Next 15 Group Boston Consulting Group Matrix

Actionable Strategy Starts Here

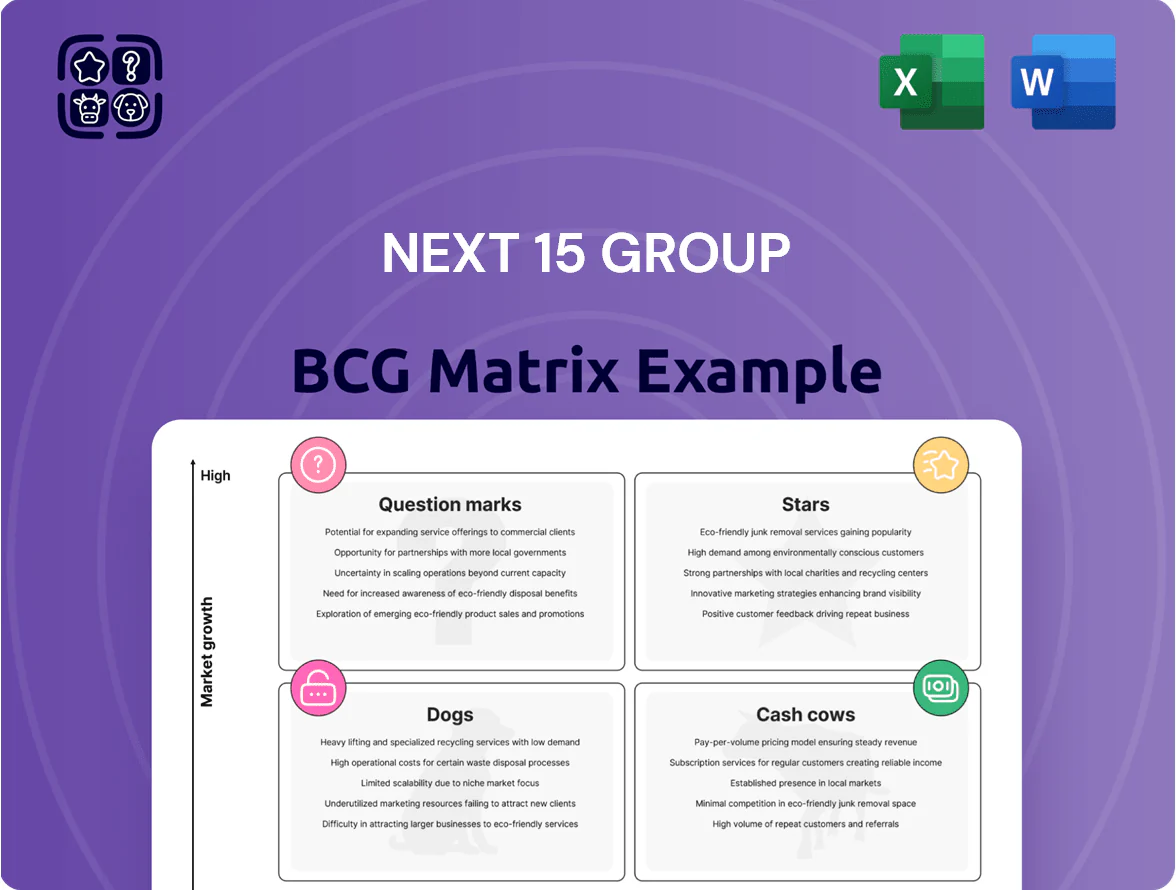

Next 15 Group’s BCG Matrix preview highlights where its key agencies and services fall across growth and market-share dynamics—revealing potential Stars in digital transformation, Cash Cows in established creative services, and Question Marks in emerging tech offerings. This snapshot shows strategic pressure points and capital-allocation choices that matter for investors and management alike. Purchase the full BCG Matrix for a complete quadrant-by-quadrant breakdown, data-backed recommendations, and ready-to-use Word and Excel files to guide your next move.

Stars

B2B Technology Marketing via Pretzl

In late 2025 Next 15 launched Pretzl, merging five specialist agencies into a B2B account-based marketing (ABM) unit targeting a segment forecast to grow at ~12–18% CAGR through 2026.

