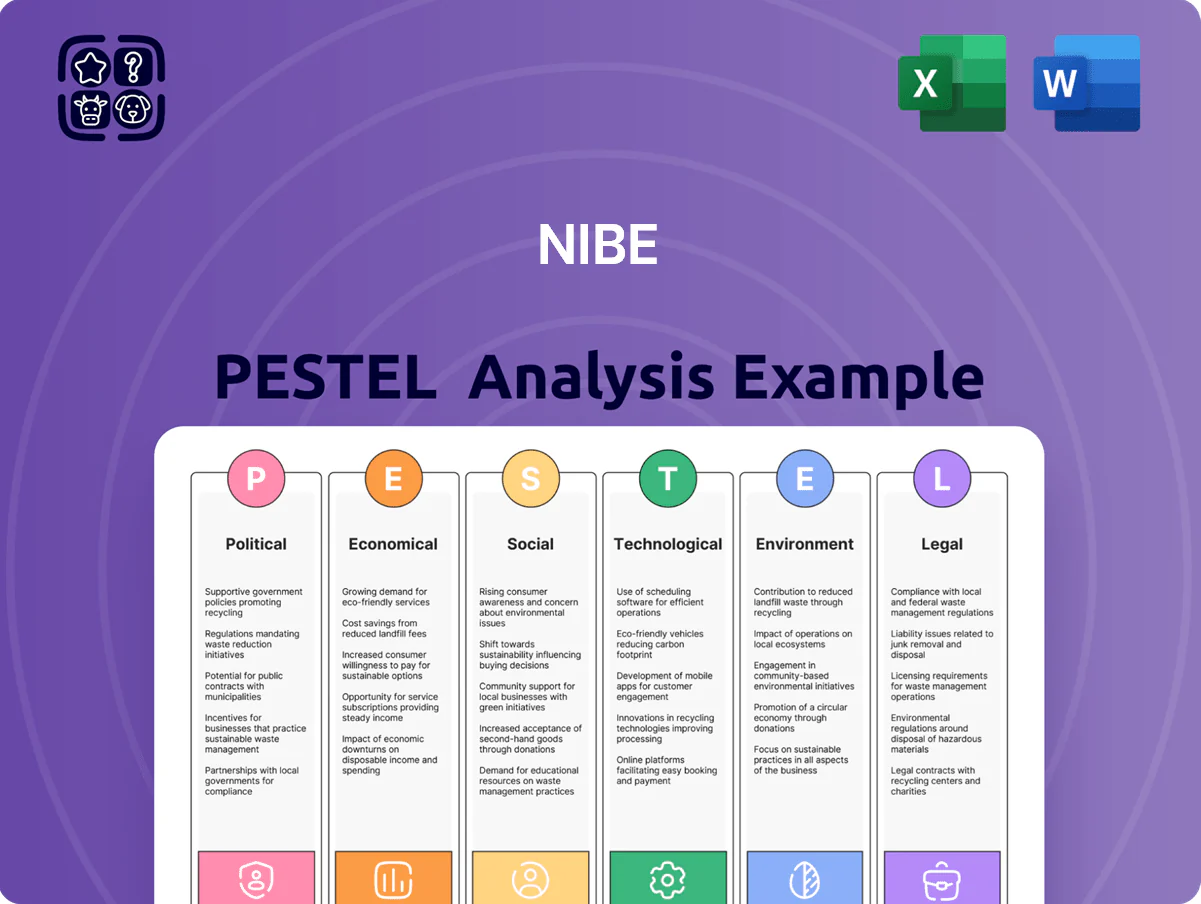

NIBE PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and sustainability trends are reshaping NIBE’s strategic outlook—our concise PESTLE highlights the external forces that matter most to investors and planners; purchase the full analysis for a detailed, actionable roadmap you can use immediately.

