Next 15 Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and rapid tech change are reshaping Next 15 Group’s strategy and market position—our concise PESTLE snapshot highlights key external risks and opportunities to inform smarter decisions. Purchase the full PESTLE for the complete, fully editable analysis and actionable insights tailored for investors, consultants, and strategists.

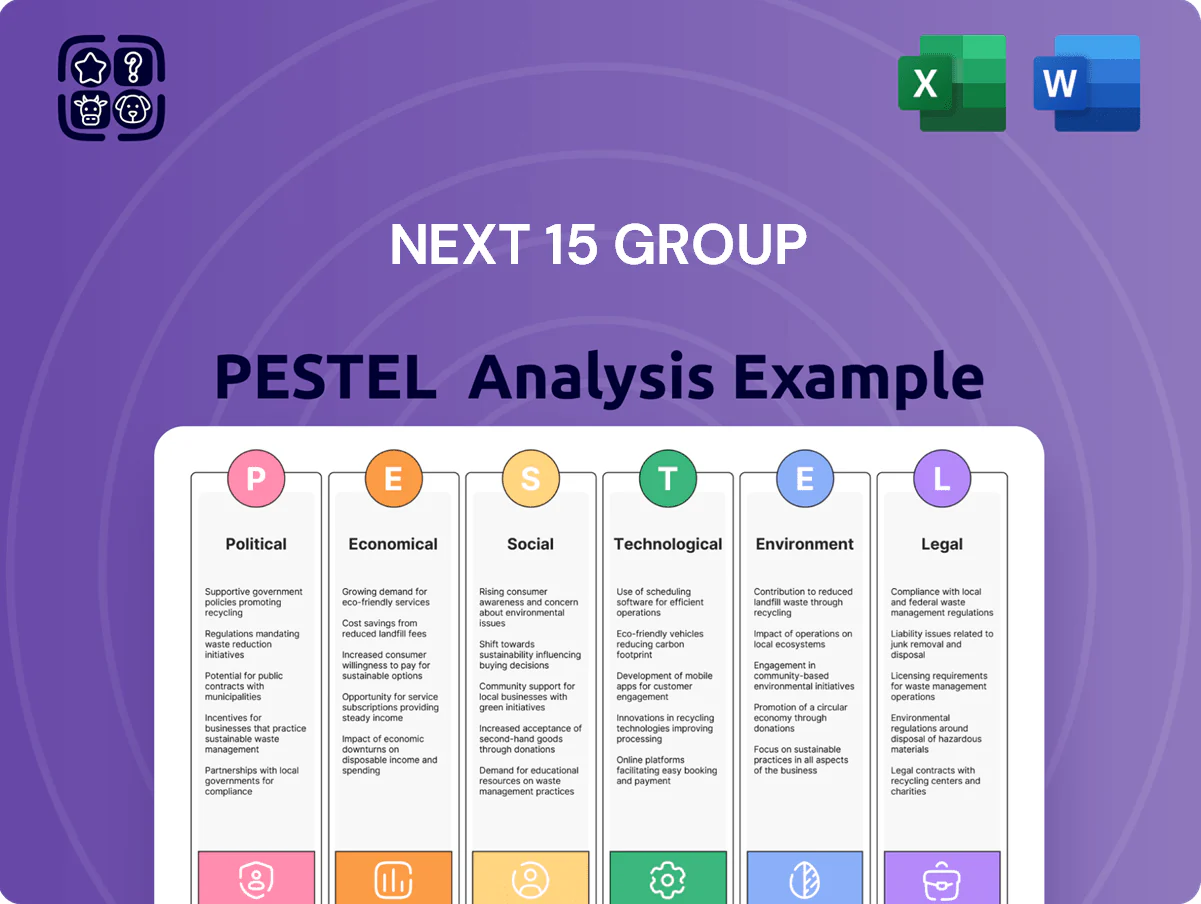

Political factors

Geopolitical instability and trade relations

Ongoing global conflicts and shifting trade alliances by late 2025 have increased cross-border operational costs for agencies like Next 15, which reported 2024 international revenue of £236.4m (55% of group). Political friction—notably US-China tensions and EU data sovereignty moves—raises the risk of market access restrictions and tighter scrutiny of international data transfers, potentially adding compliance costs equal to 1–3% of revenue.

