NextEra Energy Boston Consulting Group Matrix

Actionable Strategy Starts Here

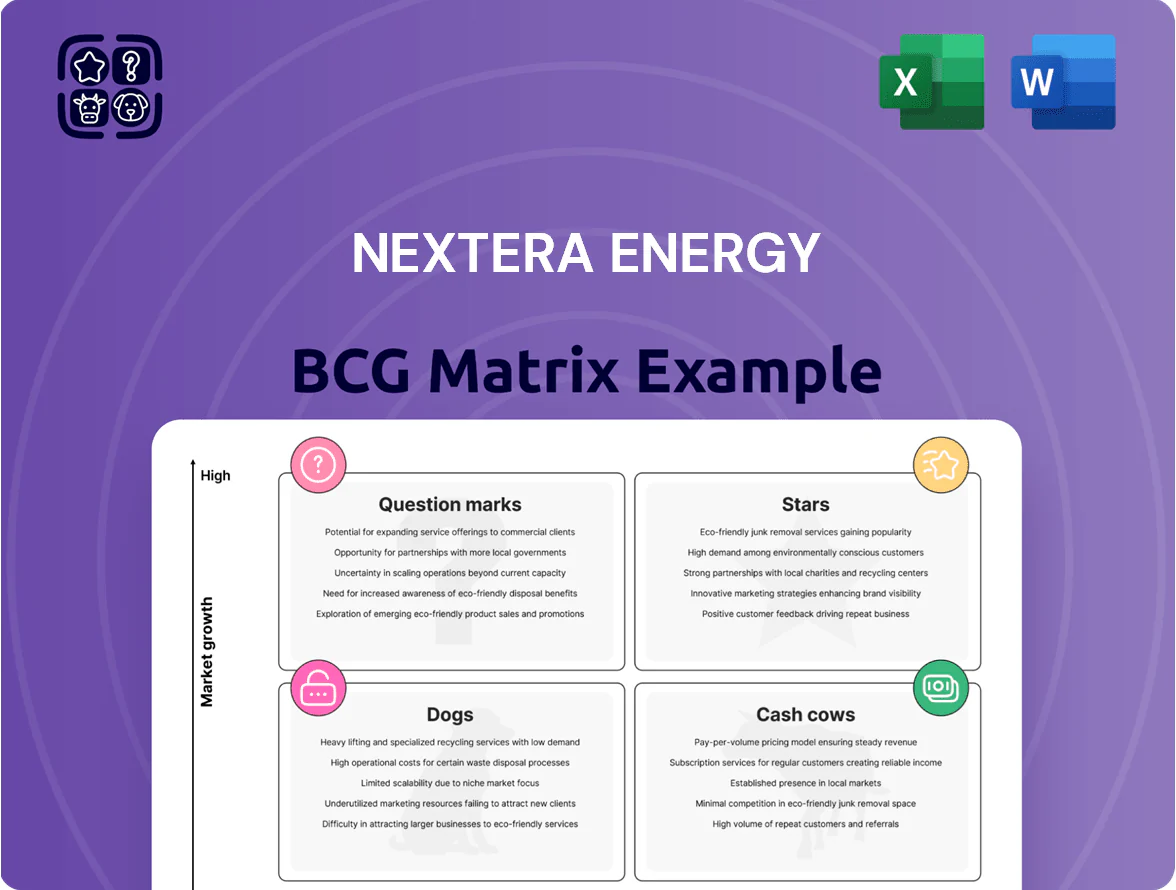

NextEra Energy sits at the intersection of rapid renewable growth and regulated utility stability—our preview maps its core businesses across Stars (growth-stage renewables), Cash Cows (regulated transmission), Question Marks (emerging storage/green hydrogen bets), and Dogs (underperforming legacy assets). Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Utility-Scale Solar Energy

NextEra Energy Resources holds the largest U.S. utility-scale solar market share, with ~15 GW operating and ~20 GW in development as of Q3 2025, benefiting from Inflation Reduction Act tax credits and rising corporate offtake; revenue for the segment grew ~18% YoY in 2024 to about $5.6B.

