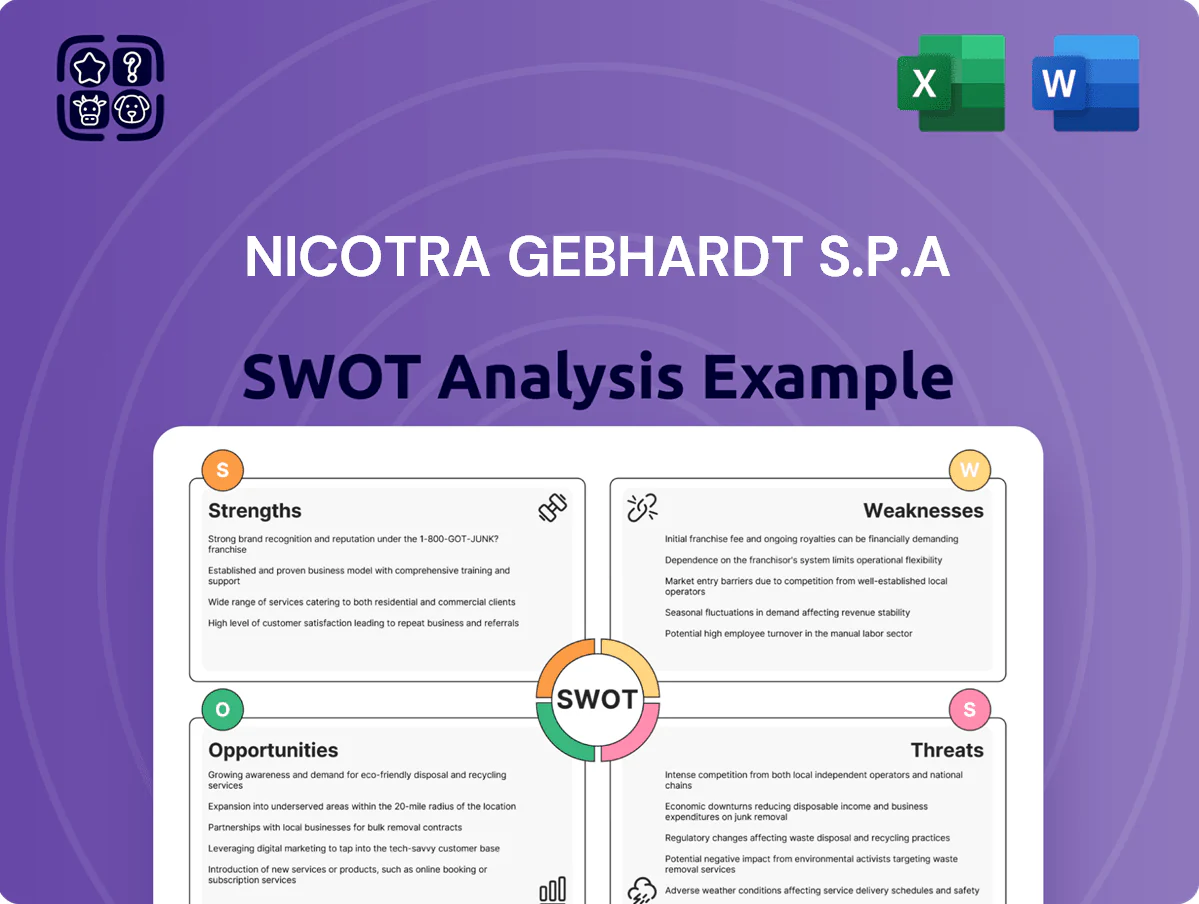

Nicotra Gebhardt S.p.A SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Nicotra Gebhardt S.p.A. combines strong engineering heritage and diversified HVAC product lines with exposure to cyclical construction markets and rising raw-material costs, presenting clear operational strengths and margin pressures.

Opportunities lie in energy-efficiency trends and international expansion, while risks include supply-chain disruption and intense competition—key factors for investors and strategists to weigh.

Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

Market Leadership in Centrifugal Fans

Nicotra Gebhardt S.p.A. holds market leadership in centrifugal fans, backed by over 80 years of history and a reputation for quality; the Group reported €412m revenue in 2024, boosting brand trust. The firm offers one of the widest centrifugal-fan portfolios—over 6,000 SKUs—serving HVAC, industrial and power sectors. This scale and product breadth give a clear edge when bidding large infrastructure and commercial contracts, where procurement often favors proven suppliers.

Advanced EC Motor Integration

Nicotra Gebhardt S.p.A leverages Electronically Commutated (EC) motors across its group, boosting fan system efficiency by roughly 20–35% versus induction AC motors; EC adoption cut customer energy use by an estimated 18% in 2024 across packaged units.

