Nicolet National Bank Business Model Canvas

Nicolet National Bank: Strategic Business Model Canvas & Playbook for Investors

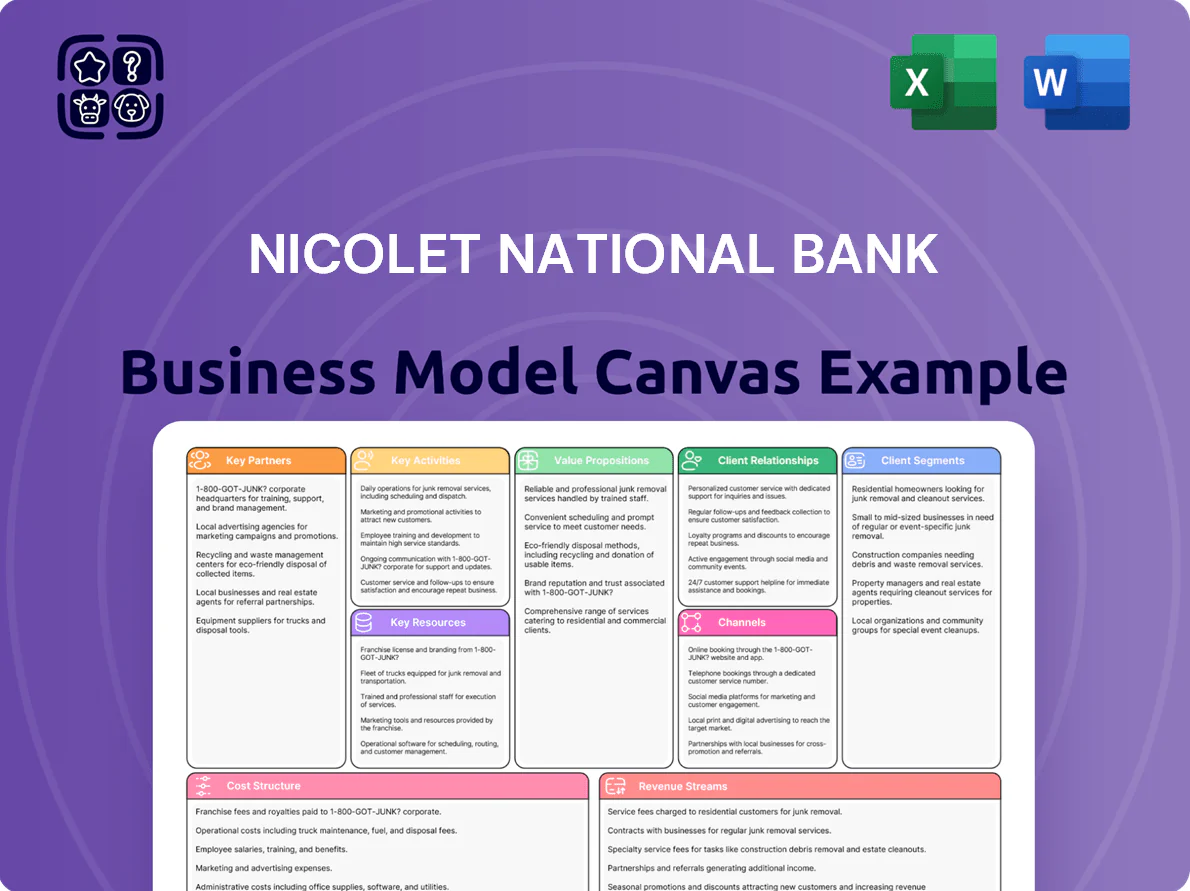

Unlock the full strategic blueprint behind Nicolet National Bank’s business model—this concise Business Model Canvas maps customer segments, value propositions, revenue streams, and key partnerships to reveal how the bank scales, manages risk, and captures market share; download the complete Word/Excel canvas for a section-by-section playbook ideal for investors, consultants, and strategists.