Political factors

EU Green Deal and REPowerEU alignment

NIBE is a primary beneficiary of the EU Green Deal and REPowerEU, with policies targeting a 55% reduction in GHG emissions by 2030 driving heat-pump adoption; EU member states allocated over EUR 210 billion under REPowerEU by 2024 to accelerate electrification. By end-2025 REPowerEU measures accelerated phase-out of gas boilers, lifting EU heat pump installations to ~19 million units (2021–2025 cumulative est.). This policy alignment supports a stable long-term European demand, with market forecasts projecting 8–10% CAGR for heat pumps through 2030, underpinning NIBE’s revenue visibility.

Geopolitical trade tensions and supply chain security

Ongoing trade friction between EU, US and China raises tariff risk, prompting NIBE to expand manufacturing beyond Sweden—production outside EU grew to 28% in 2024 from 21% in 2021 to diversify exposure. Political instability in Eastern Europe and Asian trade barriers increased localization spend, with capex on European plants up 18% YoY to SEK 1.4bn in 2024. EU push for strategic autonomy in heat pump components has shifted procurement toward local suppliers, reducing non-EU sourcing to 12% of purchases in 2025.

National subsidy fluctuations and fiscal policy

Energy security and independence initiatives

National security concerns over energy sovereignty are boosting political support for heat pumps; EU member states targeted a 40% reduction in gas imports by 2030 (European Commission, 2024), accelerating electrified heating adoption.

Governments view electrified heating as a hedge against external price shocks—2022–2024 saw EU wholesale gas prices spike by over 300% at peak—making NIBE’s heat-pump systems strategic for resilience.

NIBE’s products are framed as critical infrastructure: public procurement and incentives expanded—e.g., Sweden’s 2024 heat-pump subsidy lift to €600M—positioning NIBE for increased demand.

- EU gas import cut target 40% by 2030 (EC 2024)

- EU gas price spikes >300% in 2022–24

- Sweden 2024 heat-pump subsidies ~€600M

- NIBE positioned as critical infrastructure supplier

Global expansion and local regulatory diplomacy

As NIBE expands in North America and Asia, navigating protectionist Buy Local rules and differing standards is critical; U.S. tariffs and state-level procurement rules can affect margins as 2024 U.S. heat-pump incentives (Inflation Reduction Act extensions) drove residential demand up ~20% YoY.

Continuation of federal climate tax incentives remains a key driver for NIBE’s Climate Solutions, with U.S. clean-energy tax credits supporting heat-pump adoption and an estimated $10–20k homeowner incentive range in many states.

Building strong ties with regional authorities mitigates political-shift risks—local partnerships and compliance programs reduce project delays and have cut permit timelines by up to 30% in pilot markets.

- Monitor Buy Local policies and tariffs

- Leverage U.S. climate incentives (IRA extensions) to boost sales

- Invest in regional regulatory teams to lower permit/delay risk

EU Green Deal Fuels 8–10% Heat-Pump Growth; Supply Shifts, Tariffs & Subsidy Cuts Bite

Policy support from EU Green Deal/REPowerEU and national incentives (EUR 210bn REPowerEU by 2024; Sweden €600M 2024) underpins ~8–10% heat-pump CAGR to 2030; trade frictions/tariffs raised non-EU sourcing cut to 12% (2025) and production abroad to 28% (2024); national subsidy shifts (−15–40% 2023–25) slowed adoption 5–12%; EU gas import cut target 40% by 2030 (EC 2024).

| Metric | Value |

|---|---|

| REPowerEU funding (2024) | EUR 210bn |

| Sweden heat-pump subsidy (2024) | €600M |

| Non-EU procurement (2025) | 12% |

| Production outside EU (2024) | 28% |

| EU gas import target (2030) | −40% |

What is included in the product

Explores how external macro-environmental factors uniquely affect NIBE across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities.

A concise, visually segmented NIBE PESTLE summary that’s easy to drop into presentations or share across teams, helping clarify external risks and market positioning for faster, aligned decision-making.

Economic factors

Interest rate cycles and construction activity

Stabilization and easing of interest rates by late 2025—with OECD policy rates falling from peaks near 4.5% in 2023 to ~3.0% projected—boosts residential construction and renovations, lifting global housing starts (2024: ~100 million units annualized) and mortgage origination. Lower borrowing costs improve affordability of high-capex systems like heat pumps, reducing payback periods by an estimated 20–30%. NIBE’s revenue growth remains tightly tied to real estate health and mortgage availability, with circa 2024 housing market correlations exceeding 0.6 in key markets.

