Nexa SWOT Analysis

Your Strategic Toolkit Starts Here

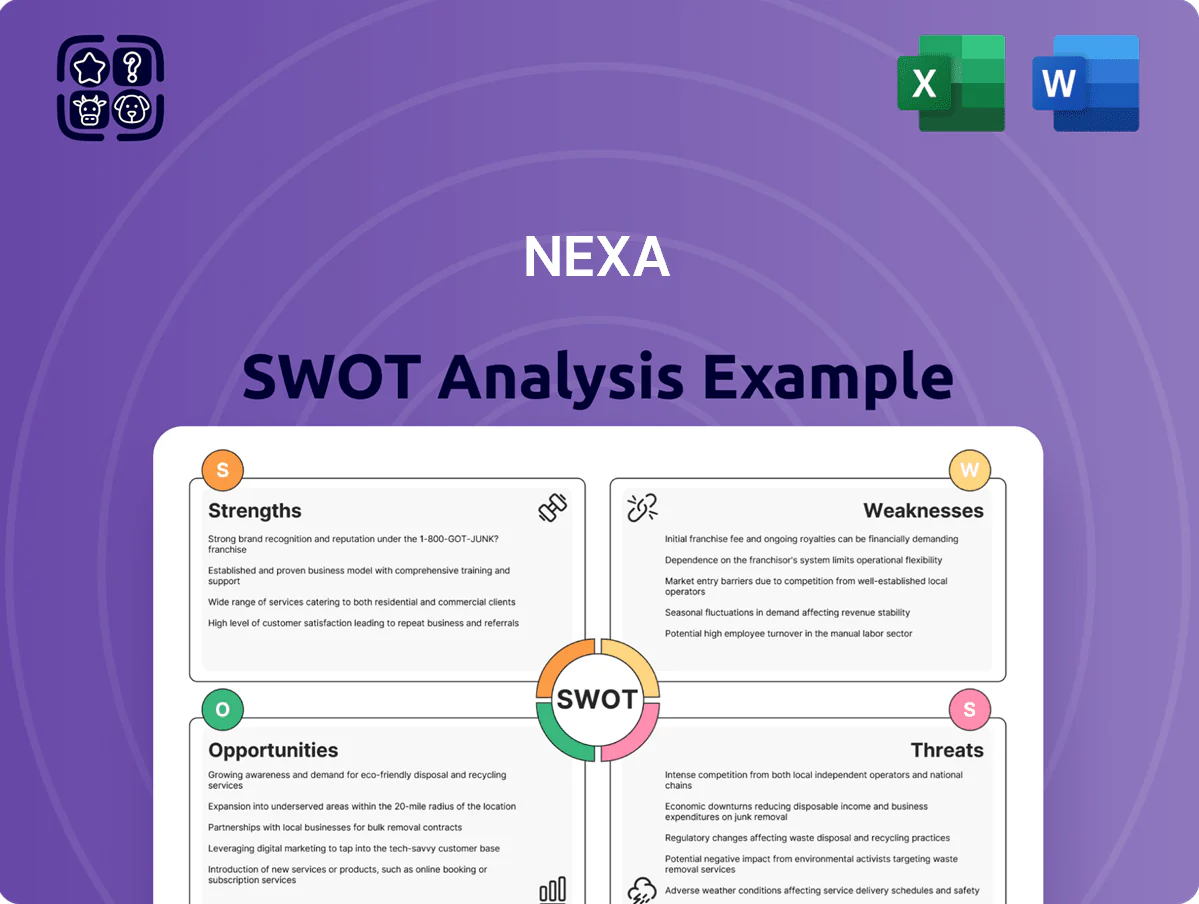

Nexa’s strengths in operational scale and tech-driven customer reach position it well against rising competition, but supply-chain constraints and regulatory shifts could temper near-term growth; our full SWOT unpacks these dynamics with data-backed implications. Purchase the complete analysis for a professionally formatted, editable report and Excel tools to strategize, pitch, or invest with confidence.

Strengths

Top-tier Global Zinc Producer

Nexa Resources is among the world’s top zinc producers, with 2024 zinc output around 600 ktZn (thousand tonnes of zinc) and forecasted 2025 output above 620 ktZn, giving it material scale and market influence.

This scale strengthened Nexa’s role in global supply chains for construction and automotive by end-2025, supporting long-term offtake deals and sales to >30 countries.

Large volumes boost negotiation power with suppliers and customers, lowering unit costs and enabling multi-year contracts covering >70% of planned output.

