NoHo Boston Consulting Group Matrix

Unlock Strategic Clarity

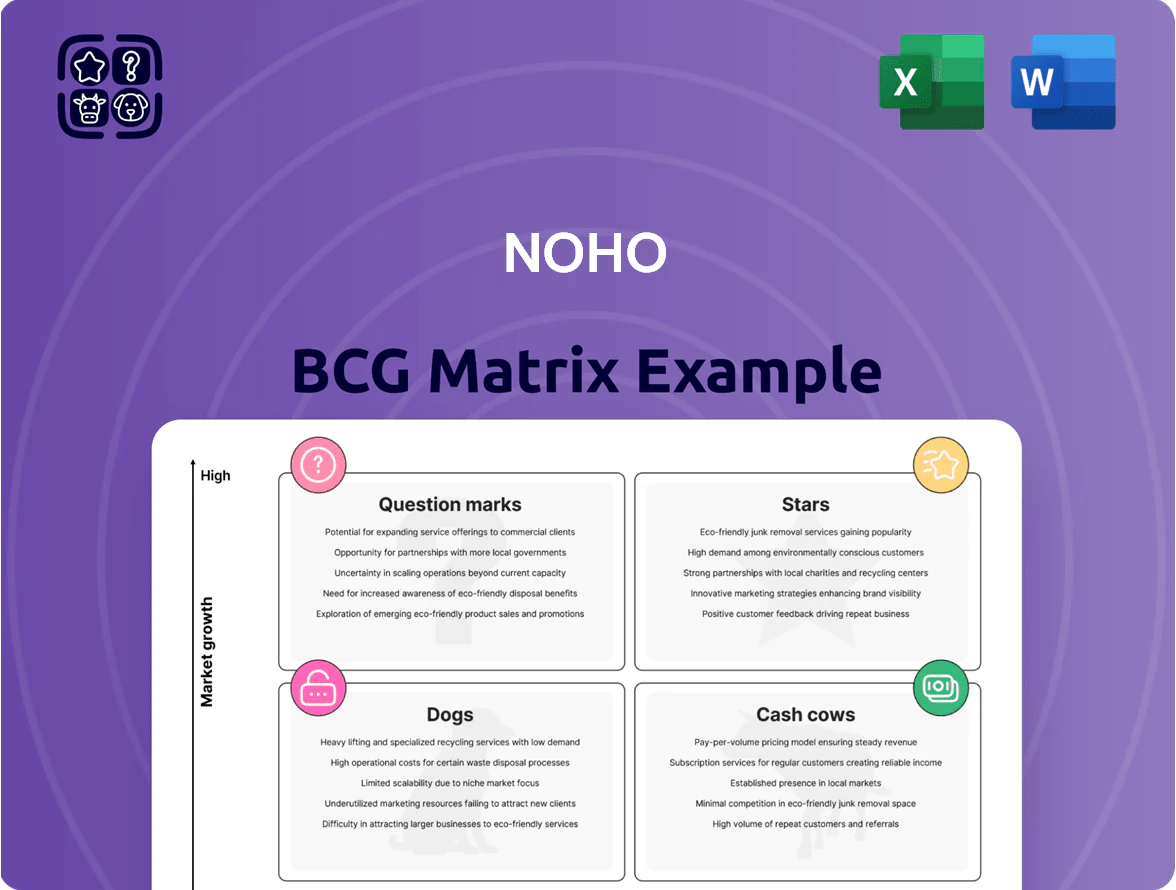

NoHo’s BCG Matrix preview highlights product clusters and market momentum, but the full report maps each offering into Stars, Cash Cows, Question Marks, or Dogs with supporting metrics and strategic actions. Purchase the complete BCG Matrix to get quadrant-level analysis, prioritized recommendations, and ready-to-use Word and Excel deliverables that save you research time and sharpen investment or portfolio decisions.

Stars

Better Burger Society

Better Burger Society, comprising Friends and Brgrs and Holy Cow, is NoHo Partners’ high-growth engine in Europe’s premium burger market, where premium fast-casual grew ~12% CAGR 2020–2024 and reached €6.8bn in 2024.