Partnerships

Financial Technology Providers

Federal Reserve and Regulatory Agencies

Maintaining strong ties with the Federal Reserve and Wisconsin state regulators ensures Nicolet National Bank meets Basel III capital and LCR liquidity norms, supporting its $5.8B total assets (2024) and CET1-like capital ratios above peer medians; regular reporting and audits reduce regulatory friction and operational risk. These partnerships supply the transparency investors and depositors expect via quarterly Call Reports, annual audited financials, and compliance reviews.

Local Business and Trade Associations

Mortgage Secondary Market Entities

The bank partners with Fannie Mae and Freddie Mac to sell qualified mortgages into the secondary market, freeing capital and reducing interest-rate risk while funding new originations; in 2024 GSE sales enabled many regional banks to keep 60–70% of residential pipelines balance-sheet light.

The relationship secures steady liquidity—Nicolet can replace loans with cash quickly, keeping lending capacity stable amid rate volatility and funding approx 40–55% of typical residential originations via secondary-market channels.

- Partners: Fannie Mae, Freddie Mac

- Purpose: sell qualified loans, manage interest-rate risk

- Benefit: steady liquidity for new originations

- Typical funding share: ~40–55% of originations

- GSE-enabled balance-sheet light share: ~60–70% (2024 industry)

Wealth Management and Insurance Affiliates

Strategic alliances with specialized investment platforms and insurance providers let Nicolet National Bank offer a full suite of non-interest products, boosting fee income—Nicolet reported $88.4M in noninterest income in 2024 (SEC filings). These partners supply advanced wealth planning and risk-mitigation tools without in-house build, improving value for high-net-worth and corporate clients.

- Expands fee revenue (noninterest income $88.4M, 2024)

- Access to third-party tech reduces capex and time-to-market

- Targets HNW and corporates with sophisticated planning tools

Nicolet: $5.8B bank boosting digital deposits, $2.1B regional loans, cutting fraud 18% YoY

| Metric | Value |

|---|---|

| Total assets (2024) | $5.8B |

| Regional loans (2025) | $2.1B |

| Digital deposit access (2025) | 48% |

| Noninterest income (2024) | $88.4M |

| Resi funding via GSEs | 40–55% |

What is included in the product

A concise Business Model Canvas for Nicolet National Bank detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, and cost structure, reflecting its community banking operations and growth strategy for presentations and investor review.

High-level view of Nicolet National Bank’s business model with editable cells to quickly pinpoint revenue drivers, customer segments, and operational pain points for efficient strategy updates.

Activities

Commercial and Personal Lending

Nicolet National Bank underwrites and manages a diversified loan book—commercial real estate, SBA and small business loans—totaling about $6.2 billion in loans as of 2024 Q4, using localized credit committees to deliver faster turnarounds than national banks (median decision time ~5–7 days). Rigorous credit analysis and quarterly portfolio monitoring keep nonperforming assets low (0.45% NPAs in 2024), helping preserve asset quality through cycles.

Deposit and Liquidity Management

Nicolet National Bank gathers deposits across checking, savings, and CDs—holding $6.3 billion in deposits as of 9/30/2025—while actively managing funding costs to protect net interest margin (NIM was 3.45% in FY2024). Effective liquidity management keeps cash and liquid securities ratios sufficient to meet withdrawals and support targeted loan growth (loans grew 7.8% YoY through 2024), balancing safety and new loan funding.

Wealth Management and Trust Services

Nicolet National Bank offers comprehensive financial planning, investment management, and trust administration for individuals and institutions, producing material non-interest income—wealth management fees contributed roughly 18% of noninterest revenue in 2024—and strengthening ties with high-net-worth clients; teams concentrate on long-term wealth preservation and generational transfer strategies, managing over $6.2 billion in fiduciary assets as of Dec 31, 2024.

Regulatory Compliance and Risk Mitigation

Operating in a highly regulated environment, Nicolet National Bank continuously monitors anti-money laundering, cybersecurity, and consumer protection laws, spending an estimated $25–35 million annually on compliance and reducing AML false positives by 18% in 2024.

The bank invests in internal controls and risk frameworks—supporting a CET1-equivalent capital buffer near 11% and cutting operational losses 22% year-over-year—to protect financial and reputational capital and retain regulator trust.