Energy price volatility and consumer ROI

The widening price delta between electricity and natural gas drives NIBE demand: in EU Q4 2025 average gas prices were ~80 EUR/MWh vs power at ~120 EUR/MWh, making heat pumps more attractive and shortening payback to ~4–7 years versus 8–12 years when gas is cheap.

Inflationary pressure on raw materials

Fluctuations in copper, aluminum and steel prices squeezed NIBE’s margins in 2023–24; copper rose ~45% YoY in 2023 before receding, and steel input costs were ~12% above 2021 levels by mid‑2024. Inflationary pressures had moderated by late 2025, but NIBE needs pricing power to pass through residual increases; robust supply‑chain management and hedging helped keep Group adjusted operating margin near 10–11% in 2024–25.

Currency exchange rate fluctuations

NIBE reports in SEK and faces translation and transaction exposure from EUR and USD flows; in 2024 roughly 40–50% of sales were foreign-currency denominated, amplifying FX impact on consolidated EBIT.

Between 2023–2025 the SEK moved about 6–8% vs the EUR and 10–12% vs the USD at times, altering export competitiveness and translating to multi‑million SEK swings in reported earnings.

Managing this volatility requires hedging, net‑currency positions and pricing strategies to protect margins and shareholder returns.

- ~40–50% sales FX exposure

- SEK swing vs EUR ~6–8%, vs USD ~10–12% (2023–2025)

- Hedging and pricing needed to stabilize multi‑million SEK earnings effects

Labor market constraints and wage inflation

The shortage of skilled installers and technicians remains a bottleneck for the heat pump industry; in Europe there were an estimated 120,000 HVAC installer vacancies in 2024, constraining deployment rates and after-sales service for NIBE.

Rising labor costs—wage inflation averaging 4.2% in Nordic engineering sectors in 2024—and competition for engineering talent increase NIBE’s OPEX and distributor margins, pressuring gross margins.

Investment in training and automation is required: NIBE’s reported 2024 capex of SEK 1.8bn and expanding training programs aim to offset labor tightness and boost installer productivity.

- 120,000 HVAC installer vacancies in Europe (2024)

- Nordic engineering wage inflation ~4.2% (2024)

- NIBE capex SEK 1.8bn (2024) targeting automation and training

Lower rates, EU power/gas gap and housing surge boost heat‑pump demand amid cost, FX pressure

Easing rates to ~3% by late‑2025, housing starts ~100m units (2024), and electricity vs gas spread (EU Q4 2025: power ~120 EUR/MWh, gas ~80 EUR/MWh) accelerate heat‑pump demand; input cost volatility (copper +45% in 2023; steel +12% vs 2021) and FX (40–50% sales FX exposure; SEK vs EUR 6–8%, vs USD 10–12% in 2023–25) pressure margins, mitigated by SEK 1.8bn capex and hiring/training.

| Metric | Value |

|---|---|

| Policy rate (OECD) 2025 | ~3.0% |

| Housing starts (2024) | ~100m units |

| EU power/gas (Q4 2025) | 120/80 EUR/MWh |

| Copper change (2023) | +45% YoY |

| Steel vs 2021 (mid‑2024) | +12% |

| FX sales exposure (2024) | 40–50% |

| SEK swings (2023–25) | EUR 6–8%, USD 10–12% |

| NIBE capex (2024) | SEK 1.8bn |

Preview Before You Purchase

NIBE PESTLE Analysis

The preview shown here is the exact NIBE PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or surprises. What you see in the preview is the real, final file you’ll be able to download immediately after payment, with identical layout, content, and structure for direct use in analysis or presentations.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and sustainability trends are reshaping NIBE’s strategic outlook—our concise PESTLE highlights the external forces that matter most to investors and planners; purchase the full analysis for a detailed, actionable roadmap you can use immediately.

