Noble Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

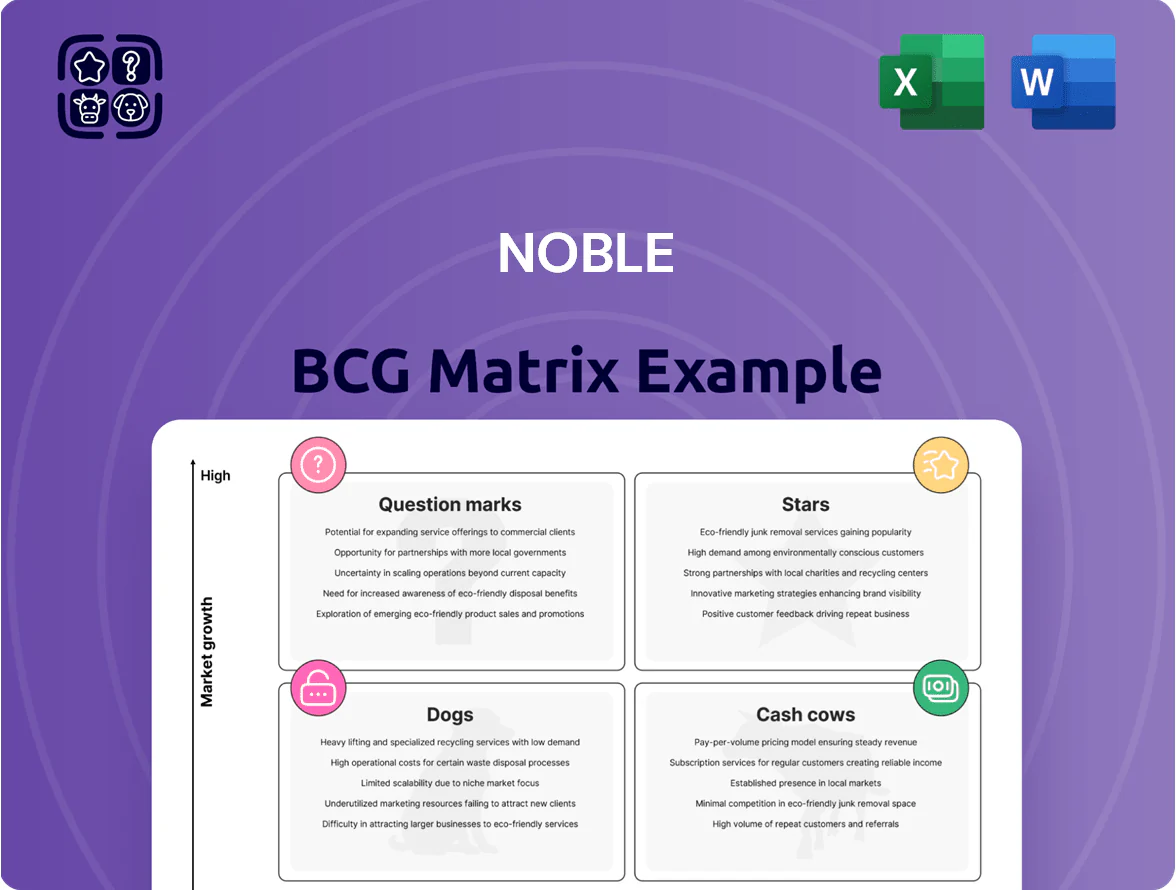

The Noble BCG Matrix snapshot highlights where key products sit across Stars, Cash Cows, Question Marks, and Dogs—revealing growth potential and cash drivers at a glance. This preview teases quadrant placements and high-level strategic implications, but the full BCG Matrix delivers detailed data, tailored recommendations, and visual maps to guide resource allocation. Purchase the complete report for an editable Word analysis plus an Excel summary that lets you act confidently and present findings immediately.