Vertically Integrated Business Model

Strategic Asset Location in Mining Hubs

Operating mainly in Brazil and Peru gives Nexa Resources access to long-established mining regions with infrastructure; in 2024 these two countries accounted for about 85% of Nexa’s zinc and copper concentrate production, lowering capex per tonne versus greenfield sites.

Local skilled labor reduces training costs and boosts plant uptime; Nexa reported 92% utilization at its Peruvian zinc operations in 2024, cutting unit cash costs by roughly 8% year-on-year.

Proximity to South American markets trims shipping; regional sales made up ~40% of revenue in 2024, cutting logistics spend versus global export hubs.

Concentrated footprint allows centralized logistics and compliance teams across two jurisdictions, simplifying permitting and reducing administrative overhead by an estimated 10–15% versus multi-country operations.

Diversified Multi-Metal Revenue Stream

Nexa’s zinc-led portfolio also produced 256 kt of copper-equivalent byproducts in 2024, with copper, lead, silver and gold contributing about 28% of revenue, cushioning zinc price swings.

These byproducts act as a hedge since zinc, copper and precious metals follow different cycles; copper’s 2024 LME average price was ~$9,300/t, supporting long-term demand tied to electrification.

Advanced Underground Mining Expertise

Nexa: Leading Zinc Producer — 600kt Zn (2024), 27% Margin, 70%+ Contracted Output

Nexa is a top zinc producer (~600 ktZn in 2024; >620 ktZn forecast 2025), with vertical integration (5 mines, 3 smelters) yielding ~789 kt Zn-eq in 2024, gross margin ~27% and byproduct revenue ~28% of sales; 92% plant utilization (Peru 2024), ore recovery ~88%, LTIFR 1.8 and multi-year contracts covering >70% output.

| Metric | 2024 | 2025F |

|---|---|---|

| Zinc output | 600 ktZn | >620 ktZn |

| Zn-eq output | 789 kt | - |

| Gross margin | 27% | - |

| Byproduct rev | 28% | - |

| Utilization (Peru) | 92% | - |

| Ore recovery | 88% | - |

| LTIFR | 1.8 | - |

| Contracted output | 70%+ | - |

What is included in the product

Offers a concise strategic overview of Nexa by highlighting its core strengths and weaknesses, mapping market opportunities and external threats, and framing the competitive and operational factors that will shape the company’s future performance.

Offers a compact Nexa SWOT summary for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

Geographic Concentration Risk

High Operational Costs at Mature Mines

Several of Nexa Resources’ older Peruvian and Brazilian mines face rising costs from deeper mining and aging infrastructure; in 2024 site-level cash costs rose to about 0.86 USD/lb Zn eq, up 12% vs 2022 as lower grades forced more stripping and energy use.

Significant Debt Obligations

The capital-intensive ramp-up of Aripuanã and other mines has pushed Nexa Resources S.A. net debt to about $1.1 billion as of Q3 2025, forcing large interest and principal payments that consume operating cash flow.

High debt servicing reduced free cash flow, constraining exploration budgets and dividend capacity—Nexa paid no ordinary dividend in 2024 after capex surged to ~$480 million.

If global rates stay elevated and Aripuanã’s EBITDA lags the projected $230–260 million/year, financial flexibility and refinancing risk will rise materially.

Environmental and Tailings Management Burdens

- 2024 enviro spend ~$310m

- Compliance capex +12% YoY

- Single-incident liability risk >$1bn

Sensitivity to Global Commodity Cycles

Nexa faces sovereign, ESG and zinc-price risk as rising costs and debt squeeze cash

| Metric | Value |

|---|---|

| Prod / Rev concentration (2024) | 92% / 88% |

| Site cash cost (2024) | $0.86 USD/lb Zn eq |

| Net debt (Q3 2025) | $1.1bn |

| Enviro spend (2024) | $310m |

| EBITDA zinc exposure (2024) | 72% |

Preview the Actual Deliverable

Nexa SWOT Analysis

This is the actual Nexa SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version becomes available after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Nexa’s strengths in operational scale and tech-driven customer reach position it well against rising competition, but supply-chain constraints and regulatory shifts could temper near-term growth; our full SWOT unpacks these dynamics with data-backed implications. Purchase the complete analysis for a professionally formatted, editable report and Excel tools to strategize, pitch, or invest with confidence.

