Nippon Paint Holdings Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

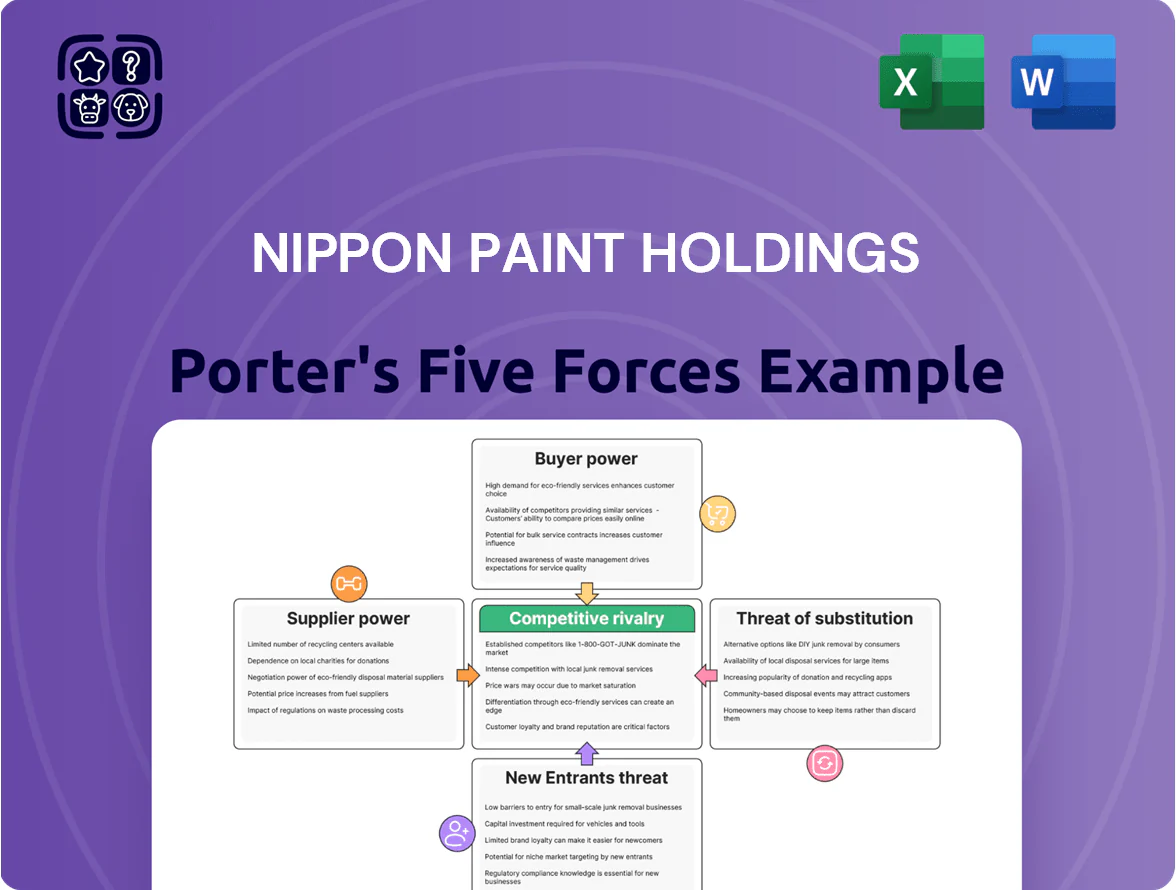

Nippon Paint Holdings faces moderate rivalry from global and regional coatings firms, strong buyer negotiation from industrial clients, and manageable supplier power due to diversified raw material sources.

Threats from new entrants are limited by scale and distribution advantages, while substitutes and regulatory shifts present targeted risks to margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nippon Paint Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Nippon Paint relies on upstream suppliers for titanium dioxide, resins and solvents, exposing margins to global commodity swings; titanium dioxide spiked 35% in 2021–22 and still shows 8–12% annual variability.

By late 2025 supply chains largely stabilized, yet makers of specialized additives retain pricing power, representing ~6–9% of COGS and driving cost pass-through risks.

The firm offsets this via long-term contracts, bulk purchasing and diversified sourcing across Asia, Europe and North America, using scale to secure ~10–15% lower input costs on core chemicals.