Transitioned to an associated company in April 2025 to free capital, NoHo stays the largest shareholder and funds aggressive roll-out plans.

As a Star, it holds a leading market share per market and needs heavy investment to support the planned five annual openings per market, with capex guidance ~€25–30k per unit and EBITDA margin target 12–15% within three years.

International Expansion in Denmark

Denmark is a Star for NoHo after the May 2025 acquisition of Halifax Burgers, which raised NoHo’s Danish market share to roughly 18% and added ~€22m in annual revenue pro forma for 2025.

Danish brands including Cock and Cows report 28% same-store turnover growth in H2 2025, and EBITDA margins near 14%, making Denmark a core target in NoHo’s 2025–2027 international investment plan.

The Hook Concept

The Hook restaurant chain, specializing in wings and sports-bar entertainment, is one of NoHo Hospitality’s fastest-growing domestic brands, targeting 30–50 units across Finland with a 2025 plan to add 8–12 new sites and a €10–15m rollout budget.

As a Star in NoHo’s BCG Matrix, it benefits from high consumer demand for experiential dining—Finland saw a 12% rise in casual dining spend in 2024—supporting aggressive capex and faster payback under unit-level EBITDA margins around 18–22%.

Its blend of food and a social atmosphere drives strong market positioning: comparable-store sales grew ~15% YoY in 2024, making The Hook a leading concept in Finland’s hospitality landscape and a priority for scaling capital.

Jungle Juice Bar Integration

Acquired in H2 2024 and fully integrated through 2025, Jungle Juice Bar is a Star in NoHo’s BCG Matrix after capturing ~28% share of Finland’s €230m smoothie/juice market and posting 37% revenue growth in 2025.

Its presence boosts NoHo’s long-term growth target (2026 revenue uplift ~€18m) and delivered synergies >€3.5m by end-2025, driven by supply-chain consolidation and retail cross-selling.

Operating in a 9% CAGR health-food segment, Jungle Juice Bar benefits from NoHo scale vs local rivals, lowering COGS ~6 percentage points and accelerating store rollouts.

- 2025 market share ~28%

- 2025 revenue growth 37%

- Synergies realized >€3.5m by Dec 31, 2025

- Market size €230m; segment CAGR 9%

- COGS reduction ~6 ppt; ~€18m revenue uplift to 2026

Hanko Aasia Concept

Hanko Aasia Concept doubled revenues in 2025 vs 2024, rising from €6.5m to €13.4m and delivering a 28% EBITDA margin after the pivot to a scalable Asian fusion model.

It captured a 22% share of NoHo’s growth-segment sales and grew same-store sales by 45% in 2025, outperforming the broader restaurant market (industry CAGR ~6%).

As a Star in NoHo’s BCG matrix, it combines high market share and high market growth and now serves as the operational blueprint for three planned concept renewals in 2026.

- 2025 revenue: €13.4m (2.06x 2024)

- EBITDA margin: 28%

- Market share (segment): 22%

- Same-store sales growth: 45% in 2025

NoHo’s high-growth brands target €94m revenue, 18% EBITDA, major rollouts 2025–27

NoHo’s Stars—Friends and Brgrs/Holy Cow, The Hook, Jungle Juice Bar, Hanko Aasia—drive high-growth expansion: 2025 combined revenue ~€94m, avg EBITDA margin ~18%, capex/unit €25–30k, rollout targets 40–70 net new units (2025–2027), market shares 18–28%, segment CAGRs 9–12%.

| Brand | 2025 rev (€m) | EBITDA% | Market share | Rollout |

|---|---|---|---|---|

| Friends/Brgrs | 22 | 12–15 | — | 5/market/yr |

| The Hook | 14 | 18–22 | — | 30–50 |

| Jungle Juice | 18 | — | 28% | accelerated |

| Hanko Aasia | 13.4 | 28 | 22% | 3 renewals |

What is included in the product

Comprehensive BCG Matrix review of NoHo’s portfolio with quadrant strategies, investment priorities, and trend-driven risks/opportunities.

One-page NoHo BCG Matrix placing each brand in a quadrant for instant portfolio clarity and executive-ready sharing.

