NFI Industries Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

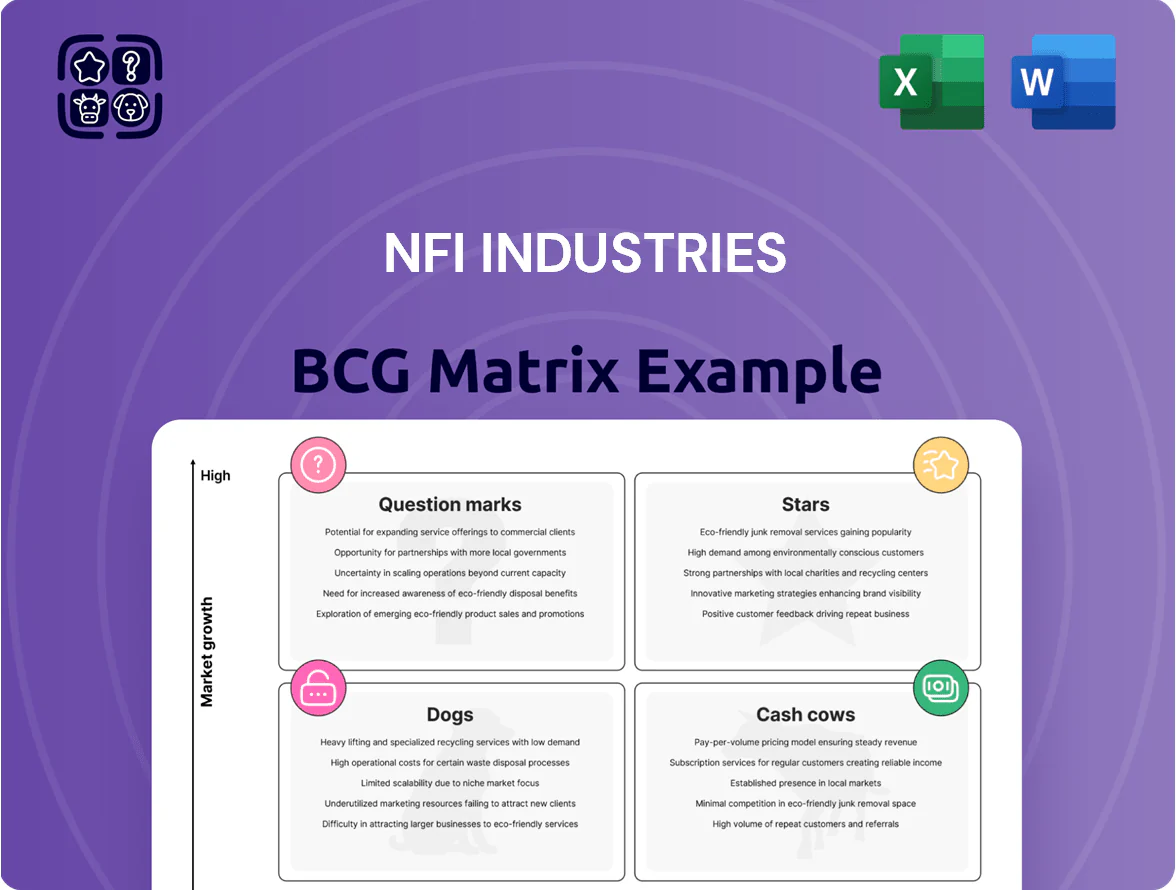

NFI Industries’ BCG Matrix preview highlights emerging growth areas in intermodal and logistics tech as potential Stars, while legacy trucking services appear as Cash Cows fueling steady cash flow; a few underperforming lines may be Dogs, and select pilot programs sit in Question Marks awaiting scale. This snapshot helps prioritize investments but the full BCG Matrix delivers quadrant-by-quadrant data, actionable recommendations, and editable Word and Excel files to turn insight into strategy—purchase now for the complete, presentation-ready analysis.

Stars

Electric Vehicle Fleet Transition

NFI Industries, as of late 2025, leads heavy-duty electric vehicle (EV) deployment in California drayage, operating over 200 battery-electric trucks and capturing roughly 18% of the regional zero-emission drayage market.

