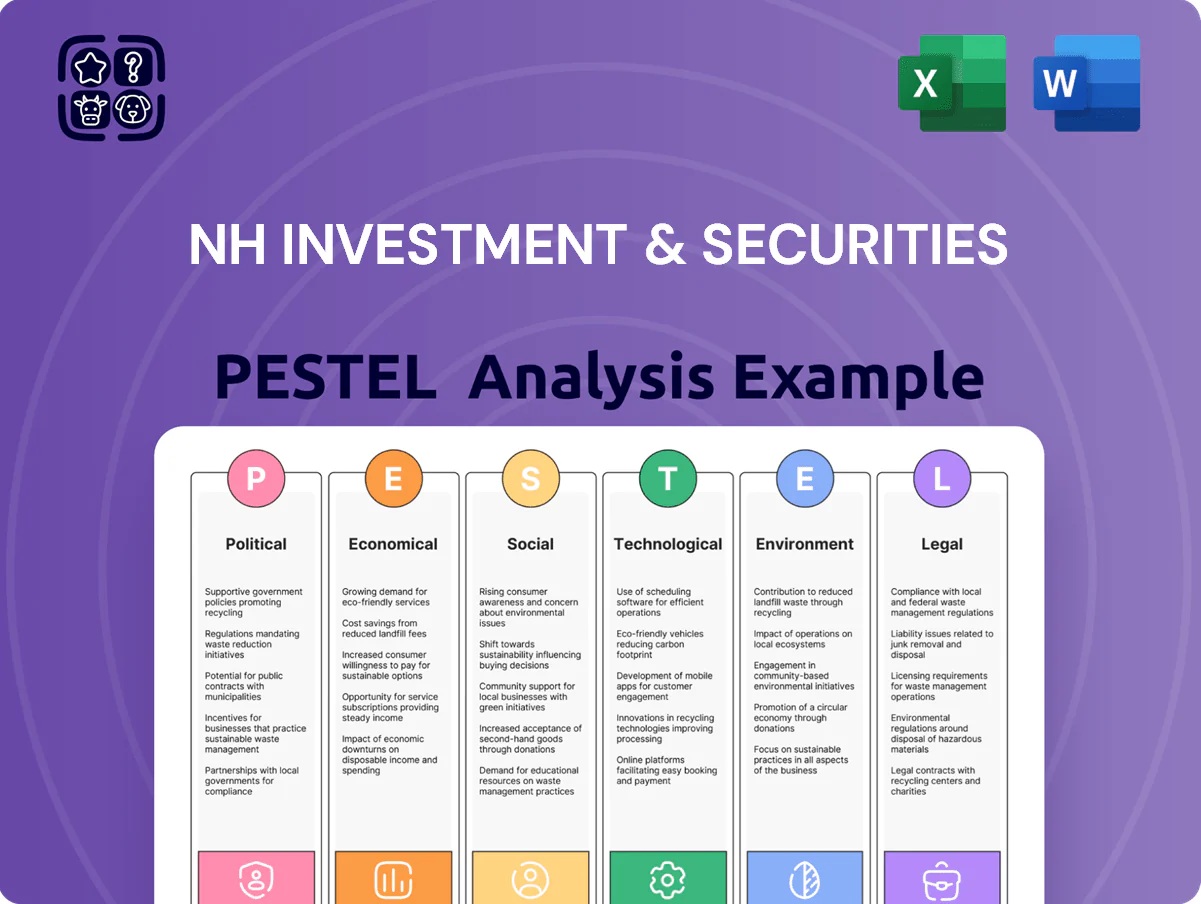

NH Investment & Securities PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our targeted PESTLE Analysis of NH Investment & Securities—spot regulatory risks, macroeconomic drivers, and technological shifts shaping performance. Ideal for investors and strategists, this concise briefing highlights actionable implications and growth levers. Purchase the full report to access detailed, editable findings and make faster, smarter decisions.

Political factors

Corporate Value-up Program Support

The South Korean government extended the Corporate Value-up Program through 2025 to close the Korea Discount, committing roughly KRW 2.5 trillion in incentives and regulatory support; NH Investment & Securities acts as a primary intermediary, advising on M&A, spin-offs and shareholder return plans for over 120 listed clients in 2024–25; this political push directly increases NH’s brokerage and advisory fee pools, contributing to a projected advisory revenue uplift of 8–12% in 2025.

