Newmont Mining PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how regulatory shifts, commodity cycles, and sustainability trends are shaping Newmont Mining’s strategic prospects—our concise PESTLE snapshot highlights the key external pressures and opportunities that matter to investors and strategists. Purchase the full PESTLE analysis for a complete, actionable breakdown you can use to stress-test portfolios, inform M&A, or guide boardroom decisions.

Political factors

Geopolitical stability in Tier 1 jurisdictions

Newmont holds ~60% of attributable gold reserves and major operations in Australia and North America, shielding the firm from abrupt regime change risks that affect emerging markets.

Tier 1 jurisdictions offer stable permitting and tax regimes, supporting Newmont's multiyear capital plans—the company reported US$2.3bn sustaining capex in 2024, underscoring predictability.

Operating focus in these regions reduced geopolitical exposure versus peers, protecting shareholders from the extreme volatility seen in several emerging-market mining jurisdictions through 2025.

Resource nationalism in emerging markets

Operations in parts of Africa and South America face resource nationalism risk, with governments pushing higher taxes, mandatory state equity and revised codes; e.g., Peru proposed royalty hikes affecting miners' margins and Ghana has sought increased state stakes, putting pressure on Newmont's 2024 adjusted EBITDA of $4.2B.

Trade policies and export restrictions

Global trade tensions and shifting alliances affect movement of concentrates and refined metals, with 2024 WTO data showing global trade growth slowing to 1.8% and trade barriers rising; Newmont faces higher logistics and treatment charges when borders tighten. Recent export duty changes in major copper/gold producers—e.g., Peru’s temporary export measures in 2023 and Indonesia’s 2024 mineral export policies—can increase Newmont’s unit costs and delay shipments. Monitoring geopolitical shifts helps Newmont protect access to smelters/refineries and adapt marketing to secure long-term offtake and maintain 2024–25 production targets.

Government relations post merger integration

Following the US$19.5bn acquisition of Newcrest in 2023, Newmont has been renegotiating terms with governments across Australia, Indonesia and Papua New Guinea to align governance, honor legacy community agreements and meet fiscal obligations tied to the deal.

Maintaining status as a preferred partner requires meeting local content, royalty and ESG commitments; lapses could affect ~30% of combined regional production and future permitting.

- US$19.5bn acquisition (2023)

- ~30% of combined regional production at stake

- Focus: local content, royalties, ESG, legacy agreements

Mining royalty and tax reforms

Many jurisdictions are reassessing fiscal regimes to capture more mining rents amid commodity volatility and rising sovereign debt; IMF reported mining-tax reviews increased 25% globally in 2024.

Proposed royalty hikes or windfall taxes could cut Newmont’s free cash flow and lower project IRRs—e.g., a 2% royalty rise could reduce NI by hundreds of millions annually given 2024 revenue of ~$12.4bn.

Newmont lobbies for balanced tax frameworks, engaging governments and ICMM to protect investment attractiveness while acknowledging revenue needs.

- IMF: 25% rise in mining-tax reviews (2024)

- 2024 revenue ~$12.4bn; 2% royalty ≈ hundreds of millions impact

- Active advocacy via ICMM and industry dialogues

Political risk in Peru/Ghana/Indonesia/PNG could threaten ~30% production, pressuring $4.2B EBITDA

Political risks concentrated in Tier 1 jurisdictions reduce abrupt regime risk, but exposure in Peru, Ghana, Indonesia and PNG raises fiscal and permitting uncertainty that could hit ~30% of combined regional production and pressure 2024 adjusted EBITDA of $4.2B; IMF flagged a 25% rise in mining-tax reviews in 2024.