- Annual compliance spend: $25–35M

- 2024 AML false positive reduction: 18%

- CET1-like buffer: ~11%

- Operational loss reduction: 22% YoY

Community Engagement and Marketing

Nicolet drives local brand equity through frequent sponsorships and philanthropy—over $4.2M donated and 320 community events in 2024—boosting household acquisition in Wisconsin and Upper Midwest markets.

Marketing is hyperlocal: campaigns segmented by county, plus 18% of marketing budget spent on community outreach in 2024, making grassroots efforts a top channel for new-account growth.

- $4.2M donated (2024)

- 320 community events (2024)

- 18% marketing spend on outreach (2024)

- Primary driver for new accounts in regional markets

Nicolet: $6.2B Loans & AUM, $6.3B Deposits — Strong NIM, Low NPAs, Community Impact

Nicolet underwrites $6.2B loans (2024 Q4), manages $6.3B deposits (9/30/2025), NIM 3.45% (FY2024), NPAs 0.45% (2024), wealth AUM $6.2B (12/31/2024), wealth fees ~18% noninterest income (2024), compliance spend $25–35M (annual), donations $4.2M (2024), 320 events (2024).

| Metric | Value |

|---|---|

| Total loans | $6.2B |

| Deposits | $6.3B |

| NIM | 3.45% |

| NPAs | 0.45% |

| Wealth AUM | $6.2B |

| Wealth fees | 18% noninterest |

| Compliance spend | $25–35M |

| Donations | $4.2M |

| Community events | 320 |

Preview Before You Purchase

Business Model Canvas

The preview you see is not a sample—it's a direct excerpt from the actual Nicolet National Bank Business Model Canvas you'll receive after purchase.

When you complete your order, you'll get this exact document in full, formatted and ready to edit, present, or share—no fillers or substitutes.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Nicolet National Bank: Strategic Business Model Canvas & Playbook for Investors

Unlock the full strategic blueprint behind Nicolet National Bank’s business model—this concise Business Model Canvas maps customer segments, value propositions, revenue streams, and key partnerships to reveal how the bank scales, manages risk, and captures market share; download the complete Word/Excel canvas for a section-by-section playbook ideal for investors, consultants, and strategists.

Partnerships

Financial Technology Providers

Federal Reserve and Regulatory Agencies

Maintaining strong ties with the Federal Reserve and Wisconsin state regulators ensures Nicolet National Bank meets Basel III capital and LCR liquidity norms, supporting its $5.8B total assets (2024) and CET1-like capital ratios above peer medians; regular reporting and audits reduce regulatory friction and operational risk. These partnerships supply the transparency investors and depositors expect via quarterly Call Reports, annual audited financials, and compliance reviews.

Local Business and Trade Associations

Mortgage Secondary Market Entities

The bank partners with Fannie Mae and Freddie Mac to sell qualified mortgages into the secondary market, freeing capital and reducing interest-rate risk while funding new originations; in 2024 GSE sales enabled many regional banks to keep 60–70% of residential pipelines balance-sheet light.

The relationship secures steady liquidity—Nicolet can replace loans with cash quickly, keeping lending capacity stable amid rate volatility and funding approx 40–55% of typical residential originations via secondary-market channels.

- Partners: Fannie Mae, Freddie Mac

- Purpose: sell qualified loans, manage interest-rate risk

- Benefit: steady liquidity for new originations

- Typical funding share: ~40–55% of originations

- GSE-enabled balance-sheet light share: ~60–70% (2024 industry)

Wealth Management and Insurance Affiliates

Strategic alliances with specialized investment platforms and insurance providers let Nicolet National Bank offer a full suite of non-interest products, boosting fee income—Nicolet reported $88.4M in noninterest income in 2024 (SEC filings). These partners supply advanced wealth planning and risk-mitigation tools without in-house build, improving value for high-net-worth and corporate clients.

