NFI Industries PESTLE Analysis

Your Shortcut to Market Insight Starts Here

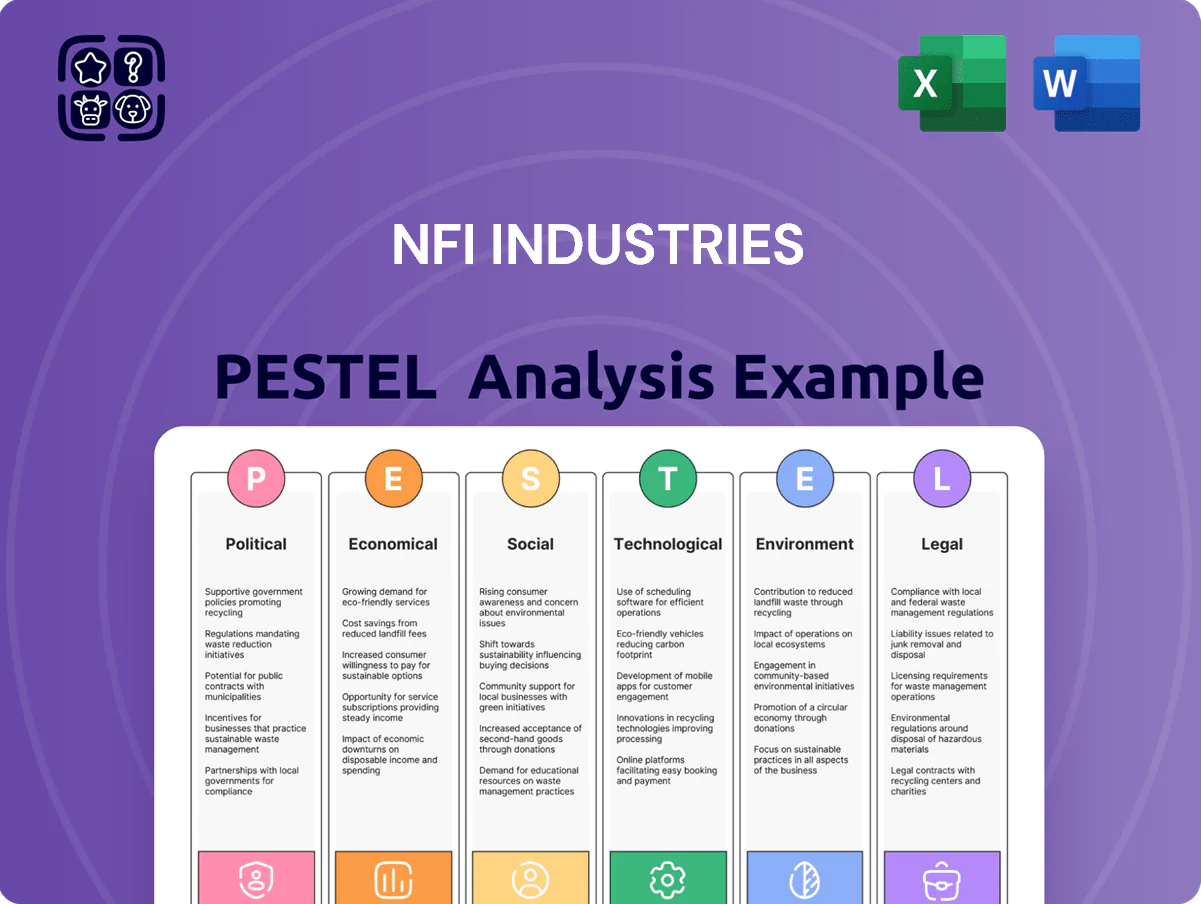

Unlock strategic clarity with our focused PESTLE Analysis of NFI Industries—examining political, economic, social, technological, legal, and environmental forces that will shape its growth and risks; ideal for investors and strategists seeking actionable foresight. Purchase the full report to access detailed, ready-to-use insights and data visualizations that accelerate smarter decisions.

Political factors

Geopolitical Trade Relations

The international trade environment remained volatile in late 2025, with US-Mexico-Canada trade tensions and US protectionist measures increasing tariff uncertainty; US goods imports fell 2.1% year-over-year in Q3 2025, pressuring NFI Industries’ freight forwarding volumes.