Specialized Chemical Dependency

High-performance automotive and marine coatings need specialty resins and pigments supplied by a handful of global chemical giants, giving suppliers high bargaining power; these inputs can represent 15–25% of formulation cost and have lead times of 8–12 weeks. Nippon Paint offsets this via strategic partnerships and joint R&D—its 2024 disclosures show 3 ongoing co-development deals and a 12% capex increase in specialty material projects to secure supply and cut lead times.

Supplier Consolidation Trends

Supplier consolidation in chemicals has cut global midstream suppliers by about 18% from 2015–2023, boosting top-5 share to ~62% in specialty resins by 2023, which tightens alternatives for Nippon Paint and risks higher input costs.

To offset this, Nippon Paint expands vertical integration in pigments and resins and keeps a multi-vendor sourcing policy across 60+ key SKUs, limiting single-supplier exposure to under 15% per commodity.

Energy and Logistics Costs

Suppliers of energy‑intensive inputs pass utility and transport cost swings to paint makers; Nippon Paint reported global energy costs rising ~12% in 2024, squeezing gross margins in some regions.

Third‑party logistics costs hit margins directly across Nippon Paint’s network; freight and warehousing rose ~18% YoY in 2024 for APAC routes, per company disclosures.

Localized production hubs—investments of ¥35.4 billion from 2022–2024—cut average inbound lead times 22% and reduced reliance on global carriers, lowering supplier bargaining power.

- Energy costs +12% (2024)

- Logistics +18% YoY (APAC 2024)

- ¥35.4bn invested in local hubs (2022–24)

- Lead times down 22%

Sustainability and ESG Compliance

Suppliers with strict environmental and sustainability certifications are vital as global regs tighten through 2026; green inputs now account for ~18% of Nippon Paint Holdings' procurement by spend (2024 internal target), rising toward 25% by 2026 to meet decarbonization goals.

These certified suppliers command premiums—estimated 8–15% higher unit costs—forcing Nippon Paint to accept margin pressure or pass costs to customers while shifting product mixes to eco-friendly lines.

Nippon Paint is auditing its supply chain (2024 audit coverage ~60% of spend) to ensure compliance and traceability, balancing higher raw-material costs with efficiency gains and supplier consolidation.

- 2024 green spend ~18%, target 25% by 2026

- Supplier premium ~8–15% on sustainable inputs

- 2024 audit coverage ~60% of procurement spend

- Trade-off: higher costs vs compliance, brand, and eco-product growth

Supply cost pressure: specialty inputs, TiO2 volatility & capex shield margins

Suppliers wield moderate-to-high power: specialty resins/pigments and certified green inputs drive 15–25% of formulation cost and carry 8–15% price premiums; titanium dioxide volatility (±8–12% pa after a 35% 2021–22 spike) and energy/logistics cost rises (energy +12% 2024, freight +18% APAC 2024) squeeze margins, while Nippon Paint limits exposure via multi-vendor sourcing, vertical integration and ¥35.4bn local-hub capex (2022–24).

| Metric | Value |

|---|---|

| TiO2 variability | ±8–12% pa |

| Specialty input share | 15–25% of cost |

| Green spend (2024) | 18% (target 25% 2026) |

| Energy cost change (2024) | +12% |

| Freight APAC (2024) | +18% YoY |

| Local hub capex (2022–24) | ¥35.4bn |

What is included in the product

Tailored analysis of Nippon Paint Holdings' competitive landscape, uncovering key drivers of rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to assess pricing leverage and market resilience.

A concise Porter's Five Forces one-sheet for Nippon Paint Holdings—quickly spot supplier, buyer, entrant, substitute, and rivalry pressures to streamline strategic decisions.

Customers Bargaining Power

Consolidated Automotive OEM Power

Major global automakers—Toyota, Volkswagen, Stellantis, Hyundai—buy coatings in volumes that give them heavy leverage to push prices and specs; OEMs accounted for about 45% of global automotive coatings demand in 2024, raising bargaining power versus suppliers like Nippon Paint Holdings.

Because coatings are essential to vehicle assembly, these OEMs routinely play vendors against each other at renewals, pressuring margins; Nippon Paint noted automotive sales made up roughly 30% of consolidated revenue in FY2024, underscoring exposure.

Nippon Paint counters by selling integrated color-management, application equipment, and proprietary high-performance formulations with multi-year OEM qualifications—barriers that slow switching and preserve pricing, keeping negotiated discounts smaller than raw-volume leverage alone would imply.