Political factors

EU Green Deal and REPowerEU alignment

NIBE is a primary beneficiary of the EU Green Deal and REPowerEU, with policies targeting a 55% reduction in GHG emissions by 2030 driving heat-pump adoption; EU member states allocated over EUR 210 billion under REPowerEU by 2024 to accelerate electrification. By end-2025 REPowerEU measures accelerated phase-out of gas boilers, lifting EU heat pump installations to ~19 million units (2021–2025 cumulative est.). This policy alignment supports a stable long-term European demand, with market forecasts projecting 8–10% CAGR for heat pumps through 2030, underpinning NIBE’s revenue visibility.

Geopolitical trade tensions and supply chain security

Ongoing trade friction between EU, US and China raises tariff risk, prompting NIBE to expand manufacturing beyond Sweden—production outside EU grew to 28% in 2024 from 21% in 2021 to diversify exposure. Political instability in Eastern Europe and Asian trade barriers increased localization spend, with capex on European plants up 18% YoY to SEK 1.4bn in 2024. EU push for strategic autonomy in heat pump components has shifted procurement toward local suppliers, reducing non-EU sourcing to 12% of purchases in 2025.

National subsidy fluctuations and fiscal policy

Energy security and independence initiatives

National security concerns over energy sovereignty are boosting political support for heat pumps; EU member states targeted a 40% reduction in gas imports by 2030 (European Commission, 2024), accelerating electrified heating adoption.

Governments view electrified heating as a hedge against external price shocks—2022–2024 saw EU wholesale gas prices spike by over 300% at peak—making NIBE’s heat-pump systems strategic for resilience.

NIBE’s products are framed as critical infrastructure: public procurement and incentives expanded—e.g., Sweden’s 2024 heat-pump subsidy lift to €600M—positioning NIBE for increased demand.

- EU gas import cut target 40% by 2030 (EC 2024)

- EU gas price spikes >300% in 2022–24

- Sweden 2024 heat-pump subsidies ~€600M

- NIBE positioned as critical infrastructure supplier

Global expansion and local regulatory diplomacy

As NIBE expands in North America and Asia, navigating protectionist Buy Local rules and differing standards is critical; U.S. tariffs and state-level procurement rules can affect margins as 2024 U.S. heat-pump incentives (Inflation Reduction Act extensions) drove residential demand up ~20% YoY.

Continuation of federal climate tax incentives remains a key driver for NIBE’s Climate Solutions, with U.S. clean-energy tax credits supporting heat-pump adoption and an estimated $10–20k homeowner incentive range in many states.

Building strong ties with regional authorities mitigates political-shift risks—local partnerships and compliance programs reduce project delays and have cut permit timelines by up to 30% in pilot markets.

- Monitor Buy Local policies and tariffs

- Leverage U.S. climate incentives (IRA extensions) to boost sales

- Invest in regional regulatory teams to lower permit/delay risk

EU Green Deal Fuels 8–10% Heat-Pump Growth; Supply Shifts, Tariffs & Subsidy Cuts Bite

Policy support from EU Green Deal/REPowerEU and national incentives (EUR 210bn REPowerEU by 2024; Sweden €600M 2024) underpins ~8–10% heat-pump CAGR to 2030; trade frictions/tariffs raised non-EU sourcing cut to 12% (2025) and production abroad to 28% (2024); national subsidy shifts (−15–40% 2023–25) slowed adoption 5–12%; EU gas import cut target 40% by 2030 (EC 2024).

| Metric | Value |

|---|---|

| REPowerEU funding (2024) | EUR 210bn |

| Sweden heat-pump subsidy (2024) | €600M |

| Non-EU procurement (2025) | 12% |

| Production outside EU (2024) | 28% |

| EU gas import target (2030) | −40% |

What is included in the product

Explores how external macro-environmental factors uniquely affect NIBE across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities.

A concise, visually segmented NIBE PESTLE summary that’s easy to drop into presentations or share across teams, helping clarify external risks and market positioning for faster, aligned decision-making.

