NoHo Business Model Canvas

NoHo Business Model Canvas: Clear Blueprint for Value, Customers & Revenue

Unlock the full strategic blueprint behind NoHo’s business model—this concise Business Model Canvas maps its value propositions, customer segments, and revenue mechanics to show how the company wins and scales.

Partnerships

Supply Chain and Logistics Partners

The company sources through major F&B wholesalers, securing 8–12% volume discounts across a 1,200-SKU portfolio and cutting COGS by ~3.5% in 2024 vs 2022.

By 2025 partners shift to sustainable sourcing and carbon-neutral logistics, trimming Scope 3 emissions 18% vs 2021, while strategic deals with beverage giants guarantee exclusive SKUs for 420 nightlife venues.

Real Estate Developers and Landlords

NoHo secures city-center and high-footfall mall sites through multi-year deals with major landlords, giving early access to 2024–25 developments and average lease terms of 7–12 years; prime locations drive ~60% of group revenue.

Digital Delivery Platforms

Third-party delivery platforms remain vital for casual dining, with delivery penetration ~25% of UK OOH (out-of-home) burger sales in 2024; NoHo uses them to reach at-home diners while protecting restaurant margins through negotiated commission caps (typical 15–20%).

Integrated POS and API links improve kitchen throughput and enable data-driven demand forecasts, cutting peak-hour ticket times by ~18% and reducing food waste 6–9% in dense urban sites.

International Joint Venture Partners

NoHo used international joint ventures to enter Norway, Denmark and Central Europe, with local partners providing market know-how and operations, cutting scaling risk and speeding openings; the 2024–2025 rollouts added 42 outlets and drove €18.6m incremental GMV in 2025.

- 42 outlets opened (2024–2025)

- €18.6m incremental GMV in 2025

- JV model cut entry time by ~30%

Event and Entertainment Organizers

Collaborating with festival organizers and stadium operators lets NoHo deliver large-scale catering and pop-up bars, capturing peak summer and major-sports demand—events can boost monthly revenue by 40–80%, with festival F&B margins averaging 18–25% in 2024.

Integrating NoHo branding into cultural events increases recognition beyond stores and diversifies income streams during June–September and game seasons.

- Seasonal revenue lift: +40–80%

- F&B margin at events: 18–25% (2024)

- Key periods: June–September, major sports fixtures

- Brand reach: off-site audience exposure +30% per event

NoHo trims costs, cuts emissions and drives growth—€18.6m GMV, 60% prime-site revenue

NoHo locks 8–12% volume discounts on 1,200 SKUs, cutting COGS ~3.5% (2024 vs 2022); sustainable sourcing and carbon-neutral logistics trim Scope 3 emissions 18% (2025 vs 2021). Multi-year landlord deals (avg lease 7–12 yrs) secure prime sites driving ~60% group revenue; JV rollouts added 42 outlets and €18.6m GMV in 2025; event partnerships lift monthly revenue 40–80%.