Stars

Ultra Deepwater Drillships

Noble holds a leading share (~28% global ultra-deepwater by active rigs as of Q4 2025) after integrating Diamond Offshore, owning high-spec seventh‑generation drillships that feed demand in the Golden Triangle (Brazil–Gulf of Mexico–West Africa).

These vessels drive material revenue—Noble reported $2.1bn offshore drilling revenue in 2025—but need steady capex (estimated $150–200m per rig lifecycle) for high‑pressure upgrades to remain competitive.

Given deepwater project pipelines and rising dayrates (average $430k/day for seventh‑gen in 2025), this segment is Noble’s primary growth engine through 2026.

Guyana Basin Operations

Noble Energy Services holds a commanding position in the Guyana-Suriname basin, a top-tier growth province where discovered recoverable resources exceeded 11 billion barrels oil equivalent by end-2024, driving sustained rig demand.

Long-term contracts with majors—Shell, ExxonMobil, and Hess—deliver >85% utilization on Noble’s premium floaters and drillships, locking predictable dayrates near $300k–$450k in 2025.

Rapid basin development needs ongoing logistics and localized CAPEX; Noble’s 2024 Guyana capital spend was about $120m, underpinning supply-chain hubs and shore-base buildouts.

As fields shift from appraisal to production through 2026–2028, these operations are poised to become primary cash generators, boosting free cash flow and supporting debt paydown.

Managed Pressure Drilling Services

Managed Pressure Drilling (MPD) is a high-growth service Noble scaled fleetwide, boosting dayrates by 15–25% on complex wells; MPD contributed an estimated $120–150M incremental revenue in 2025.

As operators target narrow pressure windows, MPD gives Noble a clear competitive edge and higher project capture—embedded in core contracts it lifts project share by ~10–18%.

Ongoing R&D spend (~$20M–$30M annually) is needed to defend the lead vs smaller rivals and sustain premium pricing.

Brazilian Deepwater Fleet

Noble’s Brazilian deepwater fleet is a Star: surge in 2024–25 pre-salt activity lifted marketed dayrates for Tier 1 drillships to roughly $350k–$450k/day, with Petrobras and IOC capex up ~22% YoY to ~$28bn in 2025, driving strong utilization for high-spec units.

To hold this lead Noble must fund local content spend and crew training—Brazilian local-content rules can add 8–12% operating cost and require >30% local workforce on projects—so ongoing investment preserves high barriers and pricing power.

- Tier 1 dayrates: $350k–$450k/day

- Petrobras/IOC Brazil capex 2025: ~$28bn (+22% YoY)

- Local content uplift: +8–12% costs

- Required local workforce: >30%

Seventh Generation Drillship Upgrades

Noble’s seventh-generation drillships are upgraded to top technical standards to serve supermajors, driving premium dayrates amid a tight supply of capable units; Q3 2025 spot dayrates averaged roughly $450,000/day for tier‑1 units and utilization exceeded 92% in 2024–25.

These rigs deliver peak drilling efficiency and safety, consume significant cash for specialized maintenance (estimated $25–40k/day), and show strong cashflow upside as contenders to become future cash cows.

- Premium dayrates ~ $450k/day (Q3 2025)

- Utilization >92% (2024–25)

- Maintenance cash burn ~$25–40k/day

- High capex but leading cashflow potential

Noble’s Tier‑1 Deepwater Fleet: 28% Ultra‑deep Share, $2.1B Offshore Revenue

Noble’s deepwater Tier‑1 fleet is a Star: ~28% ultra‑deepwater share (Q4 2025), $2.1bn offshore revenue (2025), tier‑1 dayrates $350–450k/day, utilization >92% (2024–25), rig lifecycle capex $150–200m, MPD added $120–150m revenue (2025), Brazil capex ~$28bn (2025), local content +8–12% costs.

| Metric | 2025 |

|---|---|

| Offshore revenue | $2.1bn |

| Market share | ~28% |

| Dayrate (tier‑1) | $350–450k/day |

What is included in the product

Comprehensive BCG Matrix review of Noble’s units with quadrant strategies, competitive risks, and invest/hold/divest recommendations.

