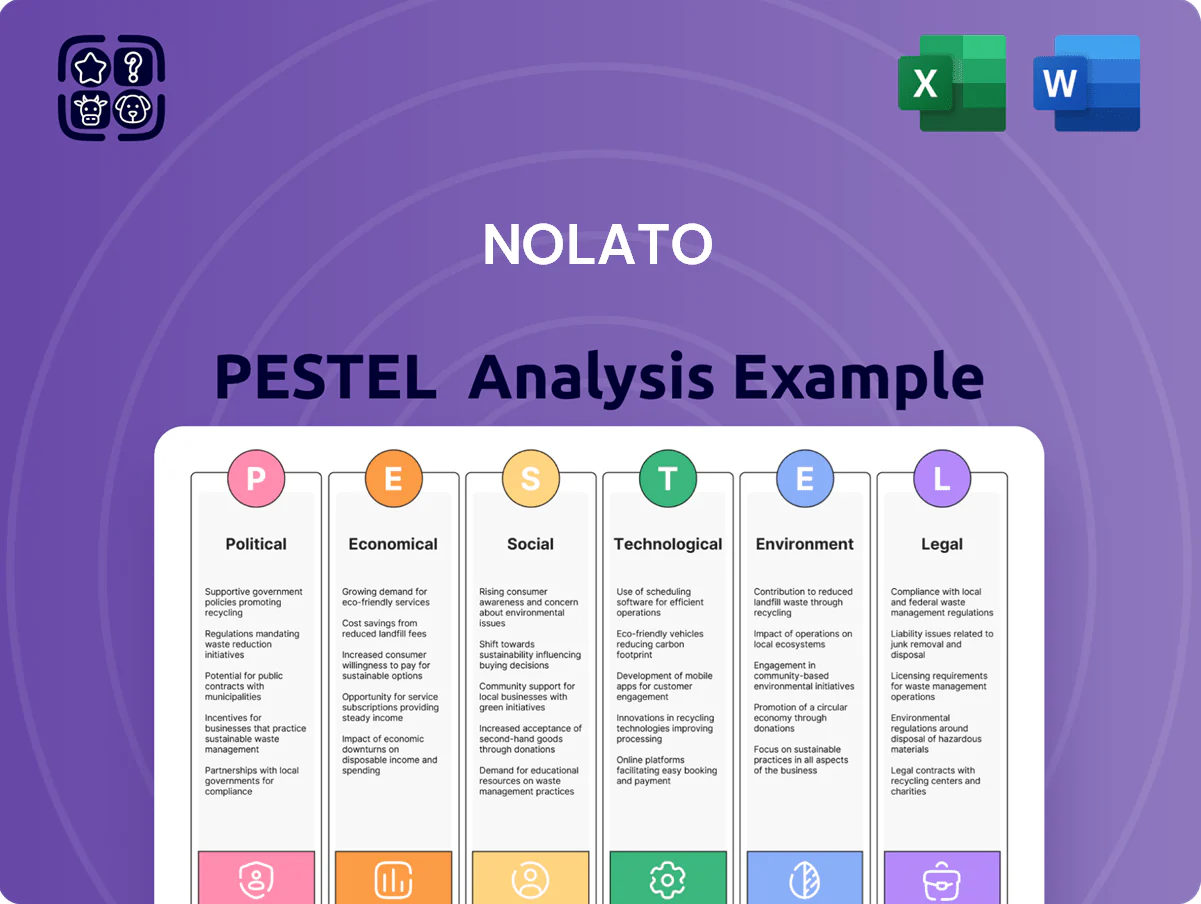

Nolato PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, economic cycles, and tech innovation are shaping Nolato’s prospects with our concise PESTLE snapshot—designed for investors and strategists who need clarity fast. Purchase the full PESTLE to access a detailed, actionable breakdown that pinpoints risks, growth levers, and regulatory pressures you can apply immediately. Get the complete analysis now and make smarter, faster decisions.

Political factors

Geopolitical Trade Relations

Global trade tensions among the US, China and EU in late 2025 have pushed Nolato to expand regional manufacturing; the company reported 18% of revenue in 2024 from Asia but invested €45m in 2025 to shift 12% of polymer capacity to Europe and North America to reduce tariff exposure.

Healthcare Policy and Spending

Industrial Subsidies and Green Deals

European Green Deal targets a 55% cut in CO2 emissions by 2030 and the EU’s 2023 Fit for 55 package injects €300+ billion/year in green investments; industrial subsidies and EV infrastructure funds (e.g., Connecting Europe Facility increases) boost demand for Nolato’s lightweight polymer components—supporting 5–10% volume growth in automotive/industrial segments forecasted 2024–2026—aligning strategy with state-backed tech shifts captures grant and procurement opportunities.