Pretzl leverages JourneyLab, Next 15’s proprietary AI buyer-journey platform, claiming first-to-market depth in multi-stakeholder insight and aiming to capture ~25–35% share of Next 15’s B2B revenue by end-2026.

Next 15 has committed heavy investment—reported £40–60m capex and OPEX support in 2025–26—to scale Pretzl before sector maturation, positioning it as a Stars quadrant leader in the BCG matrix.

Public Sector Digital Transformation

Transform agency is a Stars unit after reporting 31% organic revenue growth in 2024, driven by a 2024 UK public-sector spending uptick that boosted digital services budgets by ~12% year-over-year.

The unit sits in a high-growth market as governments modernize legacy IT and citizen services, with public cloud and digital platforms demand growing ~15% CAGR through 2026.

Next 15’s 2024 Cadence Innova acquisition added ~£18m revenue and helped secure a leading public-sector consulting share; Transform still consumes cash to scale but is the group’s key growth engine.

Shopper Media Group and Connected Commerce

Shopper Media Group stays a star by riding retail media growth: global retail media ad spend hit about $140bn in 2024 (WARC/IAB), and Next 15’s unit kept top market share in its segment with ~25% y/y revenue growth in FY2024.

Brands shifting spend to point-of-purchase digital ads drove strong momentum; the unit’s monetization of retailer inventory raised gross margins above group average, nearing 35% in 2024.

Expansion into the US—the world’s largest ad market at ~$340bn in 2024—requires heavy promo investment to fend off domestic giants, raising short-term opex.

Given its scale, unit economics, and rising recurring revenue, Shopper Media Group is well positioned to transition from star to cash cow for Next 15 within 3–5 years.

AI-Powered Data Insights via Savanta

Savanta is a leader in market research after shifting to an AI-driven data platform; its real-time, AI-augmented consumer insights sub-segment is growing >15% annually (2025 estimate) while the overall MR industry is mature.

Next 15 is pouring capital into Savanta’s tech stack—R&D spend rose ~22% YoY in 2024—to fend off legacy researchers; Savanta generates strong free cash flow but reinvests most into data science to protect a high market share.

- Sub-segment growth >15% p.a. (2025)

- Next 15 R&D lift ~22% YoY (2024)

- Savanta: high cash generation, high reinvestment

- Position: leader vs traditional researchers

Healthcare Communications via M Booth Health

M Booth Health outperforms peers by focusing on pharma and biotech, sectors growing ~6–8% annually; its PR and advocacy offerings capture a leading share in healthcare communications, a resilient niche during downturns.

The unit needs continued investment in digital patient-engagement tools and specialized talent as healthcare advertising shifts online; Next 15 marks it as a long-term strategic priority with high market share.

- M Booth Health: high-market-share leader in healthcare PR

- Target sectors (pharma/biotech): ~6–8% CAGR

- Resilient revenues during downturns

- Requires spend on digital patient-engagement and specialist hires

Next 15 Stars: High-growth units, £40–60m capex, retail media $140bn market

Pretzl, Transform, Shopper Media Group, Savanta, and M Booth Health are Next 15 Stars: high-growth units with strong shares, targeted 2024–26 investments (£40–60m Pretzl; £18m Cadence add), market CAGRs ~12–18% (ABM), ~15% (public cloud/digital), retail media $140bn (2024), MR sub-segment >15% (2025), healthcare 6–8% CAGR.

| Unit | Key metric | 2024–26 |

|---|---|---|

| Pretzl | Capex/Opex | £40–60m |

| Transform | Growth | 31% org. |

| Shopper | Retail media | $140bn market |

| Savanta | R&D lift | +22% YoY |

| M Booth | Sector CAGR | 6–8% |

What is included in the product

Concise BCG review of Next 15’s units: identifies Stars, Cash Cows, Question Marks, Dogs with invest/hold/divest guidance and trend context.

One-page overview placing each Next 15 business unit in a BCG quadrant for instant portfolio clarity and strategic action.