| Metric | Value |

|---|---|

| 2024 revenue | $12.4B |

| 2024 adj. EBITDA | $4.2B |

| Acquisition | $19.5B (Newcrest, 2023) |

| At-risk production | ~30% |

| IMF: mining-tax reviews (2024) | +25% |

What is included in the product

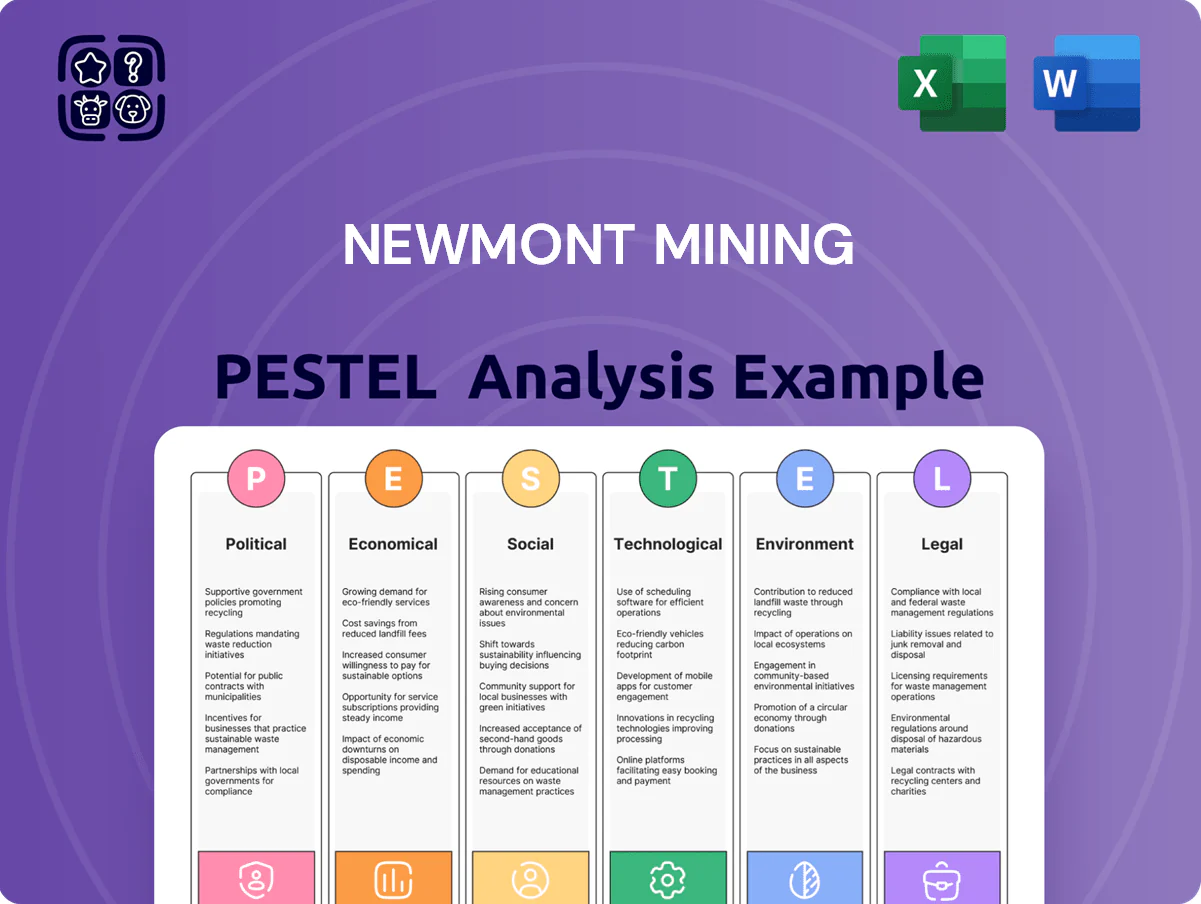

Explores how macro-environmental factors uniquely affect Newmont Mining across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and region-specific trends to identify risks and opportunities.

A concise Newmont Mining PESTLE summary that’s visually segmented for quick meetings, easily editable for regional or business-line notes, and ready to drop into presentations to support risk discussions and cross-team alignment.

Economic factors

Gold price volatility and safe haven demand

As the world’s largest gold producer, Newmont’s revenue is highly sensitive to spot gold movements; a 10% change in gold price can shift annual revenue by roughly $2–3 billion based on 2024–2025 production and pricing levels. By end-2025, persistent inflation and geopolitical tensions kept gold elevated near $1,900–2,000/oz, sustaining safe-haven demand. Newmont’s scale and 2025 all-in sustaining costs around $1,100–1,200/oz help preserve margins through temporary price pullbacks.