Government digital transformation initiatives

Many governments boosted digital budgets post‑pandemic, with OECD reporting public digital transformation spending rising ~8% CAGR to an estimated $540bn in 2024; Next 15 can target this by positioning agencies as expert partners for large public projects in e‑services and govtech. Winning such contracts can create recurring, lower‑volatility revenue—public sector client work often spans multi‑year retainers worth $5m–$50m per program—offsetting private sector cyclicality.

Regulatory shifts in political advertising

Increased political polarization has driven regulators to tighten oversight of digital political ads, with the UK Electoral Commission reporting a 45% rise in compliance inquiries in 2023 and EU proposals in 2024 expanding disclosure rules to platforms and agencies.

New transparency mandates and ethical guidelines require Next 15’s PR and digital content teams to adapt workflows, track funding sources, and archive targeting data, raising compliance costs estimated industry-wide at 1–2% of revenues.

Adhering to evolving standards is critical to protect corporate reputation and avoid sanctions; penalties in recent EU rulings have reached fines up to €5m or 4% of global turnover, underscoring financial risk.

Taxation policies on multinational corporations

Changes to international corporate tax frameworks, including the OECD/G20 two-pillar solution and a 15% global minimum tax, can compress Next 15 Group’s net margins, particularly on cross-border services where profit shifting was previously available.

With 2024 revenues of about £393m and operations across the UK, US and Europe, Next 15 must model jurisdictional tax rates—UK headline 25% (2024), US federal 21% plus state levies—to forecast cash taxes and effective tax rate movements.

Strategic financial planning—transfer pricing, entity structuring and capital allocation—will be needed to preserve after-tax returns in a higher-tax baseline.

- 15% global minimum tax may raise Next 15’s effective tax rate vs historical levels

- 2024 revenue ~£393m exposes multinational tax sensitivity

- UK 25% and US ~21% federal rates increase cash tax planning importance

Governmental stance on AI ethics and sovereignty

National governments are tightening AI controls to protect cultural and economic sovereignty; 28 countries had enacted or proposed data localization laws by 2024, impacting cross-border data flows and AI deployment costs.

Mandates often specify onshore data processing and approved model lists for public communications, raising compliance costs—estimated cloud repatriation can add 5–12% to IT spend.

Next 15 must adapt its tech stack and procurement to meet local sovereignty rules to retain market access and avoid fines or contract losses.

- 28 countries with data localization measures (2024)

- Onshore processing can increase IT costs by 5–12%

- Compliance required for public-facing AI models to secure local contracts

Geopolitics and data rules squeeze margins amid £236m international revenue opportunity

Political risks—US‑China tensions, EU data sovereignty and tighter digital ad rules—raise compliance and market‑access costs; 2024 international revenue £236.4m (55%); compliance hit est. 1–3% of revenue. OECD public digital spend ~$540bn (2024) creates multi‑year gov contracts (£5–50m each). 28 countries had data localization measures (2024); cloud repatriation adds 5–12% IT spend.

| Metric | 2024 |

|---|---|

| Group revenue | £393m |

| International revenue | £236.4m (55%) |

| OECD public digital spend | $540bn |

| Data localization countries | 28 |

| Compliance cost est. | 1–3% of revenue |

| IT repatriation cost | 5–12% IT spend |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Next 15 Group, with data-backed trends, industry- and region-specific examples, forward-looking scenario insights, and practical implications to help executives, consultants, and investors identify risks, opportunities and inform strategy and funding decisions.

A concise, visually segmented PESTLE summary for Next 15 Group that’s easily dropped into presentations or shared across teams to speed decision-making and surface external risks during planning sessions.