Battery Storage Systems

Battery Storage Systems: Energy storage is a high-growth area to smooth renewables; US deployments grew ~160% in 2023–2024, reaching ~8.5 GW of new capacity in 2024 (SEIA/BNEF). NextEra Energy has scaled to ~4 GW of owned/contracted storage by end-2025, pairing batteries with solar/wind to secure market leadership. High upfront capital—projects often $200–350/kWh installed—drives heavy investment but yields strategic value via capacity markets and firming revenue. Rapid adoption of long-duration and lithium-ion tech keeps NextEra central to the energy transition.

Competitive Transmission Infrastructure

NextEra Energy Transmission is capturing urgent North American grid upgrades, winning competitive bids for large regional projects and growing revenues—transmission capex pipelines exceeded $9.5bn in 2024 and backlog rose ~28% year-over-year.

Projects are capital-intensive and regulatory-complex, yet operate largely outside Florida’s regulated utility, expanding non-regulated footprint and boosting strategic returns.

High entry barriers and massive scale needs position this unit as a BCG Matrix star, driving rapid growth and market share gains.

Wind Energy Repowering

NextEra Energy leads wind repowering by replacing older turbines with higher-capacity models, boosting output ~20–40% per site and extending life by 15–20 years; repowering helped secure $1.2B in tax-credit benefits in 2024 and supports maintaining ~25% U.S. market share.

High demand from utilities racing to meet 2025 RPS keeps capacity additions strong—U.S. wind additions hit 14 GW in 2024—requiring ongoing capital but reinforcing NextEra’s position as the world renewables leader.

- Repowering raises output 20–40%

- Extends life 15–20 years

- $1.2B tax-credit benefit (2024)

- ~25% U.S. market share

- U.S. wind additions 14 GW (2024)

Data Center Power Solutions

NextEra Energy is a Star in data center power: AI-driven demand for hyperscale compute lifted corporate renewables demand ~30% year-over-year in 2024, and NextEra signed multi-year power purchase agreements (PPAs) delivering combined 4.2 GW capacity to big tech through 2025.

The niche outpaces the broader US utility growth (~2–3% annually), needs rapid build-out of specialized transmission and battery storage, and fits NextEra’s scale—$58 billion development pipeline in 2024 enables high-stakes, high-reward deals.

- 2024 AI-driven renewables demand +30%

- 4.2 GW committed to big tech via PPAs by 2025

- NextEra development pipeline $58B (2024)

- Sector growth >> utility market (2–3% pa)

NextEra’s Renewables Surge: 15GW Solar, 4GW Storage & $58B Development Pipeline

NextEra’s renewables + storage are Stars: ~15 GW solar operating, ~20 GW development (Q3 2025); ~4 GW storage owned/contracted (end-2025); transmission capex pipeline $9.5B (2024); development pipeline $58B (2024); segment revenue ~$5.6B (2024) driving rapid share and growth.

| Metric | Value |

|---|---|

| Solar op./dev | 15 GW / 20 GW |

| Storage | ~4 GW |

| Dev pipeline | $58B (2024) |

| Trans. capex | $9.5B (2024) |

| Segment rev | $5.6B (2024) |

What is included in the product

BCG Matrix breakdown of NextEra Energy’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing NextEra Energy's segments into BCG quadrants for quick portfolio clarity and strategic prioritization

Cash Cows

FPL Regulated Utility Operations

Florida Power & Light (FPL) is NextEra Energy’s liquidity engine, delivering regulated utility cash flow—FPL reported $6.5 billion operating cash flow in 2024—via monopoly rates in a growing Florida market with ~22 million residents (2024 Census estimate), giving stable, predictable receipts versus retail-scale renewables.

