Nisshin Seifun Porter's Five Forces Analysis

From Overview to Strategy Blueprint

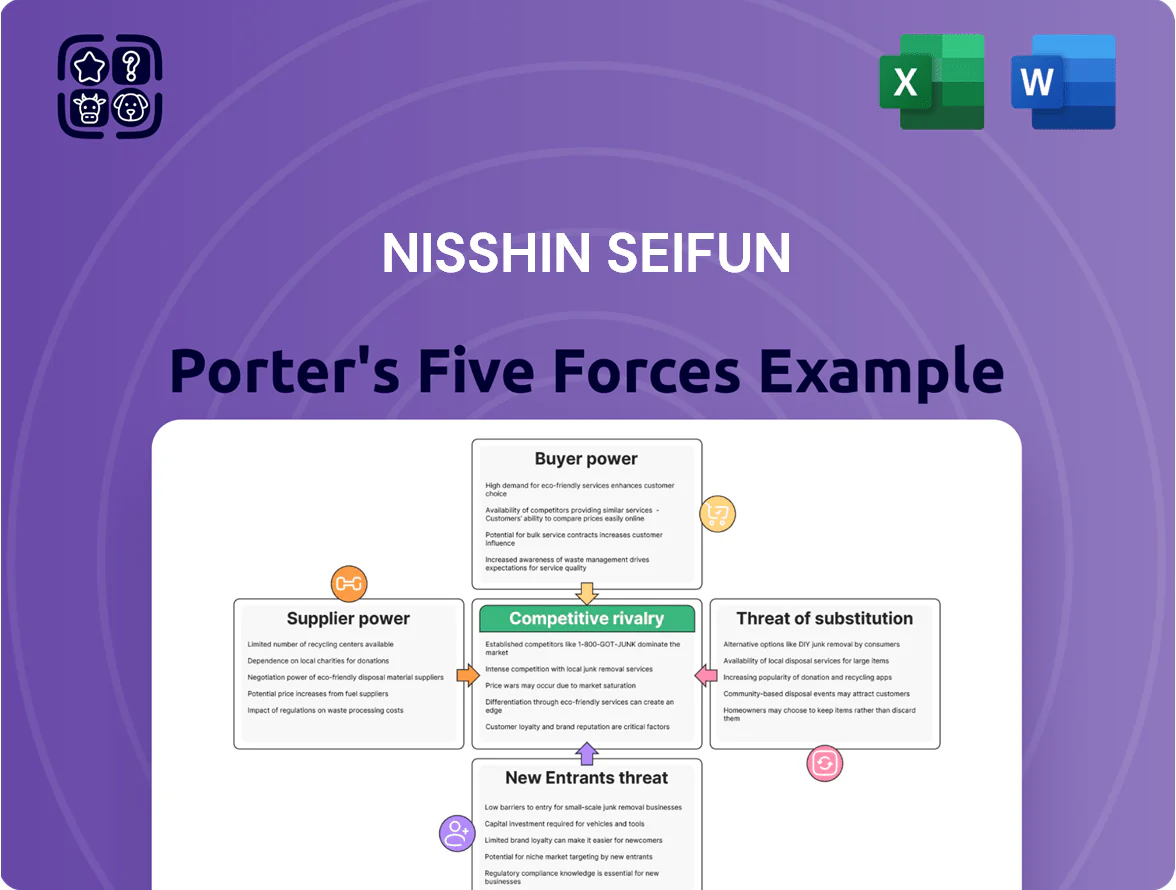

Nisshin Seifun faces moderate buyer power and fragmentation among suppliers, while scale, brand strength, and distribution networks limit new entrants and intensify rivalry in staple foods and ingredients.

Suppliers Bargaining Power

Governmental Control of Wheat Imports

The Japanese Ministry of Agriculture, Forestry and Fisheries tightly controls wheat imports and pricing to protect food security, meaning Nisshin Seifun cannot directly negotiate with global suppliers and acts as a price taker for ~60–70% of its milling input (2024 trade data: Japan imported 3.2 million tonnes of wheat, MAFF-managed quotas cover ~85%).