Copper demand for the green energy transition

Newmont has increased copper exposure, aligning with predicted demand growth; BloombergNEF estimates cumulative copper demand for energy transition could reach +60% by 2035 vs 2022, supporting higher long-term prices.

Projected structural deficits—ICSG and S&P GL suggest supply shortfalls of several million tonnes by the early 2030s—benefit Newmont’s copper assets and projects.

Diversifying into industrial metals balances Newmont’s gold-heavy portfolio and captures a high-growth market as EVs and renewables drive sustained copper intensity per vehicle (300–400 kg for BEVs vs ~20–50 kg for ICE).

Inflationary pressures on operational costs

Rising labor, energy and consumable costs—cyanide up ~18% and steel ~12% year-on-year in 2024—pressure Newmont’s margins as diesel averaged ~USD 1.10/litre and electricity tariffs rose in key jurisdictions by ~6–9% in 2024.

Newmont reported 2024 site cost improvements and $1.2 billion in sustainability and efficiency investments to offset inflation through fleet electrification and renewables.

Rigorous cost control, hedging, and supply-chain optimization helped Newmont limit AISC volatility, keeping 2024 adjusted AISC near guidance at about $1,050/oz.

Currency exchange rate fluctuations

Newmont operates across Australia, Canada and other jurisdictions, incurring costs in AUD, CAD and local currencies while reporting revenues in USD; a 10% AUD/USD move altered operating margins at Australian sites materially in 2023–2025.

Exchange-rate swings can therefore cause volatility in reported EPS and site-level competitiveness; Newmont reported FX impacts of roughly $150–300 million on cash flows in 2024.

The company employs financial hedges and natural hedges (USD-priced sales, local sourcing) to reduce exposure and stabilize outcomes.

- Operations: multi-currency costs (AUD, CAD)

- Reported FX impact: ~$150–300M (2024)

- Hedges: financial instruments + natural hedges

Global interest rate environment

The global interest rate environment shapes Newmont’s cost of capital and valuation metrics; higher central bank rates raise debt service costs and discount rates applied to long‑life mining assets, compressing NPV. In 2024, US Fed policy rates near 5.25–5.50% raised borrowing costs, but Newmont’s investment‑grade rating (S&P BBB, Moody’s Baa2 as of 2024) and $4.2bn liquidity position preserved access to financing.

- Higher rates → higher discount rates, lower project NPVs

- Raises cost of debt for capital‑intensive projects

- Shifts investor preference between bullion and yield

- Newmont’s BBB/Baa2 rating and ~$4.2bn liquidity mitigate funding risk

Newmont: Gold at $1.9–2k, AISC ~$1.05–1.2k, FX swings hit $150–300m; $4.2bn liquidity

Gold price swings drive ~$2–3bn revenue per 10% move (2024–25); 2025 gold ~1,900–2,000/oz. AISC ~$1,100–1,200/oz; 2024 adjusted AISC ~1,050/oz. Copper demand +60% by 2035 (BNEF) supports Newmont’s copper pivot. 2024 FX hit cash flows ~$150–300m; AUD/USD 10% swing materially affects margins. Net liquidity ~$4.2bn; rating S&P BBB / Moody’s Baa2 (2024).

| Metric | 2024–25 |

|---|---|

| Gold price | $1,900–2,000/oz |

| AISC | $1,050–1,200/oz |

| FX impact | $150–300m |

| Liquidity | $4.2bn |

What You See Is What You Get

Newmont Mining PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use, containing a concise PESTLE analysis of Newmont Mining covering political, economic, social, technological, legal, and environmental factors.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how regulatory shifts, commodity cycles, and sustainability trends are shaping Newmont Mining’s strategic prospects—our concise PESTLE snapshot highlights the key external pressures and opportunities that matter to investors and strategists. Purchase the full PESTLE analysis for a complete, actionable breakdown you can use to stress-test portfolios, inform M&A, or guide boardroom decisions.

