Nintendo Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

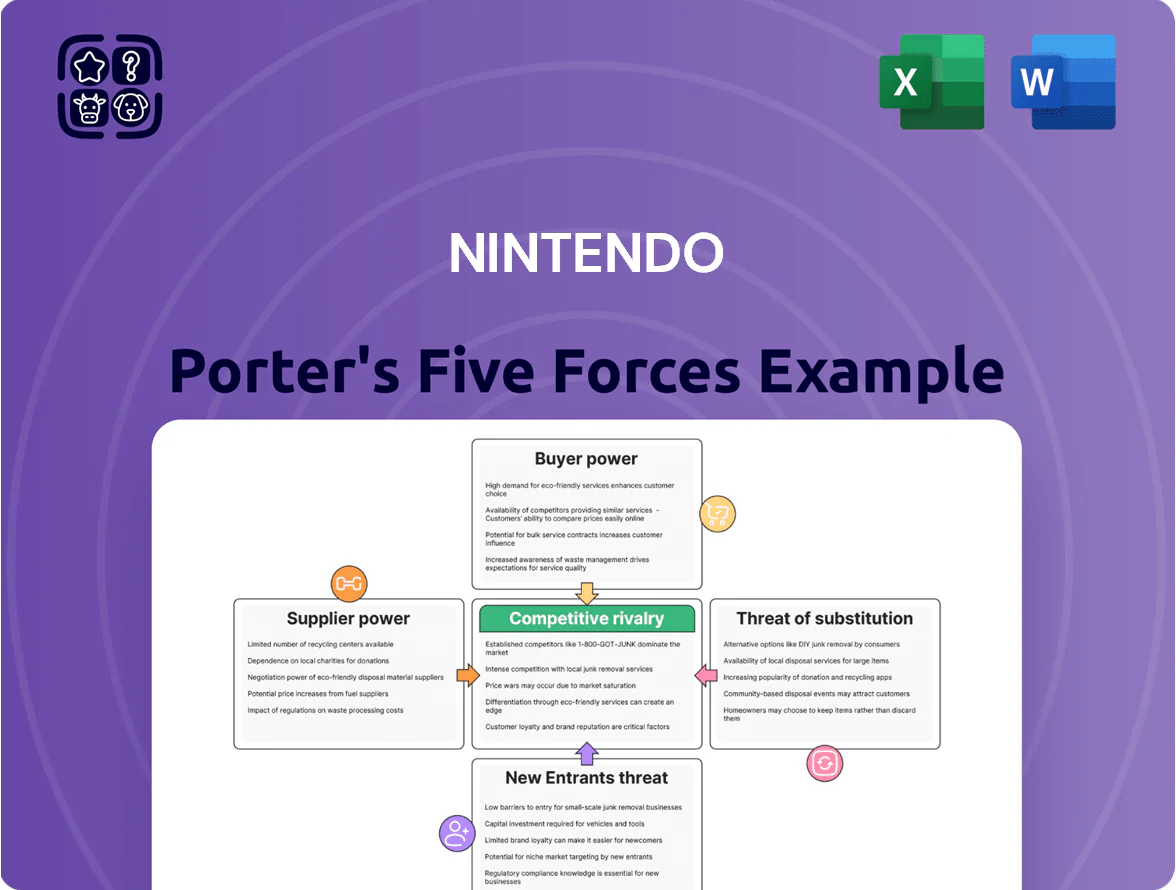

Nintendo faces intense rivalry from Sony and Microsoft, moderate supplier leverage, rising buyer expectations, and evolving substitute threats from mobile/cloud gaming that shape strategic choices and margin pressure; this snapshot highlights competitive levers and emerging risks. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, data-driven implications, and tactical recommendations tailored to Nintendo.

Suppliers Bargaining Power

Concentration of Specialized Semiconductor Suppliers

Nintendo depends on specialized chipmakers—notably NVIDIA for Tegra-class SoCs—creating supplier power as advanced nodes and AI-capable hardware demand rose in late 2025; foundry capacity at TSMC for 5nm/4nm/3nm remained tight with fab utilization >95% and spot premiums up 18% year-over-year.

Diversification of Manufacturing Partners

Nintendo has expanded assembly and component sourcing across Vietnam, Malaysia, Thailand and Mexico; by 2024 about 40% of Switch production shifted outside Japan and China, lowering single-region risk.

This geographic spread creates competition among contract manufacturers like Foxconn and Pegatron, reducing any one supplier’s bargaining power and keeping margins from being squeezed.