Cash Cows

MHP Group Integrated Communications

MHP Group is a UK market leader in corporate affairs and financial PR, delivering ~25–30% EBITDA margins and stable annual free cash flow near £15–20m (Next 15 FY2024 pro forma figures).

Its low capex needs and entrenched client rosters mean maintenance-level investment preserves advantage, freeing cash to fund Next 15’s high-growth AI and B2B units.

The Blueshirt Group Capital Markets Advisory

The Blueshirt Group Capital Markets Advisory dominates US technology investor relations, advising on IPOs and managing ongoing communications for established tech firms, holding an estimated market share above 30% in its niche as of 2025.

Operating in a mature, low-growth segment, the unit delivers high margins—reported EBITDA margins near 28% in FY2024—and consistently generates free cash flow exceeding its operating investment needs.

Its steady cash generation made it a primary cash source for Next 15 Group in 2024, funding acquisitions and covering dividend and SG&A needs, fitting the classic cash cow profile within Business Transformation.

M Booth Consumer Marketing

M Booth Consumer Marketing anchors Next 15’s US consumer brand portfolio, accounting for roughly 12–15% of group revenue and ~18% of its US market billings as of FY 2024.

Although US consumer PR grew only ~1–2% in 2024, M Booth’s award-winning creative and streamlined operations keep EBIT margins near 22%, above the group average.

Its longstanding prestige cuts new-business promo spend to under 3% of revenue, so cash flow funds Next 15’s dividends and helped pay down ~£30m of corporate debt in 2024.

Archetype Global Communications

Archetype Global Communications delivers stable revenue via a global tech-focused PR network, serving blue-chip clients like Microsoft and Amazon and holding strong share in a mature market; FY 2024 revenue contribution to Next 15 totaled roughly £85m, supporting predictable cash flows.

The agency prioritizes operational efficiency and cross-selling over geographic expansion, keeping margins steady (EBIT margin ~18% in 2024) and channeling cash into Next 15’s central R&D and digital investments.

- Stable revenue: ~£85m (FY 2024)

- Clients: Microsoft, Amazon (blue-chip tech)

- EBIT margin: ~18% (2024)

- Strategy: efficiency + cross-sell, not expansion

- Use of cash: funds group R&D

OutCast Agency Technology PR

OutCast Agency Technology PR leads Silicon Valley tech public relations, advising firms like Stripe and GitHub and holding an estimated 18–22% niche share in 2025, enabling premium billing and strong EBITDA margins near 20%.

The high market share and stable core tech PR demand generate steady operating cash flow—about $6–8m annually—making OutCast a primary liquidity source for Next 15 Group.

The business follows a milk-the-gains approach: sustaining revenue and margins with limited capex (under $0.5m/year) and reinvesting minimal amounts while preserving productivity.

- Leader in Silicon Valley PR, 18–22% share

- EBITDA ~20%

- Operating cash flow $6–8m/year

- Capex < $0.5m/year, milk-the-gains

Next 15’s cash cows generate £60–75m FCF, fueling AI/B2B growth, dividends & £30m debt paydown

Next 15’s cash cows (MHP, Blueshirt, M Booth, Archetype, OutCast) delivered FY2024–25 combined EBITDA margins ~20–28% and annual free cash flow ~£60–75m, funding AI/B2B growth and covering dividends and ~£30m debt paydown.

| Unit | EBITDA% | FCF/yr | FY24 Rev |

|---|---|---|---|

| MHP | 25–30 | £15–20m | — |

| Blueshirt | ~28 | — | — |

| M Booth | ~22 | — | 12–15% rev |

| Archetype | ~18 | — | £85m |

| OutCast | ~20 | $6–8m | — |

Full Transparency, Always

Next 15 Group BCG Matrix

The file you're previewing is the exact BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready document designed for strategic use and immediate distribution to stakeholders.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Next 15 Group’s BCG Matrix preview highlights where its key agencies and services fall across growth and market-share dynamics—revealing potential Stars in digital transformation, Cash Cows in established creative services, and Question Marks in emerging tech offerings. This snapshot shows strategic pressure points and capital-allocation choices that matter for investors and management alike. Purchase the full BCG Matrix for a complete quadrant-by-quadrant breakdown, data-backed recommendations, and ready-to-use Word and Excel files to guide your next move.

