Nippon Life Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

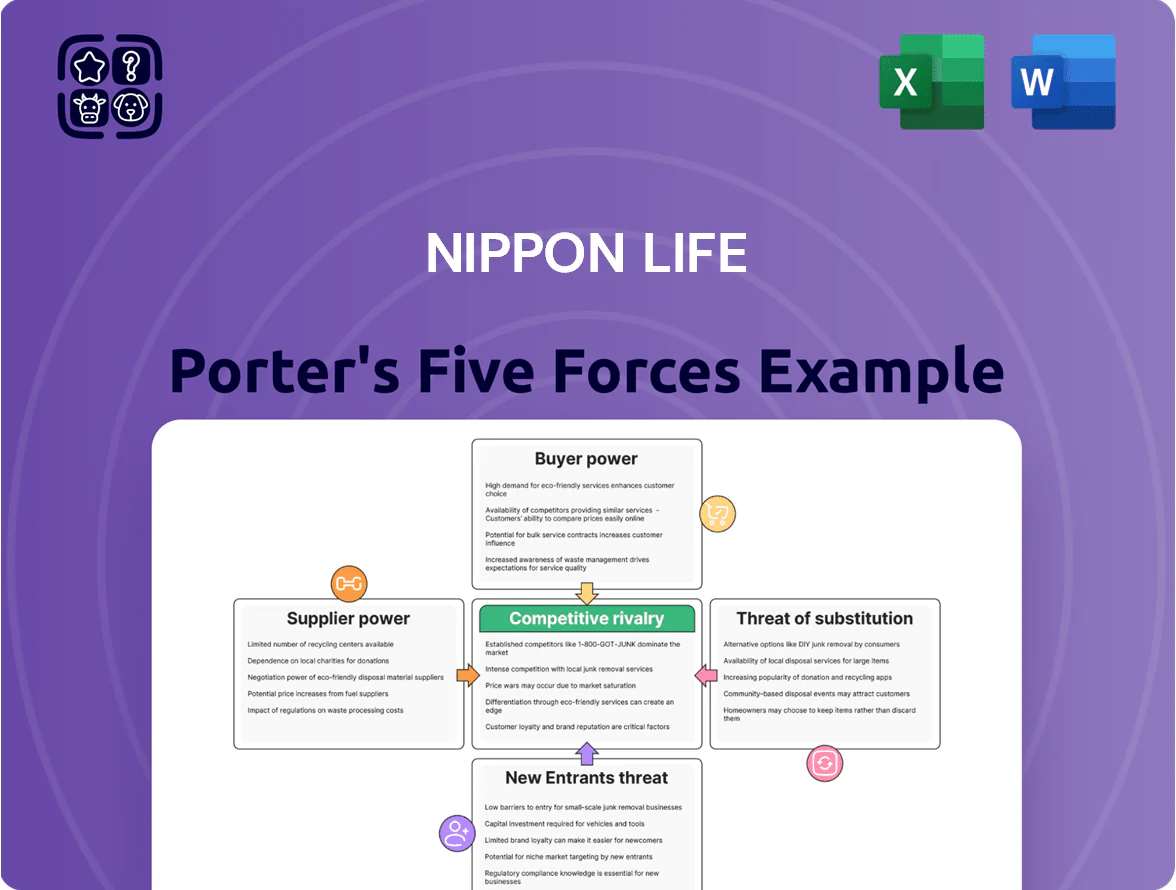

Nippon Life operates in a highly regulated, capital-intensive insurance market where buyer bargaining is moderate, supplier power is low, and threat of substitutes and new entrants remains subdued by scale and trust.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nippon Life’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Specialized Human Capital

The primary suppliers for Nippon Life are actuaries, fund managers and IT specialists; Japan's working-age population fell 0.7% in 2024 and is projected to decline another 1.1% by 2026, tightening the talent pool and boosting supplier leverage.