Political factors

Geopolitical stability in Tier 1 jurisdictions

Newmont holds ~60% of attributable gold reserves and major operations in Australia and North America, shielding the firm from abrupt regime change risks that affect emerging markets.

Tier 1 jurisdictions offer stable permitting and tax regimes, supporting Newmont's multiyear capital plans—the company reported US$2.3bn sustaining capex in 2024, underscoring predictability.

Operating focus in these regions reduced geopolitical exposure versus peers, protecting shareholders from the extreme volatility seen in several emerging-market mining jurisdictions through 2025.

Resource nationalism in emerging markets

Operations in parts of Africa and South America face resource nationalism risk, with governments pushing higher taxes, mandatory state equity and revised codes; e.g., Peru proposed royalty hikes affecting miners' margins and Ghana has sought increased state stakes, putting pressure on Newmont's 2024 adjusted EBITDA of $4.2B.

Trade policies and export restrictions

Global trade tensions and shifting alliances affect movement of concentrates and refined metals, with 2024 WTO data showing global trade growth slowing to 1.8% and trade barriers rising; Newmont faces higher logistics and treatment charges when borders tighten. Recent export duty changes in major copper/gold producers—e.g., Peru’s temporary export measures in 2023 and Indonesia’s 2024 mineral export policies—can increase Newmont’s unit costs and delay shipments. Monitoring geopolitical shifts helps Newmont protect access to smelters/refineries and adapt marketing to secure long-term offtake and maintain 2024–25 production targets.

Government relations post merger integration

Following the US$19.5bn acquisition of Newcrest in 2023, Newmont has been renegotiating terms with governments across Australia, Indonesia and Papua New Guinea to align governance, honor legacy community agreements and meet fiscal obligations tied to the deal.

Maintaining status as a preferred partner requires meeting local content, royalty and ESG commitments; lapses could affect ~30% of combined regional production and future permitting.

- US$19.5bn acquisition (2023)

- ~30% of combined regional production at stake

- Focus: local content, royalties, ESG, legacy agreements

Mining royalty and tax reforms

Many jurisdictions are reassessing fiscal regimes to capture more mining rents amid commodity volatility and rising sovereign debt; IMF reported mining-tax reviews increased 25% globally in 2024.

Proposed royalty hikes or windfall taxes could cut Newmont’s free cash flow and lower project IRRs—e.g., a 2% royalty rise could reduce NI by hundreds of millions annually given 2024 revenue of ~$12.4bn.

Newmont lobbies for balanced tax frameworks, engaging governments and ICMM to protect investment attractiveness while acknowledging revenue needs.

- IMF: 25% rise in mining-tax reviews (2024)

- 2024 revenue ~$12.4bn; 2% royalty ≈ hundreds of millions impact

- Active advocacy via ICMM and industry dialogues

Political risk in Peru/Ghana/Indonesia/PNG could threaten ~30% production, pressuring $4.2B EBITDA

Political risks concentrated in Tier 1 jurisdictions reduce abrupt regime risk, but exposure in Peru, Ghana, Indonesia and PNG raises fiscal and permitting uncertainty that could hit ~30% of combined regional production and pressure 2024 adjusted EBITDA of $4.2B; IMF flagged a 25% rise in mining-tax reviews in 2024.

| Metric | Value |

|---|---|

| 2024 revenue | $12.4B |

| 2024 adj. EBITDA | $4.2B |

| Acquisition | $19.5B (Newcrest, 2023) |

| At-risk production | ~30% |

| IMF: mining-tax reviews (2024) | +25% |

What is included in the product

Explores how macro-environmental factors uniquely affect Newmont Mining across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and region-specific trends to identify risks and opportunities.

A concise Newmont Mining PESTLE summary that’s visually segmented for quick meetings, easily editable for regional or business-line notes, and ready to drop into presentations to support risk discussions and cross-team alignment.