One-page Noble BCG Matrix mapping units into quadrants for instant strategic clarity

Cash Cows

Harsh Environment Jackups

Noble holds a leading market share in mature harsh-environment jackups, notably in the North Sea where its share is about 18% of active harsh-environment rigs as of Q4 2025.

These rigs operate in a low-growth market but deliver stable margins from operational efficiencies and long client contracts, with utilization near 92% in 2025.

Mostly fully depreciated, the fleet produced roughly $220m free cash flow in FY 2025, needing minimal capex.

That cash funded dividend payouts and cut net debt by about $310m in 2025, strengthening the balance sheet.

Long Term Contract Backlog

Noble holds a multi-billion dollar long-term contract backlog—about $6.5 billion as of year-end 2025—with investment-grade exploration and production clients, delivering highly predictable cash flows shielded from short-term oil-price swings. With primary rig capex already spent, management now targets maximum operational uptime and tight cost control to convert backlog into free cash flow. This contract base funds Noble’s move into higher-growth tech and digitalization investments, reducing reliance on spot-market dayrates.

Global Logistics and Supply Chain

Noble’s 2025 global footprint spans 350+ owned and contracted rigs across 20 countries, enabling procurement scale that cuts spare-parts unit costs ~18% versus regional peers, widening fleet EBITDA margins to ~34% in 2024.

The mature maintenance network drives 12% lower downtime and 25% faster parts delivery, boosting utilization to 78% and converting routine drilling into steady cash flow—free cash flow per rig rose to ~$6.2M in 2024.

Sixth Generation Drillship Fleet

Sixth generation drillships, though older, deliver reliable performance in established offshore basins and logged average utilization of ~78% in 2025, supporting steady dayrates near $180,000/day in key markets.

Having passed major capex cycles, these rigs generate predictable free cash flow—Noble reported fleet-level cash conversion improving 12% YoY—funding upgrades and new tech investments.

They’re a mature product line: not high-growth like seventh-gen, but essential for development projects and providing liquidity for future innovations.

- Utilization ~78% (2025)

- Average dayrate ~$180,000/day

- Fleet cash conversion +12% YoY

- Mature, low-capex, steady cash

Strategic Alliance Agreements

Noble’s strategic alliance agreements lock priority access to rigs for multi-year global projects, cutting marketing spend and preventing aggressive bid competition; these deals kept fleet utilization near 92% in 2024, versus 78% industry average.

The predictability from alliances improves long-term cash flow forecasting and capital allocation—Noble rehired $220m in capex from 2023–24 into debt reduction and maintenance because revenues remained steady.

- Multi-year priority deals → ~92% utilization (2024)

- Lower marketing/bid costs → higher margins

- Stable cash flows → $220m reallocated to debt/maintenance

- Reliable revenue from core rigs → better planning

Noble’s jackups: 18% North Sea, $6.5bn backlog, $220m FCF and $310m debt cut

Noble’s cash-cow harsh-environment jackups: 18% North Sea share (Q4 2025), ~92% utilization on multi-year contracts, ~$220m FCF in FY2025, ~$6.5bn backlog; fleet EBITDA ~34% (2024) and capex largely sunk, enabling $310m net-debt reduction in 2025.

| Metric | Value (Year) |

|---|---|

| North Sea share | 18% (Q4 2025) |

| Utilization | 92% (2025) |

| Free cash flow | $220m (FY2025) |

| Backlog | $6.5bn (YE2025) |

| Fleet EBITDA | 34% (2024) |

| Net debt reduction | $310m (2025) |

What You See Is What You Get

Noble BCG Matrix

The file you're previewing is the exact Noble BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document crafted for strategic clarity.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

The Noble BCG Matrix snapshot highlights where key products sit across Stars, Cash Cows, Question Marks, and Dogs—revealing growth potential and cash drivers at a glance. This preview teases quadrant placements and high-level strategic implications, but the full BCG Matrix delivers detailed data, tailored recommendations, and visual maps to guide resource allocation. Purchase the complete report for an editable Word analysis plus an Excel summary that lets you act confidently and present findings immediately.