FPL’s favorable regulatory returns (allowed ROE ~10–11% in recent Florida dockets) and low relative promotional spend free capital that NextEra deploys to Stars and Question Marks, financing ~\$6–8 billion annual clean-energy investment through 2024.

Nuclear Power Generation

NextEra’s nuclear fleet delivers reliable, carbon-free baseload power with industry-leading margins; in 2024 nuclear generated ~25% of NextEra’s power, with capacity factors ~92% and operating margins above 35%.

After sunk construction costs, marginal operating costs are low, so nuclear produces steady cash flow; in FY 2024 the segment contributed roughly $1.4 billion in free cash flow supporting dividends and debt service.

The nuclear market is mature with limited growth potential but remains vital for grid stability and firming renewables, keeping these assets as BCG Cash Cows for NextEra.

Natural Gas Pipelines

NextEra’s midstream assets, notably Sabal Trail and Florida Southeast Connection, deliver steady fee-based cash flows via long-term contracts—these pipelines contributed roughly $250–300 million EBITDA in 2024, shielding revenues from natural gas price swings.

New pipeline builds have slowed amid stricter permitting and environmental reviews since 2020, but existing lines show high utilization (>90% in 2024) and low maintenance capex, making the segment a classic cash cow.

Regulated Transmission and Distribution

Regulated transmission and distribution in Florida is a mature, cash-generating core for NextEra Energy, holding dominant market share and a protected monopoly position in its service territories.

Grid hardening and smart-meter investments raised the regulated rate base to about $35 billion by YE 2024, boosting efficiency and stabilizing returns while supporting an investment-grade credit rating (S&P A‑ as of 2025).

Because the market is geographically defined and state‑regulated, growth is steady—roughly mid-single-digit rate base CAGR—allowing NextEra to fund R&D and innovation without risking credit strength.

- Dominant Florida monopoly

- Rate base ≈ $35B (YE 2024)

- S&P A‑ rating (2025)

- Mid-single-digit steady growth

- Funds R&D from stable cash flows

Commercial Natural Gas Generation

NextEra Energy's modern natural gas fleet in Florida provides essential backup and peaking power, with combined-cycle plants averaging thermal efficiencies >60% and representing roughly 25% of Florida's installed capacity as of 2025.

These high‑share, mature assets focus on maximizing dispatch efficiency and extending remaining life to generate steady cash flow; in 2024 gas generation contributed about $2.1 billion in operating cash to NextEra Energy Resources.

The cash supports renewables buildout— NextEra invested $6.5 billion in clean energy projects in 2024—so gas acts as the companys cash cow funding the transition.

- High efficiency: >60% thermal for combined-cycle units

- Market share: ~25% of Florida capacity (2025)

- 2024 cash from gas gen: ~$2.1B

- 2024 clean energy capex: $6.5B

NextEra’s Cash Cows: FPL, Nuclear, Pipelines, T&D & Gas Driving ~$10B+ OCF/FCF

FPL, nuclear, pipelines, T&D, and gas are NextEra’s cash cows: FPL OCF $6.5B (2024); nuclear FCF ~$1.4B (2024); pipelines EBITDA $250–300M (2024); T&D rate base ~$35B (YE2024); gas OCF ~$2.1B (2024).

| Asset | 2024/YE2024 |

|---|---|

| FPL OCF | $6.5B |

| Nuclear FCF | $1.4B |

| Pipelines EBITDA | $250–300M |

| T&D rate base | $35B |

| Gas OCF | $2.1B |

Preview = Final Product

NextEra Energy BCG Matrix

The file you're previewing on this page is the exact NextEra Energy BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just a fully formatted, analysis-ready document designed for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

NextEra Energy sits at the intersection of rapid renewable growth and regulated utility stability—our preview maps its core businesses across Stars (growth-stage renewables), Cash Cows (regulated transmission), Question Marks (emerging storage/green hydrogen bets), and Dogs (underperforming legacy assets). Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Utility-Scale Solar Energy

NextEra Energy Resources holds the largest U.S. utility-scale solar market share, with ~15 GW operating and ~20 GW in development as of Q3 2025, benefiting from Inflation Reduction Act tax credits and rising corporate offtake; revenue for the segment grew ~18% YoY in 2024 to about $5.6B.

