Nichols PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and technological change are shaping Nichols's prospects in our concise PESTLE snapshot—perfect for investors and strategists who need quick, actionable context. Purchase the full PESTLE analysis to unlock detailed risk assessments, regulatory impacts, and growth opportunities, delivered in editable formats for immediate use.

Political factors

Middle East Trade Relations

Nichols' Vimto holds a dominant share in Gulf markets, driving over 40% of the firm's export revenues in 2024, with Ramadan sales often boosting regional volumes by 25–35% year-on-year.

Geopolitical stability across the GCC is critical: disruptions in 2022–24 showed supply-chain delays that trimmed export volumes by an estimated 8–12% in affected quarters.

Shifts in UK–Middle East trade policy or diplomatic ties could therefore materially affect Nichols' most profitable international segment, risking revenue volatility and higher logistics costs.

UK Government Health Initiatives

The UK government targets high-sugar drinks through measures like the Soft Drinks Industry Levy, which raised £400m in 2023, and updated guidance on promotions and on-shelf placement affecting Nichols' market of UK adult soft drinks (worth ~£6.5bn in 2024).

Nichols must adapt marketing and reformulation strategies as guidelines tighten; Public Health England and DHSC recommendations press for sugar reduction targets—some voluntary codes since 2019 pushed manufacturers to cut sugar by up to 20%-30% in certain categories.

Political pressure to reduce obesity risks further mandatory codes or stricter advertising/placement rules, posing potential compliance costs and reformulation capex that could impact Nichols' margins and product pricing in the domestic market.

Post-Brexit Trade Agreements

As of end-2025, UK trade deals beyond the EU—covering 60+ preferential agreements—continue to reshape Nichols’ sourcing: 12% of cane sugar and 18% of packaging inputs now come from non-EU partners, altering input cost structures. Tariff shifts and new customs procedures have changed landed costs by up to 4–6% in key emerging markets, squeezing margins on exports. Nichols must stay agile to capture tariff-free access while absorbing an estimated £2–3m annual compliance overhead from increased paperwork and rules-of-origin checks.

Geopolitical Stability in African Markets

- Watch: currency volatility >12% (2023–24)

- Focus markets: Nigeria, South Africa, Kenya

- Benefit: 18% faster entry via local partners (2022–24)

Taxation and Fiscal Policy

Changes in UK corporation tax—from 19% in 2023 to 25% for profits over £250k in 2024—would materially affect Nichols PLC margins, while proposals for environmental levies (e.g., estimated £10–£30/tonne carbon pricing scenarios) could raise production costs across its soft-drinks operations.

Business rate reforms and capital allowances adjustments influence planned CAPEX for Nichols’ UK manufacturing and distribution sites; a 2024 relief extension or increased investment allowances could accelerate £10–£50m facility upgrades.

Continuous monitoring of fiscal policy is vital for long-term planning and shareholder value: sensitivity analyses on tax and levy changes should be incorporated into DCF models and earnings-per-share forecasts.

- Corporation tax rise to 25% for large profits

- Potential carbon/environmental levies £10–£30/tonne

- Business rate reforms and capital allowance impacts on £10–£50m CAPEX

- Incorporate tax scenarios into DCF and EPS sensitivity

Nichols faces GCC export dependence, UK levy costs, higher trade fees and tax squeeze

Political risks for Nichols include GCC geopolitical stability affecting >40% export revenue (Ramadan +25–35% sales), UK regulatory pressure (Soft Drinks Industry Levy raised £400m in 2023; UK adult soft drinks market ~£6.5bn in 2024) forcing reformulation capex, trade-policy shifts changing landed costs by 4–6% and £2–3m compliance overhead, and fiscal changes (corporation tax 25%) impacting margins.

