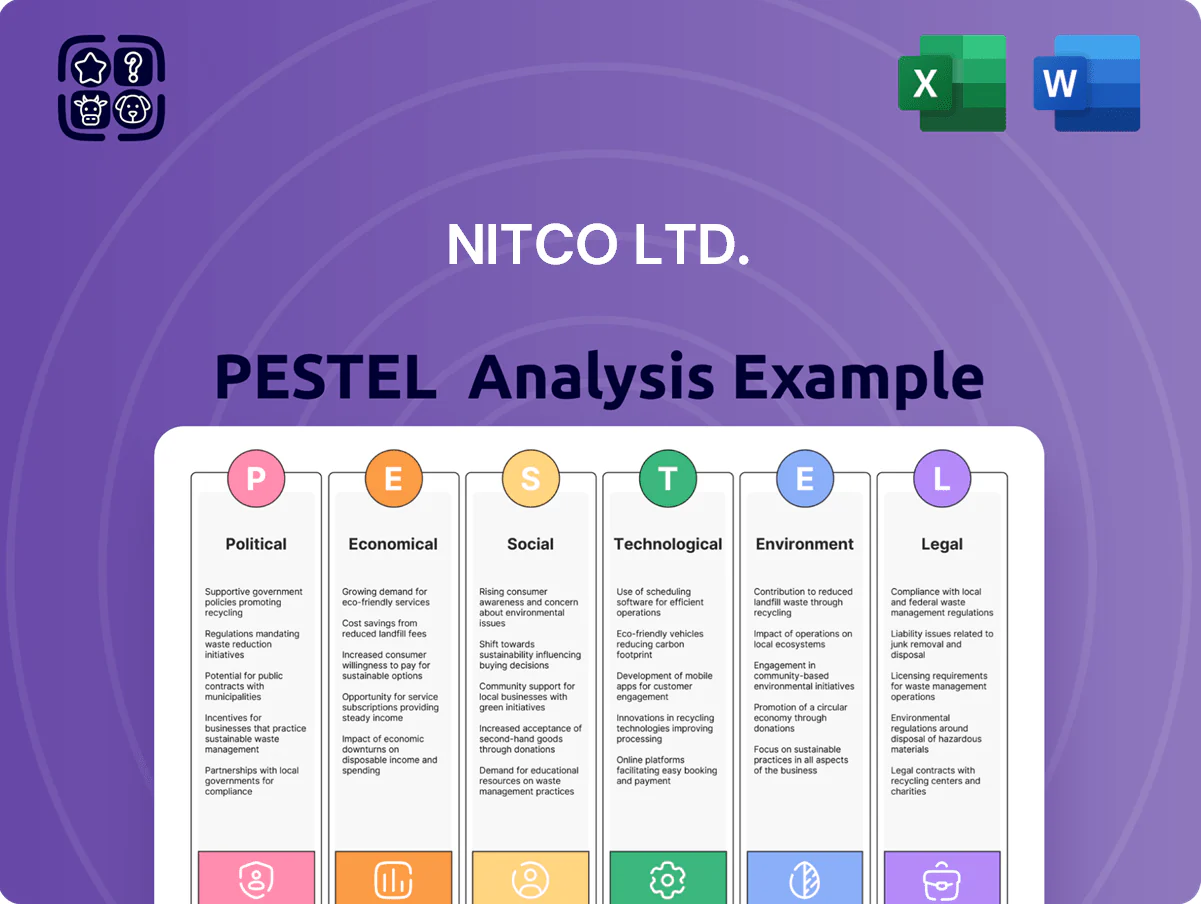

Nitco Ltd. PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Nitco Ltd. faces shifting regulatory, economic, and environmental tides that will redefine its growth trajectory—our PESTLE snapshot highlights these critical external drivers and immediate strategic implications. Purchase the full analysis for a detailed, actionable breakdown of political risks, market trends, tech disruptions, and sustainability pressures tailored to Nitco’s markets. Download now to turn external insight into competitive advantage.