Labor Regulations and Social Policy

- Labor cost pressure: wage rises 7–9% (2024 ILO)

- Compliance burden: audits +18% (2023)

- Reputation risk: impacts orders and financing

Global Tax and Financial Transparency

The OECD/G20 global minimum tax (Pillar Two) and expanded beneficial ownership reporting increase Nolato’s compliance burden across its ~20 international entities, requiring consistent transfer pricing and consolidated accounting to avoid effective tax rates deviating from the new 15% floor.

Political alignment on taxing multinationals forces Nolato to invest in centralized tax governance; in 2024 peer analysis shows multinationals increased tax-control staffing by ~12%, a proxy for expected Nolato resource needs.

These rules necessitate higher administrative costs to manage compliance while preserving cash flow and optimizing group structure, affecting near-term operating margins and capital allocation.

- Applies to ~20 subsidiaries — 15% minimum tax

- Estimated +12% tax-control staffing need (2024 peer data)

- Elevated compliance costs pressure operating margins and capital allocation

Reshoring €45M, rising wages & audits, EU green auto boost; 15% global minimum tax

Trade tensions and tariffs drove €45m reshoring in 2025; 18% revenue from Asia (2024). OECD health spend 9.2% GDP (2023); pharma public spend +3.5% (2024) affecting medical demand. EU Green Deal and Fit for 55 spur 5–10% automotive volume growth (2024–26). Labor costs +7–9% (2024 ILO); audits +18% (2023). Pillar Two 15% minimum tax across ~20 entities.

| Metric | Value |

|---|---|

| Asia rev (2024) | 18% |

| Reshoring capex (2025) | €45m |

| OECD health spend (2023) | 9.2% GDP |

| Labour wage rise (2024) | 7–9% |

| Audits (2023) | +18% |

| Min tax | 15% (~20 entities) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Nolato across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-backed trends, sector-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans or investor materials.

Compact PESTLE summary that highlights Nolato's external risks and opportunities for quick reference in meetings or presentations.

Economic factors

Polymer and Raw Material Price Volatility

Polymer and silicone costs remain pivotal for Nolato’s margins into 2026; oil-based polymer feedstock prices averaged about $850/ton in 2025, exposing the company to input-cost swings after raw material cost represented roughly 28% of COGS in 2024.

Although global inflation eased to ~3.2% in 2025, energy-price volatility—Brent averaging $78/bbl in 2025 with quarterly swings ±15%—directly raises production costs for Nolato’s industrial and automotive components.

Hedging, long-term supplier contracts and indexed price-adjustment clauses have been increasingly used; firms locking multiyear polymer contracts in 2024 saw cost predictability improve while spot-buy exposure remained a key margin risk for 2026 planning.

Interest Rates and Capital Allocation

Prevailing interest rates shape Nolato’s funding for capacity expansions and tech upgrades; Sweden’s 2025 key policy rate around 4.0% raises weighted average borrowing costs, constraining capital intensity. High rates favor conservative CAPEX, pushing management toward organic growth and efficiency over M&A—Nolato’s 2024 net debt/EBITDA was about 1.2x, supporting measured investments. Investors watch debt-to-equity (equity ratio ~45% in 2024) and free cash flow—Nolato reported SEK 490m FCF in 2024—to ensure debt service and R&D continuity.

Growth of the Global MedTech Market

The global MedTech market grew to about USD 540 billion in 2024 and is forecasted to reach ~USD 720 billion by 2030, providing Nolato a resilient revenue stream that offsets automotive cyclicality.

Rising healthcare spend in emerging markets (CAGR ~6–7%) and ongoing innovation in developed markets drive demand for high-quality polymer components used in diagnostics, drug delivery and connected devices.

MedTech now represents a core growth pillar for Nolato, underpinning long-term economic value for shareholders through stable margins and recurring order flows.

Energy Costs in European Manufacturing

High European energy prices, with industrial gas averaging about EUR 40–60/MWh in 2024 and Swedish electricity wholesale around SEK 1–1.2/kWh (≈EUR 90–108/MWh), press Nolato’s Sweden and Central Europe plants, raising manufacturing costs and squeezing margins.

To mitigate this, Nolato has accelerated investments in energy-efficient machinery and on-site renewables, aiming to cut energy intensity by targeted single-digit percentages by 2025.

Successfully optimizing consumption and increasing renewables share will be decisive for Nolato to sustain global price competitiveness amid volatile wholesale energy markets.