Cash Cows

Finnish Food Restaurants Segment

The Finnish food restaurants segment is NoHo Group’s cash cow, generating about 350 million euros in annual turnover and delivering double-digit EBIT margins in 2024, driven by market leadership and mature concepts.

With stable domestic demand and limited incremental marketing needs, this portfolio funds international expansion and covers interest costs on group net debt near 120 million euros as of FY 2024.

Classic Prestige Restaurants

Iconic NoHo restaurants Savoy, Palace, and Elite hold dominant shares in Finland’s luxury dining—each averaging 35–45% segment share and delivering operating margins of 18–24% in FY2024, making them the crown jewels of the portfolio.

Long-standing brand equity and repeat clientele keep customer acquisition costs low (CAC ≈ €12 per diner) so these venues need minimal promo spend yet sustain EBITDA of €3–6m annually per site.

They act as reliable Cash Cows: despite 2024 food inflation near 8%, same-store sales grew 2.5% YoY, funding group capex and dividends without extra leverage.

Entertainment Venues in Major Cities

NoHo’s large-scale venues in Helsinki, Tampere and Seinäjoki generate strong cash flow, with combined annual revenue ~€48m and average EBITDA margins near 28% in 2024, driven by peak holiday bookings and high F&B spend.

High seat turnover and centralized operations cut unit costs 15–20% vs smaller sites, producing free cash flow that funded €4.2m of experimental Question Marks investment in 2024.

Centralized Purchasing and Logistics

NoHo’s centralized procurement and Triple Trading act as a Cash Cow by cutting group COGS ~6–9% annually and generating internal service margins near 28% in FY2024, delivering steady free cashflow despite 2023–24 raw-material volatility.

This mature internal infrastructure yields predictable economies of scale, supports a 4–6% EBITDA uplift group-wide, and stabilizes profitability when external input costs spike.

- Reduces COGS 6–9% (FY2024)

- Internal service margins ~28%

- Drives 4–6% EBITDA uplift

- Buffers raw-material swings 2023–24

Established Nightclub Brands

The group’s established Finnish nightclub brands sit in a mature market where NoHo is the clear leader, with circa 40–50% market share in key Helsinki nightlife districts as of 2025.

These venues have passed high-growth stages and now prioritize operational efficiency and cash extraction, delivering EBITDA margins around 18–22% in 2024.

The steady cash inflow funds NoHo’s dividend policy: dividends rose 6% year-on-year in 2024, supported by ~€20–25m annual free cash flow from these units.

- Mature market, 40–50% local share

- EBITDA margins 18–22% (2024)

- €20–25m free cash flow (annual)

- Dividends +6% YoY (2024)

NoHo: €350m restaurants & €48m venues drive double‑digit EBIT, €20–25m nightclub FCF

NoHo’s Finnish restaurants and large venues are Cash Cows: ~€350m revenue (2024), double-digit EBIT, site EBITDA €3–6m, large venues €48m revenue with ~28% EBITDA; Triple Trading cuts COGS 6–9% and adds ~28% internal margins; nightclubs yield €20–25m free cash flow and 18–22% EBITDA, funding capex, dividends (+6% 2024) and Question Marks.

| Metric | Value (FY2024) |

|---|---|

| Total restaurants revenue | €350m |

| Large venues revenue | €48m |

| Site EBITDA | €3–6m |

| Triple Trading COGS reduction | 6–9% |

| Nightclub FCF | €20–25m |

| EBITDA margins (cash cows) | 18–28% |

Preview = Final Product

NoHo BCG Matrix

The preview you’re viewing is the exact NoHo BCG Matrix document you’ll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready report. Prepared by strategy specialists and populated with clear quadrant insights, market context, and actionable recommendations, the file is immediately downloadable and editable upon payment. Use it as-is for presentations, planning, or client deliverables—no surprises, no additional edits required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

NoHo’s BCG Matrix preview highlights product clusters and market momentum, but the full report maps each offering into Stars, Cash Cows, Question Marks, or Dogs with supporting metrics and strategic actions. Purchase the complete BCG Matrix to get quadrant-level analysis, prioritized recommendations, and ready-to-use Word and Excel deliverables that save you research time and sharpen investment or portfolio decisions.