This centralized system raises exposure to policy shifts: MAFF-set resale prices and tariff-rate quota adjustments in 2023–2024 caused domestic wheat cost swings of ±8–12%, directly hitting Nisshin Seifun’s gross margin on flour and starch products.

Global Commodity Market Volatility

Fluctuations in international wheat prices—up 28% year-on-year in 2024 after Black Sea disruptions—drive procurement cost swings for Nisshin Seifun, since global supply/demand set the floor. The firm uses hedging (futures/options) to smooth volatility, but spot prices rose 18% in H1 2024, squeezing margins. Persistent input-price risk forces efficiency gains or retail price hikes to protect operating margin.

Energy and Logistics Costs

Suppliers of energy and transportation exert moderate bargaining power because flour milling and distribution are energy-intensive; in 2024 Japan industrial electricity prices rose ~6% YoY and diesel jumped ~18% YoY, raising input costs for Nisshin Seifun. Labor shortages in Japan’s logistics cut trunking capacity by an estimated 5–8% in 2023, lifting freight premiums; Nisshin must secure long-term contracts and collaborative routing to stabilize margins.

Climate Change and Crop Resilience

Climate-driven extreme weather cut North American and Australian wheat yields by up to 15% in 2023–24, constraining supply of high-protein grades Nisshin Seifun needs for premium flours and raising spot premiums by ~18% vs 2021 levels.

Suppliers that deliver climate-resilient, high-yield varieties gain pricing power as global stock-to-use ratios tightened to ~18% in 2024, increasing Nisshin’s sourcing risk and cost volatility.

- 2023–24 yield drops ~15%

- Spot premiums up ~18% vs 2021

- Global stock-to-use ~18% in 2024

- Resilient suppliers gain pricing power

Specialized Ingredient Providers

For processed and health food lines, Nisshin Seifun depends on niche suppliers for functional ingredients, additives, and specialized packaging; many hold proprietary tech or unique sourcing, giving them greater bargaining power versus commodity vendors.

As of FY2024, specialized ingredient spend estimated ~12% of COGS, so supplier concentration risk could materially affect margins; diversifying suppliers and qualifying alternates reduces supply disruption risk.

- Specialized spend ≈12% of COGS (FY2024)

- Proprietary suppliers = higher price/terms leverage

- Diversification cuts disruption and margin risk

Nisshin Seifun margin risk: MAFF-driven wheat exposure, rising input & supplier concentration

MAFF control makes Nisshin Seifun a price taker on ~60–70% of wheat (Japan imported 3.2m t in 2024; MAFF quotas ~85%), exposing margins to policy and spot swings (wheat +28% YoY 2024; spot +18% H1 2024). Energy/diesel rose ~6%/18% in 2024; specialized ingredients ≈12% of COGS (FY2024), raising supplier concentration risk.

| Metric | 2024 |

|---|---|

| Japan wheat imports | 3.2m t |

| MAFF quota coverage | ~85% |

| Wheat price change | +28% YoY |

| Specialized spend | ≈12% COGS |

What is included in the product

Tailored exclusively for Nisshin Seifun, this Porter’s Five Forces overview uncovers key drivers of competition, supplier and buyer power, substitutes, and entry barriers affecting its pricing and profitability.

A concise Porter's Five Forces snapshot for Nisshin Seifun—boiling complex industry dynamics into one-sheet clarity for faster strategic decisions.

Customers Bargaining Power

Retailer Consolidation and Dominance

Large retail groups in Japan like Aeon (2024 net sales ¥8.6 trillion) and Seven & i Holdings (2024 net sales ¥6.4 trillion) push strong bargaining power via huge purchasing volumes, forcing lower wholesale prices and deeper promotional support from food makers.