| Risk | Key data |

|---|---|

| GCC exports | >40% revenues; Ramadan +25–35% |

| UK levy | £400m raised (2023); market £6.5bn (2024) |

| Trade costs | +4–6% landed; £2–3m compliance |

| Tax | Corp tax 25% |

What is included in the product

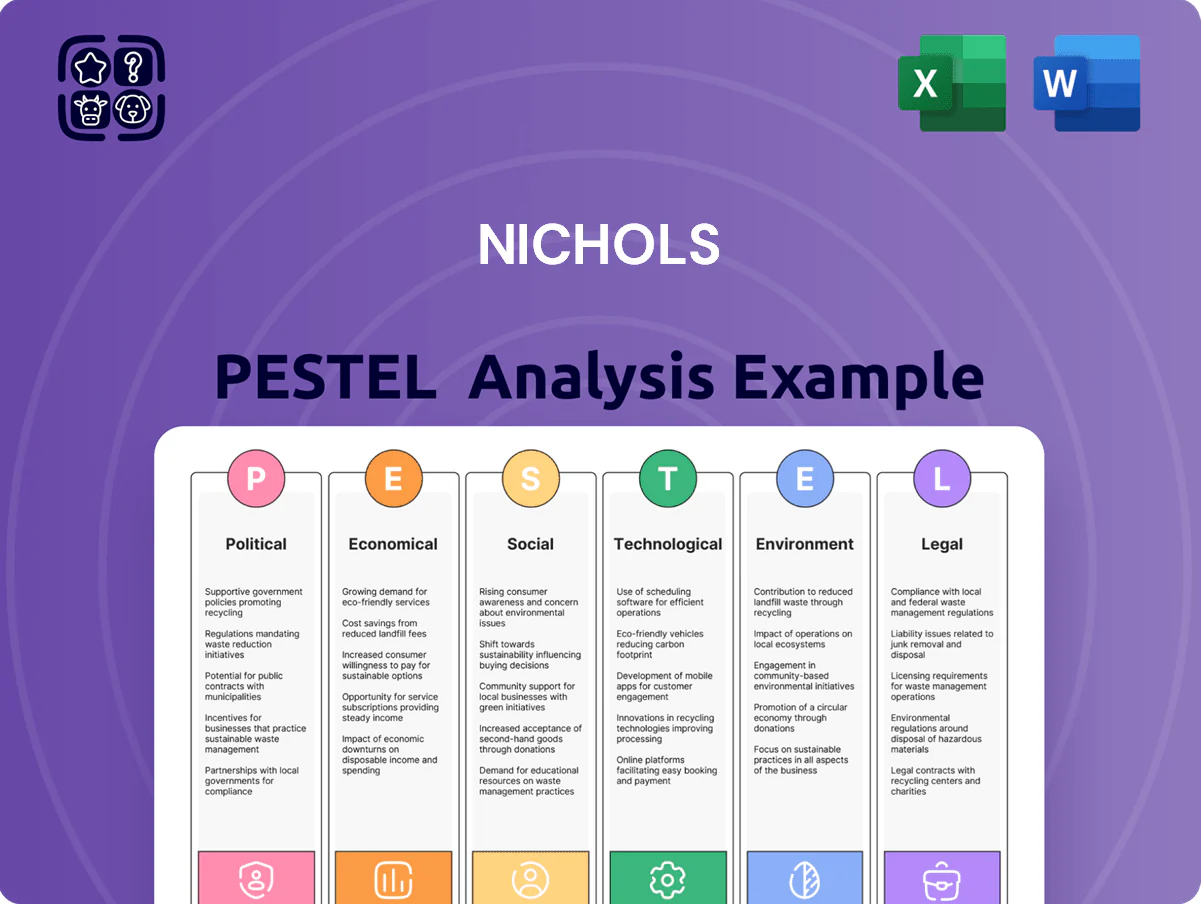

Explores how external macro-environmental factors uniquely affect the Nichols across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Nichols' full PESTLE into a clean, presentation-ready summary that’s visually segmented by factor, easily editable for local context, and instantly shareable for quick team alignment during planning or client briefings.

Economic factors

Commodity Price Volatility

Commodity price volatility—sugar, fruit concentrates and CO2—raises input-cost risk for Nichols as global sugar prices rose ~18% in 2023 and CO2 shortages pushed European spot prices up over 40% in 2022–24; climate shocks amplify supply-side volatility.