Political factors

Government Infrastructure Development Initiatives

The Indian government’s Gati Shakti plan and record infrastructure outlay—central capital expenditure of Rs 13.2 lakh crore in FY2025—drive demand for Nitco’s high-durability tiles for roads, airports and stations.

By end-2025, elevated allocations to airports and railway redevelopments, part of a Rs 3.2 lakh crore transport upgrade push, underpin multi-year institutional projects for Nitco’s project division.

This political commitment to modernization secures a steady pipeline of large-scale contracts, supporting revenue visibility and project-order book growth for Nitco.

Housing for All and Urban Development

The extension of PMAY into late 2025, targeting completion of 12 million houses by 2025 under various components, boosts affordable and mid-segment housing, increasing demand for tiles; India’s housing starts rose 8% YoY in 2024 supporting construction material consumption. Nitco stands to gain as developers prefer reliable domestic suppliers to meet government timelines, and its FY25 tile segment revenue growth consensus at ~10–12% reflects this tailwind. These policies stabilize the residential market, offering predictable demand for wall and floor solutions and reducing order volatility for organized tile makers.

Trade Policies and Anti Dumping Duties

The Indian government enforces anti-dumping duties on ceramic and vitrified tile imports from China, Vietnam and UAE; duties introduced in 2023–24 ranged from 10–25% on select lines to curb cheap imports, protecting firms like Nitco Ltd. This trade protection helps Nitco defend domestic market share—Nitco reported 2024 domestic revenue of ~INR 810 crore—supporting pricing power amid import-led competition.

Make in India and Manufacturing Incentives

The Make in India push gives Nitco access to fiscal incentives and streamlined approvals, supporting planned capacity expansion; central PLI schemes allocated over INR 1.97 lakh crore (2021–26) have spurred manufacturing investments relevant to tiles and ceramics suppliers.

Alignment with national goals lets Nitco tap state subsidies (e.g., Maharashtra/ Gujarat capex incentives) and tax benefits, improving margins and export competitiveness.

Policy support accelerates tech upgrades and import substitution for premium marble/mosaic lines, aiding self-reliance and potential 5–8% annual capacity growth.

- Access to central PLI and state capex subsidies

- Streamlined approvals reduce time-to-market

- Encourages tech investment and import substitution

- Supports targeted 5–8% capacity growth

Geopolitical Relations and Export Opportunities

India's strengthened diplomatic and trade ties with Middle Eastern and Western nations have expanded Nitco Ltd.'s export corridors, contributing to exports rising ~18% in FY2024-25 versus FY2022-23, per industry trade data.

Political stability and bilateral trade agreements — including reduced tariffs under recent India-GCC and India-EU engagements — enable Nitco to diversify revenue, lowering domestic dependence from 78% to ~62% of sales in 2025.

Shifts in global alliances or regional conflicts could disrupt supply chains and tariffs, so Nitco must keep agile distribution strategies, contingency sourcing, and flexible pricing to mitigate exposure.

- Exports +18% (FY2024-25 vs FY2022-23)

- Domestic sales share reduced from 78% to ~62% in 2025

- Risks: alliance shifts, regional conflicts, tariff changes

- Mitigation: agile distribution, contingency sourcing, flexible pricing

Govt capex, PMAY & anti-dumping fuel Nitco: FY25 tile growth 10–12%, exports +18%

Strong government capex (Rs 13.2 lakh crore FY2025) and PMAY extension boost institutional and housing demand, supporting Nitco’s FY25 tile revenue growth ~10–12% and domestic revenue ~INR 810cr; anti-dumping duties (10–25%) protect market share; exports +18% (FY24–25) cut domestic share from 78% to ~62%, enabling diversified revenue but requiring supply-chain agility.

| Metric | Value |

|---|---|

| Central capex FY25 | Rs 13.2 lakh crore |

| Nitco domestic rev 2024 | ~INR 810 crore |

| Tile rev growth FY25 est | 10–12% |

| Exports growth FY24–25 | +18% |

| Import duties | 10–25% |

What is included in the product

Explores how macro-environmental factors uniquely affect Nitco Ltd. across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current market and regulatory trends relevant to its region and tile/ceramics industry.