Fluctuating tariffs and non-tariff barriers have raised cross-border logistics costs by an estimated 3–5% for shippers in 2025, directly affecting NFI’s port drayage demand and margin management.

Nearshoring to Mexico accelerated—US FDI into Mexico rose 8% in 2024–25—requiring NFI to navigate evolving customs rules and enhanced security protocols across border routes to support volume shifts.

Infrastructure Investment Legislation

Federal infrastructure bills through 2025, including the Bipartisan Infrastructure Law allocations, channel about $110 billion to highways and $17 billion to ports, directly shaping NFI Industries’ route efficiency and fleet utilization by reducing congestion and improving transit times.

State-level matching grants and FASTLANE-like programs, totaling roughly $30–40 billion across key states in 2024–25, accelerate highway and bridge upgrades that enhance NFI’s dedicated service reliability and lower maintenance costs.

Continued federal support for intermodal rail projects—about $12–15 billion earmarked for rail connectivity enhancements in 2024–25—remains pivotal to NFI’s long-term asset utilization, enabling expanded intermodal lanes and higher-margin logistics offerings.

Labor Union Dynamics and Regulations

Cross-Border Regulatory Alignment

As NFI scales in the USMCA region, harmonized customs and safety standards are critical: USMCA trade was valued at about USD 1.7 trillion in 2024 between the three countries, so misalignment could disrupt major flows.

Political stability among the United States, Canada and Mexico supports throughput at inland ports like Laredo and Niagara, which handled multimodal cargo valued in the hundreds of billions in 2024.

Any diplomatic friction or policy shifts can raise administrative costs and delays for NFI’s integrated logistics, potentially increasing border dwell times and operating expenses.

- USMCA 2024 trade ~USD 1.7T

- Key inland ports processed cargo worth hundreds of billions

- Political friction risks higher dwell times and admin costs

Energy Security and Subsidies

Government policies on energy independence and subsidies for alternative fuels significantly shape NFI Industries fleet choices; U.S. federal grants and state incentives covered up to 30-40% of electric heavy-duty vehicle costs in 2024, reducing upfront barriers.

Political incentives for EVs and hydrogen—such as the 2023-25 Inflation Reduction Act credits and Canadian Zero-Emission Vehicle mandates—increased NFI’s green fleet purchases, targeting 25-40% electrification by 2030.

Shifts in political leadership can alter subsidy levels and tax credits, creating ROI uncertainty: a 10-20% swing in incentives can change payback periods for electric buses by 3–6 years.

- 2024 incentives covered 30–40% of EV heavy-duty costs

- NFI target: 25–40% electrified fleet by 2030

- 10–20% incentive change = 3–6 year ROI swing

Trade frictions, nearshoring & incentives reshape logistics costs, labor and electrification

Political factors: trade tensions and tariffs raised cross-border logistics costs ~3–5% in 2025, nearshoring (US FDI into Mexico +8% in 2024–25) shifted volumes, infrastructure funding (~$139B to highways/ports in 2024–25) improved routes, unionization and labor actions increased labor cost share (~46% of operating costs) and strike risk, and EV/hydrogen incentives (covering 30–40% of HD EV costs in 2024) drive fleet electrification targets (25–40% by 2030).

| Metric | Value |

|---|---|

| Cross-border cost rise | 3–5% |

| US FDI into Mexico | +8% (2024–25) |

| Infra funding | $139B (2024–25) |

| Labor cost share | ~46% |

| EV incentive support | 30–40% |

What is included in the product

Explores how external macro-environmental factors uniquely affect NFI Industries across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights, forward-looking scenarios, and actionable implications to inform strategy, risk management, and funding decisions for executives, consultants, and investors.

A concise, PESTLE-segmented summary of NFI Industries that’s easily drop-in ready for presentations or strategy sessions, helping teams quickly align on external risks, regulatory shifts, and market opportunities.

Economic factors

Interest Rate and Capital Cost Fluctuations

The 10-year U.S. Treasury yield rising to about 4.5% at end-2025 raises NFI’s average borrowing costs, increasing capex financing expenses for fleet and warehouse expansion; higher rates could lift lease and loan yields by several hundred basis points, slowing acquisitions of specialized equipment and real estate. NFI needs to manage a conservative debt-to-equity target—keeping net leverage near its 2024 range (~2.0x EBITDA) to preserve liquidity while pursuing measured growth in a cautious macro backdrop.

