Nine Energy Service PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and technological advances are reshaping Nine Energy Service’s prospects—our concise PESTLE snapshot highlights risks and opportunities for investors and strategists; purchase the full analysis to access a detailed, actionable roadmap and download-ready files for immediate use.

Political factors

Federal Land Permitting Policies

Federal land permitting policies shape North America’s TAM for service firms; federal acreage accounted for roughly 10-15% of US crude production in 2023–2024, so permit pace materially alters demand for Nine Energy Service’s well services.

Administration shifts through 2025 slowed BLM onshore permit approvals by ~20% YoY in 2021–2022, with partial recovery to pre-2021 levels by 2024, causing volatile lease auction volumes and scheduling uncertainty.

Nine must adjust to permit-driven capex swings: US onshore rig counts fluctuated ±25% between 2021–2024, directly affecting service revenue timing and utilization of completion and wireline fleets.

Geopolitical Influence on Oil Prices

Global political stability and OPEC+ production cuts set baseline incentives for US onshore output; OPEC+ pledged 3.66 million b/d of adjustments in 2024–25, keeping WTI around a $70–80/bbl band and influencing operator CAPEX for completions.

Political tensions in the Middle East and Russia-Ukraine dynamics raised Brent volatility, with 2024 implied volatility spiking by ~30%, creating uncertain demand for Nine Energy Service completion crews and equipment.

Nine Energy’s backlog and utilization depend on steady drilling schedules; US rig counts averaged ~680 in 2025 YTD, so any geopolitically driven price shock can quickly defer projects and pressure quarterly revenues.

Trade Policies and Tariffs

International trade agreements and tariffs on imported steel and specialized components raised costs for completion tools and wireline equipment; US tariffs on steel (25% since 2018) and recent 2024 tariffs on certain Chinese oilfield equipment increased input costs by an estimated 4–7% industry-wide, pressuring Nine Energy Service margins.

Protective measures can force Nine Energy to absorb costs or raise client prices; in 2024 steel-price volatility added roughly $3–6 per ton to manufacturing, squeezing gross margins for equipment segments that reported a 6–9% margin range in 2023–2024.

Monitoring trade relations—US-China, US-EU, and regional CPTPP dynamics—remains essential to protect proprietary technology margins, with supply-chain reshoring and alternative sourcing reducing tariff exposure by up to 15% in pilot programs.

State-Level Energy Regulations

Regional politics in the Permian, Eagle Ford, and Appalachian basins directly affect Nine Energy Service operations; Texas alone accounted for about 40% of US crude production in 2024, making state policy shifts material to continuity and margins.

State governments differ on taxation, permitting speed, and local mandates—e.g., Texas and Oklahoma favor pro-development policies while Pennsylvania’s stricter emissions and royalty rules can raise operating costs up to several percentage points.

Nine must customize strategies per state—adjusting capital allocation, fleet deployment, and compliance budgets—to mitigate political risk and capture basin-specific demand; in 2024, Permian activity drove roughly 30–35% of US drilling rig demand.

- Texas: pro-development, ~40% of US crude (2024)

- Pennsylvania: tighter emissions/royalty rules, higher compliance costs

- Strategy: local-tailored capex, fleet mix, regulatory engagement

Energy Security Initiatives

- U.S. production: 12.4M b/d (2024), 11.5M b/d (2025)

- Horizontal rig count: ~730 (2025)

- Infrastructure investments: >$60B announced 2024–25

Permits, tariffs & OPEC cuts spark ±25% US onshore volatility and cost hikes

Federal and state permitting, trade tariffs, and geopolitics drove demand volatility for Nine Energy; US onshore permits and rig counts swung ~±25% (2021–2024), Texas produced ~40% of US crude (2024), US crude averaged 12.4M b/d (2024) and 11.5M b/d (2025), OPEC+ adjustments ~3.66M b/d (2024–25), and tariffs raised input costs ~4–7%.