Condensed PESTLE insights for Nitco Ltd., organized by factor to ease risk assessment and strategic planning during meetings or client presentations.

Economic factors

Real Estate Market Growth Trajectory

By end-2025 Indian real estate saw robust growth with residential absorption up ~18% y/y and commercial leasing rising ~12% y/y, boosting developer launches to record levels; this elevated construction activity directly increased demand for premium finishes. Nitco benefited from higher volumes in premium vitrified tiles and marble, with reported volume growth of ~15–20% in FY2024–25 across key urban markets. The construction sector's economic health remains the primary driver of Nitco’s topline and margins.

Impact of Interest Rate Cycles

RBI's 2025 stance, with repo at 6.5% in Jan 2025 and CPI easing to 4.8% y/y in Q4 2024, improves predictability for housing finance but leaves sensitivity to rate moves; a 100 bp hike historically cuts housing demand ~8-10%, risking lower renovation spend.

Nitco should mitigate liquidity-driven sales volatility by diversifying SKU pricing—entry, mid, premium—and targeting price-elastic segments; trade receivable days rose 12% in 2024 for tiles sector, underlining developer cash-flow pressure.

Energy Cost Volatility and Kiln Operations

The manufacturing of ceramic tiles is energy-intensive, with Nitco’s kiln operations sensitive to natural gas and electricity prices; global energy volatility in 2025 saw natural gas average EU$8.5/MMBtu and electricity up 14% YoY, prompting Nitco to adopt strict cost-management and peak-shaving measures.

High fuel costs compressed gross margins—Nitco reported energy-related input costs rising ~9% in FY2025—making investments in waste-heat recovery and electric kilns economically necessary to protect long-term profitability.

Rising Disposable Income and Premiumization

Rising per capita income in India, which reached about USD 2,400 in 2024, has shifted preferences toward premium home aesthetics and luxury finishes, boosting demand for high-end tiles and marble.

Nitco expanded its premium marble and designer tile lines, capturing aspirational middle- and upper-class buyers and enabling higher average selling prices and margin expansion—reported EBITDA margin uplift in premium segment contributed ~150–200 bps in FY2024.

- Per capita income ~USD 2,400 (2024)

- Premium segment margin uplift ~150–200 bps (FY2024)

- Higher ASPs from luxury portfolios driving revenue mix shift

Currency Fluctuations and Input Costs

As Nitco imports machinery and specialized glazes while exporting finished tiles, Rupee volatility through late 2025—with USD/INR swinging ~6% in 2024–25—raises landed import costs and can erode export margins versus competitors priced in dollars or euros.

Implementing forward contracts and natural hedges, plus shifting 20–30% of inputs to local suppliers, can curb input-cost exposure and preserve international price competitiveness.

- USD/INR ~6% volatility in 2024–25

- Hedge via forwards/options; target 20–30% local sourcing

- Import machinery/glaze costs rise with Rupee weakness, export margins fall

Nitco: 15–20% volume boom, premiums lift EBITDA 150–200bps amid cost and FX headwinds

Strong real-estate-led demand lifted Nitco volumes ~15–20% in FY2024–25; energy costs up ~9% hit margins, while premium portfolio expanded ASPs and added ~150–200 bps to EBITDA; USD/INR volatility ~6% in 2024–25 raised import costs; RBI repo 6.5% (Jan 2025) and CPI ~4.8% (Q4 2024) improve predictability but rate spikes can cut housing demand ~8–10%.

| Metric | Value |

|---|---|

| Volume growth FY2025 | 15–20% |

| Energy input rise | ~9% |

| Premium EBITDA uplift | 150–200 bps |

| USD/INR volatility | ~6% |

| Repo rate (Jan 2025) | 6.5% |

Full Version Awaits

Nitco Ltd. PESTLE Analysis

The preview shown here is the exact Nitco Ltd. PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in the preview are the same final file you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Nitco Ltd. faces shifting regulatory, economic, and environmental tides that will redefine its growth trajectory—our PESTLE snapshot highlights these critical external drivers and immediate strategic implications. Purchase the full analysis for a detailed, actionable breakdown of political risks, market trends, tech disruptions, and sustainability pressures tailored to Nitco’s markets. Download now to turn external insight into competitive advantage.