Battery Storage Systems

Battery Storage Systems: Energy storage is a high-growth area to smooth renewables; US deployments grew ~160% in 2023–2024, reaching ~8.5 GW of new capacity in 2024 (SEIA/BNEF). NextEra Energy has scaled to ~4 GW of owned/contracted storage by end-2025, pairing batteries with solar/wind to secure market leadership. High upfront capital—projects often $200–350/kWh installed—drives heavy investment but yields strategic value via capacity markets and firming revenue. Rapid adoption of long-duration and lithium-ion tech keeps NextEra central to the energy transition.

Competitive Transmission Infrastructure

NextEra Energy Transmission is capturing urgent North American grid upgrades, winning competitive bids for large regional projects and growing revenues—transmission capex pipelines exceeded $9.5bn in 2024 and backlog rose ~28% year-over-year.

Projects are capital-intensive and regulatory-complex, yet operate largely outside Florida’s regulated utility, expanding non-regulated footprint and boosting strategic returns.

High entry barriers and massive scale needs position this unit as a BCG Matrix star, driving rapid growth and market share gains.

Wind Energy Repowering

NextEra Energy leads wind repowering by replacing older turbines with higher-capacity models, boosting output ~20–40% per site and extending life by 15–20 years; repowering helped secure $1.2B in tax-credit benefits in 2024 and supports maintaining ~25% U.S. market share.

High demand from utilities racing to meet 2025 RPS keeps capacity additions strong—U.S. wind additions hit 14 GW in 2024—requiring ongoing capital but reinforcing NextEra’s position as the world renewables leader.

- Repowering raises output 20–40%

- Extends life 15–20 years

- $1.2B tax-credit benefit (2024)

- ~25% U.S. market share

- U.S. wind additions 14 GW (2024)

Data Center Power Solutions

NextEra Energy is a Star in data center power: AI-driven demand for hyperscale compute lifted corporate renewables demand ~30% year-over-year in 2024, and NextEra signed multi-year power purchase agreements (PPAs) delivering combined 4.2 GW capacity to big tech through 2025.

The niche outpaces the broader US utility growth (~2–3% annually), needs rapid build-out of specialized transmission and battery storage, and fits NextEra’s scale—$58 billion development pipeline in 2024 enables high-stakes, high-reward deals.

- 2024 AI-driven renewables demand +30%

- 4.2 GW committed to big tech via PPAs by 2025

- NextEra development pipeline $58B (2024)

- Sector growth >> utility market (2–3% pa)

NextEra’s Renewables Surge: 15GW Solar, 4GW Storage & $58B Development Pipeline

NextEra’s renewables + storage are Stars: ~15 GW solar operating, ~20 GW development (Q3 2025); ~4 GW storage owned/contracted (end-2025); transmission capex pipeline $9.5B (2024); development pipeline $58B (2024); segment revenue ~$5.6B (2024) driving rapid share and growth.

| Metric | Value |

|---|---|

| Solar op./dev | 15 GW / 20 GW |

| Storage | ~4 GW |

| Dev pipeline | $58B (2024) |

| Trans. capex | $9.5B (2024) |

| Segment rev | $5.6B (2024) |

What is included in the product

BCG Matrix breakdown of NextEra Energy’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing NextEra Energy's segments into BCG quadrants for quick portfolio clarity and strategic prioritization

Cash Cows

FPL Regulated Utility Operations

Florida Power & Light (FPL) is NextEra Energy’s liquidity engine, delivering regulated utility cash flow—FPL reported $6.5 billion operating cash flow in 2024—via monopoly rates in a growing Florida market with ~22 million residents (2024 Census estimate), giving stable, predictable receipts versus retail-scale renewables.