| Metric | Value |

|---|---|

| US crude | 12.4M b/d (2024); 11.5M b/d (2025) |

| Texas share | ~40% (2024) |

| Rig count swing | ±25% (2021–24) |

| OPEC+ cuts | ~3.66M b/d (2024–25) |

| Tariff impact | Input cost +4–7% |

What is included in the product

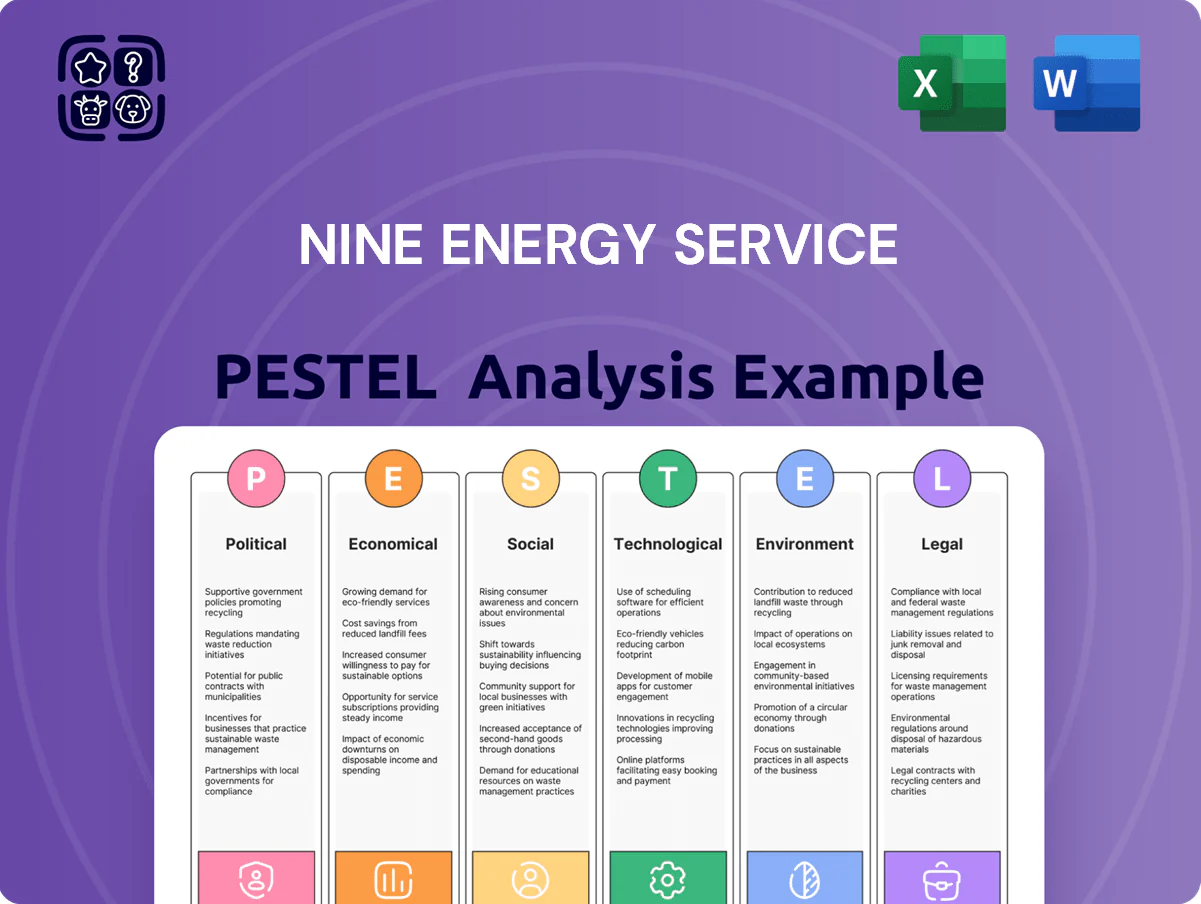

Explores how external macro-environmental factors uniquely affect Nine Energy Service across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed insights and region-specific trends to identify risks and opportunities.