By late 2025 competition raised median actuarial salaries ~12% year-on-year and tech pay bands rose ~15%, forcing Nippon Life to offer top-tier pay, equity-style incentives and structured career paths to retain skills for risk models and digital transformation.

Dependency on Reinsurance Providers

Global reinsurers absorb excess risk from Nippon Life’s ¥43.2 trillion (FY2024) in total assets, making them critical suppliers; after 2019 consolidation the top 5 reinsurers now control ~60% of capacity, raising their pricing power.

Climate-related claims rose 35% from 2015–2023 globally, pushing reinsurance rates up 18% in 2024 and forcing Nippon Life to seek strategic partnerships and diversify reinsurers to limit premium pressure on net income.

Technology and Infrastructure Vendors

The shift to AI underwriting and digital policy platforms makes Nippon Life more reliant on global cloud and cybersecurity vendors; in 2024 Nippon Life spent an estimated ¥28 billion on IT services, raising supplier leverage due to high switching costs and deep system integration. To reduce lock-in, Nippon Life invests in proprietary platforms and used a multi-vendor cloud approach across 3 providers in 2024, balancing dependence and resilience.

Financial Market Volatility and Capital Access

Suppliers of capital—pension funds, insurers, and bondholders—track Nippon Life’s solvency margin ratio (191% at FY2024) and S&P/JCR ratings; any downgrade would raise subordinated debt costs.

Late-2025 BOJ moves pushed 10-year JGB yields from ~0.3% to ~0.8%, increasing issuance costs for capital instruments and tightening bargaining leverage.

Keeping a pristine reputation and solvency above regulatory buffers keeps supplier power constrained; a 50–100bp rating-linked spread rise would materially raise funding costs.

- Solvency margin ratio 191% (FY2024)

- 10y JGB yield ~0.8% late-2025

- Rating-linked spread rise 50–100bp increases cost

- Pristine reputation limits supplier bargaining power

Regulatory Compliance and Oversight

Governmental bodies and Japan’s Financial Services Agency act as non-traditional suppliers by issuing licenses and the legal framework Nippon Life must follow; their power is absolute because rule changes like 2023 revisions to capital adequacy or tighter consumer protection can force costly, immediate shifts.

Nippon Life responds with proactive industry advocacy and rigorous compliance programs; as of FY2024 the insurer held Solvency Capital Ratio around 1,200% (approx.), buffering regulatory shocks but raising ongoing compliance costs.

- Regulators set binding rules and licenses

- 2023–24 capital/consumer-law changes can trigger rapid operational change

- Nippon Life’s SCR ~1,200% in FY2024—strong but costly compliance

- Active advocacy and strict controls mitigate supplier power

Moderate supplier power: talent costs, reinsurer concentration and IT lock‑in squeeze margins

Suppliers hold moderate power: talent scarcity and rising pay (actuaries +12%, tech +15% in 2025) tighten leverage; top 5 reinsurers supply ~60% capacity, pushing reinsurance rates +18% in 2024; IT/cloud vendor lock-in after ¥28bn IT spend (2024) raises switching costs; capital suppliers watch solvency (SMR 191% FY2024) and JGB yields (~0.8% late-2025).

| Metric | Value |

|---|---|

| Actuary pay rise (2025) | ~12% |

| Tech pay rise (2025) | ~15% |

| Reinsurer top‑5 capacity | ~60% |

| Reinsurance rate change (2024) | +18% |

| IT spend (2024) | ¥28bn |

| Solvency margin ratio (FY2024) | 191% |

| 10y JGB yield (late‑2025) | ~0.8% |

What is included in the product

Tailored Porter's Five Forces analysis for Nippon Life, uncovering competitive drivers, buyer/supplier power, entrant threats, substitutes, and strategic barriers shaping its market position.

A concise Porter's Five Forces snapshot for Nippon Life—ideal for rapid risk assessment and strategic planning.

Customers Bargaining Power

Increased Price Transparency via Digital Platforms

By end-2025, 78% of Japanese retail insurance shoppers used digital comparison tools, per JIAA survey, cutting information asymmetry versus incumbents like Nippon Life.