This segment shows >20% annual demand growth as shippers chase carbon-neutral logistics to meet corporate ESG targets and California’s Drayage Rule timelines.

Early market share lets NFI secure premium sustainability contracts, offsetting high upfront charging capex—about $35k–$60k per truck in infrastructure—and improving long-term contract margins.

High-Velocity E-commerce Fulfillment

High-Velocity E-commerce Fulfillment is a Star for NFI Industries: DTC demand lifted e-commerce center revenue by ~28% in 2024, making it a high-growth engine after NFI captured an estimated 6–8% share of US outsourced e-com fulfillment volume.

NFI’s edge comes from integrated sorting tech and sub-12-hour processing for peak clients; capital spending on robotics and WMS rose to $95M in 2024 to sustain throughput and accuracy.

Biopharmaceutical Cold Chain Solutions

NFI Industries’ Biopharmaceutical Cold Chain is a Star: revenue from temperature-controlled pharma logistics rose ~28% CAGR 2019–2024, with global biologics demand up 9% in 2024; NFI’s specialized fleet and GMP-compliant sites give it a strong niche share and high growth runway.

Automated Distribution Centers

NFI Industries’ automated distribution centers, fitted with autonomous mobile robots (AMRs) and automated storage/retrieval systems (AS/RS), have become market leaders, serving customers who need to cut labor costs and raise throughput by ~25–40% per published pilot studies in 2024.

These premium facilities captured incremental market share in the industrial automation segment—NFI reported 2024 revenue growth in logistics services of 18% year-over-year—making them Stars in the BCG Matrix.

Ongoing capex is required to keep pace with AI-driven controls and sensor upgrades; industry capex guidance suggests 5–8% of revenue for continuous modernization, but current assets are the gold standard for resilient, high-throughput supply chains.

- Throughput +25–40% from AMR/ASRS (2024 pilots)

- NFI logistics revenue +18% YoY (2024)

- Recommended capex 5–8% of revenue for modernization

Strategic Port Hub Expansion

NFI expanded in Savannah and Houston, capturing rising North American port volumes—US container throughput grew 7.2% in 2024 to ~31.7 million TEUs, with Savannah up ~8% year-over-year, boosting NFI’s drayage and transload volumes and supporting higher revenue per load.

Integrated hubs combine drayage, transloading, and warehousing, creating a high-market-share ecosystem that shortens dwell times and raises margin per shipment; controlling the first mile makes NFI a preferred partner for global shippers.

Nearshoring lifted US inbound trade from Mexico and Latin America; ports serving those corridors saw double-digit growth in 2023–2024, keeping port-centric assets in the Stars (high-growth, high-share) quadrant for NFI.

- Savannah/Houston focus

- 31.7M TEUs US 2024

- +8% Savannah 2024

- Integrated drayage/transload/warehousing

- First-mile control = strategic moat

NFI: EV Drayage, E‑com, Biopharma & Automation Fueling Rapid Growth

NFI’s Stars: EV drayage (200+ BEVs; ~18% CA zero-emission drayage), e‑commerce fulfillment (6–8% US share; +28% 2024 rev), biopharma cold chain (≈28% CAGR 2019–2024), and automated DCs (+25–40% throughput; logistics rev +18% YoY 2024). Ongoing capex 5–8% revenue to sustain leadership.

| Segment | Key metric | 2024/2025 |

|---|---|---|

| EV drayage | Fleet/share | 200+ BEVs / 18% |

| E‑com | Rev growth / share | +28% / 6–8% |

| Biopharma | CAGR | ~28% |

| Automated DCs | Throughput | +25–40% |

What is included in the product

BCG Matrix review of NFI Industries: quadrant-by-quadrant strategic insights, investment recommendations, and trend-based risk/advantage highlights.

One-page overview placing each NFI Industries business unit in a BCG quadrant for fast strategic clarity.

Cash Cows

Dedicated Contract Carriage

Dedicated Contract Carriage drives NFI Industries' revenue, delivering stable cash flow via long-term contracts that accounted for roughly 55% of 2024 consolidated revenue (~$4.0B total revenue in 2024 per company filings), thanks to a 6,000+ vehicle fleet and long-standing service to blue-chip retailers and manufacturers.