Geopolitical Tensions and Market Volatility

Ongoing tensions on the Korean Peninsula and shifting Indo-Pacific alliances keep investor risk premia elevated; Korea risk spreads widened in 2024, with sovereign CDS rising to ~40–50bps during peak episodes, influencing capital flows into safer assets.

Political instability heightens market volatility, which in 2024 correlated with a 12–18% rise in trading volumes at major Korean brokerages, potentially boosting NH Investment’s brokerage revenues.

Prolonged geopolitical risk can deter FDI—Korea’s FDI inflows fell 6% in 2024 YoY—and complicate NH Investment’s international expansion and cross-border M&A strategies.

Agricultural Cooperative Group Influence

As a subsidiary of the National Agricultural Cooperative Federation, NH Investment & Securities aligns with cooperative political objectives, affecting strategy and capital allocation; in 2024 the parent’s consolidated assets exceeded KRW 200 trillion, anchoring NH’s RMB-equivalent AUM and lending focus. Government agricultural support programs and the Rural Development Fund (2023 budget KRW 4.5 trillion) steer NH’s product mix toward rural financing, offering stability but requiring compliance with national rural development targets.

Trade Policy and Export-Led Growth

South Korea's trade ties with the US and China—respectively 11% and 25% of exports in 2024—directly shape revenue for NH Investment's large corporate clients in semiconductors and autos; a 10% US tariff or a 5% Chinese import slowdown could cut client export revenues materially.

Political shifts in trade agreements alter margins for manufacturing and tech firms, impacting deal pipelines and M&A valuations NH advises on; Korea's goods exports were $644bn in 2024, underscoring sensitivity.

NH Investment must adapt advisory, hedging, and risk-management services to scenario-driven stress tests and tariff contingency models to protect client earnings and fee income.

- US and China account for ~36% of SK exports (2024)

- Goods exports $644bn (2024) — high client exposure

- Tariff or policy shifts can materially affect deal valuations

- Requires scenario stress tests, hedging, and advisory adjustments

Financial Regulatory Liberalization

Government moves to liberalize finance and promote Seoul as a global hub gained momentum by late 2025, with regulatory reforms easing capital flow and expanding offshore license scopes, supporting NH Investment & Securities’ international branches.

Policy changes allowing greater flexibility in offshore operations and FX transactions—reflected in a 12% rise in offshore deal volume in 2024 and a 9% increase in FX trading turnover through H1 2025—boost NH’s regional competitiveness.

These shifts enable NH to better compete with global investment banks in Asia by lowering compliance barriers and facilitating cross-border product distribution.

- Regulatory liberalization accelerated late 2025

- Offshore deal volume +12% in 2024

- FX turnover +9% H1 2025

- Improved cross-border distribution and competitive parity with global banks

Policy boosts Korea capital markets amid export tariff risks and rising trading volumes

Political initiatives like the Corporate Value-up Program (KRW 2.5tn through 2025) and finance liberalization (offshore deals +12% 2024; FX turnover +9% H1 2025) expand NH Investment’s advisory and trading revenue pools, while Korea’s 2024 exports of $644bn and US/China ~36% share raise client vulnerability to tariff shocks; geopolitical risk pushed sovereign CDS to ~40–50bps in 2024, lifting trading volumes +12–18% and stressing cross-border deal flow (FDI -6% 2024).

| Metric | Value (2024/2025) |

|---|---|

| Corporate Value-up Fund | KRW 2.5tn |

| Goods exports | $644bn |

| US+China export share | ~36% |

| Sovereign CDS (peak) | ~40–50bps |

| Trading volume change | +12–18% |

| Offshore deal vol | +12% (2024) |

| FX turnover | +9% H1 2025 |

| FDI inflows | -6% YoY (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect NH Investment & Securities across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights tailored for executives, investors, and consultants to identify actionable risks and opportunities in its region and industry.

Condenses NH Investment & Securities' PESTLE into a concise, shareable brief—visually segmented by category and written in plain language—so teams can quickly align on external risks, market positioning, and strategic actions during meetings or client presentations.

