Bank of Nanjing Boston Consulting Group Matrix

Download Your Competitive Advantage

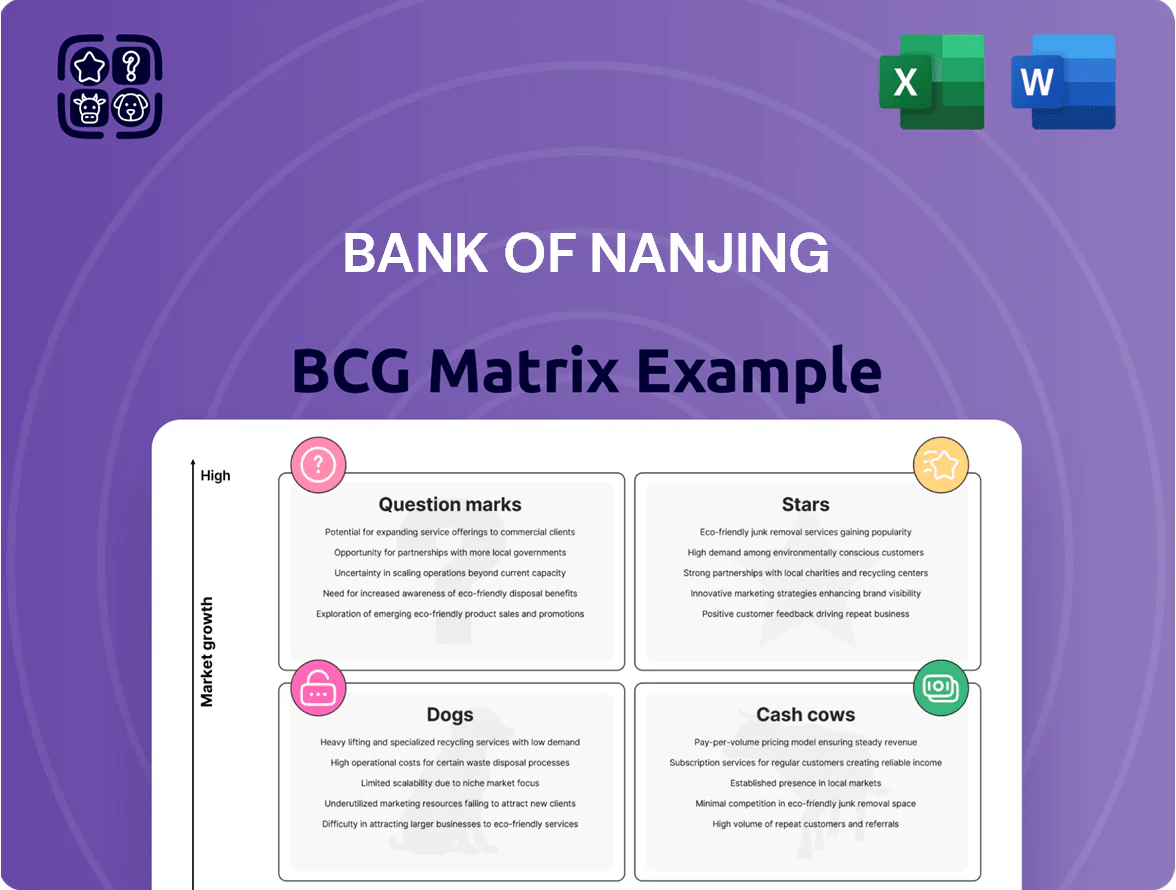

The Bank of Nanjing’s BCG Matrix preview highlights its core business lines against market growth and relative share, flagging potential Stars in retail banking and Cash Cows in corporate lending while noting areas that may require strategic pruning. This snapshot suggests where management can double down on growth, defend market positions, or reallocate capital for higher returns. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-use Word + Excel package to guide investment and strategic decisions.