- Expands fee revenue (noninterest income $88.4M, 2024)

- Access to third-party tech reduces capex and time-to-market

- Targets HNW and corporates with sophisticated planning tools

Nicolet: $5.8B bank boosting digital deposits, $2.1B regional loans, cutting fraud 18% YoY

| Metric | Value |

|---|---|

| Total assets (2024) | $5.8B |

| Regional loans (2025) | $2.1B |

| Digital deposit access (2025) | 48% |

| Noninterest income (2024) | $88.4M |

| Resi funding via GSEs | 40–55% |

What is included in the product

A concise Business Model Canvas for Nicolet National Bank detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, and cost structure, reflecting its community banking operations and growth strategy for presentations and investor review.

High-level view of Nicolet National Bank’s business model with editable cells to quickly pinpoint revenue drivers, customer segments, and operational pain points for efficient strategy updates.

Activities

Commercial and Personal Lending

Nicolet National Bank underwrites and manages a diversified loan book—commercial real estate, SBA and small business loans—totaling about $6.2 billion in loans as of 2024 Q4, using localized credit committees to deliver faster turnarounds than national banks (median decision time ~5–7 days). Rigorous credit analysis and quarterly portfolio monitoring keep nonperforming assets low (0.45% NPAs in 2024), helping preserve asset quality through cycles.

Deposit and Liquidity Management

Nicolet National Bank gathers deposits across checking, savings, and CDs—holding $6.3 billion in deposits as of 9/30/2025—while actively managing funding costs to protect net interest margin (NIM was 3.45% in FY2024). Effective liquidity management keeps cash and liquid securities ratios sufficient to meet withdrawals and support targeted loan growth (loans grew 7.8% YoY through 2024), balancing safety and new loan funding.

Wealth Management and Trust Services

Nicolet National Bank offers comprehensive financial planning, investment management, and trust administration for individuals and institutions, producing material non-interest income—wealth management fees contributed roughly 18% of noninterest revenue in 2024—and strengthening ties with high-net-worth clients; teams concentrate on long-term wealth preservation and generational transfer strategies, managing over $6.2 billion in fiduciary assets as of Dec 31, 2024.

Regulatory Compliance and Risk Mitigation

Operating in a highly regulated environment, Nicolet National Bank continuously monitors anti-money laundering, cybersecurity, and consumer protection laws, spending an estimated $25–35 million annually on compliance and reducing AML false positives by 18% in 2024.

The bank invests in internal controls and risk frameworks—supporting a CET1-equivalent capital buffer near 11% and cutting operational losses 22% year-over-year—to protect financial and reputational capital and retain regulator trust.

- Annual compliance spend: $25–35M

- 2024 AML false positive reduction: 18%

- CET1-like buffer: ~11%

- Operational loss reduction: 22% YoY

Community Engagement and Marketing

Nicolet drives local brand equity through frequent sponsorships and philanthropy—over $4.2M donated and 320 community events in 2024—boosting household acquisition in Wisconsin and Upper Midwest markets.

Marketing is hyperlocal: campaigns segmented by county, plus 18% of marketing budget spent on community outreach in 2024, making grassroots efforts a top channel for new-account growth.

- $4.2M donated (2024)

- 320 community events (2024)

- 18% marketing spend on outreach (2024)

- Primary driver for new accounts in regional markets

Nicolet: $6.2B Loans & AUM, $6.3B Deposits — Strong NIM, Low NPAs, Community Impact

Nicolet underwrites $6.2B loans (2024 Q4), manages $6.3B deposits (9/30/2025), NIM 3.45% (FY2024), NPAs 0.45% (2024), wealth AUM $6.2B (12/31/2024), wealth fees ~18% noninterest income (2024), compliance spend $25–35M (annual), donations $4.2M (2024), 320 events (2024).

| Metric | Value |

|---|---|

| Total loans | $6.2B |

| Deposits | $6.3B |

| NIM | 3.45% |

| NPAs | 0.45% |

| Wealth AUM | $6.2B |

| Wealth fees | 18% noninterest |

| Compliance spend | $25–35M |

| Donations | $4.2M |

| Community events | 320 |

Preview Before You Purchase

Business Model Canvas

The preview you see is not a sample—it's a direct excerpt from the actual Nicolet National Bank Business Model Canvas you'll receive after purchase.

When you complete your order, you'll get this exact document in full, formatted and ready to edit, present, or share—no fillers or substitutes.