They also extract favorable payment terms—trade receivables stretch—pressuring Nisshin Seifun’s margins and working capital; in 2024 Japan grocery consolidation left top 5 chains with ~45% market share.

Nisshin Seifun must refresh SKUs and launch private-label partnerships regularly; product innovation and co-branded promotions kept its retail penetration stable in 2023–24.

Growth of Private Label Brands

Retailers’ private-label flour and pasta now account for roughly 18–22% of Japan’s category sales (2024 Kantar), directly squeezing Nisshin Seifun’s branded volumes and raising customer bargaining power.

Buyers can switch to higher-margin store brands if Nisshin Seifun fails to differentiate on price or value, pressuring margins and forcing promotional spend.

Nisshin Seifun counters with premiumization and unique nutrition claims—enzyme-treated flours and fiber-fortified pastas—where private labels held only ~6% share in premium SKUs (IRI 2024).

Industrial Bakery and Food Service Demands

B2B buyers like industrial bakeries and convenience-store chains demand large, spec-driven flour volumes; top customers can represent 20–35% of a miller’s revenue, so they push hard on price and run competitive bids among leading millers. These buyers are highly price-sensitive—industry tenders cut margins by 3–6 percentage points—and expect tight batch-to-batch consistency and technical support. To retain accounts, Nisshin Seifun must deliver superior R&D-backed formulation support, <0.5% quality variance, and reliable logistic SLAs.

Consumer Price Sensitivity

End consumers in Japan are highly price-sensitive for staples like flour and bread; during 2023–2024 food inflation averaged about 3–4% annually, and a 5% price rise often cut volume demand noticeably.

This sensitivity constrains Nisshin Seifun’s ability to pass higher wheat costs (Russian and Ukrainian supply fluctuations pushed global wheat up ~20% in 2022–23) without losing sales.

Strong brand loyalty cushions some impact—Nisshin held ~15–18% domestic flour market share in 2024—but cheaper private-label and discount brands constantly threaten share.

- Food inflation 2023–24: 3–4%

- Global wheat jump ~20% (2022–23)

- Nisshin Seifun domestic flour share 15–18% (2024)

- 5% price rise often lowers volume

Digital Transformation in Procurement

Digital procurement platforms and e-commerce let retail and industrial buyers compare prices and specs instantly, cutting information asymmetry that once favored big millers; global B2B e-procurement hit $5.9 trillion in 2023, raising buyer leverage.

Nisshin Seifun must deploy its own digital tools and analytics—CRM-driven personalization, demand forecasting, and dynamic pricing—to boost repeat orders and protect margins.

- 2023 B2B e-procurement: $5.9T

- Use CRM + forecasting to raise retention

- Transparency increases price pressure

Retailer power, private labels rising—premium SKUs & digital tools defend margins

Large retailers (Aeon ¥8.6T, Seven & i ¥6.4T in 2024) and B2B tenders give customers high bargaining power, pushing lower wholesale prices, longer payment terms, and tighter specs that shave margins 3–6ppt; private-labels hold 18–22% of category sales (Kantar 2024) while Nisshin Seifun kept 15–18% flour share (2024), so premium SKUs and digital tools are key to defend price and volume.

| Metric | 2023–24 |

|---|---|

| Aeon net sales | ¥8.6T (2024) |

| Seven & i net sales | ¥6.4T (2024) |

| Private-label share | 18–22% (Kantar 2024) |

| Nisshin Seifun flour share | 15–18% (2024) |

| Food inflation | 3–4% (2023–24) |

| B2B margin hit | 3–6 ppt (tenders) |

What You See Is What You Get

Nisshin Seifun Porter's Five Forces Analysis

This preview shows the exact Nisshin Seifun Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; once payment is complete, you’ll get instant access to this same file. No surprises, no setup required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Nisshin Seifun faces moderate buyer power and fragmentation among suppliers, while scale, brand strength, and distribution networks limit new entrants and intensify rivalry in staple foods and ingredients.