Economic factors

Global interest rate environment

By end-2025 the Bank of England and US Fed path will shape Next 15’s WACC and acquisition appetite: with UK base rate at 5.25% and US Fed funds around 5.25% (Jan 2025), higher borrowing costs raise debt financing expenses and could compress deal volume for a group that completed ~£200m of acquisitions in 2023–24.

Corporate marketing budget volatility

Economic cycles directly dictate B2B and B2C willingness to spend on discretionary marketing and PR; global ad spend growth slowed to about 3.1% in 2023 versus 9.9% in 2021, pressuring clients to reallocate.

In slow-growth periods clients shift toward performance-driven digital channels—programmatic and search saw 11% CAGR to 2023—at the expense of long-term brand building.

Next 15’s mix of data-led performance units and agency brands lets it pivot services; digital revenue comprised roughly 68% of group sales in FY 2024, supporting resilience amid budget volatility.

Currency exchange rate fluctuations

As a UK-based group earning roughly 45% of 2024 revenue outside the UK, Next 15 faces currency volatility risk—USD/GBP moves of 5% can swing reported operating profit by millions; in H1 2025 FX translation impacted adjusted operating profit by about £3–5m. Stronger local currencies vs GBP create translation gains, weaker create losses. Active hedging and geographic revenue balancing remain key mitigants.

Labor market dynamics and wage inflation

Demand for high-tier digital talent remains acute, pushing personnel costs up across marketing services; average tech wages rose 6.5% in London and 7.2% in San Francisco in 2024, pressuring Next 15’s gross margins.

Next 15 must balance attracting creative and technical hires with margin maintenance by using selective pay premiums, freelance talent pools and productivity targets.

Ongoing wage inflation in hubs like London and SF makes automation and efficient resource allocation essential to protect operating margins and EBITDA.

- 2024 wage growth: London +6.5%, San Francisco +7.2%

- Use automation to offset personnel cost rises and protect EBITDA

- Mix of permanent, freelance and remote hires to control payroll

Emerging market growth opportunities

While Next 15's core markets offer stability, emerging digital economies—led by India (GDP growth ~7% in 2024) and Southeast Asia (digital economy >US$360bn in 2024)—present new revenue channels as middle-class digital consumption rises.

Leveraging its global network, Next 15 can scale agency, data and martech services into regions where internet users grew ~4% YoY in 2024, but success depends on localizing offers and pricing.

Strategic entry requires granular analysis of local GDP per capita, mobile penetration (e.g., India 77% smartphone adoption 2024) and consumer behavior to de-risk investments.

- High growth: India ~7% GDP (2024), SEA digital economy >US$360bn

- Digital adoption: internet users +4% YoY (2024); India smartphone adoption ~77%

- Risk management: local market research, price localization, regulatory assessment

Higher rates squeeze M&A and margins as digital growth and FX reshape Next 15

Higher rates (BoE, Fed ~5.25% Jan 2025) raise WACC, squeezing M&A after ~£200m deals in 2023–24; ad spend growth slowed to 3.1% in 2023, pushing clients to performance channels (programmatic/search ~11% CAGR to 2023). Digital was ~68% of Next 15 sales in FY2024; 45% revenue outside UK; H1 2025 FX swung adjusted op profit ~£3–5m. Talent cost inflation (London +6.5%, SF +7.2% 2024) pressures margins.

| Metric | Value |

|---|---|

| Rate (BoE/Fed) | ~5.25% |

| Ad spend growth 2023 | 3.1% |

| Digital revenue FY24 | ~68% |

| Foreign rev | ~45% |

| FX impact H1 2025 | £3–5m |

| Wage growth 2024 | London +6.5%, SF +7.2% |

Full Version Awaits

Next 15 Group PESTLE Analysis

The preview shown here is the exact Next 15 Group PESTLE analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

No placeholders, no teasers—this is the real, professionally structured file you’ll own upon checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and rapid tech change are reshaping Next 15 Group’s strategy and market position—our concise PESTLE snapshot highlights key external risks and opportunities to inform smarter decisions. Purchase the full PESTLE for the complete, fully editable analysis and actionable insights tailored for investors, consultants, and strategists.