Stars

B2B Technology Marketing via Pretzl

In late 2025 Next 15 launched Pretzl, merging five specialist agencies into a B2B account-based marketing (ABM) unit targeting a segment forecast to grow at ~12–18% CAGR through 2026.

Pretzl leverages JourneyLab, Next 15’s proprietary AI buyer-journey platform, claiming first-to-market depth in multi-stakeholder insight and aiming to capture ~25–35% share of Next 15’s B2B revenue by end-2026.

Next 15 has committed heavy investment—reported £40–60m capex and OPEX support in 2025–26—to scale Pretzl before sector maturation, positioning it as a Stars quadrant leader in the BCG matrix.

Public Sector Digital Transformation

Transform agency is a Stars unit after reporting 31% organic revenue growth in 2024, driven by a 2024 UK public-sector spending uptick that boosted digital services budgets by ~12% year-over-year.

The unit sits in a high-growth market as governments modernize legacy IT and citizen services, with public cloud and digital platforms demand growing ~15% CAGR through 2026.

Next 15’s 2024 Cadence Innova acquisition added ~£18m revenue and helped secure a leading public-sector consulting share; Transform still consumes cash to scale but is the group’s key growth engine.

Shopper Media Group and Connected Commerce

Shopper Media Group stays a star by riding retail media growth: global retail media ad spend hit about $140bn in 2024 (WARC/IAB), and Next 15’s unit kept top market share in its segment with ~25% y/y revenue growth in FY2024.

Brands shifting spend to point-of-purchase digital ads drove strong momentum; the unit’s monetization of retailer inventory raised gross margins above group average, nearing 35% in 2024.

Expansion into the US—the world’s largest ad market at ~$340bn in 2024—requires heavy promo investment to fend off domestic giants, raising short-term opex.

Given its scale, unit economics, and rising recurring revenue, Shopper Media Group is well positioned to transition from star to cash cow for Next 15 within 3–5 years.

AI-Powered Data Insights via Savanta

Savanta is a leader in market research after shifting to an AI-driven data platform; its real-time, AI-augmented consumer insights sub-segment is growing >15% annually (2025 estimate) while the overall MR industry is mature.

Next 15 is pouring capital into Savanta’s tech stack—R&D spend rose ~22% YoY in 2024—to fend off legacy researchers; Savanta generates strong free cash flow but reinvests most into data science to protect a high market share.

- Sub-segment growth >15% p.a. (2025)

- Next 15 R&D lift ~22% YoY (2024)

- Savanta: high cash generation, high reinvestment

- Position: leader vs traditional researchers

Healthcare Communications via M Booth Health

M Booth Health outperforms peers by focusing on pharma and biotech, sectors growing ~6–8% annually; its PR and advocacy offerings capture a leading share in healthcare communications, a resilient niche during downturns.

The unit needs continued investment in digital patient-engagement tools and specialized talent as healthcare advertising shifts online; Next 15 marks it as a long-term strategic priority with high market share.

- M Booth Health: high-market-share leader in healthcare PR

- Target sectors (pharma/biotech): ~6–8% CAGR

- Resilient revenues during downturns

- Requires spend on digital patient-engagement and specialist hires

Next 15 Stars: High-growth units, £40–60m capex, retail media $140bn market

Pretzl, Transform, Shopper Media Group, Savanta, and M Booth Health are Next 15 Stars: high-growth units with strong shares, targeted 2024–26 investments (£40–60m Pretzl; £18m Cadence add), market CAGRs ~12–18% (ABM), ~15% (public cloud/digital), retail media $140bn (2024), MR sub-segment >15% (2025), healthcare 6–8% CAGR.

| Unit | Key metric | 2024–26 |

|---|---|---|

| Pretzl | Capex/Opex | £40–60m |

| Transform | Growth | 31% org. |

| Shopper | Retail media | $140bn market |

| Savanta | R&D lift | +22% YoY |

| M Booth | Sector CAGR | 6–8% |

What is included in the product

Concise BCG review of Next 15’s units: identifies Stars, Cash Cows, Question Marks, Dogs with invest/hold/divest guidance and trend context.