Economic factors

Interest rate cycles and construction activity

Stabilization and easing of interest rates by late 2025—with OECD policy rates falling from peaks near 4.5% in 2023 to ~3.0% projected—boosts residential construction and renovations, lifting global housing starts (2024: ~100 million units annualized) and mortgage origination. Lower borrowing costs improve affordability of high-capex systems like heat pumps, reducing payback periods by an estimated 20–30%. NIBE’s revenue growth remains tightly tied to real estate health and mortgage availability, with circa 2024 housing market correlations exceeding 0.6 in key markets.

Energy price volatility and consumer ROI

The widening price delta between electricity and natural gas drives NIBE demand: in EU Q4 2025 average gas prices were ~80 EUR/MWh vs power at ~120 EUR/MWh, making heat pumps more attractive and shortening payback to ~4–7 years versus 8–12 years when gas is cheap.

Inflationary pressure on raw materials

Fluctuations in copper, aluminum and steel prices squeezed NIBE’s margins in 2023–24; copper rose ~45% YoY in 2023 before receding, and steel input costs were ~12% above 2021 levels by mid‑2024. Inflationary pressures had moderated by late 2025, but NIBE needs pricing power to pass through residual increases; robust supply‑chain management and hedging helped keep Group adjusted operating margin near 10–11% in 2024–25.

Currency exchange rate fluctuations

NIBE reports in SEK and faces translation and transaction exposure from EUR and USD flows; in 2024 roughly 40–50% of sales were foreign-currency denominated, amplifying FX impact on consolidated EBIT.

Between 2023–2025 the SEK moved about 6–8% vs the EUR and 10–12% vs the USD at times, altering export competitiveness and translating to multi‑million SEK swings in reported earnings.

Managing this volatility requires hedging, net‑currency positions and pricing strategies to protect margins and shareholder returns.

- ~40–50% sales FX exposure

- SEK swing vs EUR ~6–8%, vs USD ~10–12% (2023–2025)

- Hedging and pricing needed to stabilize multi‑million SEK earnings effects

Labor market constraints and wage inflation

The shortage of skilled installers and technicians remains a bottleneck for the heat pump industry; in Europe there were an estimated 120,000 HVAC installer vacancies in 2024, constraining deployment rates and after-sales service for NIBE.

Rising labor costs—wage inflation averaging 4.2% in Nordic engineering sectors in 2024—and competition for engineering talent increase NIBE’s OPEX and distributor margins, pressuring gross margins.

Investment in training and automation is required: NIBE’s reported 2024 capex of SEK 1.8bn and expanding training programs aim to offset labor tightness and boost installer productivity.

- 120,000 HVAC installer vacancies in Europe (2024)

- Nordic engineering wage inflation ~4.2% (2024)

- NIBE capex SEK 1.8bn (2024) targeting automation and training

Lower rates, EU power/gas gap and housing surge boost heat‑pump demand amid cost, FX pressure

Easing rates to ~3% by late‑2025, housing starts ~100m units (2024), and electricity vs gas spread (EU Q4 2025: power ~120 EUR/MWh, gas ~80 EUR/MWh) accelerate heat‑pump demand; input cost volatility (copper +45% in 2023; steel +12% vs 2021) and FX (40–50% sales FX exposure; SEK vs EUR 6–8%, vs USD 10–12% in 2023–25) pressure margins, mitigated by SEK 1.8bn capex and hiring/training.

| Metric | Value |

|---|---|

| Policy rate (OECD) 2025 | ~3.0% |

| Housing starts (2024) | ~100m units |

| EU power/gas (Q4 2025) | 120/80 EUR/MWh |

| Copper change (2023) | +45% YoY |

| Steel vs 2021 (mid‑2024) | +12% |

| FX sales exposure (2024) | 40–50% |

| SEK swings (2023–25) | EUR 6–8%, USD 10–12% |

| NIBE capex (2024) | SEK 1.8bn |

Preview Before You Purchase

NIBE PESTLE Analysis

The preview shown here is the exact NIBE PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or surprises. What you see in the preview is the real, final file you’ll be able to download immediately after payment, with identical layout, content, and structure for direct use in analysis or presentations.