New Hope Liuhe Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

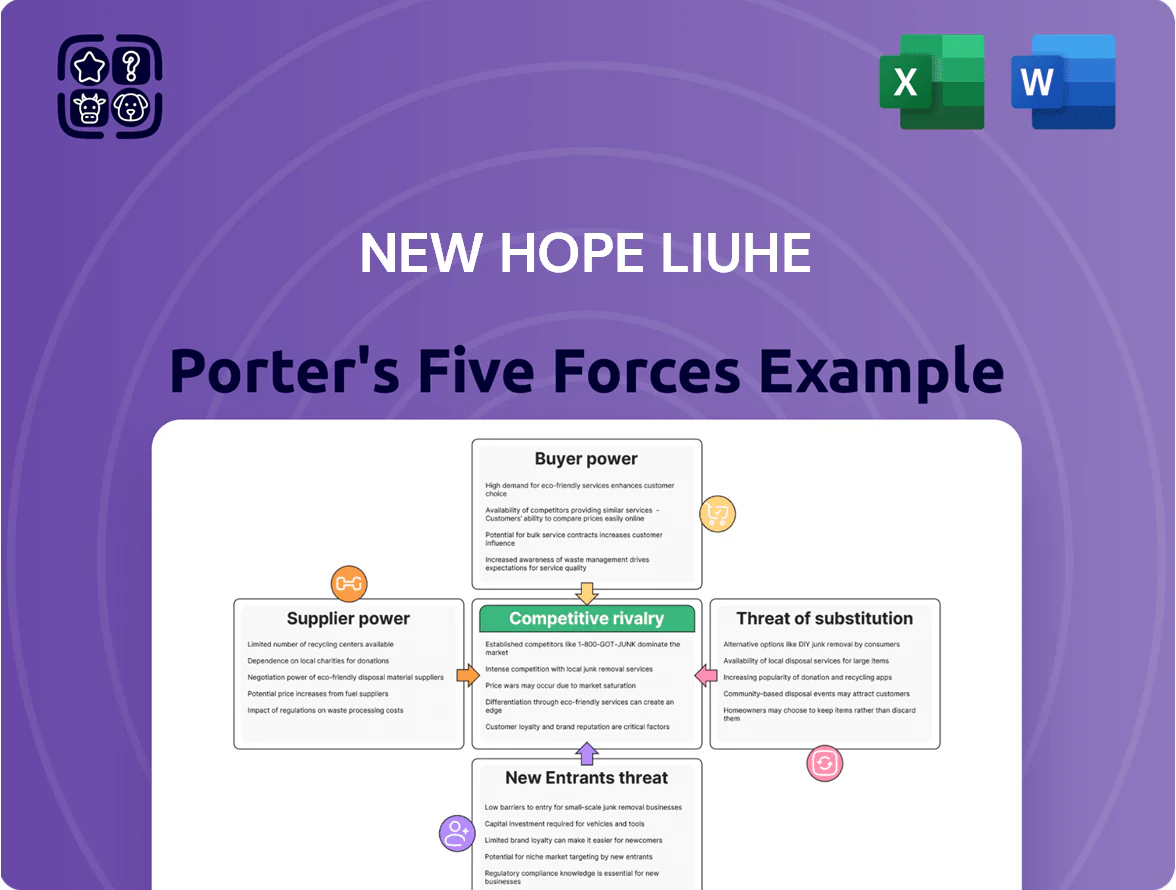

New Hope Liuhe faces moderate supplier leverage, intense buyer price sensitivity, and growing competition from integrated agribusiness and plant-based protein producers, shaping a challenging margin environment.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore New Hope Liuhe’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of raw material inputs

Corn and soybean meal, which made up about 68% of New Hope Liuhe’s feed raw-cost base in 2024, move with global commodity markets and tariffs, so price swings hit margins across its feed-to-meat chain.

Supplier pressure is moderate-to-high: a 2023–24 global corn price spike raised domestic feed costs by roughly 12–18%, compressing gross margins for producers like New Hope.

New Hope offsets volatility via strategic procurement contracts and large-scale storage—its silos held an estimated 2.4 million tonnes of grain capacity in 2024—reducing spot-buy exposure.

Still, sustained export policy shifts or crop failures could force spot purchases and erode margin resilience despite these measures.

Concentration of global grain merchants

A handful of global grain merchants—ADM, Bunge, Cargill, Louis Dreyfus, plus state-owned CNFCO—handle roughly 60–70% of global soy and corn trade, giving them strong pricing and delivery leverage over buyers like New Hope Liuhe.

In 2024 grain export disruptions raised FOB soy prices 18% year-over-year, showing how geopolitical shocks and crop shortfalls quickly amplify supplier power.