Economic factors

Interest Rate Environment and Monetary Policy

Bank of Korea’s end-2025 policy rate largely determines NH Investment & Securities’ fixed-income and wealth management results; with the BOK holding 2024 rates at 3.50% then signaling cuts to ~3.00% by late 2025, bond yields and duration risk compress, lifting bond prices and boosting AUM performance.

Domestic Economic Growth and Consumption

South Korea's GDP grew 1.8% in 2024 after 2.6% in 2023, and household consumption slowed to a 2024 real growth near 1.0%, constraining retail investment inflows into brokerage and wealth products.

Economic stagnation and muted wage growth—real wage change ~0–1% in 2024—reduce new capital into NH Investment accounts, lowering fee and AUM growth prospects.

NH Investment should shift toward low-cost, income-generating products and digital advisory suited to risk-averse retail sentiment and subdued consumption.

Currency Exchange Rate Volatility

The strength of the Korean Won against the US Dollar is critical for NH Investment’s international asset management and brokerage; in 2024 the KRW appreciated ~3.5% vs USD year-to-date, directly altering USD-denominated returns for domestic clients.

Exchange-rate fluctuations influence client demand for global market access—NH reported 18% of AUM in offshore assets in 2024, prompting shifts in product flows.

The firm employs dynamic hedging—forward contracts and cross-currency swaps—reducing currency P&L volatility; hedging coverage reached ~65% of offshore exposure in 2024.

Capital Market Liquidity Trends

Capital market liquidity in KOSPI/KOSDAQ directly affects NH Investment’s ability to execute large institutional orders; average daily turnover on KOSPI reached about KRW 12.4 trillion and KOSDAQ KRW 5.1 trillion in 2024, enabling tighter spreads and greater commission income during high-liquidity periods.

The firm tracks liquidity cycles—2023–2025 saw volatility spikes that widened spreads but 2024 market-wide ADV gains improved market-making profitability and supported proprietary trading deployment strategies.

- 2024 KOSPI ADV ~KRW 12.4T; KOSDAQ ADV ~KRW 5.1T

- Higher liquidity → tighter spreads ↑ commission revenue

- Monitors cycles to time market-making and prop trades

Inflationary Pressures and Asset Valuation

Persistent or volatile inflation alters real returns across NH Investment & Securities' portfolios; South Korea's CPI rose 2.5% in 2025 vs 3.7% in 2024, compressing real yields on nominal bonds and equities.

Higher inflation shifts client demand toward commodities, real estate and inflation-linked bonds—Korean CPI-linked bond issuance grew ~18% YoY in 2024—prompting reweighting away from traditional fixed income.

NH Investment's research and allocation teams must adjust strategies, offering TIPS-like products, real assets and dynamic inflation-hedging overlays to preserve purchasing power.

- Inflation: Korea CPI 3.7% (2024), 2.5% (2025 est)

- Asset flows: CPI-linked bond issuance +18% YoY (2024)

- Strategy: increased allocation to real assets and inflation-linked instruments

BOK easing lifts bond prices & AUM; modest growth, softer CPI, KRW up

BOK rate path (3.50% in 2024 → ~3.00% by late‑2025) compresses yields, boosting bond prices and AUM; 2024 GDP 1.8% and household consumption ~1.0% constrain retail inflows; KRW appreciated ~3.5% YTD 2024 with 18% AUM offshore and ~65% hedging coverage; KOSPI/KOSDAQ ADV 12.4T/5.1T KRW (2024); CPI 3.7% (2024) → 2.5% (2025 est), CPI‑linked issuance +18% YoY (2024).

| Metric | 2024 | 2025 est |

|---|---|---|

| BOK rate | 3.50% | ~3.00% |

| GDP growth | 1.8% | - |

| CPI | 3.7% | 2.5% |

| KOSPI/KOSDAQ ADV | 12.4T / 5.1T KRW | - |

Same Document Delivered

NH Investment & Securities PESTLE Analysis

The preview shown here is the exact NH Investment & Securities PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our targeted PESTLE Analysis of NH Investment & Securities—spot regulatory risks, macroeconomic drivers, and technological shifts shaping performance. Ideal for investors and strategists, this concise briefing highlights actionable implications and growth levers. Purchase the full report to access detailed, editable findings and make faster, smarter decisions.