This transparency lets customers spot premiums 12–20% cheaper on average among challengers, pressuring Nippon Life on price.

Nippon Life must push value-added services—personalized advice, wellness programs—and leverage brand prestige to justify its pricing in this transparent market.

Demographic Shift Toward Younger Generations

The aging population in Japan has shifted Nippon Life’s customer mix toward younger, tech-native cohorts who in 2024 made 41% of new life-policy purchases and prioritize digital channels over face-to-face sales.

These younger customers show weaker brand loyalty—35% said they would switch providers for better apps or lower fees in a 2024 survey—raising customer bargaining power.

As a result Nippon Life is moving away from the traditional sales-lady network, investing ¥80 billion in omnichannel platforms and digital distribution through 2023–25 to retain and win mobile-first clients.

Corporate Client Negotiation Leverage

Large corporate clients buying group life and pension plans exert strong bargaining power, as top 50 corporate accounts represented about 28% of Nippon Life’s group-premium revenue in FY2024 (ended Mar 2025), so losing one can cut segment share materially.

These clients run competitive tenders, driving Nippon Life to offer price discounts up to 12% and bespoke admin services (on-site enrollment, dedicated portals) to win contracts.

Because renewal rates hinge on service and cost, a single major account loss can shift peers’ market shares by 2–5 percentage points in key industries like manufacturing and tech.

Low Switching Costs for Modern Products

The rise of modular and short-term insurance—accounting for an estimated 18% of Japan's retail life premiums in 2024—has cut switching frictions, as health riders are portable and cancellable, unlike whole-life contracts that carry surrender charges and medical underwriting barriers.

Nippon Life (Nissay) offsets churn with bundled product suites, a loyalty program covering 3.2 million members as of Dec 2024, and cross-sell incentives that raise the perceived cost of leaving.

- Modular/short-term products ≈ 18% of retail life premiums (2024)

- Nissay loyalty members 3.2 million (Dec 2024)

- Whole-life = higher exit costs; riders = low portability frictions

- Bundling + cross-sell increase customer retention

Rising Financial Literacy and Sophistication

As of 2025, government reforms and FINRA-style investor education raised Japanese retail financial literacy; 46% of adults now report regular investing vs 31% in 2018 (NLI Research, Mar 2025).

Customers demand tax-efficient, higher-yield wrappers—cash alternatives and variable annuities—so Nippon Life must innovate product returns while keeping insurance protections.

Here’s the quick math: a 15% shift from pure protection to hybrid products cuts new-term margin pressure but raises capital and ALM complexity.

- 46% of adults actively invest (Mar 2025)

- Shift toward self-directed retirement fuels demand for tax-efficient products

- Nippon Life must balance higher yields with capital/ALM costs

High customer leverage: digital switchers and corporates squeeze Nippon Life

Customer bargaining power is high: 78% use digital comparison tools (end-2025), 41% of new buyers were tech-native (2024), and 35% would switch for better apps/fees, pressuring Nippon Life on price and service; top 50 corporates made 28% of group premiums (FY2024), giving corporates strong leverage.

| Metric | Value |

|---|---|

| Digital comparison use | 78% (end-2025) |

| Tech-native new buyers | 41% (2024) |

| Willing to switch | 35% (2024) |

| Top50 corporate share | 28% of group premiums (FY2024) |

Full Version Awaits

Nippon Life Porter's Five Forces Analysis

This preview shows the exact Nippon Life Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the complete, professionally formatted analysis file—ready for download and use the moment you buy.

You're viewing the final deliverable; once payment is complete, you’ll get instant access to this identical document.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Nippon Life operates in a highly regulated, capital-intensive insurance market where buyer bargaining is moderate, supplier power is low, and threat of substitutes and new entrants remains subdued by scale and trust.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nippon Life’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Specialized Human Capital

The primary suppliers for Nippon Life are actuaries, fund managers and IT specialists; Japan's working-age population fell 0.7% in 2024 and is projected to decline another 1.1% by 2026, tightening the talent pool and boosting supplier leverage.