Retailer Dominance in DIY Segments

Low Switching Costs for Consumers

Individual consumers in the decorative paint market face very low switching costs—surveys show price and local availability drive 68% of mid-range purchases—so Nippon Paint competes directly with Sherwin-Williams and AkzoNobel on price promotions and distribution. Brand loyalty in this segment is weak; only ~22% cite technical features as the main reason for repeat buys. Nippon Paint is countering by rolling out improved color-matching tech and eco-friendly lines (sales of eco-range rose 14% in FY2024) to deepen preference.

Price Sensitivity in Emerging Markets

- ~48% revenue from price-sensitive regions (FY2024)

- Multi-brand mix: premium + value tiers to retain share

- Price hikes risk share loss vs low-cost locals

Digital Transparency and Comparison

OEMs, APAC retailers dictate paint margins as Nippon fights back with premium, e‑commerce

Large OEMs and retailers wield strong bargaining power—OEMs were ~45% of automotive coatings demand (2024) and ~30% of Nippon Paint revenue (FY2024); APAC chains drove ~45% channel sales, with trade discounts ~8–12%. Digital tools raised DIY/contractor price transparency; online sales +22% (2024). Nippon counters via multi-brand premium/value strategy, proprietary formulations, color tech and e-commerce.

| Metric | 2024 |

|---|---|

| OEM share (auto demand) | ~45% |

| Nippon auto revenue | ~30% FY2024 |

| APAC channel share | ~45% |

| Trade discounts | 8–12% |

| Online sales growth | +22% |

Preview Before You Purchase

Nippon Paint Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Nippon Paint Holdings you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Nippon Paint Holdings faces moderate rivalry from global and regional coatings firms, strong buyer negotiation from industrial clients, and manageable supplier power due to diversified raw material sources.

Threats from new entrants are limited by scale and distribution advantages, while substitutes and regulatory shifts present targeted risks to margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nippon Paint Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Nippon Paint relies on upstream suppliers for titanium dioxide, resins and solvents, exposing margins to global commodity swings; titanium dioxide spiked 35% in 2021–22 and still shows 8–12% annual variability.

By late 2025 supply chains largely stabilized, yet makers of specialized additives retain pricing power, representing ~6–9% of COGS and driving cost pass-through risks.

The firm offsets this via long-term contracts, bulk purchasing and diversified sourcing across Asia, Europe and North America, using scale to secure ~10–15% lower input costs on core chemicals.

Specialized Chemical Dependency

High-performance automotive and marine coatings need specialty resins and pigments supplied by a handful of global chemical giants, giving suppliers high bargaining power; these inputs can represent 15–25% of formulation cost and have lead times of 8–12 weeks. Nippon Paint offsets this via strategic partnerships and joint R&D—its 2024 disclosures show 3 ongoing co-development deals and a 12% capex increase in specialty material projects to secure supply and cut lead times.

Supplier Consolidation Trends

Supplier consolidation in chemicals has cut global midstream suppliers by about 18% from 2015–2023, boosting top-5 share to ~62% in specialty resins by 2023, which tightens alternatives for Nippon Paint and risks higher input costs.

To offset this, Nippon Paint expands vertical integration in pigments and resins and keeps a multi-vendor sourcing policy across 60+ key SKUs, limiting single-supplier exposure to under 15% per commodity.

Energy and Logistics Costs

Suppliers of energy‑intensive inputs pass utility and transport cost swings to paint makers; Nippon Paint reported global energy costs rising ~12% in 2024, squeezing gross margins in some regions.

Third‑party logistics costs hit margins directly across Nippon Paint’s network; freight and warehousing rose ~18% YoY in 2024 for APAC routes, per company disclosures.

Localized production hubs—investments of ¥35.4 billion from 2022–2024—cut average inbound lead times 22% and reduced reliance on global carriers, lowering supplier bargaining power.

- Energy costs +12% (2024)

- Logistics +18% YoY (APAC 2024)

- ¥35.4bn invested in local hubs (2022–24)

- Lead times down 22%

Sustainability and ESG Compliance

Suppliers with strict environmental and sustainability certifications are vital as global regs tighten through 2026; green inputs now account for ~18% of Nippon Paint Holdings' procurement by spend (2024 internal target), rising toward 25% by 2026 to meet decarbonization goals.