Strengths

Top-tier Global Zinc Producer

Nexa Resources is among the world’s top zinc producers, with 2024 zinc output around 600 ktZn (thousand tonnes of zinc) and forecasted 2025 output above 620 ktZn, giving it material scale and market influence.

This scale strengthened Nexa’s role in global supply chains for construction and automotive by end-2025, supporting long-term offtake deals and sales to >30 countries.

Large volumes boost negotiation power with suppliers and customers, lowering unit costs and enabling multi-year contracts covering >70% of planned output.

Vertically Integrated Business Model

Strategic Asset Location in Mining Hubs

Operating mainly in Brazil and Peru gives Nexa Resources access to long-established mining regions with infrastructure; in 2024 these two countries accounted for about 85% of Nexa’s zinc and copper concentrate production, lowering capex per tonne versus greenfield sites.

Local skilled labor reduces training costs and boosts plant uptime; Nexa reported 92% utilization at its Peruvian zinc operations in 2024, cutting unit cash costs by roughly 8% year-on-year.

Proximity to South American markets trims shipping; regional sales made up ~40% of revenue in 2024, cutting logistics spend versus global export hubs.

Concentrated footprint allows centralized logistics and compliance teams across two jurisdictions, simplifying permitting and reducing administrative overhead by an estimated 10–15% versus multi-country operations.

Diversified Multi-Metal Revenue Stream

Nexa’s zinc-led portfolio also produced 256 kt of copper-equivalent byproducts in 2024, with copper, lead, silver and gold contributing about 28% of revenue, cushioning zinc price swings.

These byproducts act as a hedge since zinc, copper and precious metals follow different cycles; copper’s 2024 LME average price was ~$9,300/t, supporting long-term demand tied to electrification.

Advanced Underground Mining Expertise

Nexa: Leading Zinc Producer — 600kt Zn (2024), 27% Margin, 70%+ Contracted Output

Nexa is a top zinc producer (~600 ktZn in 2024; >620 ktZn forecast 2025), with vertical integration (5 mines, 3 smelters) yielding ~789 kt Zn-eq in 2024, gross margin ~27% and byproduct revenue ~28% of sales; 92% plant utilization (Peru 2024), ore recovery ~88%, LTIFR 1.8 and multi-year contracts covering >70% output.

| Metric | 2024 | 2025F |

|---|---|---|

| Zinc output | 600 ktZn | >620 ktZn |

| Zn-eq output | 789 kt | - |

| Gross margin | 27% | - |

| Byproduct rev | 28% | - |

| Utilization (Peru) | 92% | - |

| Ore recovery | 88% | - |

| LTIFR | 1.8 | - |

| Contracted output | 70%+ | - |

What is included in the product

Offers a concise strategic overview of Nexa by highlighting its core strengths and weaknesses, mapping market opportunities and external threats, and framing the competitive and operational factors that will shape the company’s future performance.

Offers a compact Nexa SWOT summary for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

Geographic Concentration Risk

High Operational Costs at Mature Mines

Several of Nexa Resources’ older Peruvian and Brazilian mines face rising costs from deeper mining and aging infrastructure; in 2024 site-level cash costs rose to about 0.86 USD/lb Zn eq, up 12% vs 2022 as lower grades forced more stripping and energy use.

Significant Debt Obligations

The capital-intensive ramp-up of Aripuanã and other mines has pushed Nexa Resources S.A. net debt to about $1.1 billion as of Q3 2025, forcing large interest and principal payments that consume operating cash flow.

High debt servicing reduced free cash flow, constraining exploration budgets and dividend capacity—Nexa paid no ordinary dividend in 2024 after capex surged to ~$480 million.

If global rates stay elevated and Aripuanã’s EBITDA lags the projected $230–260 million/year, financial flexibility and refinancing risk will rise materially.

Environmental and Tailings Management Burdens

- 2024 enviro spend ~$310m

- Compliance capex +12% YoY

- Single-incident liability risk >$1bn

Sensitivity to Global Commodity Cycles

Nexa faces sovereign, ESG and zinc-price risk as rising costs and debt squeeze cash

| Metric | Value |

|---|---|

| Prod / Rev concentration (2024) | 92% / 88% |

| Site cash cost (2024) | $0.86 USD/lb Zn eq |

| Net debt (Q3 2025) | $1.1bn |

| Enviro spend (2024) | $310m |

| EBITDA zinc exposure (2024) | 72% |

Preview the Actual Deliverable

Nexa SWOT Analysis

This is the actual Nexa SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version becomes available after checkout.