| Metric | Value |

|---|---|

| SKU discounts | 8–12% |

| COGS reduction | ~3.5% |

| Scope 3 cut | 18% |

| Lease term | 7–12 yrs |

| Prime-site revenue | ~60% |

| JV outlets (2024–25) | 42 |

| Incremental GMV (2025) | €18.6m |

| Event revenue lift | 40–80% |

What is included in the product

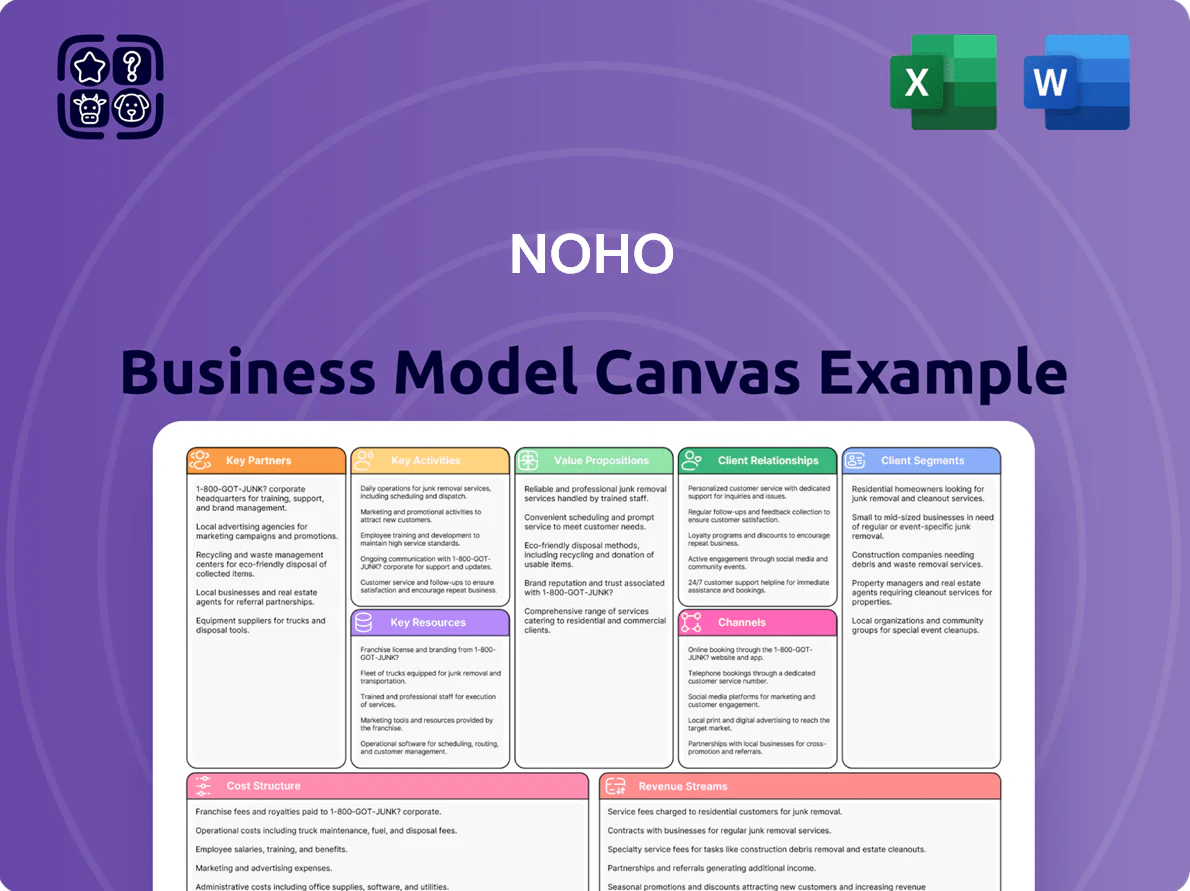

A concise, pre-built Business Model Canvas for NoHo that maps nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—paired with competitive analyses, SWOT-linked insights, and real-world operational detail to support presentations, funding discussions, and strategic decision-making.

Streamlines your strategic planning by presenting NoHo’s entire business model in a clean, editable one-page canvas—ideal for rapid comparison, team collaboration, and saving hours on formatting.

Activities

Concept Development and Innovation

NoHo refines its portfolio by launching or adapting concepts through market research, menu R&D, and interior branding; in 2024 NoHo opened 7 new concepts and reported a 12% like-for-like sales uplift from concept refreshes, and in 2025 the group targets a 20% pipeline tilt to health-conscious and experiential venues to capture younger demographics.

Operational Excellence and Management

Strategic Acquisitions and Integration

A key pillar of growth is acquiring profitable restaurant groups or high-potential units, sourcing targets that can add EBITDA margins of 12–18% and lift group revenue by €10–50m per deal. The team runs rigorous due diligence and integrates purchases into a shared service center to cut operating costs 8–15%; by late 2025 the focus shifted to consolidating Northern Europe with disciplined capital allocation, targeting 3–5 bolt-on deals per year.

Marketing and Brand Positioning

NoHo uses data-driven digital marketing and a tiered loyalty program to defend share in crowded casual dining; paid social and SEM drove 18% year-over-year online bookings in 2024 and loyalty contributed 22% of repeat visits.

Brand architecture management keeps 12 concepts distinct via influencer partnerships, seasonal campaigns, and local PR, yielding a 9% uplift in footfall during targeted promos (2023–24 averages).

- 18% YoY online bookings (2024)

- 22% repeat visits via loyalty

- 12 distinct concepts managed

- 9% average promo footfall uplift (2023–24)

- Influencer + paid social core to acquisition

Supply Chain and Procurement Optimization

Centralized purchasing keeps margins by cutting ingredient costs; NoHo used group buying to save ~8–12% on food and beverage COGS in 2024, offsetting ~60% of UK food inflation that year.