Consumer Spending and E-commerce Demand

NFI’s warehousing and distribution are closely tied to retail health; U.S. retail sales grew 3.8% y/y through 2024, supporting demand for logistics capacity, yet weakening consumer confidence (Index 2024 avg 100.2) raises downside risk.

As e-commerce approached maturity by late 2025—global e-commerce sales projected at $6.6T in 2024 with CAGR slowing—the need for advanced fulfillment (automation, omnichannel) remains a core revenue driver for NFI.

Inflationary pressure (U.S. CPI 3.4% in 2024) and shifts toward services can cause inventory volatility across NFI’s client mix, prompting variable warehouse utilization and shorter contract durations.

Fuel Price Volatility and Surcharges

Global energy market swings pushed US diesel futures up ~36% between Jan 2023 and Dec 2024, raising NFI’s dedicated fleet fuel bills and squeezing margins; fuel surcharges offset some cost but 2024 volatility still compressed brokerage pricing power. In 2024 NFI reported fuel & fuel taxes ~14% of operating expenses, underscoring the economic need to boost mpg, electrify assets, and adopt low-carbon fuels to protect profitability.

Labor Market Tightness and Wage Inflation

The logistics sector projected a driver shortfall of ~80,000 by 2025 and reported median hourly wages rising ~12% YoY in 2024; NFI faces recruiting/retention pressure that increases labor costs and compresses operating margins.

To mitigate, NFI must expand automation capex and retention programs—automation can cut labor hours per shipment by 15–30% while retention initiatives reduce turnover costs (often 20–30% of annual salary).

- Driver shortfall ~80,000 by 2025; median wages +12% YoY (2024)

- Wage inflation strains margins; retention programs lower turnover costs 20–30%

- Automation can reduce labor hours per shipment 15–30%

Global Supply Chain Nearshoring Trends

Nearshoring to Mexico and the Southern US has boosted demand for NFI’s warehousing and transportation, with US-Mexico trade rising 12% year-over-year to about $870 billion in 2024, increasing cross-border freight volumes supporting NFI’s regional growth.

To capture this, NFI must reallocate assets and build new logistics corridors; estimates suggest reshoring could raise demand for regional capacity by 8–15% through 2026, pressuring capital expenditures.

Economic viability hinges on regional wages—Mexican manufacturing wages remain ~40–60% lower than US levels in 2024—and border infrastructure efficiency, where average truck border wait times fell from 3.5 to 2.1 hours after 2023 investments, but still lag ocean routes for certain cost-sensitive goods.

- US-Mexico trade ~$870B (2024)

- Regional capacity demand +8–15% by 2026

- Mexican wages ~40–60% of US (2024)

- Border wait times improved to ~2.1 hrs (post-2023)

Rising rates, fuel and wages squeeze logistics margins as e‑commerce boosts demand

Rising rates (10y ~4.5% end-2025) raise borrowing costs; keep net leverage ~2.0x EBITDA. Retail sales +3.8% y/y (2024) support demand; e-commerce $6.6T (2024) drives fulfillment capex. CPI 3.4% (2024) and diesel +36% (Jan 2023–Dec 2024) squeeze margins; fuel ≈14% of opex. Driver shortfall ~80,000 (2025); wages +12% (2024) raise labor costs.

| Metric | Value |

|---|---|

| 10y Yield | ~4.5% |

| Retail sales | +3.8% y/y (2024) |

| E‑commerce | $6.6T (2024) |

| CPI | 3.4% (2024) |

| Diesel | +36% (2023–24) |

| Fuel opex | ~14% |

| Driver gap | ~80,000 (2025) |

| Wage infl. | +12% (2024) |

What You See Is What You Get

NFI Industries PESTLE Analysis

The preview shown here is the exact PESTLE analysis of NFI Industries you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file with no placeholders or teasers; the content and layout visible now are exactly what you’ll download immediately after payment. Use it as-is for strategic planning, presentations, or further customization. What you see is the finished document you’ll own upon checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our focused PESTLE Analysis of NFI Industries—examining political, economic, social, technological, legal, and environmental forces that will shape its growth and risks; ideal for investors and strategists seeking actionable foresight. Purchase the full report to access detailed, ready-to-use insights and data visualizations that accelerate smarter decisions.