New Hope Liuhe needs long-term contracts, financing ties, and localized storage to secure feed inputs for its ~20 MT annual feed output and to mitigate spot-market spikes.

Dependence on high-quality breeding stock

The livestock division needs superior genetics to sustain productivity and disease resistance; access to elite breeding stock drives yield and feed-conversion gains of 5–12% per generation. New Hope Liuhe has internal breeding programs but still buys traits from specialist firms, making suppliers able to charge premiums—elite semen/embryos can cost 20–50% more. This technical edge creates concentrated supplier power in a niche market.

Energy and logistical infrastructure costs

Operating a vertically integrated supply chain needs large energy inputs for processing and diesel for nationwide haulage; New Hope Liuhe spent about RMB 4.2 billion on energy and logistics in FY2024, exposing it to supplier pricing.

Energy and logistics providers wield bargaining power via regulated tariffs and regional oligopolies—port/rail bottlenecks in Northeast China raise costs by an estimated 8–12% vs national average.

Tighter environmental rules through end-2025 push up compliant green energy and low-emission transport premiums; green power contracts can cost 15–30% more, boosting supplier leverage.

- RMB 4.2bn energy/logistics spend (FY2024)

- Regional cost premium 8–12%

- Green premium 15–30% by end-2025

Land and environmental compliance resources

Access to large-scale farmland in China is mainly controlled by local governments and rural collectives, making them gatekeepers for New Hope Liuhe’s expansion; in 2024 about 60–70% of new lease approvals in key provinces required local-government endorsement per Ministry of Natural Resources reports.

Stricter environmental laws since 2021 force specific waste-treatment tech and certifications from specialist vendors; noncompliance can trigger fines up to CNY 1 million and suspension of licenses, so these vendors effectively control operational legality.

- Land access: local govts/rural collectives = primary suppliers

- Certs/tech: specialized vendors required for legal operation

- Regulatory risk: fines up to CNY 1,000,000; license suspension

- Bargaining power: high, because services are mandatory

High supplier leverage: commodities, merchants & premiums squeeze margins

Supplier power is moderate-to-high: feed commodities (68% of raw-costs) and four global grain merchants control ~60–70% of trade, pushing cost swings (corn/soy FOB up ~18% YoY 2024). New Hope’s 2.4Mt storage and long-term contracts limit spot risk, but RMB 4.2bn energy/logistics spend, regional premiums (8–12%) and paid breeding inputs (elite traits +20–50%) keep supplier leverage elevated.

| Metric | 2024 value |

|---|---|

| Feed raw-cost share | 68% |

| Grain merchant market share | 60–70% |

| Storage capacity | 2.4 Mt |

| Energy/logistics spend | RMB 4.2bn |

| Regional premium | 8–12% |

| Elite breeding premium | 20–50% |

What is included in the product

Tailored Five Forces analysis of New Hope Liuhe that uncovers competitive drivers, supplier and buyer power, entry barriers, substitution risks, and emerging disruptors to inform strategic positioning and pricing decisions.

A concise Porter's Five Forces snapshot for New Hope Liuhe—quickly pinpoints supplier, buyer, and competitive pressures to streamline strategic decisions and investor briefings.

Customers Bargaining Power

Dominance of large scale retail chains

Hypermarkets and major grocery chains force meat processors like New Hope Liuhe to cut wholesale prices while keeping high quality; in 2024 China’s top 10 retailers accounted for ~38% of FMCG sales, boosting buyer clout. These chains use volume to secure longer payment terms and slotting fees, which pressured New Hope Liuhe’s food-margin in 2024 (gross margin fell to 12.8% vs 14.5% in 2022). As Chinese retail consolidation continues, institutional buyer leverage keeps rising.

Price sensitivity in commodity meat markets

Growth of institutional food service buyers

Digital platform and e-commerce influence

The rise of online grocery and community group-buying platforms (e.g., Meituan, Pinduoduo) gives intermediaries data-driven bargaining power; in China online FMCG sales hit 38% of retail grocery in 2024, shifting shelf control to platforms.

Platforms control product visibility and can push items based on margin splits and commission rates—commissions for fresh food ranged 8–18% in 2024—forcing New Hope Liuhe to accept lower margins to keep scale.

Here’s the quick math: if platform commission averages 12% and promotional discounts add 6%, net margin on a SKU falls by ~18%, squeezing gross margin and pricing flexibility.