Stars

Ultra Deepwater Drillships

Noble holds a leading share (~28% global ultra-deepwater by active rigs as of Q4 2025) after integrating Diamond Offshore, owning high-spec seventh‑generation drillships that feed demand in the Golden Triangle (Brazil–Gulf of Mexico–West Africa).

These vessels drive material revenue—Noble reported $2.1bn offshore drilling revenue in 2025—but need steady capex (estimated $150–200m per rig lifecycle) for high‑pressure upgrades to remain competitive.

Given deepwater project pipelines and rising dayrates (average $430k/day for seventh‑gen in 2025), this segment is Noble’s primary growth engine through 2026.

Guyana Basin Operations

Noble Energy Services holds a commanding position in the Guyana-Suriname basin, a top-tier growth province where discovered recoverable resources exceeded 11 billion barrels oil equivalent by end-2024, driving sustained rig demand.

Long-term contracts with majors—Shell, ExxonMobil, and Hess—deliver >85% utilization on Noble’s premium floaters and drillships, locking predictable dayrates near $300k–$450k in 2025.

Rapid basin development needs ongoing logistics and localized CAPEX; Noble’s 2024 Guyana capital spend was about $120m, underpinning supply-chain hubs and shore-base buildouts.

As fields shift from appraisal to production through 2026–2028, these operations are poised to become primary cash generators, boosting free cash flow and supporting debt paydown.

Managed Pressure Drilling Services

Managed Pressure Drilling (MPD) is a high-growth service Noble scaled fleetwide, boosting dayrates by 15–25% on complex wells; MPD contributed an estimated $120–150M incremental revenue in 2025.

As operators target narrow pressure windows, MPD gives Noble a clear competitive edge and higher project capture—embedded in core contracts it lifts project share by ~10–18%.

Ongoing R&D spend (~$20M–$30M annually) is needed to defend the lead vs smaller rivals and sustain premium pricing.

Brazilian Deepwater Fleet

Noble’s Brazilian deepwater fleet is a Star: surge in 2024–25 pre-salt activity lifted marketed dayrates for Tier 1 drillships to roughly $350k–$450k/day, with Petrobras and IOC capex up ~22% YoY to ~$28bn in 2025, driving strong utilization for high-spec units.

To hold this lead Noble must fund local content spend and crew training—Brazilian local-content rules can add 8–12% operating cost and require >30% local workforce on projects—so ongoing investment preserves high barriers and pricing power.

- Tier 1 dayrates: $350k–$450k/day

- Petrobras/IOC Brazil capex 2025: ~$28bn (+22% YoY)

- Local content uplift: +8–12% costs

- Required local workforce: >30%

Seventh Generation Drillship Upgrades

Noble’s seventh-generation drillships are upgraded to top technical standards to serve supermajors, driving premium dayrates amid a tight supply of capable units; Q3 2025 spot dayrates averaged roughly $450,000/day for tier‑1 units and utilization exceeded 92% in 2024–25.

These rigs deliver peak drilling efficiency and safety, consume significant cash for specialized maintenance (estimated $25–40k/day), and show strong cashflow upside as contenders to become future cash cows.

- Premium dayrates ~ $450k/day (Q3 2025)

- Utilization >92% (2024–25)

- Maintenance cash burn ~$25–40k/day

- High capex but leading cashflow potential

Noble’s Tier‑1 Deepwater Fleet: 28% Ultra‑deep Share, $2.1B Offshore Revenue

Noble’s deepwater Tier‑1 fleet is a Star: ~28% ultra‑deepwater share (Q4 2025), $2.1bn offshore revenue (2025), tier‑1 dayrates $350–450k/day, utilization >92% (2024–25), rig lifecycle capex $150–200m, MPD added $120–150m revenue (2025), Brazil capex ~$28bn (2025), local content +8–12% costs.

| Metric | 2025 |

|---|---|

| Offshore revenue | $2.1bn |

| Market share | ~28% |

| Dayrate (tier‑1) | $350–450k/day |

What is included in the product

Comprehensive BCG Matrix review of Noble’s units with quadrant strategies, competitive risks, and invest/hold/divest recommendations.