Political factors

Geopolitical Trade Relations

The international trade environment remained volatile in late 2025, with US-Mexico-Canada trade tensions and US protectionist measures increasing tariff uncertainty; US goods imports fell 2.1% year-over-year in Q3 2025, pressuring NFI Industries’ freight forwarding volumes.

Fluctuating tariffs and non-tariff barriers have raised cross-border logistics costs by an estimated 3–5% for shippers in 2025, directly affecting NFI’s port drayage demand and margin management.

Nearshoring to Mexico accelerated—US FDI into Mexico rose 8% in 2024–25—requiring NFI to navigate evolving customs rules and enhanced security protocols across border routes to support volume shifts.

Infrastructure Investment Legislation

Federal infrastructure bills through 2025, including the Bipartisan Infrastructure Law allocations, channel about $110 billion to highways and $17 billion to ports, directly shaping NFI Industries’ route efficiency and fleet utilization by reducing congestion and improving transit times.

State-level matching grants and FASTLANE-like programs, totaling roughly $30–40 billion across key states in 2024–25, accelerate highway and bridge upgrades that enhance NFI’s dedicated service reliability and lower maintenance costs.

Continued federal support for intermodal rail projects—about $12–15 billion earmarked for rail connectivity enhancements in 2024–25—remains pivotal to NFI’s long-term asset utilization, enabling expanded intermodal lanes and higher-margin logistics offerings.

Labor Union Dynamics and Regulations

Cross-Border Regulatory Alignment

As NFI scales in the USMCA region, harmonized customs and safety standards are critical: USMCA trade was valued at about USD 1.7 trillion in 2024 between the three countries, so misalignment could disrupt major flows.

Political stability among the United States, Canada and Mexico supports throughput at inland ports like Laredo and Niagara, which handled multimodal cargo valued in the hundreds of billions in 2024.

Any diplomatic friction or policy shifts can raise administrative costs and delays for NFI’s integrated logistics, potentially increasing border dwell times and operating expenses.

- USMCA 2024 trade ~USD 1.7T

- Key inland ports processed cargo worth hundreds of billions

- Political friction risks higher dwell times and admin costs

Energy Security and Subsidies

Government policies on energy independence and subsidies for alternative fuels significantly shape NFI Industries fleet choices; U.S. federal grants and state incentives covered up to 30-40% of electric heavy-duty vehicle costs in 2024, reducing upfront barriers.

Political incentives for EVs and hydrogen—such as the 2023-25 Inflation Reduction Act credits and Canadian Zero-Emission Vehicle mandates—increased NFI’s green fleet purchases, targeting 25-40% electrification by 2030.

Shifts in political leadership can alter subsidy levels and tax credits, creating ROI uncertainty: a 10-20% swing in incentives can change payback periods for electric buses by 3–6 years.

- 2024 incentives covered 30–40% of EV heavy-duty costs

- NFI target: 25–40% electrified fleet by 2030

- 10–20% incentive change = 3–6 year ROI swing

Trade frictions, nearshoring & incentives reshape logistics costs, labor and electrification

Political factors: trade tensions and tariffs raised cross-border logistics costs ~3–5% in 2025, nearshoring (US FDI into Mexico +8% in 2024–25) shifted volumes, infrastructure funding (~$139B to highways/ports in 2024–25) improved routes, unionization and labor actions increased labor cost share (~46% of operating costs) and strike risk, and EV/hydrogen incentives (covering 30–40% of HD EV costs in 2024) drive fleet electrification targets (25–40% by 2030).

| Metric | Value |

|---|---|

| Cross-border cost rise | 3–5% |

| US FDI into Mexico | +8% (2024–25) |

| Infra funding | $139B (2024–25) |

| Labor cost share | ~46% |

| EV incentive support | 30–40% |

What is included in the product

Explores how external macro-environmental factors uniquely affect NFI Industries across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights, forward-looking scenarios, and actionable implications to inform strategy, risk management, and funding decisions for executives, consultants, and investors.

A concise, PESTLE-segmented summary of NFI Industries that’s easily drop-in ready for presentations or strategy sessions, helping teams quickly align on external risks, regulatory shifts, and market opportunities.