Suppliers Bargaining Power

Governmental Control of Wheat Imports

The Japanese Ministry of Agriculture, Forestry and Fisheries tightly controls wheat imports and pricing to protect food security, meaning Nisshin Seifun cannot directly negotiate with global suppliers and acts as a price taker for ~60–70% of its milling input (2024 trade data: Japan imported 3.2 million tonnes of wheat, MAFF-managed quotas cover ~85%).

This centralized system raises exposure to policy shifts: MAFF-set resale prices and tariff-rate quota adjustments in 2023–2024 caused domestic wheat cost swings of ±8–12%, directly hitting Nisshin Seifun’s gross margin on flour and starch products.

Global Commodity Market Volatility

Fluctuations in international wheat prices—up 28% year-on-year in 2024 after Black Sea disruptions—drive procurement cost swings for Nisshin Seifun, since global supply/demand set the floor. The firm uses hedging (futures/options) to smooth volatility, but spot prices rose 18% in H1 2024, squeezing margins. Persistent input-price risk forces efficiency gains or retail price hikes to protect operating margin.

Energy and Logistics Costs

Suppliers of energy and transportation exert moderate bargaining power because flour milling and distribution are energy-intensive; in 2024 Japan industrial electricity prices rose ~6% YoY and diesel jumped ~18% YoY, raising input costs for Nisshin Seifun. Labor shortages in Japan’s logistics cut trunking capacity by an estimated 5–8% in 2023, lifting freight premiums; Nisshin must secure long-term contracts and collaborative routing to stabilize margins.

Climate Change and Crop Resilience

Climate-driven extreme weather cut North American and Australian wheat yields by up to 15% in 2023–24, constraining supply of high-protein grades Nisshin Seifun needs for premium flours and raising spot premiums by ~18% vs 2021 levels.

Suppliers that deliver climate-resilient, high-yield varieties gain pricing power as global stock-to-use ratios tightened to ~18% in 2024, increasing Nisshin’s sourcing risk and cost volatility.

- 2023–24 yield drops ~15%

- Spot premiums up ~18% vs 2021

- Global stock-to-use ~18% in 2024

- Resilient suppliers gain pricing power

Specialized Ingredient Providers

For processed and health food lines, Nisshin Seifun depends on niche suppliers for functional ingredients, additives, and specialized packaging; many hold proprietary tech or unique sourcing, giving them greater bargaining power versus commodity vendors.

As of FY2024, specialized ingredient spend estimated ~12% of COGS, so supplier concentration risk could materially affect margins; diversifying suppliers and qualifying alternates reduces supply disruption risk.

- Specialized spend ≈12% of COGS (FY2024)

- Proprietary suppliers = higher price/terms leverage

- Diversification cuts disruption and margin risk

Nisshin Seifun margin risk: MAFF-driven wheat exposure, rising input & supplier concentration

MAFF control makes Nisshin Seifun a price taker on ~60–70% of wheat (Japan imported 3.2m t in 2024; MAFF quotas ~85%), exposing margins to policy and spot swings (wheat +28% YoY 2024; spot +18% H1 2024). Energy/diesel rose ~6%/18% in 2024; specialized ingredients ≈12% of COGS (FY2024), raising supplier concentration risk.

| Metric | 2024 |

|---|---|

| Japan wheat imports | 3.2m t |

| MAFF quota coverage | ~85% |

| Wheat price change | +28% YoY |

| Specialized spend | ≈12% COGS |

What is included in the product

Tailored exclusively for Nisshin Seifun, this Porter’s Five Forces overview uncovers key drivers of competition, supplier and buyer power, substitutes, and entry barriers affecting its pricing and profitability.

A concise Porter's Five Forces snapshot for Nisshin Seifun—boiling complex industry dynamics into one-sheet clarity for faster strategic decisions.

Customers Bargaining Power

Retailer Consolidation and Dominance

Large retail groups in Japan like Aeon (2024 net sales ¥8.6 trillion) and Seven & i Holdings (2024 net sales ¥6.4 trillion) push strong bargaining power via huge purchasing volumes, forcing lower wholesale prices and deeper promotional support from food makers.