Stars

Tech-Finance Integration

Bank of Nanjing held roughly 28% market share of lending to high-tech firms in Jiangsu’s innovation corridor by Q4 2025, driven by 36% year-on-year growth in tech-sector loan book to CNY 112 billion.

Provincial incentives—CNY 15 billion in credit guarantees and a 20% subsidized-rate program—lowered provisioning but raised concentration: semiconductors and biotech account for 62% of exposures.

Capital needs are high: risk-weighted assets for this segment rose 42% in 2025, yet projected NPV from fee income and equity stakes could add CNY 6–9 billion to bank valuation over five years.

Green Banking Solutions

Bank of Nanjing’s Green Banking Solutions leads East China with a ~22% share of regional green bond issuance and ¥48.7bn in sustainable loans at end-2025, reflecting a 38% CAGR since 2021.

With China’s 2025 decarbonization push, ESG-linked financing demand rose 45% YoY in 2024–25; the unit’s early-mover structuring capability keeps growth above 30% annually.

High-Net-Worth Wealth Management

Leveraging the Yangtze River Delta’s affluent base, Bank of Nanjing’s private banking saw AUM surge to about CNY 220 billion by end-2024, up ~28% year-on-year, classifying it as a Stars unit in the BCG matrix.

Personalized family office services and exclusive structured products drove a regional market share near 18% among high-net-worth clients in Jiangsu province as of 2024.

To fend off national rivals like ICBC Private and CCB Wealth, the bank must keep investing in senior relationship managers and its digital wealth platform—client onboarding times fell to 7 days in 2024, but scale gaps remain.

Digital Ecosystem Services

Bank of Nanjing’s proprietary digital platforms for supply-chain integration became a regional benchmark by Dec 31, 2025, supporting 4,200 corporate clients and processing CNY 128 billion in transaction volume, securing a high-growth, high-share Stars position in the BCG matrix.

Embedding finance into clients’ ERP systems raised fee income by 22% YoY in 2025 but required CNY 480 million R&D spend for continuous software iterations, which consume cash yet sustain the bank’s digital-first edge.

- 4,200 corporate clients

- CNY 128 billion annual transaction volume (2025)

- Fee income +22% YoY (2025)

- CNY 480 million R&D spend (2025)

Smart Supply Chain Finance

Smart Supply Chain Finance is a Star for Bank of Nanjing: by 2025 it holds ~28% market share in Jiangsu’s automated supply-chain credit, driven by financing to manufacturing clusters worth CNY 320 billion annually.

Growth is rapid as domestic trade digitization rises ~22% CAGR (2022–25); the bank’s heavy investments—CNY 1.1 billion in blockchain and IoT by 2024—keep it a primary liquidity provider.

- 28% market share in Jiangsu automated SCF

- CNY 320bn annual cluster financing

- 22% CAGR in digitized trade (2022–25)

- CNY 1.1bn invested in blockchain/IoT by 2024

Bank of Nanjing’s Stars: Tech, Green, PB & Smart SCF Fuel 2025 Growth Surge

Stars: High-growth, high-share units—Tech lending, Green Banking, Private Banking, Smart SCF—drive Bank of Nanjing’s regional leadership with key 2024–25 metrics: tech loans CNY112bn (36% YoY), green loans CNY48.7bn (38% CAGR since 2021), PB AUM CNY220bn (28% YoY), SCF volume CNY128bn (4,200 clients); combined RWA rise +42% (2025), R&D & infra spend ~CNY1.58bn.

| Unit | Key 2025 metric | Growth/notes |

|---|---|---|

| Tech lending | CNY112bn | +36% YoY; 28% market share |

| Green Banking | CNY48.7bn | 38% CAGR since 2021 |

| Private Banking | CNY220bn AUM | +28% YoY |

| Smart SCF | CNY128bn tx vol | 4,200 clients; 28% Jiangsu share |

What is included in the product

Comprehensive BCG Matrix analysis of Bank of Nanjing’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each Bank of Nanjing business unit in a quadrant for quick strategic decisions.