Economic factors

Gold price volatility and safe haven demand

As the world’s largest gold producer, Newmont’s revenue is highly sensitive to spot gold movements; a 10% change in gold price can shift annual revenue by roughly $2–3 billion based on 2024–2025 production and pricing levels. By end-2025, persistent inflation and geopolitical tensions kept gold elevated near $1,900–2,000/oz, sustaining safe-haven demand. Newmont’s scale and 2025 all-in sustaining costs around $1,100–1,200/oz help preserve margins through temporary price pullbacks.

Copper demand for the green energy transition

Newmont has increased copper exposure, aligning with predicted demand growth; BloombergNEF estimates cumulative copper demand for energy transition could reach +60% by 2035 vs 2022, supporting higher long-term prices.

Projected structural deficits—ICSG and S&P GL suggest supply shortfalls of several million tonnes by the early 2030s—benefit Newmont’s copper assets and projects.

Diversifying into industrial metals balances Newmont’s gold-heavy portfolio and captures a high-growth market as EVs and renewables drive sustained copper intensity per vehicle (300–400 kg for BEVs vs ~20–50 kg for ICE).

Inflationary pressures on operational costs

Rising labor, energy and consumable costs—cyanide up ~18% and steel ~12% year-on-year in 2024—pressure Newmont’s margins as diesel averaged ~USD 1.10/litre and electricity tariffs rose in key jurisdictions by ~6–9% in 2024.

Newmont reported 2024 site cost improvements and $1.2 billion in sustainability and efficiency investments to offset inflation through fleet electrification and renewables.

Rigorous cost control, hedging, and supply-chain optimization helped Newmont limit AISC volatility, keeping 2024 adjusted AISC near guidance at about $1,050/oz.

Currency exchange rate fluctuations

Newmont operates across Australia, Canada and other jurisdictions, incurring costs in AUD, CAD and local currencies while reporting revenues in USD; a 10% AUD/USD move altered operating margins at Australian sites materially in 2023–2025.

Exchange-rate swings can therefore cause volatility in reported EPS and site-level competitiveness; Newmont reported FX impacts of roughly $150–300 million on cash flows in 2024.

The company employs financial hedges and natural hedges (USD-priced sales, local sourcing) to reduce exposure and stabilize outcomes.

- Operations: multi-currency costs (AUD, CAD)

- Reported FX impact: ~$150–300M (2024)

- Hedges: financial instruments + natural hedges

Global interest rate environment

The global interest rate environment shapes Newmont’s cost of capital and valuation metrics; higher central bank rates raise debt service costs and discount rates applied to long‑life mining assets, compressing NPV. In 2024, US Fed policy rates near 5.25–5.50% raised borrowing costs, but Newmont’s investment‑grade rating (S&P BBB, Moody’s Baa2 as of 2024) and $4.2bn liquidity position preserved access to financing.

- Higher rates → higher discount rates, lower project NPVs

- Raises cost of debt for capital‑intensive projects

- Shifts investor preference between bullion and yield

- Newmont’s BBB/Baa2 rating and ~$4.2bn liquidity mitigate funding risk

Newmont: Gold at $1.9–2k, AISC ~$1.05–1.2k, FX swings hit $150–300m; $4.2bn liquidity

Gold price swings drive ~$2–3bn revenue per 10% move (2024–25); 2025 gold ~1,900–2,000/oz. AISC ~$1,100–1,200/oz; 2024 adjusted AISC ~1,050/oz. Copper demand +60% by 2035 (BNEF) supports Newmont’s copper pivot. 2024 FX hit cash flows ~$150–300m; AUD/USD 10% swing materially affects margins. Net liquidity ~$4.2bn; rating S&P BBB / Moody’s Baa2 (2024).

| Metric | 2024–25 |

|---|---|

| Gold price | $1,900–2,000/oz |

| AISC | $1,050–1,200/oz |

| FX impact | $150–300m |

| Liquidity | $4.2bn |

What You See Is What You Get

Newmont Mining PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use, containing a concise PESTLE analysis of Newmont Mining covering political, economic, social, technological, legal, and environmental factors.