Spreading production limits disruption: no single partner controls >25% of Nintendo’s assembly capacity, so unilateral term changes are hard to enforce.

Proprietary Software Development Control

Nintendo tightly controls software via internal studios and strict licenses, so supplier power for content is minimal; Nintendo EPD produced major titles that drove 2024 software sales of ¥1.56 trillion (Nintendo Co., Ltd. FY2024).

Commoditization of Standard Components

For non-specialized parts like plastics, standard memory modules, and basic displays, Nintendo sources from dozens of global vendors; in 2024 Nintendo disclosed procurement across Asia and the Americas, helping keep unit component cost volatility below 3% year-over-year.

These components are largely commoditized and highly substitutable, so Nintendo can switch suppliers if prices rise or quality falls, limiting supplier leverage and keeping bargaining power negligible.

- Many vendors: dozens across Asia/Americas

- Component cost volatility: <3% YoY (2024)

- High substitutability → low supplier power

Strategic Raw Material Procurement

Nintendo depends on rare earths and specific metals—neodymium, cobalt, copper—that face geopolitical supply risk; in 2024 China supplied ~60% of global rare earths, pushing price volatility up to 35% year-over-year for some magnets.

To curb this, Nintendo uses multi-year contracts and strategic procurement, reported R&D + IPP capex of ¥246.3bn in FY2024 supporting supply stability and component sourcing.

By locking prices and volumes via long-term deals, Nintendo reduces exposure to short-term supplier-driven spikes and secures production continuity.

- Multi-year contracts: lower price volatility

- China ~60% of rare earth supply (2024)

- Price swings up to 35% for key magnets (2024)

- FY2024 capex ¥246.3bn supports sourcing

Supplier power muted despite chokepoints: rare earths & SoCs vs. diversified supply

Suppliers have limited bargaining power: specialized SoCs and rare-earths create pockets of leverage (TSMC fab tightness >95% utilization; China ~60% rare earths, magnet prices +35% in 2024), but geographic assembly diversification (40% production outside Japan/China by 2024), multi-year contracts, and commoditized parts (component volatility <3% YoY) keep overall supplier power low.

| Metric | 2024/25 |

|---|---|

| TSMC utilization | >95% |

| Production outside JP/CN | ≈40% |

| Rare earth share (China) | ~60% |

| Magnet price swing | +35% YoY |

| Component volatility | <3% YoY |

What is included in the product

Tailored Porter's Five Forces analysis for Nintendo that uncovers competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and highlights disruptive trends shaping its profitability and strategic defenses.

Concise Porter's Five Forces snapshot for Nintendo—rapidly assess competitive pressures and strategic levers to inform investment or corporate moves.

Customers Bargaining Power

High Brand Loyalty and IP Exclusivity

Nintendo’s exclusive franchises—Mario, The Legend of Zelda, Pokémon—create strong brand loyalty that lowers customer bargaining power; fans can’t get these titles elsewhere so price negotiation is limited. In FY2024 Nintendo reported ¥1.8 trillion revenue and 54% from IP-driven software, showing consumers pay premium prices. This exclusivity sustains hardware/software pricing deep into lifecycle, keeping margins higher than typical console peers.

Price Sensitivity in the Family Segment

Influence of Digital Storefront Policies

As digital downloads rose to 54% of Nintendo software sales by FY2024 (ending Mar 2024), price transparency and instant eShop comparisons have increased customer leverage, pushing Nintendo toward frequent promotions—eShop global sales averaged ~20% off for major titles in 2023. Still, Nintendo’s closed ecosystem—no third-party digital storefronts for first-party titles—caps customer power by preventing alternate digital retailers and limits full-price competition.

Collective Consumer Sentiment and Social Media

Collective social-media sentiment now shapes Nintendo decisions; after the 2020 Joy-Con drift lawsuits and 2021 Twitter backlash over Switch Online changes, Nintendo saw stock volatility and paid repair/legal costs—Joy-Con claims contributed to a 2021 reserve of ¥1.7 billion (about $15.5M) for repairs and settlements.

Negative viral campaigns can force firmware rollbacks or policy shifts; 2023/X (Twitter) metrics show spikes of 100k+ complaint tweets causing rapid PR responses, making consumer voice a real check on strategy.