Protecting gross margins without large consumer price hikes forces Nichols to use strategic hedging and multi-year supplier contracts; hedging reduced raw-material cost variance by an estimated 5–8% in recent years.

Consumer Purchasing Power

UK inflation eased to 3.9% in December 2025 from a 2023 peak, but Bank of England base rate remains around 5.25% (Jan 2026), squeezing real incomes and reducing discretionary spend on soft drinks.

Household real wages fell cumulatively ~4% from 2021–2024, prompting consumers to trade down to private labels—Grocery Market share for own-label rose to ~51% in 2024.

Nichols must balance Fever-Tree’s premium positioning with value SKUs and multipack promotions to retain share during tighter cycles and sustain OOH sales recovery.

Exchange Rate Fluctuations

Nichols faces currency risk across GBP, USD and EUR given its international operations; a 10% GBP depreciation versus USD in 2023 would have reduced reported UK revenue in USD terms materially, mirroring a 2024 FX volatility rise—GBP moved about 8% vs EUR and 6% vs USD in 2024–2025. Significant swings alter reported sales and imported input costs, notably PET and syrup purchases invoiced in USD. Nichols uses forward contracts, FX options and natural hedges (foreign-sourced revenue vs costs) to stabilise cashflows, with hedging covering a sizable portion of anticipated exposures—company disclosures in 2024 show hedges reducing reported FX impact by mid-single digits percentage points.

Out-of-Home Sector Recovery

The economic health of hospitality and leisure directly affects Nichols Out-of-Home; UK cinema admissions rose 18% in 2023 vs 2022 and global themed-park attendance recovered to 91% of 2019 levels in 2024, supporting demand for post-mix and dispensed soft drinks.

Higher tourist spending—UNWTO reported 2024 international tourist spending up 28% vs 2022—boosts this high-margin segment and underpins revenue growth as consumer behavior stabilizes.

- Cinema admissions +18% (UK, 2023)

- Theme-park attendance 91% of 2019 (2024)

- Intl tourist spending +28% vs 2022 (UNWTO, 2024)

Labor Market Pressures

Rising UK wage inflation—4.5% year-on-year in 2025 Q4 for regular pay excluding bonuses—heightens labor costs for Nichols' manufacturing and distribution, pressing margins and prompting higher spend on recruitment and retention to secure scarce skilled staff amid a 3.8% unemployment rate.

To sustain innovation and operational excellence Nichols must boost retention (pay, training, benefits); higher labor costs make automation investments more attractive—robotics and process controls can cut unit labor hours by 15–30% in similar FMCG operations.

- UK wage inflation: 4.5% (2025 Q4)

- Unemployment: 3.8% (2025)

- Retention spend: increased pay, training, benefits

- Automation potential: 15–30% reduction in unit labor hours

Input-cost, FX & price pressure squeeze premium brands as private-label hits ~51%

Commodity and FX volatility (sugar +18% in 2023; GBP ±8% vs EUR, ±6% vs USD in 2024–25) raise input-cost risk; hedging cut raw-cost variance ~5–8% and reduced FX impact by mid-single digits (2024). UK inflation eased to 3.9% (Dec 2025) with base rate ~5.25% (Jan 2026); real wages down ~4% (2021–24) pushing private-label share to ~51% (2024), squeezing premium Fever-Tree and favoring value SKUs.

| Metric | Value |

|---|---|

| Sugar price change (2023) | +18% |

| GBP vs EUR/USD (2024–25) | ±8% / ±6% |

| Hedging effect (raw materials) | -5–8% variance |

| UK inflation (Dec 2025) | 3.9% |

| Bank rate (Jan 2026) | ~5.25% |

| Real wages (2021–24) | -4% |

| Private-label grocery share (2024) | ~51% |

Full Version Awaits

Nichols PESTLE Analysis

The preview shown here is the exact Nichols PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are identical to the file you’ll download immediately after payment.

What you see is the final document—clear, comprehensive, and deliverable as shown with no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and technological change are shaping Nichols's prospects in our concise PESTLE snapshot—perfect for investors and strategists who need quick, actionable context. Purchase the full PESTLE analysis to unlock detailed risk assessments, regulatory impacts, and growth opportunities, delivered in editable formats for immediate use.