- 2024 EU industrial gas EUR 40–60/MWh; Sweden wholesale electricity ≈EUR 90–108/MWh

- Nolato targeting single-digit % energy-intensity reductions by 2025

- On-site renewables and efficiency investments key to protect margins

Currency Exchange Rate Fluctuations

As a Swedish multinational, Nolato faces sizable transaction and translation exposure; in 2024 around 62% of net sales were outside Sweden, making SEK/USD and SEK/EUR swings materially affect reported revenue.

From 2022–2024 SEK strengthened ~8% vs USD and weakened ~3% vs EUR at times, impacting export competitiveness and gross margins for foreign sales.

Management uses forward contracts, currency options and production localization—20+ global production sites—to hedge and reduce FX volatility on earnings.

- ~62% sales outside Sweden (2024)

- SEK moved ~+8% vs USD (2022–2024 peak)

- ~20 global production sites used for localization

- Hedging via forwards/options to limit translation risk

Stable MedTech demand offsets input and FX pressures as FCF supports cautious CAPEX

Input-costs (polymers/silicones ~28% COGS) and energy (Brent $78/bbl 2025; EU gas €40–60/MWh) drive margins; 2024 FCF SEK 490m and net debt/EBITDA ~1.2x constrain CAPEX amid 4.0% Swedish policy rate; MedTech (~USD 540bn 2024) offers stable demand; FX exposure (62% sales outside Sweden) managed via hedges and localization.

| Metric | Value |

|---|---|

| Polymer cost share | ~28% COGS (2024) |

| Brent | $78/bbl (2025) |

| FCF | SEK 490m (2024) |

| Net debt/EBITDA | ~1.2x (2024) |

| Sales outside Sweden | ~62% (2024) |

Preview Before You Purchase

Nolato PESTLE Analysis

The preview shown here is the exact Nolato PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers, just the finished file.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, economic cycles, and tech innovation are shaping Nolato’s prospects with our concise PESTLE snapshot—designed for investors and strategists who need clarity fast. Purchase the full PESTLE to access a detailed, actionable breakdown that pinpoints risks, growth levers, and regulatory pressures you can apply immediately. Get the complete analysis now and make smarter, faster decisions.

Political factors

Geopolitical Trade Relations

Global trade tensions among the US, China and EU in late 2025 have pushed Nolato to expand regional manufacturing; the company reported 18% of revenue in 2024 from Asia but invested €45m in 2025 to shift 12% of polymer capacity to Europe and North America to reduce tariff exposure.

Healthcare Policy and Spending

Industrial Subsidies and Green Deals

European Green Deal targets a 55% cut in CO2 emissions by 2030 and the EU’s 2023 Fit for 55 package injects €300+ billion/year in green investments; industrial subsidies and EV infrastructure funds (e.g., Connecting Europe Facility increases) boost demand for Nolato’s lightweight polymer components—supporting 5–10% volume growth in automotive/industrial segments forecasted 2024–2026—aligning strategy with state-backed tech shifts captures grant and procurement opportunities.

Labor Regulations and Social Policy

- Labor cost pressure: wage rises 7–9% (2024 ILO)

- Compliance burden: audits +18% (2023)

- Reputation risk: impacts orders and financing

Global Tax and Financial Transparency

The OECD/G20 global minimum tax (Pillar Two) and expanded beneficial ownership reporting increase Nolato’s compliance burden across its ~20 international entities, requiring consistent transfer pricing and consolidated accounting to avoid effective tax rates deviating from the new 15% floor.

Political alignment on taxing multinationals forces Nolato to invest in centralized tax governance; in 2024 peer analysis shows multinationals increased tax-control staffing by ~12%, a proxy for expected Nolato resource needs.

These rules necessitate higher administrative costs to manage compliance while preserving cash flow and optimizing group structure, affecting near-term operating margins and capital allocation.

- Applies to ~20 subsidiaries — 15% minimum tax

- Estimated +12% tax-control staffing need (2024 peer data)

- Elevated compliance costs pressure operating margins and capital allocation

Reshoring €45M, rising wages & audits, EU green auto boost; 15% global minimum tax

Trade tensions and tariffs drove €45m reshoring in 2025; 18% revenue from Asia (2024). OECD health spend 9.2% GDP (2023); pharma public spend +3.5% (2024) affecting medical demand. EU Green Deal and Fit for 55 spur 5–10% automotive volume growth (2024–26). Labor costs +7–9% (2024 ILO); audits +18% (2023). Pillar Two 15% minimum tax across ~20 entities.

| Metric | Value |

|---|---|

| Asia rev (2024) | 18% |

| Reshoring capex (2025) | €45m |

| OECD health spend (2023) | 9.2% GDP |

| Labour wage rise (2024) | 7–9% |

| Audits (2023) | +18% |

| Min tax | 15% (~20 entities) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Nolato across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-backed trends, sector-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans or investor materials.