Political factors

Geopolitical instability and trade relations

Ongoing global conflicts and shifting trade alliances by late 2025 have increased cross-border operational costs for agencies like Next 15, which reported 2024 international revenue of £236.4m (55% of group). Political friction—notably US-China tensions and EU data sovereignty moves—raises the risk of market access restrictions and tighter scrutiny of international data transfers, potentially adding compliance costs equal to 1–3% of revenue.

Government digital transformation initiatives

Many governments boosted digital budgets post‑pandemic, with OECD reporting public digital transformation spending rising ~8% CAGR to an estimated $540bn in 2024; Next 15 can target this by positioning agencies as expert partners for large public projects in e‑services and govtech. Winning such contracts can create recurring, lower‑volatility revenue—public sector client work often spans multi‑year retainers worth $5m–$50m per program—offsetting private sector cyclicality.

Regulatory shifts in political advertising

Increased political polarization has driven regulators to tighten oversight of digital political ads, with the UK Electoral Commission reporting a 45% rise in compliance inquiries in 2023 and EU proposals in 2024 expanding disclosure rules to platforms and agencies.

New transparency mandates and ethical guidelines require Next 15’s PR and digital content teams to adapt workflows, track funding sources, and archive targeting data, raising compliance costs estimated industry-wide at 1–2% of revenues.

Adhering to evolving standards is critical to protect corporate reputation and avoid sanctions; penalties in recent EU rulings have reached fines up to €5m or 4% of global turnover, underscoring financial risk.

Taxation policies on multinational corporations

Changes to international corporate tax frameworks, including the OECD/G20 two-pillar solution and a 15% global minimum tax, can compress Next 15 Group’s net margins, particularly on cross-border services where profit shifting was previously available.

With 2024 revenues of about £393m and operations across the UK, US and Europe, Next 15 must model jurisdictional tax rates—UK headline 25% (2024), US federal 21% plus state levies—to forecast cash taxes and effective tax rate movements.

Strategic financial planning—transfer pricing, entity structuring and capital allocation—will be needed to preserve after-tax returns in a higher-tax baseline.

- 15% global minimum tax may raise Next 15’s effective tax rate vs historical levels

- 2024 revenue ~£393m exposes multinational tax sensitivity

- UK 25% and US ~21% federal rates increase cash tax planning importance

Governmental stance on AI ethics and sovereignty

National governments are tightening AI controls to protect cultural and economic sovereignty; 28 countries had enacted or proposed data localization laws by 2024, impacting cross-border data flows and AI deployment costs.

Mandates often specify onshore data processing and approved model lists for public communications, raising compliance costs—estimated cloud repatriation can add 5–12% to IT spend.

Next 15 must adapt its tech stack and procurement to meet local sovereignty rules to retain market access and avoid fines or contract losses.

- 28 countries with data localization measures (2024)

- Onshore processing can increase IT costs by 5–12%

- Compliance required for public-facing AI models to secure local contracts

Geopolitics and data rules squeeze margins amid £236m international revenue opportunity

Political risks—US‑China tensions, EU data sovereignty and tighter digital ad rules—raise compliance and market‑access costs; 2024 international revenue £236.4m (55%); compliance hit est. 1–3% of revenue. OECD public digital spend ~$540bn (2024) creates multi‑year gov contracts (£5–50m each). 28 countries had data localization measures (2024); cloud repatriation adds 5–12% IT spend.

| Metric | 2024 |

|---|---|

| Group revenue | £393m |

| International revenue | £236.4m (55%) |

| OECD public digital spend | $540bn |

| Data localization countries | 28 |

| Compliance cost est. | 1–3% of revenue |

| IT repatriation cost | 5–12% IT spend |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Next 15 Group, with data-backed trends, industry- and region-specific examples, forward-looking scenario insights, and practical implications to help executives, consultants, and investors identify risks, opportunities and inform strategy and funding decisions.