Political factors

Middle East Trade Relations

Nichols' Vimto holds a dominant share in Gulf markets, driving over 40% of the firm's export revenues in 2024, with Ramadan sales often boosting regional volumes by 25–35% year-on-year.

Geopolitical stability across the GCC is critical: disruptions in 2022–24 showed supply-chain delays that trimmed export volumes by an estimated 8–12% in affected quarters.

Shifts in UK–Middle East trade policy or diplomatic ties could therefore materially affect Nichols' most profitable international segment, risking revenue volatility and higher logistics costs.

UK Government Health Initiatives

The UK government targets high-sugar drinks through measures like the Soft Drinks Industry Levy, which raised £400m in 2023, and updated guidance on promotions and on-shelf placement affecting Nichols' market of UK adult soft drinks (worth ~£6.5bn in 2024).

Nichols must adapt marketing and reformulation strategies as guidelines tighten; Public Health England and DHSC recommendations press for sugar reduction targets—some voluntary codes since 2019 pushed manufacturers to cut sugar by up to 20%-30% in certain categories.

Political pressure to reduce obesity risks further mandatory codes or stricter advertising/placement rules, posing potential compliance costs and reformulation capex that could impact Nichols' margins and product pricing in the domestic market.

Post-Brexit Trade Agreements

As of end-2025, UK trade deals beyond the EU—covering 60+ preferential agreements—continue to reshape Nichols’ sourcing: 12% of cane sugar and 18% of packaging inputs now come from non-EU partners, altering input cost structures. Tariff shifts and new customs procedures have changed landed costs by up to 4–6% in key emerging markets, squeezing margins on exports. Nichols must stay agile to capture tariff-free access while absorbing an estimated £2–3m annual compliance overhead from increased paperwork and rules-of-origin checks.

Geopolitical Stability in African Markets

- Watch: currency volatility >12% (2023–24)

- Focus markets: Nigeria, South Africa, Kenya

- Benefit: 18% faster entry via local partners (2022–24)

Taxation and Fiscal Policy

Changes in UK corporation tax—from 19% in 2023 to 25% for profits over £250k in 2024—would materially affect Nichols PLC margins, while proposals for environmental levies (e.g., estimated £10–£30/tonne carbon pricing scenarios) could raise production costs across its soft-drinks operations.

Business rate reforms and capital allowances adjustments influence planned CAPEX for Nichols’ UK manufacturing and distribution sites; a 2024 relief extension or increased investment allowances could accelerate £10–£50m facility upgrades.

Continuous monitoring of fiscal policy is vital for long-term planning and shareholder value: sensitivity analyses on tax and levy changes should be incorporated into DCF models and earnings-per-share forecasts.

- Corporation tax rise to 25% for large profits

- Potential carbon/environmental levies £10–£30/tonne

- Business rate reforms and capital allowance impacts on £10–£50m CAPEX

- Incorporate tax scenarios into DCF and EPS sensitivity

Nichols faces GCC export dependence, UK levy costs, higher trade fees and tax squeeze

Political risks for Nichols include GCC geopolitical stability affecting >40% export revenue (Ramadan +25–35% sales), UK regulatory pressure (Soft Drinks Industry Levy raised £400m in 2023; UK adult soft drinks market ~£6.5bn in 2024) forcing reformulation capex, trade-policy shifts changing landed costs by 4–6% and £2–3m compliance overhead, and fiscal changes (corporation tax 25%) impacting margins.

| Risk | Key data |

|---|---|

| GCC exports | >40% revenues; Ramadan +25–35% |

| UK levy | £400m raised (2023); market £6.5bn (2024) |

| Trade costs | +4–6% landed; £2–3m compliance |

| Tax | Corp tax 25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Nichols across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Nichols' full PESTLE into a clean, presentation-ready summary that’s visually segmented by factor, easily editable for local context, and instantly shareable for quick team alignment during planning or client briefings.

Economic factors

Commodity Price Volatility

Commodity price volatility—sugar, fruit concentrates and CO2—raises input-cost risk for Nichols as global sugar prices rose ~18% in 2023 and CO2 shortages pushed European spot prices up over 40% in 2022–24; climate shocks amplify supply-side volatility.