Economic factors

Interest Rate and Capital Cost Fluctuations

The 10-year U.S. Treasury yield rising to about 4.5% at end-2025 raises NFI’s average borrowing costs, increasing capex financing expenses for fleet and warehouse expansion; higher rates could lift lease and loan yields by several hundred basis points, slowing acquisitions of specialized equipment and real estate. NFI needs to manage a conservative debt-to-equity target—keeping net leverage near its 2024 range (~2.0x EBITDA) to preserve liquidity while pursuing measured growth in a cautious macro backdrop.

Consumer Spending and E-commerce Demand

NFI’s warehousing and distribution are closely tied to retail health; U.S. retail sales grew 3.8% y/y through 2024, supporting demand for logistics capacity, yet weakening consumer confidence (Index 2024 avg 100.2) raises downside risk.

As e-commerce approached maturity by late 2025—global e-commerce sales projected at $6.6T in 2024 with CAGR slowing—the need for advanced fulfillment (automation, omnichannel) remains a core revenue driver for NFI.

Inflationary pressure (U.S. CPI 3.4% in 2024) and shifts toward services can cause inventory volatility across NFI’s client mix, prompting variable warehouse utilization and shorter contract durations.

Fuel Price Volatility and Surcharges

Global energy market swings pushed US diesel futures up ~36% between Jan 2023 and Dec 2024, raising NFI’s dedicated fleet fuel bills and squeezing margins; fuel surcharges offset some cost but 2024 volatility still compressed brokerage pricing power. In 2024 NFI reported fuel & fuel taxes ~14% of operating expenses, underscoring the economic need to boost mpg, electrify assets, and adopt low-carbon fuels to protect profitability.

Labor Market Tightness and Wage Inflation

The logistics sector projected a driver shortfall of ~80,000 by 2025 and reported median hourly wages rising ~12% YoY in 2024; NFI faces recruiting/retention pressure that increases labor costs and compresses operating margins.

To mitigate, NFI must expand automation capex and retention programs—automation can cut labor hours per shipment by 15–30% while retention initiatives reduce turnover costs (often 20–30% of annual salary).

- Driver shortfall ~80,000 by 2025; median wages +12% YoY (2024)

- Wage inflation strains margins; retention programs lower turnover costs 20–30%

- Automation can reduce labor hours per shipment 15–30%

Global Supply Chain Nearshoring Trends

Nearshoring to Mexico and the Southern US has boosted demand for NFI’s warehousing and transportation, with US-Mexico trade rising 12% year-over-year to about $870 billion in 2024, increasing cross-border freight volumes supporting NFI’s regional growth.

To capture this, NFI must reallocate assets and build new logistics corridors; estimates suggest reshoring could raise demand for regional capacity by 8–15% through 2026, pressuring capital expenditures.

Economic viability hinges on regional wages—Mexican manufacturing wages remain ~40–60% lower than US levels in 2024—and border infrastructure efficiency, where average truck border wait times fell from 3.5 to 2.1 hours after 2023 investments, but still lag ocean routes for certain cost-sensitive goods.

- US-Mexico trade ~$870B (2024)

- Regional capacity demand +8–15% by 2026

- Mexican wages ~40–60% of US (2024)

- Border wait times improved to ~2.1 hrs (post-2023)

Rising rates, fuel and wages squeeze logistics margins as e‑commerce boosts demand

Rising rates (10y ~4.5% end-2025) raise borrowing costs; keep net leverage ~2.0x EBITDA. Retail sales +3.8% y/y (2024) support demand; e-commerce $6.6T (2024) drives fulfillment capex. CPI 3.4% (2024) and diesel +36% (Jan 2023–Dec 2024) squeeze margins; fuel ≈14% of opex. Driver shortfall ~80,000 (2025); wages +12% (2024) raise labor costs.

| Metric | Value |

|---|---|

| 10y Yield | ~4.5% |

| Retail sales | +3.8% y/y (2024) |

| E‑commerce | $6.6T (2024) |

| CPI | 3.4% (2024) |

| Diesel | +36% (2023–24) |

| Fuel opex | ~14% |

| Driver gap | ~80,000 (2025) |

| Wage infl. | +12% (2024) |

What You See Is What You Get

NFI Industries PESTLE Analysis

The preview shown here is the exact PESTLE analysis of NFI Industries you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file with no placeholders or teasers; the content and layout visible now are exactly what you’ll download immediately after payment. Use it as-is for strategic planning, presentations, or further customization. What you see is the finished document you’ll own upon checkout.