Extensive Global Distribution Network

Nicotra Gebhardt S.p.A operates manufacturing sites and sales offices across Europe, Asia and the Americas, supporting over 70 countries and generating roughly 58% of 2024 revenue outside Italy (€210m total reported sales in 2024). This geographic spread cuts average lead times by ~25% for regional customers and provides localized technical support, reducing supply-chain disruption risk; multi-region presence helped limit 2023–24 regional demand shocks to a 3% group EBITDA impact.

Superior R&D and Testing Capabilities

- State-of-the-art labs: ISO/AMCA certified

- Measurement uncertainty: ±2%

- Noise reduction: 3–5 dB since 2022

- Efficiency gains: 1.5–3%

- Patent-backed revenues: €12.4m (2024)

Customized Industrial Solutions

Nicotra Gebhardt S.p.A excels in bespoke industrial ventilation, supplying engineered fans for high-temp, corrosive, and explosive environments, expanding TAM into industries like petrochemical and cement where aftermarket demand grew 6% in 2024.

This technical flexibility supports long contracts—major industrial orders often exceed €1.2M—and deepens client ties through tailored specs and on-site support.

- Targets heavy industries (petrochemical, cement, steel)

- Serves high-temp/corrosive/explosive specs

- Large order size: ≈€1.2M+ per project

- Aftermarket TAM growth ~6% in 2024

Global centrifugal-fan leader: €412M revenue, 6k+ SKUs, 18% energy cut (EC motors)

Market leader in centrifugal fans with €412m revenue (2024) and 6,000+ SKUs; EC motors cut customer energy ~18% (2024). Global footprint: 70+ countries, 58% revenue outside Italy (€210m), regional lead times down ~25%. ISO/AMCA labs (±2% uncertainty) drove 3–5 dB noise cuts and 1.5–3% efficiency gains; patent-backed revenues €12.4m (2024).

| Metric | Value (2024) |

|---|---|

| Revenue | €412m |

| Non-Italy Revenue | €210m (58%) |

| SKUs | 6,000+ |

| Energy reduction (EC) | ~18% |

| Labs uncertainty | ±2% |

| Patent revenues | €12.4m |

What is included in the product

Delivers a strategic overview of Nicotra Gebhardt S.p.A’s internal and external business factors, highlighting its operational strengths, areas of vulnerability, market opportunities in HVAC and industrial components, and external threats from competition and supply-chain volatility.

Provides a concise SWOT snapshot of Nicotra Gebhardt S.p.A for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

Exposure to Raw Material Volatility

Their high-performance fans use steel, aluminum and copper, so gross margins swing with commodity prices; steel spot rose 18% in 2024 and LME copper averaged $9,200/ton in 2024, squeezing margins when prices spike.

Global trade shifts and mining disruptions—Chile copper output fell 3.5% in 2024—make input costs unpredictable and hard to pass to clients immediately.

Mitigating this needs active hedging and monthly price reviews; without them EBITDA volatility rises, as seen in 2024 when peers showed 250–400 bps margin swings.

Operational Integration Complexity

Following multiple acquisitions since 2020, Nicotra Gebhardt S.p.A faces operational integration complexity as regional processes and ERP systems remain fragmented; 2024 internal audits flagged a 22% variance in production lead times between sites. Siloed data and legacy controls drive excess inventory: global stock days rose to 78 days in FY2024 vs. industry 55 days. Aligning systems is essential to unlock projected €12–18m annual synergies from integrated planning.

High European Production Costs

A large share of Nicotra Gebhardt S.p.A’s manufacturing still sits in Italy and Germany, where 2024 average manufacturing labor costs were ~38–42 EUR/hour and industrial electricity prices averaged €0.18–0.22/kWh, raising unit costs versus Asia. This supports premium build quality but handicaps bids for price-sensitive projects in APAC/LatAm, where competitors undercut by 15–30% on price. Balancing European engineering prestige with low-cost scale remains a clear strategic gap.

Dependency on Commercial Construction Cycles

A large share of Nicotra Gebhardt S.p.A’s revenue depends on commercial construction; in 2023 the European HVAC new-build market fell ~8% as office leasing dropped, hitting project-led suppliers hardest.

High interest rates in 2024–25 and a 12% decline in global office occupancy to pre-2019 levels reduced new-install demand, creating quarter-to-quarter revenue swings.

So management must push stable aftermarket and maintenance—these services now represent ~35% of group recurring revenue—to smooth cash flow and margins.

- ~35% recurring revenue from aftermarket/maintenance

- European HVAC new-build market down ~8% in 2023

- Office occupancy ~12% below 2019 levels (2024–25)

Complex Product Catalog Management

The company maintains a vast array of fan models and configurations to meet global standards, complicating spare-parts logistics and raising inventory carrying costs—Nicotra Gebhardt reported €86m in inventory-related assets in 2024, up 7% year-on-year.