A concise PESTLE summary of Nine Energy Service that’s visually segmented for quick meeting reference, easily editable for regional or business-line notes, and formatted to drop straight into presentations or strategy packs.

Economic factors

Commodity Price Volatility

The economic viability of Nine Energy Service is tightly tied to WTI and Henry Hub prices; in 2024 WTI averaged about 80 USD/bbl and Henry Hub ~3.50 USD/MMBtu, levels that support shale breakevens and lifted demand for cementing and coiled tubing. When WTI falls below typical shale breakevens (~50–60 USD/bbl) or price wars occur, operator activity and Nine’s revenue can drop sharply, as seen in prior downturns where activity fell 30–50%.

Interest Rate Environment

As of end-2025, Nine Energy Service’s historically high leverage makes prevailing rates critical: the U.S. Fed funds rate near 5.25%–5.50% kept benchmark borrowing costly, raising annual interest expense and constraining free cash flow needed for servicing roughly $400–600 million of debt on recent balance-sheet ranges. Elevated rates through 2024–2025 increased financing costs for fleet expansion and R&D, slowing capital allocation to next-gen completion technologies. A shift to lower rates would reduce interest expense materially—potentially freeing tens of millions annually—and restore flexibility to pursue equipment upgrades and technology investments.

E&P Capital Discipline

E&P capital discipline has driven US oil producers to target free cash flow and shareholder returns, with US upstream capex down about 12% year-over-year in 2024 and dividend + buyback payouts rising to roughly $80 billion industry-wide; this compresses well counts and raises competition for completions. Nine Energy Service must prove superior efficiency and lower per-well costs—backed by metrics like service utilization and margin—to win a smaller, more selective volume of contracts.

Inflationary Pressure on Labor

- Wage growth ~7.8% YoY (2024)

- Technician premium pay 10–20% in tight markets

- CPI ~3.4% (2024) → more frequent price adjustments

- Labor costs ~18–22% of revenue among peers

Supply Chain Resilience

Supply chain resilience directly affects Nine Energy Service's economic efficiency in delivering completion tools and chemicals, with logistics stability determining margins and on-time project delivery.

Disruptions in shipping or shortages of specialized materials have historically increased operational costs by up to 12–18% per project in the oilfield services sector, causing schedule slippage and higher working capital needs.

By end-2025 Nine Energy prioritized localizing suppliers, targeting a 30% reduction in international freight exposure to mitigate volatility from global shipping and tariff fluctuations.

- Localized sourcing target: reduce international freight exposure 30% by 2025

- Estimated cost impact of disruptions: 12–18% per project

- Focus areas: completion tools, specialty chemicals, logistics

Oil at $80, Fed tightness and rising costs squeeze upstream cash flow

Economic exposure: 2024 WTI ~$80/bbl, Henry Hub ~$3.50/MMBtu supporting activity; downturns below $50–60/bbl cut demand 30–50%. Fed funds ~5.25%–5.50% (2024–25) raised interest on ~$400–600M debt, squeezing FCF. Upstream capex down ~12% YoY (2024) with $80B dividends/buybacks; labor wage growth ~7.8% (2024), CPI ~3.4% (2024), supply disruptions cost +12–18% per project.

| Metric | 2024/2025 |

|---|---|

| WTI (avg) | $80/bbl |

| Henry Hub | $3.50/MMBtu |

| Fed funds | 5.25%–5.50% |

| Upstream capex YoY | -12% |

| Dividends+buybacks | $80B |

| Wage growth | 7.8% |

| CPI | 3.4% |

| Debt exposure | $400–600M |

| Supply disruption cost | +12–18% |

Preview Before You Purchase

Nine Energy Service PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Nine Energy Service you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and technological advances are reshaping Nine Energy Service’s prospects—our concise PESTLE snapshot highlights risks and opportunities for investors and strategists; purchase the full analysis to access a detailed, actionable roadmap and download-ready files for immediate use.