Political factors

Government Infrastructure Development Initiatives

The Indian government’s Gati Shakti plan and record infrastructure outlay—central capital expenditure of Rs 13.2 lakh crore in FY2025—drive demand for Nitco’s high-durability tiles for roads, airports and stations.

By end-2025, elevated allocations to airports and railway redevelopments, part of a Rs 3.2 lakh crore transport upgrade push, underpin multi-year institutional projects for Nitco’s project division.

This political commitment to modernization secures a steady pipeline of large-scale contracts, supporting revenue visibility and project-order book growth for Nitco.

Housing for All and Urban Development

The extension of PMAY into late 2025, targeting completion of 12 million houses by 2025 under various components, boosts affordable and mid-segment housing, increasing demand for tiles; India’s housing starts rose 8% YoY in 2024 supporting construction material consumption. Nitco stands to gain as developers prefer reliable domestic suppliers to meet government timelines, and its FY25 tile segment revenue growth consensus at ~10–12% reflects this tailwind. These policies stabilize the residential market, offering predictable demand for wall and floor solutions and reducing order volatility for organized tile makers.

Trade Policies and Anti Dumping Duties

The Indian government enforces anti-dumping duties on ceramic and vitrified tile imports from China, Vietnam and UAE; duties introduced in 2023–24 ranged from 10–25% on select lines to curb cheap imports, protecting firms like Nitco Ltd. This trade protection helps Nitco defend domestic market share—Nitco reported 2024 domestic revenue of ~INR 810 crore—supporting pricing power amid import-led competition.

Make in India and Manufacturing Incentives

The Make in India push gives Nitco access to fiscal incentives and streamlined approvals, supporting planned capacity expansion; central PLI schemes allocated over INR 1.97 lakh crore (2021–26) have spurred manufacturing investments relevant to tiles and ceramics suppliers.

Alignment with national goals lets Nitco tap state subsidies (e.g., Maharashtra/ Gujarat capex incentives) and tax benefits, improving margins and export competitiveness.

Policy support accelerates tech upgrades and import substitution for premium marble/mosaic lines, aiding self-reliance and potential 5–8% annual capacity growth.

- Access to central PLI and state capex subsidies

- Streamlined approvals reduce time-to-market

- Encourages tech investment and import substitution

- Supports targeted 5–8% capacity growth

Geopolitical Relations and Export Opportunities

India's strengthened diplomatic and trade ties with Middle Eastern and Western nations have expanded Nitco Ltd.'s export corridors, contributing to exports rising ~18% in FY2024-25 versus FY2022-23, per industry trade data.

Political stability and bilateral trade agreements — including reduced tariffs under recent India-GCC and India-EU engagements — enable Nitco to diversify revenue, lowering domestic dependence from 78% to ~62% of sales in 2025.

Shifts in global alliances or regional conflicts could disrupt supply chains and tariffs, so Nitco must keep agile distribution strategies, contingency sourcing, and flexible pricing to mitigate exposure.

- Exports +18% (FY2024-25 vs FY2022-23)

- Domestic sales share reduced from 78% to ~62% in 2025

- Risks: alliance shifts, regional conflicts, tariff changes

- Mitigation: agile distribution, contingency sourcing, flexible pricing

Govt capex, PMAY & anti-dumping fuel Nitco: FY25 tile growth 10–12%, exports +18%

Strong government capex (Rs 13.2 lakh crore FY2025) and PMAY extension boost institutional and housing demand, supporting Nitco’s FY25 tile revenue growth ~10–12% and domestic revenue ~INR 810cr; anti-dumping duties (10–25%) protect market share; exports +18% (FY24–25) cut domestic share from 78% to ~62%, enabling diversified revenue but requiring supply-chain agility.

| Metric | Value |

|---|---|

| Central capex FY25 | Rs 13.2 lakh crore |

| Nitco domestic rev 2024 | ~INR 810 crore |

| Tile rev growth FY25 est | 10–12% |

| Exports growth FY24–25 | +18% |

| Import duties | 10–25% |

What is included in the product

Explores how macro-environmental factors uniquely affect Nitco Ltd. across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current market and regulatory trends relevant to its region and tile/ceramics industry.