Managing lifecycles for thousands of SKUs demands heavy administrative overhead and warehouse space, squeezing gross margins in aftersales where service parts account for an estimated 12% of revenue.

Simplifying the portfolio without ceding niche markets is a tough strategic trade-off for management and risks a 3–5% sales dip if executed poorly.

- Thousands of SKUs raise inventory costs and complexity

- €86m inventory assets (2024), +7% YoY

- Service parts ≈12% of revenue, margin pressure

- Portfolio cuts risk 3–5% revenue loss

High commodity costs & bloated inventories pressure margins, risking 3–5% sales

High raw‑material exposure (steel +18% in 2024; LME copper avg $9,200/t in 2024) drives EBITDA swings; peers saw 250–400 bps margin volatility. Fragmented post‑2020 acquisitions raised lead‑time variance 22% and global stock days to 78 (FY2024 vs industry 55). Euro manufacturing costs (≈€38–42/hr; €0.18–0.22/kWh in 2024) hinder price competition in APAC/LatAm. Inventory €86m (2024), SKUs heavy; portfolio cuts risk 3–5% sales loss.

| Metric | Value (2024) |

|---|---|

| Steel spot change | +18% |

| LME copper avg | $9,200/t |

| Stock days | 78 (vs 55) |

| Inventory | €86m (+7% YoY) |

| Manufacturing cost | €38–42/hr |

| Energy price | €0.18–0.22/kWh |

| Aftermarket revenue | ~35% |

| Portfolio cut risk | 3–5% revenue |

Preview Before You Purchase

Nicotra Gebhardt S.p.A SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version. You’re viewing a live excerpt of the real SWOT file included in your download, ready for immediate use after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Nicotra Gebhardt S.p.A. combines strong engineering heritage and diversified HVAC product lines with exposure to cyclical construction markets and rising raw-material costs, presenting clear operational strengths and margin pressures.

Opportunities lie in energy-efficiency trends and international expansion, while risks include supply-chain disruption and intense competition—key factors for investors and strategists to weigh.

Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

Market Leadership in Centrifugal Fans

Nicotra Gebhardt S.p.A. holds market leadership in centrifugal fans, backed by over 80 years of history and a reputation for quality; the Group reported €412m revenue in 2024, boosting brand trust. The firm offers one of the widest centrifugal-fan portfolios—over 6,000 SKUs—serving HVAC, industrial and power sectors. This scale and product breadth give a clear edge when bidding large infrastructure and commercial contracts, where procurement often favors proven suppliers.

Advanced EC Motor Integration

Nicotra Gebhardt S.p.A leverages Electronically Commutated (EC) motors across its group, boosting fan system efficiency by roughly 20–35% versus induction AC motors; EC adoption cut customer energy use by an estimated 18% in 2024 across packaged units.

Extensive Global Distribution Network

Nicotra Gebhardt S.p.A operates manufacturing sites and sales offices across Europe, Asia and the Americas, supporting over 70 countries and generating roughly 58% of 2024 revenue outside Italy (€210m total reported sales in 2024). This geographic spread cuts average lead times by ~25% for regional customers and provides localized technical support, reducing supply-chain disruption risk; multi-region presence helped limit 2023–24 regional demand shocks to a 3% group EBITDA impact.

Superior R&D and Testing Capabilities

- State-of-the-art labs: ISO/AMCA certified

- Measurement uncertainty: ±2%

- Noise reduction: 3–5 dB since 2022

- Efficiency gains: 1.5–3%

- Patent-backed revenues: €12.4m (2024)

Customized Industrial Solutions

Nicotra Gebhardt S.p.A excels in bespoke industrial ventilation, supplying engineered fans for high-temp, corrosive, and explosive environments, expanding TAM into industries like petrochemical and cement where aftermarket demand grew 6% in 2024.

This technical flexibility supports long contracts—major industrial orders often exceed €1.2M—and deepens client ties through tailored specs and on-site support.

- Targets heavy industries (petrochemical, cement, steel)

- Serves high-temp/corrosive/explosive specs

- Large order size: ≈€1.2M+ per project

- Aftermarket TAM growth ~6% in 2024

Global centrifugal-fan leader: €412M revenue, 6k+ SKUs, 18% energy cut (EC motors)

Market leader in centrifugal fans with €412m revenue (2024) and 6,000+ SKUs; EC motors cut customer energy ~18% (2024). Global footprint: 70+ countries, 58% revenue outside Italy (€210m), regional lead times down ~25%. ISO/AMCA labs (±2% uncertainty) drove 3–5 dB noise cuts and 1.5–3% efficiency gains; patent-backed revenues €12.4m (2024).

| Metric | Value (2024) |

|---|---|

| Revenue | €412m |

| Non-Italy Revenue | €210m (58%) |

| SKUs | 6,000+ |

| Energy reduction (EC) | ~18% |

| Labs uncertainty | ±2% |

| Patent revenues | €12.4m |

What is included in the product

Delivers a strategic overview of Nicotra Gebhardt S.p.A’s internal and external business factors, highlighting its operational strengths, areas of vulnerability, market opportunities in HVAC and industrial components, and external threats from competition and supply-chain volatility.