Political factors

Federal Land Permitting Policies

Federal land permitting policies shape North America’s TAM for service firms; federal acreage accounted for roughly 10-15% of US crude production in 2023–2024, so permit pace materially alters demand for Nine Energy Service’s well services.

Administration shifts through 2025 slowed BLM onshore permit approvals by ~20% YoY in 2021–2022, with partial recovery to pre-2021 levels by 2024, causing volatile lease auction volumes and scheduling uncertainty.

Nine must adjust to permit-driven capex swings: US onshore rig counts fluctuated ±25% between 2021–2024, directly affecting service revenue timing and utilization of completion and wireline fleets.

Geopolitical Influence on Oil Prices

Global political stability and OPEC+ production cuts set baseline incentives for US onshore output; OPEC+ pledged 3.66 million b/d of adjustments in 2024–25, keeping WTI around a $70–80/bbl band and influencing operator CAPEX for completions.

Political tensions in the Middle East and Russia-Ukraine dynamics raised Brent volatility, with 2024 implied volatility spiking by ~30%, creating uncertain demand for Nine Energy Service completion crews and equipment.

Nine Energy’s backlog and utilization depend on steady drilling schedules; US rig counts averaged ~680 in 2025 YTD, so any geopolitically driven price shock can quickly defer projects and pressure quarterly revenues.

Trade Policies and Tariffs

International trade agreements and tariffs on imported steel and specialized components raised costs for completion tools and wireline equipment; US tariffs on steel (25% since 2018) and recent 2024 tariffs on certain Chinese oilfield equipment increased input costs by an estimated 4–7% industry-wide, pressuring Nine Energy Service margins.

Protective measures can force Nine Energy to absorb costs or raise client prices; in 2024 steel-price volatility added roughly $3–6 per ton to manufacturing, squeezing gross margins for equipment segments that reported a 6–9% margin range in 2023–2024.

Monitoring trade relations—US-China, US-EU, and regional CPTPP dynamics—remains essential to protect proprietary technology margins, with supply-chain reshoring and alternative sourcing reducing tariff exposure by up to 15% in pilot programs.

State-Level Energy Regulations

Regional politics in the Permian, Eagle Ford, and Appalachian basins directly affect Nine Energy Service operations; Texas alone accounted for about 40% of US crude production in 2024, making state policy shifts material to continuity and margins.

State governments differ on taxation, permitting speed, and local mandates—e.g., Texas and Oklahoma favor pro-development policies while Pennsylvania’s stricter emissions and royalty rules can raise operating costs up to several percentage points.

Nine must customize strategies per state—adjusting capital allocation, fleet deployment, and compliance budgets—to mitigate political risk and capture basin-specific demand; in 2024, Permian activity drove roughly 30–35% of US drilling rig demand.

- Texas: pro-development, ~40% of US crude (2024)

- Pennsylvania: tighter emissions/royalty rules, higher compliance costs

- Strategy: local-tailored capex, fleet mix, regulatory engagement

Energy Security Initiatives

- U.S. production: 12.4M b/d (2024), 11.5M b/d (2025)

- Horizontal rig count: ~730 (2025)

- Infrastructure investments: >$60B announced 2024–25

Permits, tariffs & OPEC cuts spark ±25% US onshore volatility and cost hikes

Federal and state permitting, trade tariffs, and geopolitics drove demand volatility for Nine Energy; US onshore permits and rig counts swung ~±25% (2021–2024), Texas produced ~40% of US crude (2024), US crude averaged 12.4M b/d (2024) and 11.5M b/d (2025), OPEC+ adjustments ~3.66M b/d (2024–25), and tariffs raised input costs ~4–7%.

| Metric | Value |

|---|---|

| US crude | 12.4M b/d (2024); 11.5M b/d (2025) |

| Texas share | ~40% (2024) |

| Rig count swing | ±25% (2021–24) |

| OPEC+ cuts | ~3.66M b/d (2024–25) |

| Tariff impact | Input cost +4–7% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Nine Energy Service across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed insights and region-specific trends to identify risks and opportunities.