Political factors

Corporate Value-up Program Support

The South Korean government extended the Corporate Value-up Program through 2025 to close the Korea Discount, committing roughly KRW 2.5 trillion in incentives and regulatory support; NH Investment & Securities acts as a primary intermediary, advising on M&A, spin-offs and shareholder return plans for over 120 listed clients in 2024–25; this political push directly increases NH’s brokerage and advisory fee pools, contributing to a projected advisory revenue uplift of 8–12% in 2025.

Geopolitical Tensions and Market Volatility

Ongoing tensions on the Korean Peninsula and shifting Indo-Pacific alliances keep investor risk premia elevated; Korea risk spreads widened in 2024, with sovereign CDS rising to ~40–50bps during peak episodes, influencing capital flows into safer assets.

Political instability heightens market volatility, which in 2024 correlated with a 12–18% rise in trading volumes at major Korean brokerages, potentially boosting NH Investment’s brokerage revenues.

Prolonged geopolitical risk can deter FDI—Korea’s FDI inflows fell 6% in 2024 YoY—and complicate NH Investment’s international expansion and cross-border M&A strategies.

Agricultural Cooperative Group Influence

As a subsidiary of the National Agricultural Cooperative Federation, NH Investment & Securities aligns with cooperative political objectives, affecting strategy and capital allocation; in 2024 the parent’s consolidated assets exceeded KRW 200 trillion, anchoring NH’s RMB-equivalent AUM and lending focus. Government agricultural support programs and the Rural Development Fund (2023 budget KRW 4.5 trillion) steer NH’s product mix toward rural financing, offering stability but requiring compliance with national rural development targets.

Trade Policy and Export-Led Growth

South Korea's trade ties with the US and China—respectively 11% and 25% of exports in 2024—directly shape revenue for NH Investment's large corporate clients in semiconductors and autos; a 10% US tariff or a 5% Chinese import slowdown could cut client export revenues materially.

Political shifts in trade agreements alter margins for manufacturing and tech firms, impacting deal pipelines and M&A valuations NH advises on; Korea's goods exports were $644bn in 2024, underscoring sensitivity.

NH Investment must adapt advisory, hedging, and risk-management services to scenario-driven stress tests and tariff contingency models to protect client earnings and fee income.

- US and China account for ~36% of SK exports (2024)

- Goods exports $644bn (2024) — high client exposure

- Tariff or policy shifts can materially affect deal valuations

- Requires scenario stress tests, hedging, and advisory adjustments

Financial Regulatory Liberalization

Government moves to liberalize finance and promote Seoul as a global hub gained momentum by late 2025, with regulatory reforms easing capital flow and expanding offshore license scopes, supporting NH Investment & Securities’ international branches.

Policy changes allowing greater flexibility in offshore operations and FX transactions—reflected in a 12% rise in offshore deal volume in 2024 and a 9% increase in FX trading turnover through H1 2025—boost NH’s regional competitiveness.

These shifts enable NH to better compete with global investment banks in Asia by lowering compliance barriers and facilitating cross-border product distribution.

- Regulatory liberalization accelerated late 2025

- Offshore deal volume +12% in 2024

- FX turnover +9% H1 2025

- Improved cross-border distribution and competitive parity with global banks

Policy boosts Korea capital markets amid export tariff risks and rising trading volumes

Political initiatives like the Corporate Value-up Program (KRW 2.5tn through 2025) and finance liberalization (offshore deals +12% 2024; FX turnover +9% H1 2025) expand NH Investment’s advisory and trading revenue pools, while Korea’s 2024 exports of $644bn and US/China ~36% share raise client vulnerability to tariff shocks; geopolitical risk pushed sovereign CDS to ~40–50bps in 2024, lifting trading volumes +12–18% and stressing cross-border deal flow (FDI -6% 2024).

| Metric | Value (2024/2025) |

|---|---|

| Corporate Value-up Fund | KRW 2.5tn |

| Goods exports | $644bn |

| US+China export share | ~36% |

| Sovereign CDS (peak) | ~40–50bps |

| Trading volume change | +12–18% |

| Offshore deal vol | +12% (2024) |

| FX turnover | +9% H1 2025 |

| FDI inflows | -6% YoY (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect NH Investment & Securities across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights tailored for executives, investors, and consultants to identify actionable risks and opportunities in its region and industry.