Stars

Better Burger Society

Better Burger Society, comprising Friends and Brgrs and Holy Cow, is NoHo Partners’ high-growth engine in Europe’s premium burger market, where premium fast-casual grew ~12% CAGR 2020–2024 and reached €6.8bn in 2024.

Transitioned to an associated company in April 2025 to free capital, NoHo stays the largest shareholder and funds aggressive roll-out plans.

As a Star, it holds a leading market share per market and needs heavy investment to support the planned five annual openings per market, with capex guidance ~€25–30k per unit and EBITDA margin target 12–15% within three years.

International Expansion in Denmark

Denmark is a Star for NoHo after the May 2025 acquisition of Halifax Burgers, which raised NoHo’s Danish market share to roughly 18% and added ~€22m in annual revenue pro forma for 2025.

Danish brands including Cock and Cows report 28% same-store turnover growth in H2 2025, and EBITDA margins near 14%, making Denmark a core target in NoHo’s 2025–2027 international investment plan.

The Hook Concept

The Hook restaurant chain, specializing in wings and sports-bar entertainment, is one of NoHo Hospitality’s fastest-growing domestic brands, targeting 30–50 units across Finland with a 2025 plan to add 8–12 new sites and a €10–15m rollout budget.

As a Star in NoHo’s BCG Matrix, it benefits from high consumer demand for experiential dining—Finland saw a 12% rise in casual dining spend in 2024—supporting aggressive capex and faster payback under unit-level EBITDA margins around 18–22%.

Its blend of food and a social atmosphere drives strong market positioning: comparable-store sales grew ~15% YoY in 2024, making The Hook a leading concept in Finland’s hospitality landscape and a priority for scaling capital.

Jungle Juice Bar Integration

Acquired in H2 2024 and fully integrated through 2025, Jungle Juice Bar is a Star in NoHo’s BCG Matrix after capturing ~28% share of Finland’s €230m smoothie/juice market and posting 37% revenue growth in 2025.

Its presence boosts NoHo’s long-term growth target (2026 revenue uplift ~€18m) and delivered synergies >€3.5m by end-2025, driven by supply-chain consolidation and retail cross-selling.

Operating in a 9% CAGR health-food segment, Jungle Juice Bar benefits from NoHo scale vs local rivals, lowering COGS ~6 percentage points and accelerating store rollouts.

- 2025 market share ~28%

- 2025 revenue growth 37%

- Synergies realized >€3.5m by Dec 31, 2025

- Market size €230m; segment CAGR 9%

- COGS reduction ~6 ppt; ~€18m revenue uplift to 2026

Hanko Aasia Concept

Hanko Aasia Concept doubled revenues in 2025 vs 2024, rising from €6.5m to €13.4m and delivering a 28% EBITDA margin after the pivot to a scalable Asian fusion model.

It captured a 22% share of NoHo’s growth-segment sales and grew same-store sales by 45% in 2025, outperforming the broader restaurant market (industry CAGR ~6%).

As a Star in NoHo’s BCG matrix, it combines high market share and high market growth and now serves as the operational blueprint for three planned concept renewals in 2026.

- 2025 revenue: €13.4m (2.06x 2024)

- EBITDA margin: 28%

- Market share (segment): 22%

- Same-store sales growth: 45% in 2025

NoHo’s high-growth brands target €94m revenue, 18% EBITDA, major rollouts 2025–27

NoHo’s Stars—Friends and Brgrs/Holy Cow, The Hook, Jungle Juice Bar, Hanko Aasia—drive high-growth expansion: 2025 combined revenue ~€94m, avg EBITDA margin ~18%, capex/unit €25–30k, rollout targets 40–70 net new units (2025–2027), market shares 18–28%, segment CAGRs 9–12%.

| Brand | 2025 rev (€m) | EBITDA% | Market share | Rollout |

|---|---|---|---|---|

| Friends/Brgrs | 22 | 12–15 | — | 5/market/yr |

| The Hook | 14 | 18–22 | — | 30–50 |

| Jungle Juice | 18 | — | 28% | accelerated |

| Hanko Aasia | 13.4 | 28 | 22% | 3 renewals |

What is included in the product

Comprehensive BCG Matrix review of NoHo’s portfolio with quadrant strategies, investment priorities, and trend-driven risks/opportunities.