- Platforms = interface + data control, raising customer bargaining power

- Online grocery 38% of retail grocery (2024 China)

- Typical commissions 8–18% (2024)

- Effective margin hit ~18% on promoted SKUs

Consumer demand for food safety transparency

Modern Chinese consumers now switch brands over safety, traceability, and animal welfare; surveys show 68% would change brands after a safety scare (2024 China Food Safety Report).

This gives buyers leverage, forcing New Hope Liuhe to spend on blockchain tracking and third-party certifications; similar firms reported 5–8% margin compression from these investments in 2023.

Failing to match transparency can rapidly cede customers to rivals with verified supply chains, as seen when a 2022 scare cut market share by ~3–6% within months.

- 68% would switch after safety scare (2024)

- 5–8% margin impact from tracking/certs (2023)

- 2022 incidents caused 3–6% share loss

Retailer power, online cuts and safety costs squeeze China food margins in 2024

Buyers have strong leverage: China’s top 10 retailers held ~38% FMCG sales (2024), forcing price cuts and longer pay terms; New Hope Liuhe food gross margin fell to 12.8% in 2024 from 14.5% in 2022. Online grocery (38% of retail grocery, 2024) and platform commissions (8–18%) shave ~18% on promoted SKUs. Safety concerns drive switching—68% would change after a scare—so traceability costs (5–8% margin hit) are necessary.

| Metric | Value (2024) |

|---|---|

| Top-10 retailers FMCG share | ~38% |

| Online grocery share | 38% |

| New Hope Liuhe gross margin (food) | 12.8% |

| Platform commissions | 8–18% |

| Promo+commission margin hit | ~18% |

| Consumers switch after safety scare | 68% |

| Traceability/cert cost impact | 5–8% |

What You See Is What You Get

New Hope Liuhe Porter's Five Forces Analysis

This preview shows the exact New Hope Liuhe Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use; no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

New Hope Liuhe faces moderate supplier leverage, intense buyer price sensitivity, and growing competition from integrated agribusiness and plant-based protein producers, shaping a challenging margin environment.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore New Hope Liuhe’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of raw material inputs

Corn and soybean meal, which made up about 68% of New Hope Liuhe’s feed raw-cost base in 2024, move with global commodity markets and tariffs, so price swings hit margins across its feed-to-meat chain.

Supplier pressure is moderate-to-high: a 2023–24 global corn price spike raised domestic feed costs by roughly 12–18%, compressing gross margins for producers like New Hope.

New Hope offsets volatility via strategic procurement contracts and large-scale storage—its silos held an estimated 2.4 million tonnes of grain capacity in 2024—reducing spot-buy exposure.

Still, sustained export policy shifts or crop failures could force spot purchases and erode margin resilience despite these measures.

Concentration of global grain merchants

A handful of global grain merchants—ADM, Bunge, Cargill, Louis Dreyfus, plus state-owned CNFCO—handle roughly 60–70% of global soy and corn trade, giving them strong pricing and delivery leverage over buyers like New Hope Liuhe.

In 2024 grain export disruptions raised FOB soy prices 18% year-over-year, showing how geopolitical shocks and crop shortfalls quickly amplify supplier power.

New Hope Liuhe needs long-term contracts, financing ties, and localized storage to secure feed inputs for its ~20 MT annual feed output and to mitigate spot-market spikes.

Dependence on high-quality breeding stock

The livestock division needs superior genetics to sustain productivity and disease resistance; access to elite breeding stock drives yield and feed-conversion gains of 5–12% per generation. New Hope Liuhe has internal breeding programs but still buys traits from specialist firms, making suppliers able to charge premiums—elite semen/embryos can cost 20–50% more. This technical edge creates concentrated supplier power in a niche market.

Energy and logistical infrastructure costs

Operating a vertically integrated supply chain needs large energy inputs for processing and diesel for nationwide haulage; New Hope Liuhe spent about RMB 4.2 billion on energy and logistics in FY2024, exposing it to supplier pricing.

Energy and logistics providers wield bargaining power via regulated tariffs and regional oligopolies—port/rail bottlenecks in Northeast China raise costs by an estimated 8–12% vs national average.

Tighter environmental rules through end-2025 push up compliant green energy and low-emission transport premiums; green power contracts can cost 15–30% more, boosting supplier leverage.

- RMB 4.2bn energy/logistics spend (FY2024)

- Regional cost premium 8–12%

- Green premium 15–30% by end-2025

Land and environmental compliance resources

Access to large-scale farmland in China is mainly controlled by local governments and rural collectives, making them gatekeepers for New Hope Liuhe’s expansion; in 2024 about 60–70% of new lease approvals in key provinces required local-government endorsement per Ministry of Natural Resources reports.