Cash Cows

Jiangsu Corporate Lending

Jiangsu Corporate Lending delivers a stable, dominant share in Jiangsu province, contributing roughly RMB 120–140 billion in outstanding loans (2025) and ~18–20% provincial market share, yielding predictable interest income.

Long-standing institutional relationships cut new marketing spend by an estimated 40% versus fintech channels, keeping cost-to-income for this portfolio near 35%.

High margins from these mature loans fund Bank of Nanjing’s push into digital banking and green loans, financing about RMB 8–12 billion of new initiatives in 2024–25.

Institutional Deposit Base

Bank of Nanjing holds a dominant institutional deposit base from local governments and public agencies, supplying low-cost stable funding; as of 2024 year-end these deposits funded roughly 38% of total liabilities (RMB 480bn of RMB 1.26tn), a classic cash cow in a mature market.

Local Government Infrastructure Financing

Bank of Nanjing holds roughly 38% of regional financing for mature local government infrastructure in Nanjing and nearby cities, backing projects with strong collateral and average LTV around 55%, which yields steady net interest margin near 2.4% in 2025.

These loans require minimal marketing and show low annual volume growth (~1–2%), so the segment consistently generates predictable cash flow and covers funding needs for higher-return question-mark ventures.

Interbank Market Operations

Bank of Nanjing’s treasury is a sophisticated interbank-market player, using RMB 280–320 billion average daily liquidity in 2025 to earn steady net interest and trading income of ~CNY 4.1 billion in FY2024, making it a reliable cash cow within a mature, tightly regulated domestic market.

The unit’s strong reputation and high-quality funding mix yield low-risk earnings—liquidity coverage ratios above 120% in 2024—supporting group capital needs and smoothing volatility for lending and investment operations.

- Average daily liquidity: RMB 280–320 billion (2025)

- FY2024 treasury income: ~CNY 4.1 billion

- Liquidity coverage ratio: >120% (2024)

- Role: steady, low-risk capital generator for group

Core Retail Mortgage Portfolio

Core Retail Mortgage Portfolio: despite 2025 market cooling, Bank of Nanjing’s outstanding retail mortgages in Tier 1–2 cities (~RMB 120 billion, ~28% of loans as of 2025Q1) remain high-quality and low-default (NPL ratio ~0.45%), delivering steady interest income with low upkeep.

As a mature product line, these long-term loans stabilize earnings—interest margin contribution ~35% of retail net interest income—and help absorb volatility from speculative segments.

- RMB 120bn outstanding; 28% of loan book (2025Q1)

Stable cash engine: RMB120–140bn corp loans, RMB120bn mortgages, LCR>120%

Jiangsu corporate lending, core retail mortgages, and treasury generate stable cash: ~RMB 120–140bn corporate loans (18–20% provincial share), RMB 120bn retail mortgages (28% of loans, NPL ~0.45%), treasury daily liquidity RMB 280–320bn, FY2024 treasury income ~CNY 4.1bn, LCR >120%, segment margins ~2.4% NIM and 35% retail margin.

| Metric | Value (2024–25) |

|---|---|

| Corporate loans | RMB 120–140bn |

| Provincial share | 18–20% |

| Retail mortgages | RMB 120bn (28%) NPL 0.45% |

| Treasury liquidity | RMB 280–320bn daily |

| FY2024 treasury income | CNY 4.1bn |

| Liquidity coverage ratio | >120% |

| Segment NIM / margin | 2.4% NIM; 35% retail margin |

Delivered as Shown

Bank of Nanjing BCG Matrix

The preview you’re viewing is the exact Bank of Nanjing BCG Matrix file you’ll receive after purchase — no watermarks, no placeholders, just the fully formatted, analysis-ready report crafted for strategic clarity and professional use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

The Bank of Nanjing’s BCG Matrix preview highlights its core business lines against market growth and relative share, flagging potential Stars in retail banking and Cash Cows in corporate lending while noting areas that may require strategic pruning. This snapshot suggests where management can double down on growth, defend market positions, or reallocate capital for higher returns. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-use Word + Excel package to guide investment and strategic decisions.