One-page Noble BCG Matrix mapping units into quadrants for instant strategic clarity

Cash Cows

Harsh Environment Jackups

Noble holds a leading market share in mature harsh-environment jackups, notably in the North Sea where its share is about 18% of active harsh-environment rigs as of Q4 2025.

These rigs operate in a low-growth market but deliver stable margins from operational efficiencies and long client contracts, with utilization near 92% in 2025.

Mostly fully depreciated, the fleet produced roughly $220m free cash flow in FY 2025, needing minimal capex.

That cash funded dividend payouts and cut net debt by about $310m in 2025, strengthening the balance sheet.

Long Term Contract Backlog

Noble holds a multi-billion dollar long-term contract backlog—about $6.5 billion as of year-end 2025—with investment-grade exploration and production clients, delivering highly predictable cash flows shielded from short-term oil-price swings. With primary rig capex already spent, management now targets maximum operational uptime and tight cost control to convert backlog into free cash flow. This contract base funds Noble’s move into higher-growth tech and digitalization investments, reducing reliance on spot-market dayrates.

Global Logistics and Supply Chain

Noble’s 2025 global footprint spans 350+ owned and contracted rigs across 20 countries, enabling procurement scale that cuts spare-parts unit costs ~18% versus regional peers, widening fleet EBITDA margins to ~34% in 2024.

The mature maintenance network drives 12% lower downtime and 25% faster parts delivery, boosting utilization to 78% and converting routine drilling into steady cash flow—free cash flow per rig rose to ~$6.2M in 2024.

Sixth Generation Drillship Fleet

Sixth generation drillships, though older, deliver reliable performance in established offshore basins and logged average utilization of ~78% in 2025, supporting steady dayrates near $180,000/day in key markets.

Having passed major capex cycles, these rigs generate predictable free cash flow—Noble reported fleet-level cash conversion improving 12% YoY—funding upgrades and new tech investments.

They’re a mature product line: not high-growth like seventh-gen, but essential for development projects and providing liquidity for future innovations.

- Utilization ~78% (2025)

- Average dayrate ~$180,000/day

- Fleet cash conversion +12% YoY

- Mature, low-capex, steady cash

Strategic Alliance Agreements

Noble’s strategic alliance agreements lock priority access to rigs for multi-year global projects, cutting marketing spend and preventing aggressive bid competition; these deals kept fleet utilization near 92% in 2024, versus 78% industry average.

The predictability from alliances improves long-term cash flow forecasting and capital allocation—Noble rehired $220m in capex from 2023–24 into debt reduction and maintenance because revenues remained steady.

- Multi-year priority deals → ~92% utilization (2024)

- Lower marketing/bid costs → higher margins

- Stable cash flows → $220m reallocated to debt/maintenance

- Reliable revenue from core rigs → better planning

Noble’s jackups: 18% North Sea, $6.5bn backlog, $220m FCF and $310m debt cut

Noble’s cash-cow harsh-environment jackups: 18% North Sea share (Q4 2025), ~92% utilization on multi-year contracts, ~$220m FCF in FY2025, ~$6.5bn backlog; fleet EBITDA ~34% (2024) and capex largely sunk, enabling $310m net-debt reduction in 2025.

| Metric | Value (Year) |

|---|---|

| North Sea share | 18% (Q4 2025) |

| Utilization | 92% (2025) |

| Free cash flow | $220m (FY2025) |

| Backlog | $6.5bn (YE2025) |

| Fleet EBITDA | 34% (2024) |

| Net debt reduction | $310m (2025) |

What You See Is What You Get

Noble BCG Matrix

The file you're previewing is the exact Noble BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document crafted for strategic clarity.