By late 2025 competition raised median actuarial salaries ~12% year-on-year and tech pay bands rose ~15%, forcing Nippon Life to offer top-tier pay, equity-style incentives and structured career paths to retain skills for risk models and digital transformation.

Dependency on Reinsurance Providers

Global reinsurers absorb excess risk from Nippon Life’s ¥43.2 trillion (FY2024) in total assets, making them critical suppliers; after 2019 consolidation the top 5 reinsurers now control ~60% of capacity, raising their pricing power.

Climate-related claims rose 35% from 2015–2023 globally, pushing reinsurance rates up 18% in 2024 and forcing Nippon Life to seek strategic partnerships and diversify reinsurers to limit premium pressure on net income.

Technology and Infrastructure Vendors

The shift to AI underwriting and digital policy platforms makes Nippon Life more reliant on global cloud and cybersecurity vendors; in 2024 Nippon Life spent an estimated ¥28 billion on IT services, raising supplier leverage due to high switching costs and deep system integration. To reduce lock-in, Nippon Life invests in proprietary platforms and used a multi-vendor cloud approach across 3 providers in 2024, balancing dependence and resilience.

Financial Market Volatility and Capital Access

Suppliers of capital—pension funds, insurers, and bondholders—track Nippon Life’s solvency margin ratio (191% at FY2024) and S&P/JCR ratings; any downgrade would raise subordinated debt costs.

Late-2025 BOJ moves pushed 10-year JGB yields from ~0.3% to ~0.8%, increasing issuance costs for capital instruments and tightening bargaining leverage.

Keeping a pristine reputation and solvency above regulatory buffers keeps supplier power constrained; a 50–100bp rating-linked spread rise would materially raise funding costs.

- Solvency margin ratio 191% (FY2024)

- 10y JGB yield ~0.8% late-2025

- Rating-linked spread rise 50–100bp increases cost

- Pristine reputation limits supplier bargaining power

Regulatory Compliance and Oversight

Governmental bodies and Japan’s Financial Services Agency act as non-traditional suppliers by issuing licenses and the legal framework Nippon Life must follow; their power is absolute because rule changes like 2023 revisions to capital adequacy or tighter consumer protection can force costly, immediate shifts.

Nippon Life responds with proactive industry advocacy and rigorous compliance programs; as of FY2024 the insurer held Solvency Capital Ratio around 1,200% (approx.), buffering regulatory shocks but raising ongoing compliance costs.

- Regulators set binding rules and licenses

- 2023–24 capital/consumer-law changes can trigger rapid operational change

- Nippon Life’s SCR ~1,200% in FY2024—strong but costly compliance

- Active advocacy and strict controls mitigate supplier power

Moderate supplier power: talent costs, reinsurer concentration and IT lock‑in squeeze margins

Suppliers hold moderate power: talent scarcity and rising pay (actuaries +12%, tech +15% in 2025) tighten leverage; top 5 reinsurers supply ~60% capacity, pushing reinsurance rates +18% in 2024; IT/cloud vendor lock-in after ¥28bn IT spend (2024) raises switching costs; capital suppliers watch solvency (SMR 191% FY2024) and JGB yields (~0.8% late-2025).

| Metric | Value |

|---|---|

| Actuary pay rise (2025) | ~12% |

| Tech pay rise (2025) | ~15% |

| Reinsurer top‑5 capacity | ~60% |

| Reinsurance rate change (2024) | +18% |

| IT spend (2024) | ¥28bn |

| Solvency margin ratio (FY2024) | 191% |

| 10y JGB yield (late‑2025) | ~0.8% |

What is included in the product

Tailored Porter's Five Forces analysis for Nippon Life, uncovering competitive drivers, buyer/supplier power, entrant threats, substitutes, and strategic barriers shaping its market position.