They also extract favorable payment terms—trade receivables stretch—pressuring Nisshin Seifun’s margins and working capital; in 2024 Japan grocery consolidation left top 5 chains with ~45% market share.

Nisshin Seifun must refresh SKUs and launch private-label partnerships regularly; product innovation and co-branded promotions kept its retail penetration stable in 2023–24.

Growth of Private Label Brands

Retailers’ private-label flour and pasta now account for roughly 18–22% of Japan’s category sales (2024 Kantar), directly squeezing Nisshin Seifun’s branded volumes and raising customer bargaining power.

Buyers can switch to higher-margin store brands if Nisshin Seifun fails to differentiate on price or value, pressuring margins and forcing promotional spend.

Nisshin Seifun counters with premiumization and unique nutrition claims—enzyme-treated flours and fiber-fortified pastas—where private labels held only ~6% share in premium SKUs (IRI 2024).

Industrial Bakery and Food Service Demands

B2B buyers like industrial bakeries and convenience-store chains demand large, spec-driven flour volumes; top customers can represent 20–35% of a miller’s revenue, so they push hard on price and run competitive bids among leading millers. These buyers are highly price-sensitive—industry tenders cut margins by 3–6 percentage points—and expect tight batch-to-batch consistency and technical support. To retain accounts, Nisshin Seifun must deliver superior R&D-backed formulation support, <0.5% quality variance, and reliable logistic SLAs.

Consumer Price Sensitivity

End consumers in Japan are highly price-sensitive for staples like flour and bread; during 2023–2024 food inflation averaged about 3–4% annually, and a 5% price rise often cut volume demand noticeably.

This sensitivity constrains Nisshin Seifun’s ability to pass higher wheat costs (Russian and Ukrainian supply fluctuations pushed global wheat up ~20% in 2022–23) without losing sales.

Strong brand loyalty cushions some impact—Nisshin held ~15–18% domestic flour market share in 2024—but cheaper private-label and discount brands constantly threaten share.

- Food inflation 2023–24: 3–4%

- Global wheat jump ~20% (2022–23)

- Nisshin Seifun domestic flour share 15–18% (2024)

- 5% price rise often lowers volume

Digital Transformation in Procurement

Digital procurement platforms and e-commerce let retail and industrial buyers compare prices and specs instantly, cutting information asymmetry that once favored big millers; global B2B e-procurement hit $5.9 trillion in 2023, raising buyer leverage.

Nisshin Seifun must deploy its own digital tools and analytics—CRM-driven personalization, demand forecasting, and dynamic pricing—to boost repeat orders and protect margins.

- 2023 B2B e-procurement: $5.9T

- Use CRM + forecasting to raise retention

- Transparency increases price pressure

Retailer power, private labels rising—premium SKUs & digital tools defend margins

Large retailers (Aeon ¥8.6T, Seven & i ¥6.4T in 2024) and B2B tenders give customers high bargaining power, pushing lower wholesale prices, longer payment terms, and tighter specs that shave margins 3–6ppt; private-labels hold 18–22% of category sales (Kantar 2024) while Nisshin Seifun kept 15–18% flour share (2024), so premium SKUs and digital tools are key to defend price and volume.

| Metric | 2023–24 |

|---|---|

| Aeon net sales | ¥8.6T (2024) |

| Seven & i net sales | ¥6.4T (2024) |

| Private-label share | 18–22% (Kantar 2024) |

| Nisshin Seifun flour share | 15–18% (2024) |

| Food inflation | 3–4% (2023–24) |

| B2B margin hit | 3–6 ppt (tenders) |

What You See Is What You Get

Nisshin Seifun Porter's Five Forces Analysis

This preview shows the exact Nisshin Seifun Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; once payment is complete, you’ll get instant access to this same file. No surprises, no setup required.