The procurement team exploits scale to secure supply, monitors risk across 12 sourcing countries, and enforces sustainable sourcing (30% of VPO-certified suppliers by end-2025).

- Saved 8–12% on COGS in 2024

- Offset ~60% of UK food inflation 2024

- Risk monitoring across 12 countries

- 30% VPO-certified suppliers target by 2025

NoHo: 320+ sites, 7 new concepts, NPS 58—driving 12–18% deal EBITDA growth

NoHo runs portfolio growth, ops excellence, M&A, marketing, brand and procurement to boost EBITDA: 7 new concepts (2024), 320+ sites (6 countries), NPS 58 (Q4 2025), 12–18% target deal EBITDA, 18% YoY online bookings (2024), 22% repeat via loyalty, saved 8–12% on COGS (2024), 30% VPO suppliers target (2025).

| Metric | Value |

|---|---|

| New concepts (2024) | 7 |

| Sites / countries | 320+ / 6 |

| NPS (Q4 2025) | 58 |

| Deal EBITDA target | 12–18% |

| Online bookings YoY (2024) | 18% |

| Repeat via loyalty | 22% |

| COGS savings (2024) | 8–12% |

| VPO suppliers target (2025) | 30% |

Delivered as Displayed

Business Model Canvas

The preview you see is the actual NoHo Business Model Canvas file, not a mockup—it's a direct snapshot of the exact document you'll receive after purchase.

When you complete your order, you'll instantly get this same fully structured, ready-to-edit canvas in the delivered formats, with all content and pages included.

No fillers or placeholders—what you see is what you’ll own, ready for presenting, editing, and sharing.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

NoHo Business Model Canvas: Clear Blueprint for Value, Customers & Revenue

Unlock the full strategic blueprint behind NoHo’s business model—this concise Business Model Canvas maps its value propositions, customer segments, and revenue mechanics to show how the company wins and scales.

Partnerships

Supply Chain and Logistics Partners

The company sources through major F&B wholesalers, securing 8–12% volume discounts across a 1,200-SKU portfolio and cutting COGS by ~3.5% in 2024 vs 2022.

By 2025 partners shift to sustainable sourcing and carbon-neutral logistics, trimming Scope 3 emissions 18% vs 2021, while strategic deals with beverage giants guarantee exclusive SKUs for 420 nightlife venues.

Real Estate Developers and Landlords

NoHo secures city-center and high-footfall mall sites through multi-year deals with major landlords, giving early access to 2024–25 developments and average lease terms of 7–12 years; prime locations drive ~60% of group revenue.

Digital Delivery Platforms

Third-party delivery platforms remain vital for casual dining, with delivery penetration ~25% of UK OOH (out-of-home) burger sales in 2024; NoHo uses them to reach at-home diners while protecting restaurant margins through negotiated commission caps (typical 15–20%).

Integrated POS and API links improve kitchen throughput and enable data-driven demand forecasts, cutting peak-hour ticket times by ~18% and reducing food waste 6–9% in dense urban sites.

International Joint Venture Partners

NoHo used international joint ventures to enter Norway, Denmark and Central Europe, with local partners providing market know-how and operations, cutting scaling risk and speeding openings; the 2024–2025 rollouts added 42 outlets and drove €18.6m incremental GMV in 2025.

- 42 outlets opened (2024–2025)

- €18.6m incremental GMV in 2025

- JV model cut entry time by ~30%

Event and Entertainment Organizers

Collaborating with festival organizers and stadium operators lets NoHo deliver large-scale catering and pop-up bars, capturing peak summer and major-sports demand—events can boost monthly revenue by 40–80%, with festival F&B margins averaging 18–25% in 2024.

Integrating NoHo branding into cultural events increases recognition beyond stores and diversifies income streams during June–September and game seasons.

