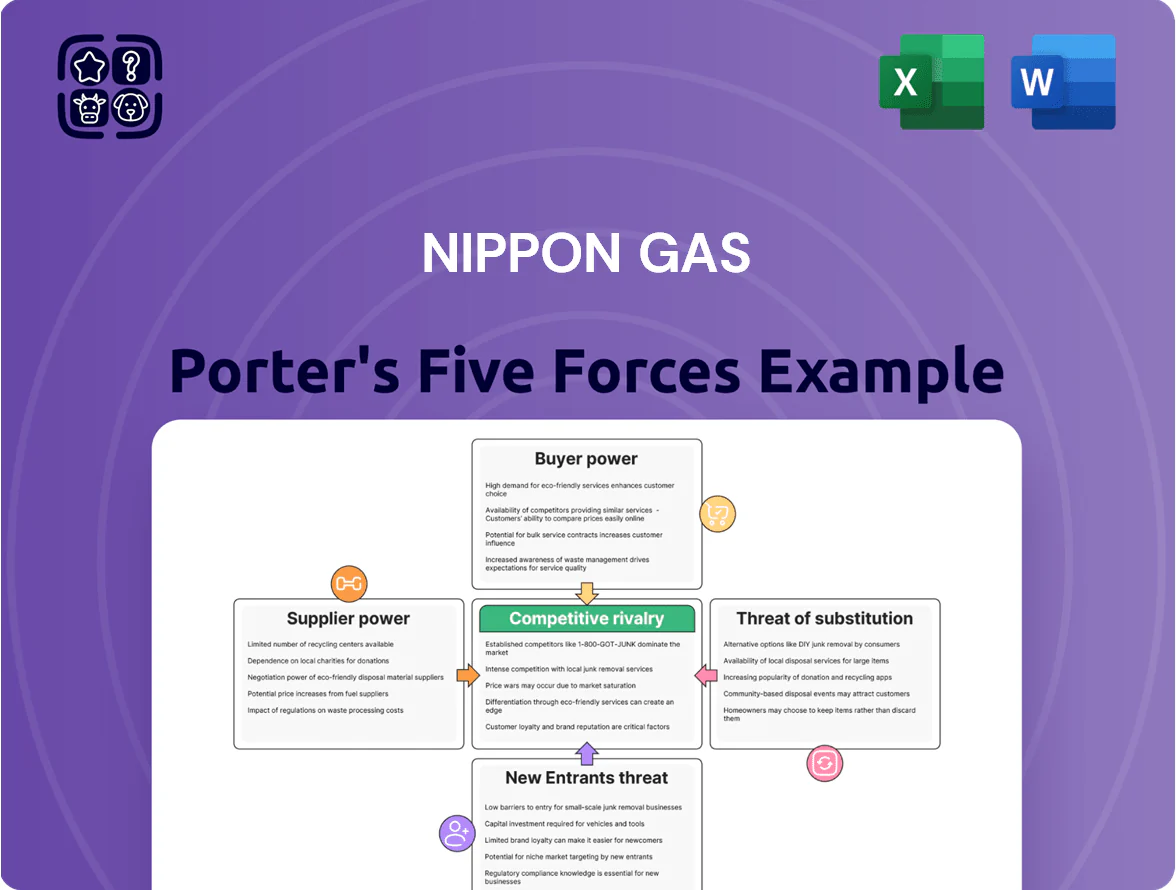

Nippon Gas Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Nippon Gas faces moderate supplier power, regulated barriers, and evolving substitute threats from renewables, shaping a competitive yet stable market landscape that warrants deeper scrutiny.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nippon Gas’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global Commodity Market Volatility

NICIGAS depends on international LPG imports and acts as a price taker in a market where 2025 Saudi Aramco contract-price swings of ±12% and North American propane index moves of ±18% have raised procurement costs by about ¥8–12 billion in FY2024.

Dependency on Wholesale City Gas Infrastructure

As a retail city gas provider, NICIGAS sources over 70% of its wholesale volumes from major infrastructure owners like Tokyo Gas, creating clear supplier leverage over pipeline access and pricing (Tokyo Gas 2024 annual report: ¥1.2TR infrastructure revenue).

This dependency means Tokyo Gas and peers set tariff pass-throughs and capacity charges, constraining NICIGAS’s ability to expand retail margins when wholesale spot prices spiked 48% in 2022–23.

The relationship is symbiotic—NICIGAS relies on stable delivery while suppliers secure steady off-take—but limits NICIGAS’s pricing flexibility and increases margin volatility during supply-cost shocks.

Power Generation Procurement Mix

NICIGAS sources retail electricity via the Japan Electric Power Exchange (JEPX) and bilateral contracts with generators, exposing it to spot volatility; JEPX average wholesale price hit about ¥27.5/kWh in 2024, up ~22% vs 2022.