Stricter environmental laws since 2021 force specific waste-treatment tech and certifications from specialist vendors; noncompliance can trigger fines up to CNY 1 million and suspension of licenses, so these vendors effectively control operational legality.

- Land access: local govts/rural collectives = primary suppliers

- Certs/tech: specialized vendors required for legal operation

- Regulatory risk: fines up to CNY 1,000,000; license suspension

- Bargaining power: high, because services are mandatory

High supplier leverage: commodities, merchants & premiums squeeze margins

Supplier power is moderate-to-high: feed commodities (68% of raw-costs) and four global grain merchants control ~60–70% of trade, pushing cost swings (corn/soy FOB up ~18% YoY 2024). New Hope’s 2.4Mt storage and long-term contracts limit spot risk, but RMB 4.2bn energy/logistics spend, regional premiums (8–12%) and paid breeding inputs (elite traits +20–50%) keep supplier leverage elevated.

| Metric | 2024 value |

|---|---|

| Feed raw-cost share | 68% |

| Grain merchant market share | 60–70% |

| Storage capacity | 2.4 Mt |

| Energy/logistics spend | RMB 4.2bn |

| Regional premium | 8–12% |

| Elite breeding premium | 20–50% |

What is included in the product

Tailored Five Forces analysis of New Hope Liuhe that uncovers competitive drivers, supplier and buyer power, entry barriers, substitution risks, and emerging disruptors to inform strategic positioning and pricing decisions.

A concise Porter's Five Forces snapshot for New Hope Liuhe—quickly pinpoints supplier, buyer, and competitive pressures to streamline strategic decisions and investor briefings.

Customers Bargaining Power

Dominance of large scale retail chains

Hypermarkets and major grocery chains force meat processors like New Hope Liuhe to cut wholesale prices while keeping high quality; in 2024 China’s top 10 retailers accounted for ~38% of FMCG sales, boosting buyer clout. These chains use volume to secure longer payment terms and slotting fees, which pressured New Hope Liuhe’s food-margin in 2024 (gross margin fell to 12.8% vs 14.5% in 2022). As Chinese retail consolidation continues, institutional buyer leverage keeps rising.

Price sensitivity in commodity meat markets

Growth of institutional food service buyers

Digital platform and e-commerce influence

The rise of online grocery and community group-buying platforms (e.g., Meituan, Pinduoduo) gives intermediaries data-driven bargaining power; in China online FMCG sales hit 38% of retail grocery in 2024, shifting shelf control to platforms.

Platforms control product visibility and can push items based on margin splits and commission rates—commissions for fresh food ranged 8–18% in 2024—forcing New Hope Liuhe to accept lower margins to keep scale.

Here’s the quick math: if platform commission averages 12% and promotional discounts add 6%, net margin on a SKU falls by ~18%, squeezing gross margin and pricing flexibility.

- Platforms = interface + data control, raising customer bargaining power

- Online grocery 38% of retail grocery (2024 China)

- Typical commissions 8–18% (2024)

- Effective margin hit ~18% on promoted SKUs

Consumer demand for food safety transparency

Modern Chinese consumers now switch brands over safety, traceability, and animal welfare; surveys show 68% would change brands after a safety scare (2024 China Food Safety Report).

This gives buyers leverage, forcing New Hope Liuhe to spend on blockchain tracking and third-party certifications; similar firms reported 5–8% margin compression from these investments in 2023.

Failing to match transparency can rapidly cede customers to rivals with verified supply chains, as seen when a 2022 scare cut market share by ~3–6% within months.

- 68% would switch after safety scare (2024)

- 5–8% margin impact from tracking/certs (2023)

- 2022 incidents caused 3–6% share loss

Retailer power, online cuts and safety costs squeeze China food margins in 2024

Buyers have strong leverage: China’s top 10 retailers held ~38% FMCG sales (2024), forcing price cuts and longer pay terms; New Hope Liuhe food gross margin fell to 12.8% in 2024 from 14.5% in 2022. Online grocery (38% of retail grocery, 2024) and platform commissions (8–18%) shave ~18% on promoted SKUs. Safety concerns drive switching—68% would change after a scare—so traceability costs (5–8% margin hit) are necessary.

| Metric | Value (2024) |

|---|---|

| Top-10 retailers FMCG share | ~38% |

| Online grocery share | 38% |

| New Hope Liuhe gross margin (food) | 12.8% |

| Platform commissions | 8–18% |

| Promo+commission margin hit | ~18% |

| Consumers switch after safety scare | 68% |

| Traceability/cert cost impact | 5–8% |

What You See Is What You Get

New Hope Liuhe Porter's Five Forces Analysis

This preview shows the exact New Hope Liuhe Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use; no placeholders or samples.