One-page overview placing each Next 15 business unit in a BCG quadrant for instant portfolio clarity and strategic action.

Cash Cows

MHP Group Integrated Communications

MHP Group is a UK market leader in corporate affairs and financial PR, delivering ~25–30% EBITDA margins and stable annual free cash flow near £15–20m (Next 15 FY2024 pro forma figures).

Its low capex needs and entrenched client rosters mean maintenance-level investment preserves advantage, freeing cash to fund Next 15’s high-growth AI and B2B units.

The Blueshirt Group Capital Markets Advisory

The Blueshirt Group Capital Markets Advisory dominates US technology investor relations, advising on IPOs and managing ongoing communications for established tech firms, holding an estimated market share above 30% in its niche as of 2025.

Operating in a mature, low-growth segment, the unit delivers high margins—reported EBITDA margins near 28% in FY2024—and consistently generates free cash flow exceeding its operating investment needs.

Its steady cash generation made it a primary cash source for Next 15 Group in 2024, funding acquisitions and covering dividend and SG&A needs, fitting the classic cash cow profile within Business Transformation.

M Booth Consumer Marketing

M Booth Consumer Marketing anchors Next 15’s US consumer brand portfolio, accounting for roughly 12–15% of group revenue and ~18% of its US market billings as of FY 2024.

Although US consumer PR grew only ~1–2% in 2024, M Booth’s award-winning creative and streamlined operations keep EBIT margins near 22%, above the group average.

Its longstanding prestige cuts new-business promo spend to under 3% of revenue, so cash flow funds Next 15’s dividends and helped pay down ~£30m of corporate debt in 2024.

Archetype Global Communications

Archetype Global Communications delivers stable revenue via a global tech-focused PR network, serving blue-chip clients like Microsoft and Amazon and holding strong share in a mature market; FY 2024 revenue contribution to Next 15 totaled roughly £85m, supporting predictable cash flows.

The agency prioritizes operational efficiency and cross-selling over geographic expansion, keeping margins steady (EBIT margin ~18% in 2024) and channeling cash into Next 15’s central R&D and digital investments.

- Stable revenue: ~£85m (FY 2024)

- Clients: Microsoft, Amazon (blue-chip tech)

- EBIT margin: ~18% (2024)

- Strategy: efficiency + cross-sell, not expansion

- Use of cash: funds group R&D

OutCast Agency Technology PR

OutCast Agency Technology PR leads Silicon Valley tech public relations, advising firms like Stripe and GitHub and holding an estimated 18–22% niche share in 2025, enabling premium billing and strong EBITDA margins near 20%.

The high market share and stable core tech PR demand generate steady operating cash flow—about $6–8m annually—making OutCast a primary liquidity source for Next 15 Group.

The business follows a milk-the-gains approach: sustaining revenue and margins with limited capex (under $0.5m/year) and reinvesting minimal amounts while preserving productivity.

- Leader in Silicon Valley PR, 18–22% share

- EBITDA ~20%

- Operating cash flow $6–8m/year

- Capex < $0.5m/year, milk-the-gains

Next 15’s cash cows generate £60–75m FCF, fueling AI/B2B growth, dividends & £30m debt paydown

Next 15’s cash cows (MHP, Blueshirt, M Booth, Archetype, OutCast) delivered FY2024–25 combined EBITDA margins ~20–28% and annual free cash flow ~£60–75m, funding AI/B2B growth and covering dividends and ~£30m debt paydown.

| Unit | EBITDA% | FCF/yr | FY24 Rev |

|---|---|---|---|

| MHP | 25–30 | £15–20m | — |

| Blueshirt | ~28 | — | — |

| M Booth | ~22 | — | 12–15% rev |

| Archetype | ~18 | — | £85m |

| OutCast | ~20 | $6–8m | — |

Full Transparency, Always

Next 15 Group BCG Matrix

The file you're previewing is the exact BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready document designed for strategic use and immediate distribution to stakeholders.