High LNG and coal costs—Japan LNG import price averaged $12.8/MMBtu in 2024—pushed generation costs and wholesale prices higher, squeezing NICIGAS margins.

Without significant proprietary generation or LNG upstream assets, NICIGAS lacks leverage, raising suppliers’ bargaining power and contract reliance.

Logistics and IoT Equipment Providers

Suppliers of smart meters and IoT devices hold moderate power for Nippon Gas because digital transformation drives demand; global smart meter shipments reached about 220 million units in 2024, so vendor choice matters.

Multiple vendors exist, but NICIGAS Stream proprietary software creates technical dependency on compatible hardware, raising switching costs and integration spend (estimated 5–8% of annual IT capex in 2024).

Steady supply of sensors and modules is critical: semiconductor shortages in 2021–23 raised component lead times to 20–30 weeks, so supplier reliability directly affects operational uptime and rollout pace.

- Moderate supplier power due to high digital demand

- Proprietary software ties to specific hardware partners

- Integration costs ~5–8% of IT capex (2024)

- Component lead times spiked to 20–30 weeks during 2021–23

Regulatory Compliance and Carbon Credits

Suppliers of carbon credits and offsets gain leverage as Japan targets carbon neutrality by 2050; demand for certified credits rose 38% in 2024, tightening supply and raising NICIGAS’s procurement costs.

NICIGAS must buy high-quality offsets to sell green energy and comply with evolving regulations like Japan’s 2030 NDC updates, pushing operating expenses higher and margin pressure.

Limited supply of vetted offsets—premium prices rose ~45% YoY in 2024—means suppliers can dictate terms, increasing cost volatility for NICIGAS.

- Demand +38% in 2024

- Premium offset prices +45% YoY (2024)

- 2030 NDC tightening raises compliance needs

- Higher OPEX, margin squeeze

Import costs, vendor lock & surging offsets squeeze NICIGAS margins in 2024

Suppliers hold moderate–high power: NICIGAS is import-dependent (LPG/LNG costs added ¥8–12bn in FY2024; Japan LNG price $12.8/MMBtu in 2024) and sources >70% wholesale from infrastructure owners (Tokyo Gas ¥1.2T infra rev 2024), limiting margin control; smart-meter vendor lock raises IT capex 5–8% and carbon-offset prices surged +45% YoY (2024), squeezing OPEX.

| Metric | 2024 value |

|---|---|

| Import cost hit | ¥8–12bn |

| Japan LNG price | $12.8/MMBtu |

| Wholesale sourced | >70% |

| Tokyo Gas infra rev | ¥1.2T |

| IT capex impact | 5–8% |

| Offset price rise | +45% YoY |

What is included in the product

Tailored Porter’s Five Forces for Nippon Gas, uncovering competitive pressures, supplier and buyer bargaining power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

A concise Nippon Gas Porter's Five Forces snapshot that highlights competitive threats and bargaining dynamics—ideal for rapid strategic decisions and investor briefings.

Customers Bargaining Power

Low Switching Costs in Retail Markets

Deregulation in Japan since 2016 for electricity and 2017 for gas cut residential switching barriers, and by 2024 roughly 35% of households had switched electricity suppliers and about 12% switched gas, lowering customer lock-in. Consumers now change suppliers via online portals in minutes with no major technical or financial hurdles. This forces Nippon Gas (NICIGAS) to sustain competitive tariffs—its 2024 average residential margin fell to ~7%—and boost service quality to curb churn.

Price Sensitivity Amid Inflation

With Japan's CPI at 2.5% in 2025 and wholesale LNG spot prices up ~35% vs 2023, households tighten budgets and prioritize utility cuts, raising NICIGAS's customer price sensitivity.

Surveys show 42% of consumers compare bundled energy offers; demand for gas+electricity bundles rises, constraining NICIGAS from fully passing procurement cost hikes to end users.

Demand for Sophisticated Digital Integration

Modern customers expect advanced digital interfaces to monitor energy use and manage billing in real time; global energy app adoption rose 27% in 2024, and Japanese utility app retention averages 42% after 90 days. NICIGAS’s ¥3.2 billion 2023–2025 digital transformation spend, including its mobile app rollout in 2024, directly answers demand for transparency. Poor UX risks immediate churn—industry churn rises 1.8 percentage points when billing tools underperform.

Commercial Volume Negotiations

Large commercial and industrial clients hold strong bargaining power at Nippon Gas (NICIGAS) due to consuming up to 40–60% of regional piped gas volumes per site, driving aggressive competitive bidding and requests for bespoke tariffs to cut operating costs.