Stars

Tech-Finance Integration

Bank of Nanjing held roughly 28% market share of lending to high-tech firms in Jiangsu’s innovation corridor by Q4 2025, driven by 36% year-on-year growth in tech-sector loan book to CNY 112 billion.

Provincial incentives—CNY 15 billion in credit guarantees and a 20% subsidized-rate program—lowered provisioning but raised concentration: semiconductors and biotech account for 62% of exposures.

Capital needs are high: risk-weighted assets for this segment rose 42% in 2025, yet projected NPV from fee income and equity stakes could add CNY 6–9 billion to bank valuation over five years.

Green Banking Solutions

Bank of Nanjing’s Green Banking Solutions leads East China with a ~22% share of regional green bond issuance and ¥48.7bn in sustainable loans at end-2025, reflecting a 38% CAGR since 2021.

With China’s 2025 decarbonization push, ESG-linked financing demand rose 45% YoY in 2024–25; the unit’s early-mover structuring capability keeps growth above 30% annually.

High-Net-Worth Wealth Management

Leveraging the Yangtze River Delta’s affluent base, Bank of Nanjing’s private banking saw AUM surge to about CNY 220 billion by end-2024, up ~28% year-on-year, classifying it as a Stars unit in the BCG matrix.

Personalized family office services and exclusive structured products drove a regional market share near 18% among high-net-worth clients in Jiangsu province as of 2024.

To fend off national rivals like ICBC Private and CCB Wealth, the bank must keep investing in senior relationship managers and its digital wealth platform—client onboarding times fell to 7 days in 2024, but scale gaps remain.

Digital Ecosystem Services

Bank of Nanjing’s proprietary digital platforms for supply-chain integration became a regional benchmark by Dec 31, 2025, supporting 4,200 corporate clients and processing CNY 128 billion in transaction volume, securing a high-growth, high-share Stars position in the BCG matrix.

Embedding finance into clients’ ERP systems raised fee income by 22% YoY in 2025 but required CNY 480 million R&D spend for continuous software iterations, which consume cash yet sustain the bank’s digital-first edge.

- 4,200 corporate clients

- CNY 128 billion annual transaction volume (2025)

- Fee income +22% YoY (2025)

- CNY 480 million R&D spend (2025)

Smart Supply Chain Finance

Smart Supply Chain Finance is a Star for Bank of Nanjing: by 2025 it holds ~28% market share in Jiangsu’s automated supply-chain credit, driven by financing to manufacturing clusters worth CNY 320 billion annually.

Growth is rapid as domestic trade digitization rises ~22% CAGR (2022–25); the bank’s heavy investments—CNY 1.1 billion in blockchain and IoT by 2024—keep it a primary liquidity provider.

- 28% market share in Jiangsu automated SCF

- CNY 320bn annual cluster financing

- 22% CAGR in digitized trade (2022–25)

- CNY 1.1bn invested in blockchain/IoT by 2024

Bank of Nanjing’s Stars: Tech, Green, PB & Smart SCF Fuel 2025 Growth Surge

Stars: High-growth, high-share units—Tech lending, Green Banking, Private Banking, Smart SCF—drive Bank of Nanjing’s regional leadership with key 2024–25 metrics: tech loans CNY112bn (36% YoY), green loans CNY48.7bn (38% CAGR since 2021), PB AUM CNY220bn (28% YoY), SCF volume CNY128bn (4,200 clients); combined RWA rise +42% (2025), R&D & infra spend ~CNY1.58bn.

| Unit | Key 2025 metric | Growth/notes |

|---|---|---|

| Tech lending | CNY112bn | +36% YoY; 28% market share |

| Green Banking | CNY48.7bn | 38% CAGR since 2021 |

| Private Banking | CNY220bn AUM | +28% YoY |

| Smart SCF | CNY128bn tx vol | 4,200 clients; 28% Jiangsu share |

What is included in the product

Comprehensive BCG Matrix analysis of Bank of Nanjing’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each Bank of Nanjing business unit in a quadrant for quick strategic decisions.