Compact PESTLE summary that highlights Nolato's external risks and opportunities for quick reference in meetings or presentations.

Economic factors

Polymer and Raw Material Price Volatility

Polymer and silicone costs remain pivotal for Nolato’s margins into 2026; oil-based polymer feedstock prices averaged about $850/ton in 2025, exposing the company to input-cost swings after raw material cost represented roughly 28% of COGS in 2024.

Although global inflation eased to ~3.2% in 2025, energy-price volatility—Brent averaging $78/bbl in 2025 with quarterly swings ±15%—directly raises production costs for Nolato’s industrial and automotive components.

Hedging, long-term supplier contracts and indexed price-adjustment clauses have been increasingly used; firms locking multiyear polymer contracts in 2024 saw cost predictability improve while spot-buy exposure remained a key margin risk for 2026 planning.

Interest Rates and Capital Allocation

Prevailing interest rates shape Nolato’s funding for capacity expansions and tech upgrades; Sweden’s 2025 key policy rate around 4.0% raises weighted average borrowing costs, constraining capital intensity. High rates favor conservative CAPEX, pushing management toward organic growth and efficiency over M&A—Nolato’s 2024 net debt/EBITDA was about 1.2x, supporting measured investments. Investors watch debt-to-equity (equity ratio ~45% in 2024) and free cash flow—Nolato reported SEK 490m FCF in 2024—to ensure debt service and R&D continuity.

Growth of the Global MedTech Market

The global MedTech market grew to about USD 540 billion in 2024 and is forecasted to reach ~USD 720 billion by 2030, providing Nolato a resilient revenue stream that offsets automotive cyclicality.

Rising healthcare spend in emerging markets (CAGR ~6–7%) and ongoing innovation in developed markets drive demand for high-quality polymer components used in diagnostics, drug delivery and connected devices.

MedTech now represents a core growth pillar for Nolato, underpinning long-term economic value for shareholders through stable margins and recurring order flows.

Energy Costs in European Manufacturing

High European energy prices, with industrial gas averaging about EUR 40–60/MWh in 2024 and Swedish electricity wholesale around SEK 1–1.2/kWh (≈EUR 90–108/MWh), press Nolato’s Sweden and Central Europe plants, raising manufacturing costs and squeezing margins.

To mitigate this, Nolato has accelerated investments in energy-efficient machinery and on-site renewables, aiming to cut energy intensity by targeted single-digit percentages by 2025.

Successfully optimizing consumption and increasing renewables share will be decisive for Nolato to sustain global price competitiveness amid volatile wholesale energy markets.

- 2024 EU industrial gas EUR 40–60/MWh; Sweden wholesale electricity ≈EUR 90–108/MWh

- Nolato targeting single-digit % energy-intensity reductions by 2025

- On-site renewables and efficiency investments key to protect margins

Currency Exchange Rate Fluctuations

As a Swedish multinational, Nolato faces sizable transaction and translation exposure; in 2024 around 62% of net sales were outside Sweden, making SEK/USD and SEK/EUR swings materially affect reported revenue.

From 2022–2024 SEK strengthened ~8% vs USD and weakened ~3% vs EUR at times, impacting export competitiveness and gross margins for foreign sales.

Management uses forward contracts, currency options and production localization—20+ global production sites—to hedge and reduce FX volatility on earnings.

- ~62% sales outside Sweden (2024)

- SEK moved ~+8% vs USD (2022–2024 peak)

- ~20 global production sites used for localization

- Hedging via forwards/options to limit translation risk

Stable MedTech demand offsets input and FX pressures as FCF supports cautious CAPEX

Input-costs (polymers/silicones ~28% COGS) and energy (Brent $78/bbl 2025; EU gas €40–60/MWh) drive margins; 2024 FCF SEK 490m and net debt/EBITDA ~1.2x constrain CAPEX amid 4.0% Swedish policy rate; MedTech (~USD 540bn 2024) offers stable demand; FX exposure (62% sales outside Sweden) managed via hedges and localization.

| Metric | Value |

|---|---|

| Polymer cost share | ~28% COGS (2024) |

| Brent | $78/bbl (2025) |

| FCF | SEK 490m (2024) |

| Net debt/EBITDA | ~1.2x (2024) |

| Sales outside Sweden | ~62% (2024) |

Preview Before You Purchase

Nolato PESTLE Analysis

The preview shown here is the exact Nolato PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers, just the finished file.