- Social spikes: 100k+ complaint tweets

- Repair reserve: ¥1.7B (2021)

- Fast policy reversals: weeks not months

Availability of Alternative Entertainment

Customers decide how to use limited leisure time, so Nintendo must compete with many alternatives despite its unique IP—global mobile gaming revenue hit $120B in 2024 and Netflix had 238M subscribers as of Q4 2024, putting steady pressure on Nintendo to justify console and software spending.

If Nintendo stalls on innovation, players can shift discretionary spend to free-to-play mobile titles or streaming, which often cost under $10/month versus higher console-game prices.

- Mobile gaming revenue: $120B (2024)

- Netflix subscribers: 238M (Q4 2024)

- Avg streaming cost: <$10/month

- High churn risk if innovation lags

Nintendo’s IP power cushions margins, but casual, digital and mobile competition heighten price risk

Nintendo’s exclusive IP (Mario, Zelda, Pokémon) and FY2024 ¥1.8T revenue with 54% IP-driven software keep customer bargaining power low for first-party titles, maintaining higher margins (FY2024 operating margin 15.6%).

But 40% casual/family users, 54% digital sales, and $120B mobile gaming (2024) raise price sensitivity and churn risk if prices rise above inflation (Japan CPI 2024: 3.2%).

| Metric | Value |

|---|---|

| FY2024 revenue | ¥1.8T |

| IP-driven software | 54% |

| Operating margin | 15.6% |

| Switch casual share | ~40% |

| Digital share | 54% |

| Mobile gaming | $120B (2024) |

Preview Before You Purchase

Nintendo Porter's Five Forces Analysis

This preview is the exact Nintendo Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples, fully formatted and ready to download.

It includes concise evaluations of competitive rivalry, supplier and buyer power, threats of substitutes and entry, and strategic implications—precisely as shown here upon instant access.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Nintendo faces intense rivalry from Sony and Microsoft, moderate supplier leverage, rising buyer expectations, and evolving substitute threats from mobile/cloud gaming that shape strategic choices and margin pressure; this snapshot highlights competitive levers and emerging risks. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, data-driven implications, and tactical recommendations tailored to Nintendo.

Suppliers Bargaining Power

Concentration of Specialized Semiconductor Suppliers

Nintendo depends on specialized chipmakers—notably NVIDIA for Tegra-class SoCs—creating supplier power as advanced nodes and AI-capable hardware demand rose in late 2025; foundry capacity at TSMC for 5nm/4nm/3nm remained tight with fab utilization >95% and spot premiums up 18% year-over-year.

Diversification of Manufacturing Partners

Nintendo has expanded assembly and component sourcing across Vietnam, Malaysia, Thailand and Mexico; by 2024 about 40% of Switch production shifted outside Japan and China, lowering single-region risk.

This geographic spread creates competition among contract manufacturers like Foxconn and Pegatron, reducing any one supplier’s bargaining power and keeping margins from being squeezed.

Spreading production limits disruption: no single partner controls >25% of Nintendo’s assembly capacity, so unilateral term changes are hard to enforce.

Proprietary Software Development Control

Nintendo tightly controls software via internal studios and strict licenses, so supplier power for content is minimal; Nintendo EPD produced major titles that drove 2024 software sales of ¥1.56 trillion (Nintendo Co., Ltd. FY2024).

Commoditization of Standard Components

For non-specialized parts like plastics, standard memory modules, and basic displays, Nintendo sources from dozens of global vendors; in 2024 Nintendo disclosed procurement across Asia and the Americas, helping keep unit component cost volatility below 3% year-over-year.

These components are largely commoditized and highly substitutable, so Nintendo can switch suppliers if prices rise or quality falls, limiting supplier leverage and keeping bargaining power negligible.

- Many vendors: dozens across Asia/Americas

- Component cost volatility: <3% YoY (2024)

- High substitutability → low supplier power

Strategic Raw Material Procurement

Nintendo depends on rare earths and specific metals—neodymium, cobalt, copper—that face geopolitical supply risk; in 2024 China supplied ~60% of global rare earths, pushing price volatility up to 35% year-over-year for some magnets.

To curb this, Nintendo uses multi-year contracts and strategic procurement, reported R&D + IPP capex of ¥246.3bn in FY2024 supporting supply stability and component sourcing.

By locking prices and volumes via long-term deals, Nintendo reduces exposure to short-term supplier-driven spikes and secures production continuity.