A concise, visually segmented PESTLE summary for Next 15 Group that’s easily dropped into presentations or shared across teams to speed decision-making and surface external risks during planning sessions.

Economic factors

Global interest rate environment

By end-2025 the Bank of England and US Fed path will shape Next 15’s WACC and acquisition appetite: with UK base rate at 5.25% and US Fed funds around 5.25% (Jan 2025), higher borrowing costs raise debt financing expenses and could compress deal volume for a group that completed ~£200m of acquisitions in 2023–24.

Corporate marketing budget volatility

Economic cycles directly dictate B2B and B2C willingness to spend on discretionary marketing and PR; global ad spend growth slowed to about 3.1% in 2023 versus 9.9% in 2021, pressuring clients to reallocate.

In slow-growth periods clients shift toward performance-driven digital channels—programmatic and search saw 11% CAGR to 2023—at the expense of long-term brand building.

Next 15’s mix of data-led performance units and agency brands lets it pivot services; digital revenue comprised roughly 68% of group sales in FY 2024, supporting resilience amid budget volatility.

Currency exchange rate fluctuations

As a UK-based group earning roughly 45% of 2024 revenue outside the UK, Next 15 faces currency volatility risk—USD/GBP moves of 5% can swing reported operating profit by millions; in H1 2025 FX translation impacted adjusted operating profit by about £3–5m. Stronger local currencies vs GBP create translation gains, weaker create losses. Active hedging and geographic revenue balancing remain key mitigants.

Labor market dynamics and wage inflation

Demand for high-tier digital talent remains acute, pushing personnel costs up across marketing services; average tech wages rose 6.5% in London and 7.2% in San Francisco in 2024, pressuring Next 15’s gross margins.

Next 15 must balance attracting creative and technical hires with margin maintenance by using selective pay premiums, freelance talent pools and productivity targets.

Ongoing wage inflation in hubs like London and SF makes automation and efficient resource allocation essential to protect operating margins and EBITDA.

- 2024 wage growth: London +6.5%, San Francisco +7.2%

- Use automation to offset personnel cost rises and protect EBITDA

- Mix of permanent, freelance and remote hires to control payroll

Emerging market growth opportunities

While Next 15's core markets offer stability, emerging digital economies—led by India (GDP growth ~7% in 2024) and Southeast Asia (digital economy >US$360bn in 2024)—present new revenue channels as middle-class digital consumption rises.

Leveraging its global network, Next 15 can scale agency, data and martech services into regions where internet users grew ~4% YoY in 2024, but success depends on localizing offers and pricing.

Strategic entry requires granular analysis of local GDP per capita, mobile penetration (e.g., India 77% smartphone adoption 2024) and consumer behavior to de-risk investments.

- High growth: India ~7% GDP (2024), SEA digital economy >US$360bn

- Digital adoption: internet users +4% YoY (2024); India smartphone adoption ~77%

- Risk management: local market research, price localization, regulatory assessment

Higher rates squeeze M&A and margins as digital growth and FX reshape Next 15

Higher rates (BoE, Fed ~5.25% Jan 2025) raise WACC, squeezing M&A after ~£200m deals in 2023–24; ad spend growth slowed to 3.1% in 2023, pushing clients to performance channels (programmatic/search ~11% CAGR to 2023). Digital was ~68% of Next 15 sales in FY2024; 45% revenue outside UK; H1 2025 FX swung adjusted op profit ~£3–5m. Talent cost inflation (London +6.5%, SF +7.2% 2024) pressures margins.

| Metric | Value |

|---|---|

| Rate (BoE/Fed) | ~5.25% |

| Ad spend growth 2023 | 3.1% |

| Digital revenue FY24 | ~68% |

| Foreign rev | ~45% |

| FX impact H1 2025 | £3–5m |

| Wage growth 2024 | London +6.5%, SF +7.2% |

Full Version Awaits

Next 15 Group PESTLE Analysis

The preview shown here is the exact Next 15 Group PESTLE analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

No placeholders, no teasers—this is the real, professionally structured file you’ll own upon checkout.