Protecting gross margins without large consumer price hikes forces Nichols to use strategic hedging and multi-year supplier contracts; hedging reduced raw-material cost variance by an estimated 5–8% in recent years.

Consumer Purchasing Power

UK inflation eased to 3.9% in December 2025 from a 2023 peak, but Bank of England base rate remains around 5.25% (Jan 2026), squeezing real incomes and reducing discretionary spend on soft drinks.

Household real wages fell cumulatively ~4% from 2021–2024, prompting consumers to trade down to private labels—Grocery Market share for own-label rose to ~51% in 2024.

Nichols must balance Fever-Tree’s premium positioning with value SKUs and multipack promotions to retain share during tighter cycles and sustain OOH sales recovery.

Exchange Rate Fluctuations

Nichols faces currency risk across GBP, USD and EUR given its international operations; a 10% GBP depreciation versus USD in 2023 would have reduced reported UK revenue in USD terms materially, mirroring a 2024 FX volatility rise—GBP moved about 8% vs EUR and 6% vs USD in 2024–2025. Significant swings alter reported sales and imported input costs, notably PET and syrup purchases invoiced in USD. Nichols uses forward contracts, FX options and natural hedges (foreign-sourced revenue vs costs) to stabilise cashflows, with hedging covering a sizable portion of anticipated exposures—company disclosures in 2024 show hedges reducing reported FX impact by mid-single digits percentage points.

Out-of-Home Sector Recovery

The economic health of hospitality and leisure directly affects Nichols Out-of-Home; UK cinema admissions rose 18% in 2023 vs 2022 and global themed-park attendance recovered to 91% of 2019 levels in 2024, supporting demand for post-mix and dispensed soft drinks.

Higher tourist spending—UNWTO reported 2024 international tourist spending up 28% vs 2022—boosts this high-margin segment and underpins revenue growth as consumer behavior stabilizes.

- Cinema admissions +18% (UK, 2023)

- Theme-park attendance 91% of 2019 (2024)

- Intl tourist spending +28% vs 2022 (UNWTO, 2024)

Labor Market Pressures

Rising UK wage inflation—4.5% year-on-year in 2025 Q4 for regular pay excluding bonuses—heightens labor costs for Nichols' manufacturing and distribution, pressing margins and prompting higher spend on recruitment and retention to secure scarce skilled staff amid a 3.8% unemployment rate.

To sustain innovation and operational excellence Nichols must boost retention (pay, training, benefits); higher labor costs make automation investments more attractive—robotics and process controls can cut unit labor hours by 15–30% in similar FMCG operations.

- UK wage inflation: 4.5% (2025 Q4)

- Unemployment: 3.8% (2025)

- Retention spend: increased pay, training, benefits

- Automation potential: 15–30% reduction in unit labor hours

Input-cost, FX & price pressure squeeze premium brands as private-label hits ~51%

Commodity and FX volatility (sugar +18% in 2023; GBP ±8% vs EUR, ±6% vs USD in 2024–25) raise input-cost risk; hedging cut raw-cost variance ~5–8% and reduced FX impact by mid-single digits (2024). UK inflation eased to 3.9% (Dec 2025) with base rate ~5.25% (Jan 2026); real wages down ~4% (2021–24) pushing private-label share to ~51% (2024), squeezing premium Fever-Tree and favoring value SKUs.

| Metric | Value |

|---|---|

| Sugar price change (2023) | +18% |

| GBP vs EUR/USD (2024–25) | ±8% / ±6% |

| Hedging effect (raw materials) | -5–8% variance |

| UK inflation (Dec 2025) | 3.9% |

| Bank rate (Jan 2026) | ~5.25% |

| Real wages (2021–24) | -4% |

| Private-label grocery share (2024) | ~51% |

Full Version Awaits

Nichols PESTLE Analysis

The preview shown here is the exact Nichols PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are identical to the file you’ll download immediately after payment.

What you see is the final document—clear, comprehensive, and deliverable as shown with no surprises.