A concise PESTLE summary of Nine Energy Service that’s visually segmented for quick meeting reference, easily editable for regional or business-line notes, and formatted to drop straight into presentations or strategy packs.

Economic factors

Commodity Price Volatility

The economic viability of Nine Energy Service is tightly tied to WTI and Henry Hub prices; in 2024 WTI averaged about 80 USD/bbl and Henry Hub ~3.50 USD/MMBtu, levels that support shale breakevens and lifted demand for cementing and coiled tubing. When WTI falls below typical shale breakevens (~50–60 USD/bbl) or price wars occur, operator activity and Nine’s revenue can drop sharply, as seen in prior downturns where activity fell 30–50%.

Interest Rate Environment

As of end-2025, Nine Energy Service’s historically high leverage makes prevailing rates critical: the U.S. Fed funds rate near 5.25%–5.50% kept benchmark borrowing costly, raising annual interest expense and constraining free cash flow needed for servicing roughly $400–600 million of debt on recent balance-sheet ranges. Elevated rates through 2024–2025 increased financing costs for fleet expansion and R&D, slowing capital allocation to next-gen completion technologies. A shift to lower rates would reduce interest expense materially—potentially freeing tens of millions annually—and restore flexibility to pursue equipment upgrades and technology investments.

E&P Capital Discipline

E&P capital discipline has driven US oil producers to target free cash flow and shareholder returns, with US upstream capex down about 12% year-over-year in 2024 and dividend + buyback payouts rising to roughly $80 billion industry-wide; this compresses well counts and raises competition for completions. Nine Energy Service must prove superior efficiency and lower per-well costs—backed by metrics like service utilization and margin—to win a smaller, more selective volume of contracts.

Inflationary Pressure on Labor

- Wage growth ~7.8% YoY (2024)

- Technician premium pay 10–20% in tight markets

- CPI ~3.4% (2024) → more frequent price adjustments

- Labor costs ~18–22% of revenue among peers

Supply Chain Resilience

Supply chain resilience directly affects Nine Energy Service's economic efficiency in delivering completion tools and chemicals, with logistics stability determining margins and on-time project delivery.

Disruptions in shipping or shortages of specialized materials have historically increased operational costs by up to 12–18% per project in the oilfield services sector, causing schedule slippage and higher working capital needs.

By end-2025 Nine Energy prioritized localizing suppliers, targeting a 30% reduction in international freight exposure to mitigate volatility from global shipping and tariff fluctuations.

- Localized sourcing target: reduce international freight exposure 30% by 2025

- Estimated cost impact of disruptions: 12–18% per project

- Focus areas: completion tools, specialty chemicals, logistics

Oil at $80, Fed tightness and rising costs squeeze upstream cash flow

Economic exposure: 2024 WTI ~$80/bbl, Henry Hub ~$3.50/MMBtu supporting activity; downturns below $50–60/bbl cut demand 30–50%. Fed funds ~5.25%–5.50% (2024–25) raised interest on ~$400–600M debt, squeezing FCF. Upstream capex down ~12% YoY (2024) with $80B dividends/buybacks; labor wage growth ~7.8% (2024), CPI ~3.4% (2024), supply disruptions cost +12–18% per project.

| Metric | 2024/2025 |

|---|---|

| WTI (avg) | $80/bbl |

| Henry Hub | $3.50/MMBtu |

| Fed funds | 5.25%–5.50% |

| Upstream capex YoY | -12% |

| Dividends+buybacks | $80B |

| Wage growth | 7.8% |

| CPI | 3.4% |

| Debt exposure | $400–600M |

| Supply disruption cost | +12–18% |

Preview Before You Purchase

Nine Energy Service PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Nine Energy Service you’ll receive after purchase—fully formatted, professionally structured, and ready to use.