As a mature segment, it needs lower incremental capex—fleet and terminals already in place—so margins are steadier and free cash helps fund NFI’s 2024–25 investments in electrification and automation (company guidance: $200–300M capex for green fleet and tech through 2025).

Core Dry Van Warehousing

NFI Industries’ Core Dry Van Warehousing holds high market share in a mature, low-growth segment: the U.S. warehousing vacancy averaged 5.4% in 2024 and national storage growth ~2% annually. These traditional dry storage facilities run with low overhead and >90% utilization, generating steady EBITDA margins near 18% and reliable free cash flow for the firm.

Established Port Drayage Operations

Established Port Drayage Operations at West Coast ports generate predictable free cash flow for NFI Industries, handling an estimated 1.2–1.5 million TEUs annually and securing ~20–25% share at key terminals as of 2024.

Operating margins near 8–10% due to scale, route-density gains, and asset utilization improvements, this mature unit yields steady cash despite low volume growth.

Intermodal Logistics Services

NFI Industries’ intermodal logistics mixes rail and truck to cut costs and emissions; as of 2024 intermodal fuel/CO2 per ton-mile fell ~20% vs truck-only, aiding cost-conscious shippers who choose long-haul efficiency over speed.

Market share is high in targeted lanes; U.S. intermodal volumes stabilized in 2023–2024 with ~1–2% annual growth, and NFI’s durable Class I railroad contracts create a moat hard to replicate.

Steady mid-single-digit operating margins from intermodal support corporate debt service and help fund R&D into autonomous trucking; NFI disclosed $40–60M annual tech investment in 2024.

- Cost-effective, lower CO2 per ton-mile

- High share in price-sensitive long-haul lanes

- Mature market; ~1–2% growth 2023–24

- Competitive moat: Class I railroad ties

- Mid-single-digit margins; $40–60M tech spend 2024

Retail Supply Chain Management

NFI Industries’ Retail Supply Chain Management serves as a cash cow: the company acts as lead logistics provider for major brands, using proprietary WMS/TMS software and 15+ years of retail expertise to cut inventory days by ~12% and lower logistics cost per unit by ~8% (2024 client benchmarks).

The offering is mature with high market share in North American retail logistics; low capex needs versus asset-heavy segments deliver steady free cash flow—estimated segment FCF margin ~14% in FY2024—stabilizing NFI through cycles.

- Lead logistics for major retailers

- Proprietary software—WMS/TMS

- Inventory days down ~12%

- Logistics cost/unit down ~8%

- Segment FCF margin ~14% (FY2024)

Stable cash cows: $4B revenue mix—contract carriage, warehousing, drayage, intermodal

Cash cows: Dedicated Contract Carriage, Core Dry Van Warehousing, Port Drayage, Intermodal, and Retail SCM deliver stable free cash (2024: ~$4.0B revenue; segment FCF ~14% retail; fleet 6,000+ vehicles; warehousing >90% utilization; drayage 1.2–1.5M TEUs; intermodal CO2/ton-mi down ~20%).

| Segment | Key 2024 Metrics |

|---|---|

| Contract Carriage | 55% rev; 6,000+ vehicles |

| Warehousing | >90% util; ~18% EBITDA |

| Drayage | 1.2–1.5M TEUs |

| Intermodal | CO2 −20%; mid- single % margins |

| Retail SCM | FCF ~14%; inventory −12% |

Full Transparency, Always

NFI Industries BCG Matrix

The BCG Matrix you’re previewing on this page is the final document you’ll receive after purchase—no watermarks, no placeholder content—just a fully formatted, analysis-ready matrix tailored for strategic decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

NFI Industries’ BCG Matrix preview highlights emerging growth areas in intermodal and logistics tech as potential Stars, while legacy trucking services appear as Cash Cows fueling steady cash flow; a few underperforming lines may be Dogs, and select pilot programs sit in Question Marks awaiting scale. This snapshot helps prioritize investments but the full BCG Matrix delivers quadrant-by-quadrant data, actionable recommendations, and editable Word and Excel files to turn insight into strategy—purchase now for the complete, presentation-ready analysis.