- Multi-year contracts: lower price volatility

- China ~60% of rare earth supply (2024)

- Price swings up to 35% for key magnets (2024)

- FY2024 capex ¥246.3bn supports sourcing

Supplier power muted despite chokepoints: rare earths & SoCs vs. diversified supply

Suppliers have limited bargaining power: specialized SoCs and rare-earths create pockets of leverage (TSMC fab tightness >95% utilization; China ~60% rare earths, magnet prices +35% in 2024), but geographic assembly diversification (40% production outside Japan/China by 2024), multi-year contracts, and commoditized parts (component volatility <3% YoY) keep overall supplier power low.

| Metric | 2024/25 |

|---|---|

| TSMC utilization | >95% |

| Production outside JP/CN | ≈40% |

| Rare earth share (China) | ~60% |

| Magnet price swing | +35% YoY |

| Component volatility | <3% YoY |

What is included in the product

Tailored Porter's Five Forces analysis for Nintendo that uncovers competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and highlights disruptive trends shaping its profitability and strategic defenses.

Concise Porter's Five Forces snapshot for Nintendo—rapidly assess competitive pressures and strategic levers to inform investment or corporate moves.

Customers Bargaining Power

High Brand Loyalty and IP Exclusivity

Nintendo’s exclusive franchises—Mario, The Legend of Zelda, Pokémon—create strong brand loyalty that lowers customer bargaining power; fans can’t get these titles elsewhere so price negotiation is limited. In FY2024 Nintendo reported ¥1.8 trillion revenue and 54% from IP-driven software, showing consumers pay premium prices. This exclusivity sustains hardware/software pricing deep into lifecycle, keeping margins higher than typical console peers.

Price Sensitivity in the Family Segment

Influence of Digital Storefront Policies

As digital downloads rose to 54% of Nintendo software sales by FY2024 (ending Mar 2024), price transparency and instant eShop comparisons have increased customer leverage, pushing Nintendo toward frequent promotions—eShop global sales averaged ~20% off for major titles in 2023. Still, Nintendo’s closed ecosystem—no third-party digital storefronts for first-party titles—caps customer power by preventing alternate digital retailers and limits full-price competition.

Collective Consumer Sentiment and Social Media

Collective social-media sentiment now shapes Nintendo decisions; after the 2020 Joy-Con drift lawsuits and 2021 Twitter backlash over Switch Online changes, Nintendo saw stock volatility and paid repair/legal costs—Joy-Con claims contributed to a 2021 reserve of ¥1.7 billion (about $15.5M) for repairs and settlements.

Negative viral campaigns can force firmware rollbacks or policy shifts; 2023/X (Twitter) metrics show spikes of 100k+ complaint tweets causing rapid PR responses, making consumer voice a real check on strategy.

- Social spikes: 100k+ complaint tweets

- Repair reserve: ¥1.7B (2021)

- Fast policy reversals: weeks not months

Availability of Alternative Entertainment

Customers decide how to use limited leisure time, so Nintendo must compete with many alternatives despite its unique IP—global mobile gaming revenue hit $120B in 2024 and Netflix had 238M subscribers as of Q4 2024, putting steady pressure on Nintendo to justify console and software spending.

If Nintendo stalls on innovation, players can shift discretionary spend to free-to-play mobile titles or streaming, which often cost under $10/month versus higher console-game prices.

- Mobile gaming revenue: $120B (2024)

- Netflix subscribers: 238M (Q4 2024)

- Avg streaming cost: <$10/month

- High churn risk if innovation lags

Nintendo’s IP power cushions margins, but casual, digital and mobile competition heighten price risk

Nintendo’s exclusive IP (Mario, Zelda, Pokémon) and FY2024 ¥1.8T revenue with 54% IP-driven software keep customer bargaining power low for first-party titles, maintaining higher margins (FY2024 operating margin 15.6%).

But 40% casual/family users, 54% digital sales, and $120B mobile gaming (2024) raise price sensitivity and churn risk if prices rise above inflation (Japan CPI 2024: 3.2%).

| Metric | Value |

|---|---|

| FY2024 revenue | ¥1.8T |

| IP-driven software | 54% |

| Operating margin | 15.6% |

| Switch casual share | ~40% |

| Digital share | 54% |

| Mobile gaming | $120B (2024) |

Preview Before You Purchase

Nintendo Porter's Five Forces Analysis

This preview is the exact Nintendo Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples, fully formatted and ready to download.

It includes concise evaluations of competitive rivalry, supplier and buyer power, threats of substitutes and entry, and strategic implications—precisely as shown here upon instant access.