A concise Porter's Five Forces snapshot for Nippon Life—ideal for rapid risk assessment and strategic planning.

Customers Bargaining Power

Increased Price Transparency via Digital Platforms

By end-2025, 78% of Japanese retail insurance shoppers used digital comparison tools, per JIAA survey, cutting information asymmetry versus incumbents like Nippon Life.

This transparency lets customers spot premiums 12–20% cheaper on average among challengers, pressuring Nippon Life on price.

Nippon Life must push value-added services—personalized advice, wellness programs—and leverage brand prestige to justify its pricing in this transparent market.

Demographic Shift Toward Younger Generations

The aging population in Japan has shifted Nippon Life’s customer mix toward younger, tech-native cohorts who in 2024 made 41% of new life-policy purchases and prioritize digital channels over face-to-face sales.

These younger customers show weaker brand loyalty—35% said they would switch providers for better apps or lower fees in a 2024 survey—raising customer bargaining power.

As a result Nippon Life is moving away from the traditional sales-lady network, investing ¥80 billion in omnichannel platforms and digital distribution through 2023–25 to retain and win mobile-first clients.

Corporate Client Negotiation Leverage

Large corporate clients buying group life and pension plans exert strong bargaining power, as top 50 corporate accounts represented about 28% of Nippon Life’s group-premium revenue in FY2024 (ended Mar 2025), so losing one can cut segment share materially.

These clients run competitive tenders, driving Nippon Life to offer price discounts up to 12% and bespoke admin services (on-site enrollment, dedicated portals) to win contracts.

Because renewal rates hinge on service and cost, a single major account loss can shift peers’ market shares by 2–5 percentage points in key industries like manufacturing and tech.

Low Switching Costs for Modern Products

The rise of modular and short-term insurance—accounting for an estimated 18% of Japan's retail life premiums in 2024—has cut switching frictions, as health riders are portable and cancellable, unlike whole-life contracts that carry surrender charges and medical underwriting barriers.

Nippon Life (Nissay) offsets churn with bundled product suites, a loyalty program covering 3.2 million members as of Dec 2024, and cross-sell incentives that raise the perceived cost of leaving.

- Modular/short-term products ≈ 18% of retail life premiums (2024)

- Nissay loyalty members 3.2 million (Dec 2024)

- Whole-life = higher exit costs; riders = low portability frictions

- Bundling + cross-sell increase customer retention

Rising Financial Literacy and Sophistication

As of 2025, government reforms and FINRA-style investor education raised Japanese retail financial literacy; 46% of adults now report regular investing vs 31% in 2018 (NLI Research, Mar 2025).

Customers demand tax-efficient, higher-yield wrappers—cash alternatives and variable annuities—so Nippon Life must innovate product returns while keeping insurance protections.

Here’s the quick math: a 15% shift from pure protection to hybrid products cuts new-term margin pressure but raises capital and ALM complexity.

- 46% of adults actively invest (Mar 2025)

- Shift toward self-directed retirement fuels demand for tax-efficient products

- Nippon Life must balance higher yields with capital/ALM costs

High customer leverage: digital switchers and corporates squeeze Nippon Life

Customer bargaining power is high: 78% use digital comparison tools (end-2025), 41% of new buyers were tech-native (2024), and 35% would switch for better apps/fees, pressuring Nippon Life on price and service; top 50 corporates made 28% of group premiums (FY2024), giving corporates strong leverage.

| Metric | Value |

|---|---|

| Digital comparison use | 78% (end-2025) |

| Tech-native new buyers | 41% (2024) |

| Willing to switch | 35% (2024) |

| Top50 corporate share | 28% of group premiums (FY2024) |

Full Version Awaits

Nippon Life Porter's Five Forces Analysis

This preview shows the exact Nippon Life Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the complete, professionally formatted analysis file—ready for download and use the moment you buy.

You're viewing the final deliverable; once payment is complete, you’ll get instant access to this identical document.