To retain these high-value accounts NICIGAS must provide tailored pricing, energy-saving services (e.g., cogeneration, heat recovery) and SLAs; losing a single mega-client can shave 2–5% off annual revenue.

- Top clients consume 40–60% site volume

- Competitive bids force bespoke tariffs

- Value-add services (cogen, heat recovery) needed

- Single mega-client loss = ~2–5% revenue hit

Influence of Environmental Awareness

- 34% of buyers prefer carbon-neutral suppliers (2025)

- 62% demand emissions transparency (2024 survey)

- Renewables share in offers +18% YoY (2024)

Rising switching, margin squeeze and carbon demand threaten gas revenues

Customer bargaining is high: residential switching rose to ~12% for gas by 2024, NICIGAS’s 2024 residential margin fell to ~7%, and price sensitivity rose with CPI 2.5% (2025) and LNG spot +35% vs 2023; C&I clients consume 40–60% per site, risking 2–5% revenue loss if lost; 34% prefer carbon-neutral suppliers (2025) and 62% demand emissions transparency (2024).

| Metric | Value |

|---|---|

| Residential gas switching (2024) | ~12% |

| Residential margin (NICIGAS, 2024) | ~7% |

| LNG spot vs 2023 | +35% |

| CPI (Japan, 2025) | 2.5% |

| Top C&I site consumption | 40–60% |

| Mega-client revenue risk | 2–5% |

| Buyers preferring carbon-neutral (2025) | 34% |

| Demanding emissions transparency (2024) | 62% |

Preview Before You Purchase

Nippon Gas Porter's Five Forces Analysis

This preview shows the exact Nippon Gas Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the same professionally written file you'll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual deliverable: complete, ready-to-use, and available instantly after payment with no further setup required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Nippon Gas faces moderate supplier power, regulated barriers, and evolving substitute threats from renewables, shaping a competitive yet stable market landscape that warrants deeper scrutiny.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nippon Gas’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global Commodity Market Volatility

NICIGAS depends on international LPG imports and acts as a price taker in a market where 2025 Saudi Aramco contract-price swings of ±12% and North American propane index moves of ±18% have raised procurement costs by about ¥8–12 billion in FY2024.

Dependency on Wholesale City Gas Infrastructure

As a retail city gas provider, NICIGAS sources over 70% of its wholesale volumes from major infrastructure owners like Tokyo Gas, creating clear supplier leverage over pipeline access and pricing (Tokyo Gas 2024 annual report: ¥1.2TR infrastructure revenue).

This dependency means Tokyo Gas and peers set tariff pass-throughs and capacity charges, constraining NICIGAS’s ability to expand retail margins when wholesale spot prices spiked 48% in 2022–23.

The relationship is symbiotic—NICIGAS relies on stable delivery while suppliers secure steady off-take—but limits NICIGAS’s pricing flexibility and increases margin volatility during supply-cost shocks.

Power Generation Procurement Mix

NICIGAS sources retail electricity via the Japan Electric Power Exchange (JEPX) and bilateral contracts with generators, exposing it to spot volatility; JEPX average wholesale price hit about ¥27.5/kWh in 2024, up ~22% vs 2022.

High LNG and coal costs—Japan LNG import price averaged $12.8/MMBtu in 2024—pushed generation costs and wholesale prices higher, squeezing NICIGAS margins.

Without significant proprietary generation or LNG upstream assets, NICIGAS lacks leverage, raising suppliers’ bargaining power and contract reliance.

Logistics and IoT Equipment Providers

Suppliers of smart meters and IoT devices hold moderate power for Nippon Gas because digital transformation drives demand; global smart meter shipments reached about 220 million units in 2024, so vendor choice matters.

Multiple vendors exist, but NICIGAS Stream proprietary software creates technical dependency on compatible hardware, raising switching costs and integration spend (estimated 5–8% of annual IT capex in 2024).

Steady supply of sensors and modules is critical: semiconductor shortages in 2021–23 raised component lead times to 20–30 weeks, so supplier reliability directly affects operational uptime and rollout pace.

- Moderate supplier power due to high digital demand

- Proprietary software ties to specific hardware partners

- Integration costs ~5–8% of IT capex (2024)

- Component lead times spiked to 20–30 weeks during 2021–23

Regulatory Compliance and Carbon Credits

Suppliers of carbon credits and offsets gain leverage as Japan targets carbon neutrality by 2050; demand for certified credits rose 38% in 2024, tightening supply and raising NICIGAS’s procurement costs.

NICIGAS must buy high-quality offsets to sell green energy and comply with evolving regulations like Japan’s 2030 NDC updates, pushing operating expenses higher and margin pressure.

Limited supply of vetted offsets—premium prices rose ~45% YoY in 2024—means suppliers can dictate terms, increasing cost volatility for NICIGAS.