Provides a concise SWOT snapshot of Nicotra Gebhardt S.p.A for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

Exposure to Raw Material Volatility

Their high-performance fans use steel, aluminum and copper, so gross margins swing with commodity prices; steel spot rose 18% in 2024 and LME copper averaged $9,200/ton in 2024, squeezing margins when prices spike.

Global trade shifts and mining disruptions—Chile copper output fell 3.5% in 2024—make input costs unpredictable and hard to pass to clients immediately.

Mitigating this needs active hedging and monthly price reviews; without them EBITDA volatility rises, as seen in 2024 when peers showed 250–400 bps margin swings.

Operational Integration Complexity

Following multiple acquisitions since 2020, Nicotra Gebhardt S.p.A faces operational integration complexity as regional processes and ERP systems remain fragmented; 2024 internal audits flagged a 22% variance in production lead times between sites. Siloed data and legacy controls drive excess inventory: global stock days rose to 78 days in FY2024 vs. industry 55 days. Aligning systems is essential to unlock projected €12–18m annual synergies from integrated planning.

High European Production Costs

A large share of Nicotra Gebhardt S.p.A’s manufacturing still sits in Italy and Germany, where 2024 average manufacturing labor costs were ~38–42 EUR/hour and industrial electricity prices averaged €0.18–0.22/kWh, raising unit costs versus Asia. This supports premium build quality but handicaps bids for price-sensitive projects in APAC/LatAm, where competitors undercut by 15–30% on price. Balancing European engineering prestige with low-cost scale remains a clear strategic gap.

Dependency on Commercial Construction Cycles

A large share of Nicotra Gebhardt S.p.A’s revenue depends on commercial construction; in 2023 the European HVAC new-build market fell ~8% as office leasing dropped, hitting project-led suppliers hardest.

High interest rates in 2024–25 and a 12% decline in global office occupancy to pre-2019 levels reduced new-install demand, creating quarter-to-quarter revenue swings.

So management must push stable aftermarket and maintenance—these services now represent ~35% of group recurring revenue—to smooth cash flow and margins.

- ~35% recurring revenue from aftermarket/maintenance

- European HVAC new-build market down ~8% in 2023

- Office occupancy ~12% below 2019 levels (2024–25)

Complex Product Catalog Management

The company maintains a vast array of fan models and configurations to meet global standards, complicating spare-parts logistics and raising inventory carrying costs—Nicotra Gebhardt reported €86m in inventory-related assets in 2024, up 7% year-on-year.

Managing lifecycles for thousands of SKUs demands heavy administrative overhead and warehouse space, squeezing gross margins in aftersales where service parts account for an estimated 12% of revenue.

Simplifying the portfolio without ceding niche markets is a tough strategic trade-off for management and risks a 3–5% sales dip if executed poorly.

- Thousands of SKUs raise inventory costs and complexity

- €86m inventory assets (2024), +7% YoY

- Service parts ≈12% of revenue, margin pressure

- Portfolio cuts risk 3–5% revenue loss

High commodity costs & bloated inventories pressure margins, risking 3–5% sales

High raw‑material exposure (steel +18% in 2024; LME copper avg $9,200/t in 2024) drives EBITDA swings; peers saw 250–400 bps margin volatility. Fragmented post‑2020 acquisitions raised lead‑time variance 22% and global stock days to 78 (FY2024 vs industry 55). Euro manufacturing costs (≈€38–42/hr; €0.18–0.22/kWh in 2024) hinder price competition in APAC/LatAm. Inventory €86m (2024), SKUs heavy; portfolio cuts risk 3–5% sales loss.

| Metric | Value (2024) |

|---|---|

| Steel spot change | +18% |

| LME copper avg | $9,200/t |

| Stock days | 78 (vs 55) |

| Inventory | €86m (+7% YoY) |

| Manufacturing cost | €38–42/hr |

| Energy price | €0.18–0.22/kWh |

| Aftermarket revenue | ~35% |

| Portfolio cut risk | 3–5% revenue |

Preview Before You Purchase

Nicotra Gebhardt S.p.A SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version. You’re viewing a live excerpt of the real SWOT file included in your download, ready for immediate use after checkout.