These certified suppliers command premiums—estimated 8–15% higher unit costs—forcing Nippon Paint to accept margin pressure or pass costs to customers while shifting product mixes to eco-friendly lines.

Nippon Paint is auditing its supply chain (2024 audit coverage ~60% of spend) to ensure compliance and traceability, balancing higher raw-material costs with efficiency gains and supplier consolidation.

- 2024 green spend ~18%, target 25% by 2026

- Supplier premium ~8–15% on sustainable inputs

- 2024 audit coverage ~60% of procurement spend

- Trade-off: higher costs vs compliance, brand, and eco-product growth

Supply cost pressure: specialty inputs, TiO2 volatility & capex shield margins

Suppliers wield moderate-to-high power: specialty resins/pigments and certified green inputs drive 15–25% of formulation cost and carry 8–15% price premiums; titanium dioxide volatility (±8–12% pa after a 35% 2021–22 spike) and energy/logistics cost rises (energy +12% 2024, freight +18% APAC 2024) squeeze margins, while Nippon Paint limits exposure via multi-vendor sourcing, vertical integration and ¥35.4bn local-hub capex (2022–24).

| Metric | Value |

|---|---|

| TiO2 variability | ±8–12% pa |

| Specialty input share | 15–25% of cost |

| Green spend (2024) | 18% (target 25% 2026) |

| Energy cost change (2024) | +12% |

| Freight APAC (2024) | +18% YoY |

| Local hub capex (2022–24) | ¥35.4bn |

What is included in the product

Tailored analysis of Nippon Paint Holdings' competitive landscape, uncovering key drivers of rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to assess pricing leverage and market resilience.

A concise Porter's Five Forces one-sheet for Nippon Paint Holdings—quickly spot supplier, buyer, entrant, substitute, and rivalry pressures to streamline strategic decisions.

Customers Bargaining Power

Consolidated Automotive OEM Power

Major global automakers—Toyota, Volkswagen, Stellantis, Hyundai—buy coatings in volumes that give them heavy leverage to push prices and specs; OEMs accounted for about 45% of global automotive coatings demand in 2024, raising bargaining power versus suppliers like Nippon Paint Holdings.

Because coatings are essential to vehicle assembly, these OEMs routinely play vendors against each other at renewals, pressuring margins; Nippon Paint noted automotive sales made up roughly 30% of consolidated revenue in FY2024, underscoring exposure.

Nippon Paint counters by selling integrated color-management, application equipment, and proprietary high-performance formulations with multi-year OEM qualifications—barriers that slow switching and preserve pricing, keeping negotiated discounts smaller than raw-volume leverage alone would imply.

Retailer Dominance in DIY Segments

Low Switching Costs for Consumers

Individual consumers in the decorative paint market face very low switching costs—surveys show price and local availability drive 68% of mid-range purchases—so Nippon Paint competes directly with Sherwin-Williams and AkzoNobel on price promotions and distribution. Brand loyalty in this segment is weak; only ~22% cite technical features as the main reason for repeat buys. Nippon Paint is countering by rolling out improved color-matching tech and eco-friendly lines (sales of eco-range rose 14% in FY2024) to deepen preference.

Price Sensitivity in Emerging Markets

- ~48% revenue from price-sensitive regions (FY2024)

- Multi-brand mix: premium + value tiers to retain share

- Price hikes risk share loss vs low-cost locals

Digital Transparency and Comparison

OEMs, APAC retailers dictate paint margins as Nippon fights back with premium, e‑commerce

Large OEMs and retailers wield strong bargaining power—OEMs were ~45% of automotive coatings demand (2024) and ~30% of Nippon Paint revenue (FY2024); APAC chains drove ~45% channel sales, with trade discounts ~8–12%. Digital tools raised DIY/contractor price transparency; online sales +22% (2024). Nippon counters via multi-brand premium/value strategy, proprietary formulations, color tech and e-commerce.

| Metric | 2024 |

|---|---|

| OEM share (auto demand) | ~45% |

| Nippon auto revenue | ~30% FY2024 |

| APAC channel share | ~45% |

| Trade discounts | 8–12% |

| Online sales growth | +22% |

Preview Before You Purchase

Nippon Paint Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Nippon Paint Holdings you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.