- Demand +38% in 2024

- Premium offset prices +45% YoY (2024)

- 2030 NDC tightening raises compliance needs

- Higher OPEX, margin squeeze

Import costs, vendor lock & surging offsets squeeze NICIGAS margins in 2024

Suppliers hold moderate–high power: NICIGAS is import-dependent (LPG/LNG costs added ¥8–12bn in FY2024; Japan LNG price $12.8/MMBtu in 2024) and sources >70% wholesale from infrastructure owners (Tokyo Gas ¥1.2T infra rev 2024), limiting margin control; smart-meter vendor lock raises IT capex 5–8% and carbon-offset prices surged +45% YoY (2024), squeezing OPEX.

| Metric | 2024 value |

|---|---|

| Import cost hit | ¥8–12bn |

| Japan LNG price | $12.8/MMBtu |

| Wholesale sourced | >70% |

| Tokyo Gas infra rev | ¥1.2T |

| IT capex impact | 5–8% |

| Offset price rise | +45% YoY |

What is included in the product

Tailored Porter’s Five Forces for Nippon Gas, uncovering competitive pressures, supplier and buyer bargaining power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

A concise Nippon Gas Porter's Five Forces snapshot that highlights competitive threats and bargaining dynamics—ideal for rapid strategic decisions and investor briefings.

Customers Bargaining Power

Low Switching Costs in Retail Markets

Deregulation in Japan since 2016 for electricity and 2017 for gas cut residential switching barriers, and by 2024 roughly 35% of households had switched electricity suppliers and about 12% switched gas, lowering customer lock-in. Consumers now change suppliers via online portals in minutes with no major technical or financial hurdles. This forces Nippon Gas (NICIGAS) to sustain competitive tariffs—its 2024 average residential margin fell to ~7%—and boost service quality to curb churn.

Price Sensitivity Amid Inflation

With Japan's CPI at 2.5% in 2025 and wholesale LNG spot prices up ~35% vs 2023, households tighten budgets and prioritize utility cuts, raising NICIGAS's customer price sensitivity.

Surveys show 42% of consumers compare bundled energy offers; demand for gas+electricity bundles rises, constraining NICIGAS from fully passing procurement cost hikes to end users.

Demand for Sophisticated Digital Integration

Modern customers expect advanced digital interfaces to monitor energy use and manage billing in real time; global energy app adoption rose 27% in 2024, and Japanese utility app retention averages 42% after 90 days. NICIGAS’s ¥3.2 billion 2023–2025 digital transformation spend, including its mobile app rollout in 2024, directly answers demand for transparency. Poor UX risks immediate churn—industry churn rises 1.8 percentage points when billing tools underperform.

Commercial Volume Negotiations

Large commercial and industrial clients hold strong bargaining power at Nippon Gas (NICIGAS) due to consuming up to 40–60% of regional piped gas volumes per site, driving aggressive competitive bidding and requests for bespoke tariffs to cut operating costs.

To retain these high-value accounts NICIGAS must provide tailored pricing, energy-saving services (e.g., cogeneration, heat recovery) and SLAs; losing a single mega-client can shave 2–5% off annual revenue.

- Top clients consume 40–60% site volume

- Competitive bids force bespoke tariffs

- Value-add services (cogen, heat recovery) needed

- Single mega-client loss = ~2–5% revenue hit

Influence of Environmental Awareness

- 34% of buyers prefer carbon-neutral suppliers (2025)

- 62% demand emissions transparency (2024 survey)

- Renewables share in offers +18% YoY (2024)

Rising switching, margin squeeze and carbon demand threaten gas revenues

Customer bargaining is high: residential switching rose to ~12% for gas by 2024, NICIGAS’s 2024 residential margin fell to ~7%, and price sensitivity rose with CPI 2.5% (2025) and LNG spot +35% vs 2023; C&I clients consume 40–60% per site, risking 2–5% revenue loss if lost; 34% prefer carbon-neutral suppliers (2025) and 62% demand emissions transparency (2024).

| Metric | Value |

|---|---|

| Residential gas switching (2024) | ~12% |

| Residential margin (NICIGAS, 2024) | ~7% |

| LNG spot vs 2023 | +35% |

| CPI (Japan, 2025) | 2.5% |

| Top C&I site consumption | 40–60% |

| Mega-client revenue risk | 2–5% |

| Buyers preferring carbon-neutral (2025) | 34% |

| Demanding emissions transparency (2024) | 62% |

Preview Before You Purchase

Nippon Gas Porter's Five Forces Analysis

This preview shows the exact Nippon Gas Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the same professionally written file you'll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual deliverable: complete, ready-to-use, and available instantly after payment with no further setup required.