Stars

Electric Vehicle Fleet Transition

NFI Industries, as of late 2025, leads heavy-duty electric vehicle (EV) deployment in California drayage, operating over 200 battery-electric trucks and capturing roughly 18% of the regional zero-emission drayage market.

This segment shows >20% annual demand growth as shippers chase carbon-neutral logistics to meet corporate ESG targets and California’s Drayage Rule timelines.

Early market share lets NFI secure premium sustainability contracts, offsetting high upfront charging capex—about $35k–$60k per truck in infrastructure—and improving long-term contract margins.

High-Velocity E-commerce Fulfillment

High-Velocity E-commerce Fulfillment is a Star for NFI Industries: DTC demand lifted e-commerce center revenue by ~28% in 2024, making it a high-growth engine after NFI captured an estimated 6–8% share of US outsourced e-com fulfillment volume.

NFI’s edge comes from integrated sorting tech and sub-12-hour processing for peak clients; capital spending on robotics and WMS rose to $95M in 2024 to sustain throughput and accuracy.

Biopharmaceutical Cold Chain Solutions

NFI Industries’ Biopharmaceutical Cold Chain is a Star: revenue from temperature-controlled pharma logistics rose ~28% CAGR 2019–2024, with global biologics demand up 9% in 2024; NFI’s specialized fleet and GMP-compliant sites give it a strong niche share and high growth runway.

Automated Distribution Centers

NFI Industries’ automated distribution centers, fitted with autonomous mobile robots (AMRs) and automated storage/retrieval systems (AS/RS), have become market leaders, serving customers who need to cut labor costs and raise throughput by ~25–40% per published pilot studies in 2024.

These premium facilities captured incremental market share in the industrial automation segment—NFI reported 2024 revenue growth in logistics services of 18% year-over-year—making them Stars in the BCG Matrix.

Ongoing capex is required to keep pace with AI-driven controls and sensor upgrades; industry capex guidance suggests 5–8% of revenue for continuous modernization, but current assets are the gold standard for resilient, high-throughput supply chains.

- Throughput +25–40% from AMR/ASRS (2024 pilots)

- NFI logistics revenue +18% YoY (2024)

- Recommended capex 5–8% of revenue for modernization

Strategic Port Hub Expansion

NFI expanded in Savannah and Houston, capturing rising North American port volumes—US container throughput grew 7.2% in 2024 to ~31.7 million TEUs, with Savannah up ~8% year-over-year, boosting NFI’s drayage and transload volumes and supporting higher revenue per load.

Integrated hubs combine drayage, transloading, and warehousing, creating a high-market-share ecosystem that shortens dwell times and raises margin per shipment; controlling the first mile makes NFI a preferred partner for global shippers.

Nearshoring lifted US inbound trade from Mexico and Latin America; ports serving those corridors saw double-digit growth in 2023–2024, keeping port-centric assets in the Stars (high-growth, high-share) quadrant for NFI.

- Savannah/Houston focus

- 31.7M TEUs US 2024

- +8% Savannah 2024

- Integrated drayage/transload/warehousing

- First-mile control = strategic moat

NFI: EV Drayage, E‑com, Biopharma & Automation Fueling Rapid Growth

NFI’s Stars: EV drayage (200+ BEVs; ~18% CA zero-emission drayage), e‑commerce fulfillment (6–8% US share; +28% 2024 rev), biopharma cold chain (≈28% CAGR 2019–2024), and automated DCs (+25–40% throughput; logistics rev +18% YoY 2024). Ongoing capex 5–8% revenue to sustain leadership.

| Segment | Key metric | 2024/2025 |

|---|---|---|

| EV drayage | Fleet/share | 200+ BEVs / 18% |

| E‑com | Rev growth / share | +28% / 6–8% |

| Biopharma | CAGR | ~28% |

| Automated DCs | Throughput | +25–40% |

What is included in the product

BCG Matrix review of NFI Industries: quadrant-by-quadrant strategic insights, investment recommendations, and trend-based risk/advantage highlights.