- Seasonal revenue lift: +40–80%

- F&B margin at events: 18–25% (2024)

- Key periods: June–September, major sports fixtures

- Brand reach: off-site audience exposure +30% per event

NoHo trims costs, cuts emissions and drives growth—€18.6m GMV, 60% prime-site revenue

NoHo locks 8–12% volume discounts on 1,200 SKUs, cutting COGS ~3.5% (2024 vs 2022); sustainable sourcing and carbon-neutral logistics trim Scope 3 emissions 18% (2025 vs 2021). Multi-year landlord deals (avg lease 7–12 yrs) secure prime sites driving ~60% group revenue; JV rollouts added 42 outlets and €18.6m GMV in 2025; event partnerships lift monthly revenue 40–80%.

| Metric | Value |

|---|---|

| SKU discounts | 8–12% |

| COGS reduction | ~3.5% |

| Scope 3 cut | 18% |

| Lease term | 7–12 yrs |

| Prime-site revenue | ~60% |

| JV outlets (2024–25) | 42 |

| Incremental GMV (2025) | €18.6m |

| Event revenue lift | 40–80% |

What is included in the product

A concise, pre-built Business Model Canvas for NoHo that maps nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—paired with competitive analyses, SWOT-linked insights, and real-world operational detail to support presentations, funding discussions, and strategic decision-making.

Streamlines your strategic planning by presenting NoHo’s entire business model in a clean, editable one-page canvas—ideal for rapid comparison, team collaboration, and saving hours on formatting.

Activities

Concept Development and Innovation

NoHo refines its portfolio by launching or adapting concepts through market research, menu R&D, and interior branding; in 2024 NoHo opened 7 new concepts and reported a 12% like-for-like sales uplift from concept refreshes, and in 2025 the group targets a 20% pipeline tilt to health-conscious and experiential venues to capture younger demographics.

Operational Excellence and Management

Strategic Acquisitions and Integration

A key pillar of growth is acquiring profitable restaurant groups or high-potential units, sourcing targets that can add EBITDA margins of 12–18% and lift group revenue by €10–50m per deal. The team runs rigorous due diligence and integrates purchases into a shared service center to cut operating costs 8–15%; by late 2025 the focus shifted to consolidating Northern Europe with disciplined capital allocation, targeting 3–5 bolt-on deals per year.

Marketing and Brand Positioning

NoHo uses data-driven digital marketing and a tiered loyalty program to defend share in crowded casual dining; paid social and SEM drove 18% year-over-year online bookings in 2024 and loyalty contributed 22% of repeat visits.

Brand architecture management keeps 12 concepts distinct via influencer partnerships, seasonal campaigns, and local PR, yielding a 9% uplift in footfall during targeted promos (2023–24 averages).

- 18% YoY online bookings (2024)

- 22% repeat visits via loyalty

- 12 distinct concepts managed

- 9% average promo footfall uplift (2023–24)

- Influencer + paid social core to acquisition

Supply Chain and Procurement Optimization

Centralized purchasing keeps margins by cutting ingredient costs; NoHo used group buying to save ~8–12% on food and beverage COGS in 2024, offsetting ~60% of UK food inflation that year.

The procurement team exploits scale to secure supply, monitors risk across 12 sourcing countries, and enforces sustainable sourcing (30% of VPO-certified suppliers by end-2025).

- Saved 8–12% on COGS in 2024

- Offset ~60% of UK food inflation 2024

- Risk monitoring across 12 countries

- 30% VPO-certified suppliers target by 2025

NoHo: 320+ sites, 7 new concepts, NPS 58—driving 12–18% deal EBITDA growth

NoHo runs portfolio growth, ops excellence, M&A, marketing, brand and procurement to boost EBITDA: 7 new concepts (2024), 320+ sites (6 countries), NPS 58 (Q4 2025), 12–18% target deal EBITDA, 18% YoY online bookings (2024), 22% repeat via loyalty, saved 8–12% on COGS (2024), 30% VPO suppliers target (2025).

| Metric | Value |

|---|---|

| New concepts (2024) | 7 |

| Sites / countries | 320+ / 6 |

| NPS (Q4 2025) | 58 |

| Deal EBITDA target | 12–18% |

| Online bookings YoY (2024) | 18% |

| Repeat via loyalty | 22% |

| COGS savings (2024) | 8–12% |

| VPO suppliers target (2025) | 30% |

Delivered as Displayed

Business Model Canvas

The preview you see is the actual NoHo Business Model Canvas file, not a mockup—it's a direct snapshot of the exact document you'll receive after purchase.

When you complete your order, you'll instantly get this same fully structured, ready-to-edit canvas in the delivered formats, with all content and pages included.

No fillers or placeholders—what you see is what you’ll own, ready for presenting, editing, and sharing.