullion banks, refineries

- Switching cost: ~zero

- Global supply: mines + >3,000 t recycled

- LBMA volume 2024: ~20,000 t

Influence of Macroeconomic Investors

Institutional investors, central banks, and gold ETFs—holding about 3,400 tonnes in ETF reserves by end-2024—drive ultimate gold demand, swinging flows with views on rates and inflation more than jewelry demand.

New Gold’s revenue and realized gold price exposure depend on those macro-driven flows; e.g., 2024 net ETF inflows of ~300 tonnes lifted spot prices ~10%, directly boosting miner cash margins.

- ETF reserves ~3,400 tonnes (2024)

- 2024 net ETF inflows ~300 tonnes

- Spot price rise ~10% in 2024 linked to flows

- Central bank purchases ~400 tonnes in 2024

Buyers Dominate: Gold's Spot Pricing and Smelter Concentration Squeeze New Gold

Buyers wield strong power: gold is a global commodity with spot pricing (LBMA/COMEX), so New Gold lacks pricing power; 2025 YTD gold ~1,950 USD/oz. Standardized output and near-zero switching costs let bullion banks/refineries demand spot terms; smelter concentration (top 10 ~60% throughput) pressures concentrate margins—concentrates = ~18% revenue (2024).

| Metric | Value |

|---|---|

| 2025 YTD gold price | ~1,950 USD/oz |

| Concentrates share (2024) | 18% |

| Top10 smelters throughput (2024) | ~60% |

Same Document Delivered

New Gold Porter's Five Forces Analysis

This preview shows the exact New Gold Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples—fully formatted, professional, and ready for download and use immediately upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

New Gold faces strong supplier and regulatory pressures, moderate buyer power, limited substitutes, and cyclical rivalry that together shape its competitive profile; this snapshot highlights key threats and strategic levers but only scratches the surface.

Suppliers Bargaining Power

Specialized Mining Equipment and OEM Reliance

New Gold depends on a few global OEMs for heavy and underground fleets, concentrating supplier power—switching cost for a 100‑unit fleet runs into tens of millions USD and multi‑year retraining; OEMs often charge 20–30% premium for proprietary parts. Maintenance contracts tied to OEM diagnostics accounted for ~12–18% of operating costs at comparable mid‑tier mines in 2024, raising vendor leverage over uptime and repair timelines.

Skilled Labor Market in Canada

As a Canada-focused operator, New Gold competes for a shrinking pool of skilled miners and trades; Canada saw a 2024 shortfall of ~11,000 mining workers, raising labour scarcity at sites like New Afton.

Experienced staff are critical for safety and throughput, so bargaining power is high, forcing New Gold to raise pay; Canadian mining average wages rose 6.2% in 2023–24.

Competition from Tier 1 firms drives retention costs up—labour-related operating expense pressure can exceed 3–5% of site opex annually.

Energy and Fuel Cost Volatility

Mining is energy-heavy: New Gold uses large diesel volumes for haulage and MW-scale electricity for mills, so input costs feed directly into All-In Sustaining Costs (AISC).

As a price-taker to global oil majors and regional utilities, New Gold had diesel costs rise ~28% in 2022–23 and electricity tariffs up to 12% in parts of Ontario and B.C. in 2024, squeezing margins.

Without long-term supply bargaining power, a $10/boe fuel swing can change AISC by ~$10–15/oz gold equivalent at mid-sized mines, raising operational risk.

Consumables and Reagent Supply Chains

Regulatory and ESG Consultancy Services

Regulatory and ESG consultancy firms in Canada now command strong supplier power for New Gold because strict federal and provincial rules (e.g., 2023 Canadian Impact Assessment changes) force use of certified auditors to keep permits and social license; specialized ESG audits cost 20–40% more than general compliance reviews, raising operating costs.

Rising sector-wide ESG reporting demand—GNWT/BC disclosure pushes and ~35% year‑on‑year growth in ESG service fees in 2024—gives these firms pricing leverage and strategic influence over project timelines and capital allocation.