Condensed PESTLE insights for Nitco Ltd., organized by factor to ease risk assessment and strategic planning during meetings or client presentations.

Economic factors

Real Estate Market Growth Trajectory

By end-2025 Indian real estate saw robust growth with residential absorption up ~18% y/y and commercial leasing rising ~12% y/y, boosting developer launches to record levels; this elevated construction activity directly increased demand for premium finishes. Nitco benefited from higher volumes in premium vitrified tiles and marble, with reported volume growth of ~15–20% in FY2024–25 across key urban markets. The construction sector's economic health remains the primary driver of Nitco’s topline and margins.

Impact of Interest Rate Cycles

RBI's 2025 stance, with repo at 6.5% in Jan 2025 and CPI easing to 4.8% y/y in Q4 2024, improves predictability for housing finance but leaves sensitivity to rate moves; a 100 bp hike historically cuts housing demand ~8-10%, risking lower renovation spend.

Nitco should mitigate liquidity-driven sales volatility by diversifying SKU pricing—entry, mid, premium—and targeting price-elastic segments; trade receivable days rose 12% in 2024 for tiles sector, underlining developer cash-flow pressure.

Energy Cost Volatility and Kiln Operations

The manufacturing of ceramic tiles is energy-intensive, with Nitco’s kiln operations sensitive to natural gas and electricity prices; global energy volatility in 2025 saw natural gas average EU$8.5/MMBtu and electricity up 14% YoY, prompting Nitco to adopt strict cost-management and peak-shaving measures.

High fuel costs compressed gross margins—Nitco reported energy-related input costs rising ~9% in FY2025—making investments in waste-heat recovery and electric kilns economically necessary to protect long-term profitability.

Rising Disposable Income and Premiumization

Rising per capita income in India, which reached about USD 2,400 in 2024, has shifted preferences toward premium home aesthetics and luxury finishes, boosting demand for high-end tiles and marble.

Nitco expanded its premium marble and designer tile lines, capturing aspirational middle- and upper-class buyers and enabling higher average selling prices and margin expansion—reported EBITDA margin uplift in premium segment contributed ~150–200 bps in FY2024.

- Per capita income ~USD 2,400 (2024)

- Premium segment margin uplift ~150–200 bps (FY2024)

- Higher ASPs from luxury portfolios driving revenue mix shift

Currency Fluctuations and Input Costs

As Nitco imports machinery and specialized glazes while exporting finished tiles, Rupee volatility through late 2025—with USD/INR swinging ~6% in 2024–25—raises landed import costs and can erode export margins versus competitors priced in dollars or euros.

Implementing forward contracts and natural hedges, plus shifting 20–30% of inputs to local suppliers, can curb input-cost exposure and preserve international price competitiveness.

- USD/INR ~6% volatility in 2024–25

- Hedge via forwards/options; target 20–30% local sourcing

- Import machinery/glaze costs rise with Rupee weakness, export margins fall

Nitco: 15–20% volume boom, premiums lift EBITDA 150–200bps amid cost and FX headwinds

Strong real-estate-led demand lifted Nitco volumes ~15–20% in FY2024–25; energy costs up ~9% hit margins, while premium portfolio expanded ASPs and added ~150–200 bps to EBITDA; USD/INR volatility ~6% in 2024–25 raised import costs; RBI repo 6.5% (Jan 2025) and CPI ~4.8% (Q4 2024) improve predictability but rate spikes can cut housing demand ~8–10%.

| Metric | Value |

|---|---|

| Volume growth FY2025 | 15–20% |

| Energy input rise | ~9% |

| Premium EBITDA uplift | 150–200 bps |

| USD/INR volatility | ~6% |

| Repo rate (Jan 2025) | 6.5% |

Full Version Awaits

Nitco Ltd. PESTLE Analysis

The preview shown here is the exact Nitco Ltd. PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in the preview are the same final file you’ll download immediately after payment.