Condenses NH Investment & Securities' PESTLE into a concise, shareable brief—visually segmented by category and written in plain language—so teams can quickly align on external risks, market positioning, and strategic actions during meetings or client presentations.

Economic factors

Interest Rate Environment and Monetary Policy

Bank of Korea’s end-2025 policy rate largely determines NH Investment & Securities’ fixed-income and wealth management results; with the BOK holding 2024 rates at 3.50% then signaling cuts to ~3.00% by late 2025, bond yields and duration risk compress, lifting bond prices and boosting AUM performance.

Domestic Economic Growth and Consumption

South Korea's GDP grew 1.8% in 2024 after 2.6% in 2023, and household consumption slowed to a 2024 real growth near 1.0%, constraining retail investment inflows into brokerage and wealth products.

Economic stagnation and muted wage growth—real wage change ~0–1% in 2024—reduce new capital into NH Investment accounts, lowering fee and AUM growth prospects.

NH Investment should shift toward low-cost, income-generating products and digital advisory suited to risk-averse retail sentiment and subdued consumption.

Currency Exchange Rate Volatility

The strength of the Korean Won against the US Dollar is critical for NH Investment’s international asset management and brokerage; in 2024 the KRW appreciated ~3.5% vs USD year-to-date, directly altering USD-denominated returns for domestic clients.

Exchange-rate fluctuations influence client demand for global market access—NH reported 18% of AUM in offshore assets in 2024, prompting shifts in product flows.

The firm employs dynamic hedging—forward contracts and cross-currency swaps—reducing currency P&L volatility; hedging coverage reached ~65% of offshore exposure in 2024.

Capital Market Liquidity Trends

Capital market liquidity in KOSPI/KOSDAQ directly affects NH Investment’s ability to execute large institutional orders; average daily turnover on KOSPI reached about KRW 12.4 trillion and KOSDAQ KRW 5.1 trillion in 2024, enabling tighter spreads and greater commission income during high-liquidity periods.

The firm tracks liquidity cycles—2023–2025 saw volatility spikes that widened spreads but 2024 market-wide ADV gains improved market-making profitability and supported proprietary trading deployment strategies.

- 2024 KOSPI ADV ~KRW 12.4T; KOSDAQ ADV ~KRW 5.1T

- Higher liquidity → tighter spreads ↑ commission revenue

- Monitors cycles to time market-making and prop trades

Inflationary Pressures and Asset Valuation

Persistent or volatile inflation alters real returns across NH Investment & Securities' portfolios; South Korea's CPI rose 2.5% in 2025 vs 3.7% in 2024, compressing real yields on nominal bonds and equities.

Higher inflation shifts client demand toward commodities, real estate and inflation-linked bonds—Korean CPI-linked bond issuance grew ~18% YoY in 2024—prompting reweighting away from traditional fixed income.

NH Investment's research and allocation teams must adjust strategies, offering TIPS-like products, real assets and dynamic inflation-hedging overlays to preserve purchasing power.

- Inflation: Korea CPI 3.7% (2024), 2.5% (2025 est)

- Asset flows: CPI-linked bond issuance +18% YoY (2024)

- Strategy: increased allocation to real assets and inflation-linked instruments

BOK easing lifts bond prices & AUM; modest growth, softer CPI, KRW up

BOK rate path (3.50% in 2024 → ~3.00% by late‑2025) compresses yields, boosting bond prices and AUM; 2024 GDP 1.8% and household consumption ~1.0% constrain retail inflows; KRW appreciated ~3.5% YTD 2024 with 18% AUM offshore and ~65% hedging coverage; KOSPI/KOSDAQ ADV 12.4T/5.1T KRW (2024); CPI 3.7% (2024) → 2.5% (2025 est), CPI‑linked issuance +18% YoY (2024).

| Metric | 2024 | 2025 est |

|---|---|---|

| BOK rate | 3.50% | ~3.00% |

| GDP growth | 1.8% | - |

| CPI | 3.7% | 2.5% |

| KOSPI/KOSDAQ ADV | 12.4T / 5.1T KRW | - |

Same Document Delivered

NH Investment & Securities PESTLE Analysis

The preview shown here is the exact NH Investment & Securities PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.