- Essential for permits and social license

- Fees up 20–40% vs general audits

- ESG service demand +35% in 2024

- Influences timelines and capex

Supplier squeeze lifts New Gold AISC: reagent + diesel shocks add US$10–25/oz

Suppliers exert high bargaining power: concentrated OEMs and reagent providers, skilled‑labour scarcity, rising fuel/electricity tariffs, and costly ESG consults push New Gold’s AISC and capex timing; a 20% reagent rise ≈ US$10–25/oz impact; diesel swings alter AISC ~US$10–15/oz.

| Factor | 2024/25 |

|---|---|

| Reagent shock (20%) | US$10–25/oz |

| Diesel swing | US$10–15/oz |

| Labour shortfall (Canada) | ~11,000 workers |

What is included in the product

Tailored Porter's Five Forces analysis for New Gold that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic implications for pricing and profitability.

A concise Porter's Five Forces one-sheet for New Gold—quickly assess supplier, buyer, competitive, entrant, and substitution pressures to speed strategic decisions.

Customers Bargaining Power

Global Commodity Price-Taking

Gold trades as a global commodity with prices set on international markets (LBMA, COMEX); New Gold cannot influence spot prices and sells at prevailing rates—gold averaged 1,950 USD/oz in 2025 YTD through Jan 2026. This lack of pricing power constrains margins for New Gold and all miners, so revenue moves with the London spot price and not company-level production choices.

Standardized Product Quality

The output from New Gold’s operations—gold bullion and copper-gold concentrate—is highly standardized, so buyers face no switching costs and can source from any producer; in 2024 global refined gold supply was ~4,400 tonnes, making individual differentiation negligible. This undifferentiated product raises buyer leverage, letting customers press for spot pricing and tighter payment terms; New Gold reported realized gold prices aligned within 1–2% of LBMA spot in 2024.

Concentration of Smelting and Refining Capacity

Bullion sells easily, but New Afton’s copper-gold concentrates must go to a few specialized smelters; global smelting capacity is highly concentrated—top 10 smelters handle ~60% of copper concentrate throughput in 2024—so these buyers set treatment and refining charges. In 2024 New Gold reported concentrates sales made up about 18% of consolidated revenue, making that revenue stream sensitive to smelter capacity constraints and contract terms.

Low Switching Costs for Buyers

Buyers like bullion banks and refineries face near-zero switching costs, sourcing gold from hundreds of mines and >3,000 tonnes of annual recycled supply; London Bullion Market Association trading volumes averaged ~20,000 tonnes in 2024, so New Gold cannot charge loyalty premiums.

Liquid global markets and spot pricing mean buyers can pick lowest-cost suppliers instantly, preventing New Gold from securing price premiums or long-term captive contracts.

- Buyers: bullion banks, refineries

- Switching cost: ~zero

- Global supply: mines + >3,000 t recycled

- LBMA volume 2024: ~20,000 t

Influence of Macroeconomic Investors

Institutional investors, central banks, and gold ETFs—holding about 3,400 tonnes in ETF reserves by end-2024—drive ultimate gold demand, swinging flows with views on rates and inflation more than jewelry demand.

New Gold’s revenue and realized gold price exposure depend on those macro-driven flows; e.g., 2024 net ETF inflows of ~300 tonnes lifted spot prices ~10%, directly boosting miner cash margins.

- ETF reserves ~3,400 tonnes (2024)

- 2024 net ETF inflows ~300 tonnes

- Spot price rise ~10% in 2024 linked to flows

- Central bank purchases ~400 tonnes in 2024

Buyers Dominate: Gold's Spot Pricing and Smelter Concentration Squeeze New Gold

Buyers wield strong power: gold is a global commodity with spot pricing (LBMA/COMEX), so New Gold lacks pricing power; 2025 YTD gold ~1,950 USD/oz. Standardized output and near-zero switching costs let bullion banks/refineries demand spot terms; smelter concentration (top 10 ~60% throughput) pressures concentrate margins—concentrates = ~18% revenue (2024).

| Metric | Value |

|---|---|

| 2025 YTD gold price | ~1,950 USD/oz |

| Concentrates share (2024) | 18% |

| Top10 smelters throughput (2024) | ~60% |

Same Document Delivered

New Gold Porter's Five Forces Analysis

This preview shows the exact New Gold Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples—fully formatted, professional, and ready for download and use immediately upon payment.