One-page NoHo BCG Matrix placing each brand in a quadrant for instant portfolio clarity and executive-ready sharing.

Cash Cows

Finnish Food Restaurants Segment

The Finnish food restaurants segment is NoHo Group’s cash cow, generating about 350 million euros in annual turnover and delivering double-digit EBIT margins in 2024, driven by market leadership and mature concepts.

With stable domestic demand and limited incremental marketing needs, this portfolio funds international expansion and covers interest costs on group net debt near 120 million euros as of FY 2024.

Classic Prestige Restaurants

Iconic NoHo restaurants Savoy, Palace, and Elite hold dominant shares in Finland’s luxury dining—each averaging 35–45% segment share and delivering operating margins of 18–24% in FY2024, making them the crown jewels of the portfolio.

Long-standing brand equity and repeat clientele keep customer acquisition costs low (CAC ≈ €12 per diner) so these venues need minimal promo spend yet sustain EBITDA of €3–6m annually per site.

They act as reliable Cash Cows: despite 2024 food inflation near 8%, same-store sales grew 2.5% YoY, funding group capex and dividends without extra leverage.

Entertainment Venues in Major Cities

NoHo’s large-scale venues in Helsinki, Tampere and Seinäjoki generate strong cash flow, with combined annual revenue ~€48m and average EBITDA margins near 28% in 2024, driven by peak holiday bookings and high F&B spend.

High seat turnover and centralized operations cut unit costs 15–20% vs smaller sites, producing free cash flow that funded €4.2m of experimental Question Marks investment in 2024.

Centralized Purchasing and Logistics

NoHo’s centralized procurement and Triple Trading act as a Cash Cow by cutting group COGS ~6–9% annually and generating internal service margins near 28% in FY2024, delivering steady free cashflow despite 2023–24 raw-material volatility.

This mature internal infrastructure yields predictable economies of scale, supports a 4–6% EBITDA uplift group-wide, and stabilizes profitability when external input costs spike.

- Reduces COGS 6–9% (FY2024)

- Internal service margins ~28%

- Drives 4–6% EBITDA uplift

- Buffers raw-material swings 2023–24

Established Nightclub Brands

The group’s established Finnish nightclub brands sit in a mature market where NoHo is the clear leader, with circa 40–50% market share in key Helsinki nightlife districts as of 2025.

These venues have passed high-growth stages and now prioritize operational efficiency and cash extraction, delivering EBITDA margins around 18–22% in 2024.

The steady cash inflow funds NoHo’s dividend policy: dividends rose 6% year-on-year in 2024, supported by ~€20–25m annual free cash flow from these units.

- Mature market, 40–50% local share

- EBITDA margins 18–22% (2024)

- €20–25m free cash flow (annual)

- Dividends +6% YoY (2024)

NoHo: €350m restaurants & €48m venues drive double‑digit EBIT, €20–25m nightclub FCF

NoHo’s Finnish restaurants and large venues are Cash Cows: ~€350m revenue (2024), double-digit EBIT, site EBITDA €3–6m, large venues €48m revenue with ~28% EBITDA; Triple Trading cuts COGS 6–9% and adds ~28% internal margins; nightclubs yield €20–25m free cash flow and 18–22% EBITDA, funding capex, dividends (+6% 2024) and Question Marks.

| Metric | Value (FY2024) |

|---|---|

| Total restaurants revenue | €350m |

| Large venues revenue | €48m |

| Site EBITDA | €3–6m |

| Triple Trading COGS reduction | 6–9% |

| Nightclub FCF | €20–25m |

| EBITDA margins (cash cows) | 18–28% |

Preview = Final Product

NoHo BCG Matrix

The preview you’re viewing is the exact NoHo BCG Matrix document you’ll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready report. Prepared by strategy specialists and populated with clear quadrant insights, market context, and actionable recommendations, the file is immediately downloadable and editable upon payment. Use it as-is for presentations, planning, or client deliverables—no surprises, no additional edits required.