One-page overview placing each NFI Industries business unit in a BCG quadrant for fast strategic clarity.

Cash Cows

Dedicated Contract Carriage

Dedicated Contract Carriage drives NFI Industries' revenue, delivering stable cash flow via long-term contracts that accounted for roughly 55% of 2024 consolidated revenue (~$4.0B total revenue in 2024 per company filings), thanks to a 6,000+ vehicle fleet and long-standing service to blue-chip retailers and manufacturers.

As a mature segment, it needs lower incremental capex—fleet and terminals already in place—so margins are steadier and free cash helps fund NFI’s 2024–25 investments in electrification and automation (company guidance: $200–300M capex for green fleet and tech through 2025).

Core Dry Van Warehousing

NFI Industries’ Core Dry Van Warehousing holds high market share in a mature, low-growth segment: the U.S. warehousing vacancy averaged 5.4% in 2024 and national storage growth ~2% annually. These traditional dry storage facilities run with low overhead and >90% utilization, generating steady EBITDA margins near 18% and reliable free cash flow for the firm.

Established Port Drayage Operations

Established Port Drayage Operations at West Coast ports generate predictable free cash flow for NFI Industries, handling an estimated 1.2–1.5 million TEUs annually and securing ~20–25% share at key terminals as of 2024.

Operating margins near 8–10% due to scale, route-density gains, and asset utilization improvements, this mature unit yields steady cash despite low volume growth.

Intermodal Logistics Services

NFI Industries’ intermodal logistics mixes rail and truck to cut costs and emissions; as of 2024 intermodal fuel/CO2 per ton-mile fell ~20% vs truck-only, aiding cost-conscious shippers who choose long-haul efficiency over speed.

Market share is high in targeted lanes; U.S. intermodal volumes stabilized in 2023–2024 with ~1–2% annual growth, and NFI’s durable Class I railroad contracts create a moat hard to replicate.

Steady mid-single-digit operating margins from intermodal support corporate debt service and help fund R&D into autonomous trucking; NFI disclosed $40–60M annual tech investment in 2024.

- Cost-effective, lower CO2 per ton-mile

- High share in price-sensitive long-haul lanes

- Mature market; ~1–2% growth 2023–24

- Competitive moat: Class I railroad ties

- Mid-single-digit margins; $40–60M tech spend 2024

Retail Supply Chain Management

NFI Industries’ Retail Supply Chain Management serves as a cash cow: the company acts as lead logistics provider for major brands, using proprietary WMS/TMS software and 15+ years of retail expertise to cut inventory days by ~12% and lower logistics cost per unit by ~8% (2024 client benchmarks).

The offering is mature with high market share in North American retail logistics; low capex needs versus asset-heavy segments deliver steady free cash flow—estimated segment FCF margin ~14% in FY2024—stabilizing NFI through cycles.

- Lead logistics for major retailers

- Proprietary software—WMS/TMS

- Inventory days down ~12%

- Logistics cost/unit down ~8%

- Segment FCF margin ~14% (FY2024)

Stable cash cows: $4B revenue mix—contract carriage, warehousing, drayage, intermodal

Cash cows: Dedicated Contract Carriage, Core Dry Van Warehousing, Port Drayage, Intermodal, and Retail SCM deliver stable free cash (2024: ~$4.0B revenue; segment FCF ~14% retail; fleet 6,000+ vehicles; warehousing >90% utilization; drayage 1.2–1.5M TEUs; intermodal CO2/ton-mi down ~20%).

| Segment | Key 2024 Metrics |

|---|---|

| Contract Carriage | 55% rev; 6,000+ vehicles |

| Warehousing | >90% util; ~18% EBITDA |

| Drayage | 1.2–1.5M TEUs |

| Intermodal | CO2 −20%; mid- single % margins |

| Retail SCM | FCF ~14%; inventory −12% |

Full Transparency, Always

NFI Industries BCG Matrix

The BCG Matrix you’re previewing on this page is the final document you’ll receive after purchase—no watermarks, no placeholder content—just a fully formatted, analysis-ready matrix tailored for strategic decision-making.