FPL’s favorable regulatory returns (allowed ROE ~10–11% in recent Florida dockets) and low relative promotional spend free capital that NextEra deploys to Stars and Question Marks, financing ~\$6–8 billion annual clean-energy investment through 2024.

Nuclear Power Generation

NextEra’s nuclear fleet delivers reliable, carbon-free baseload power with industry-leading margins; in 2024 nuclear generated ~25% of NextEra’s power, with capacity factors ~92% and operating margins above 35%.

After sunk construction costs, marginal operating costs are low, so nuclear produces steady cash flow; in FY 2024 the segment contributed roughly $1.4 billion in free cash flow supporting dividends and debt service.

The nuclear market is mature with limited growth potential but remains vital for grid stability and firming renewables, keeping these assets as BCG Cash Cows for NextEra.

Natural Gas Pipelines

NextEra’s midstream assets, notably Sabal Trail and Florida Southeast Connection, deliver steady fee-based cash flows via long-term contracts—these pipelines contributed roughly $250–300 million EBITDA in 2024, shielding revenues from natural gas price swings.

New pipeline builds have slowed amid stricter permitting and environmental reviews since 2020, but existing lines show high utilization (>90% in 2024) and low maintenance capex, making the segment a classic cash cow.

Regulated Transmission and Distribution

Regulated transmission and distribution in Florida is a mature, cash-generating core for NextEra Energy, holding dominant market share and a protected monopoly position in its service territories.

Grid hardening and smart-meter investments raised the regulated rate base to about $35 billion by YE 2024, boosting efficiency and stabilizing returns while supporting an investment-grade credit rating (S&P A‑ as of 2025).

Because the market is geographically defined and state‑regulated, growth is steady—roughly mid-single-digit rate base CAGR—allowing NextEra to fund R&D and innovation without risking credit strength.

- Dominant Florida monopoly

- Rate base ≈ $35B (YE 2024)

- S&P A‑ rating (2025)

- Mid-single-digit steady growth

- Funds R&D from stable cash flows

Commercial Natural Gas Generation

NextEra Energy's modern natural gas fleet in Florida provides essential backup and peaking power, with combined-cycle plants averaging thermal efficiencies >60% and representing roughly 25% of Florida's installed capacity as of 2025.

These high‑share, mature assets focus on maximizing dispatch efficiency and extending remaining life to generate steady cash flow; in 2024 gas generation contributed about $2.1 billion in operating cash to NextEra Energy Resources.

The cash supports renewables buildout— NextEra invested $6.5 billion in clean energy projects in 2024—so gas acts as the companys cash cow funding the transition.

- High efficiency: >60% thermal for combined-cycle units

- Market share: ~25% of Florida capacity (2025)

- 2024 cash from gas gen: ~$2.1B

- 2024 clean energy capex: $6.5B

NextEra’s Cash Cows: FPL, Nuclear, Pipelines, T&D & Gas Driving ~$10B+ OCF/FCF

FPL, nuclear, pipelines, T&D, and gas are NextEra’s cash cows: FPL OCF $6.5B (2024); nuclear FCF ~$1.4B (2024); pipelines EBITDA $250–300M (2024); T&D rate base ~$35B (YE2024); gas OCF ~$2.1B (2024).

| Asset | 2024/YE2024 |

|---|---|

| FPL OCF | $6.5B |

| Nuclear FCF | $1.4B |

| Pipelines EBITDA | $250–300M |

| T&D rate base | $35B |

| Gas OCF | $2.1B |

Preview = Final Product

NextEra Energy BCG Matrix

The file you're previewing on this page is the exact NextEra Energy BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just a fully formatted, analysis-ready document designed for strategic clarity and professional use.