Cash Cows

Jiangsu Corporate Lending

Jiangsu Corporate Lending delivers a stable, dominant share in Jiangsu province, contributing roughly RMB 120–140 billion in outstanding loans (2025) and ~18–20% provincial market share, yielding predictable interest income.

Long-standing institutional relationships cut new marketing spend by an estimated 40% versus fintech channels, keeping cost-to-income for this portfolio near 35%.

High margins from these mature loans fund Bank of Nanjing’s push into digital banking and green loans, financing about RMB 8–12 billion of new initiatives in 2024–25.

Institutional Deposit Base

Bank of Nanjing holds a dominant institutional deposit base from local governments and public agencies, supplying low-cost stable funding; as of 2024 year-end these deposits funded roughly 38% of total liabilities (RMB 480bn of RMB 1.26tn), a classic cash cow in a mature market.

Local Government Infrastructure Financing

Bank of Nanjing holds roughly 38% of regional financing for mature local government infrastructure in Nanjing and nearby cities, backing projects with strong collateral and average LTV around 55%, which yields steady net interest margin near 2.4% in 2025.

These loans require minimal marketing and show low annual volume growth (~1–2%), so the segment consistently generates predictable cash flow and covers funding needs for higher-return question-mark ventures.

Interbank Market Operations

Bank of Nanjing’s treasury is a sophisticated interbank-market player, using RMB 280–320 billion average daily liquidity in 2025 to earn steady net interest and trading income of ~CNY 4.1 billion in FY2024, making it a reliable cash cow within a mature, tightly regulated domestic market.

The unit’s strong reputation and high-quality funding mix yield low-risk earnings—liquidity coverage ratios above 120% in 2024—supporting group capital needs and smoothing volatility for lending and investment operations.

- Average daily liquidity: RMB 280–320 billion (2025)

- FY2024 treasury income: ~CNY 4.1 billion

- Liquidity coverage ratio: >120% (2024)

- Role: steady, low-risk capital generator for group

Core Retail Mortgage Portfolio

Core Retail Mortgage Portfolio: despite 2025 market cooling, Bank of Nanjing’s outstanding retail mortgages in Tier 1–2 cities (~RMB 120 billion, ~28% of loans as of 2025Q1) remain high-quality and low-default (NPL ratio ~0.45%), delivering steady interest income with low upkeep.

As a mature product line, these long-term loans stabilize earnings—interest margin contribution ~35% of retail net interest income—and help absorb volatility from speculative segments.

- RMB 120bn outstanding; 28% of loan book (2025Q1)

Stable cash engine: RMB120–140bn corp loans, RMB120bn mortgages, LCR>120%

Jiangsu corporate lending, core retail mortgages, and treasury generate stable cash: ~RMB 120–140bn corporate loans (18–20% provincial share), RMB 120bn retail mortgages (28% of loans, NPL ~0.45%), treasury daily liquidity RMB 280–320bn, FY2024 treasury income ~CNY 4.1bn, LCR >120%, segment margins ~2.4% NIM and 35% retail margin.

| Metric | Value (2024–25) |

|---|---|

| Corporate loans | RMB 120–140bn |

| Provincial share | 18–20% |

| Retail mortgages | RMB 120bn (28%) NPL 0.45% |

| Treasury liquidity | RMB 280–320bn daily |

| FY2024 treasury income | CNY 4.1bn |

| Liquidity coverage ratio | >120% |

| Segment NIM / margin | 2.4% NIM; 35% retail margin |

Delivered as Shown

Bank of Nanjing BCG Matrix

The preview you’re viewing is the exact Bank of Nanjing BCG Matrix file you’ll receive after purchase — no watermarks, no placeholders, just the fully formatted, analysis-ready report crafted for strategic clarity and professional use.