Nomad Foods Porter's Five Forces Analysis

Don't Miss the Bigger Picture

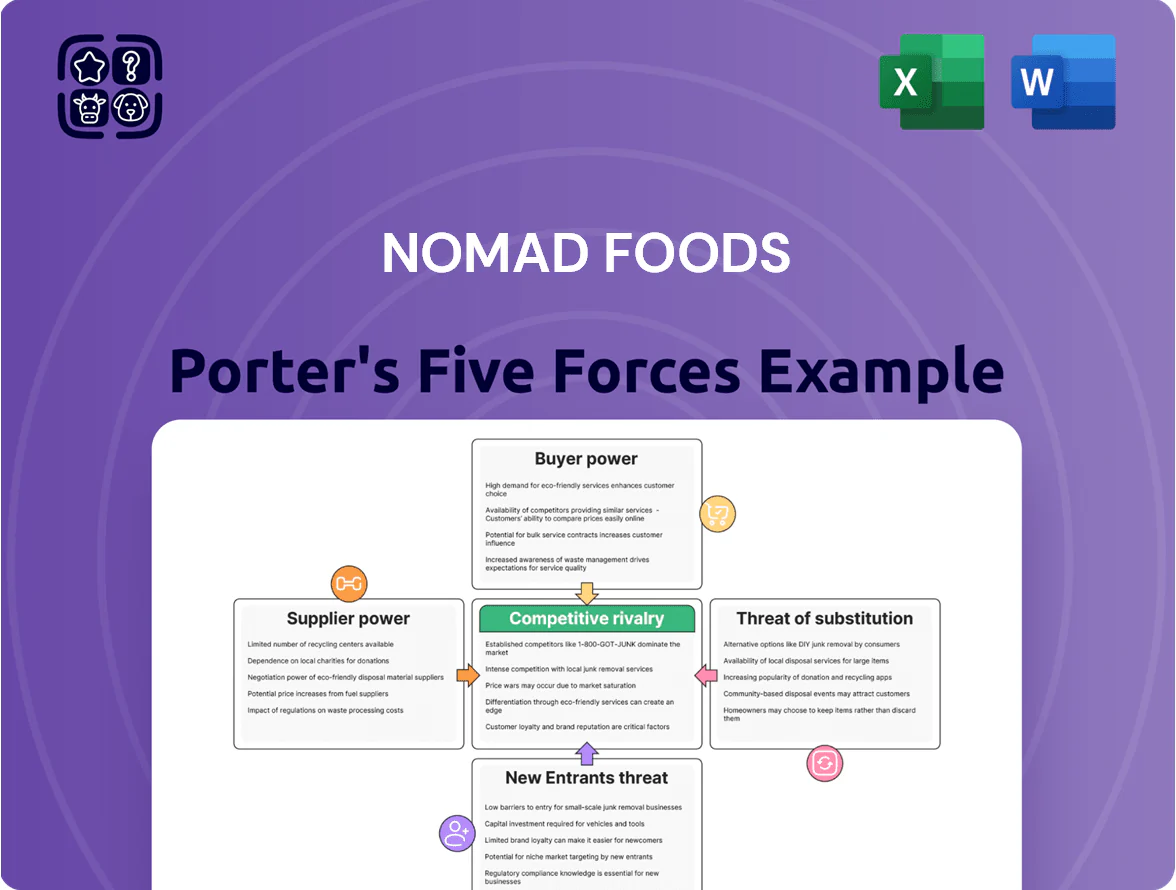

Nomad Foods faces intense supplier negotiation for raw materials, moderate buyer power amid branded frozen-food loyalty, significant competition from private labels and global players, manageable threat of new entrants due to scale advantages, and evolving substitute risks from fresh-food trends; this snapshot hints at strategic pressures but omits force-by-force ratings and implications.

Suppliers Bargaining Power

Fragmented agricultural and seafood supply base

Nomad Foods sources raw materials from thousands of independent European and global farmers and fisheries, so supplier concentration is low and the firm shifted ~65% of procurement volumes across suppliers in 2024 to optimise costs; this fragmentation limits individual supplier power. Still, suppliers of sustainably certified fish (MSC/ASC) or organic vegetables command higher leverage given limited certified supply—these account for ~18% of input spend in 2024.

Volatility in global commodity pricing

Nomad Foods is highly exposed to volatility in fish, vegetable and energy costs; fish accounts for ~28% of COGS and energy/cold storage added ~6% in 2024, so price swings hit margins quickly.

The firm uses forward contracts covering ~60% of near-term purchases to hedge spikes, but long-term inflation (EU food CPI up 5.1% in 2024) strengthens suppliers in renegotiations.

Environmental shifts and EU/North Atlantic fishing quotas through late 2025 have tightened supply elasticity for cod and haddock, keeping spot prices elevated and supplier bargaining power higher.

Strict adherence to sustainability and ESG standards

Nomad Foods’ strict MSC (Marine Stewardship Council) and ASC (Aquaculture Stewardship Council) requirements shrink its supplier pool, raising supplier bargaining power as certified producers are scarce; globally, only about 15% of seafood producers held such certifications by 2024. This certification reliance lets suppliers demand premiums—often 5–15% higher prices—since other ESG-focused firms like Unilever and Nestlé compete for the same vendors. To secure supply, Nomad commonly signs multi-year contracts and vertical partnership deals covering 3–7 years, locking in volumes and quality.

Impact of logistics and cold chain costs

Suppliers of specialized refrigerated logistics hold strong leverage over Nomad Foods because frozen supply chains need tight temperature control and have high switching costs.

In 2025 rising fuel prices (average diesel up ~18% vs 2024) and a 6–8% transport labor shortfall pushed refrigerated transport rates up 10–15%, squeezing margins.

Nomad has limited short-term partner flexibility; any switch risks spoilage and service gaps that cost millions in lost product and sales.

- Specialized logistics = high switching cost

- Diesel +18% YoY in 2025

- Refrigerated rates +10–15% in 2025

- Labor shortfall 6–8% in transport

Limited threat of forward integration

Most agricultural and seafood suppliers lack the capital and brand expertise to build consumer frozen-meal businesses, so they rely on large processors like Nomad Foods, lowering supplier bargaining power.

Flash-freezing technology and global cold-chain logistics are complex and costly—CapEx and operating scale needed act as a barrier to forward integration; Nomad reported €3.6bn revenue in 2024, highlighting scale advantage.

- Suppliers dependent on processors

- High CapEx for freezing/distribution

- Branding/marketing gaps for suppliers

- Nomad scale: €3.6bn revenue (2024)

Nomad Foods: Moderate Supplier Power, Cost Pressure from Fish, Diesel & Cold-Chain

Supplier power for Nomad Foods is moderate: fragmented raw-material base lowers power, but certified seafood/organic inputs (≈18% spend) and specialized cold-logistics increase leverage; fish = ~28% of COGS, energy/cold = ~6% (2024). Hedging covers ~60% near-term buys; multi-year contracts (3–7 yrs) mitigate but rising diesel (+18% in 2025) and refrigerated rates (+10–15%) keep supplier pressure.

| Metric | 2024/2025 |

|---|---|

| Revenue | €3.6bn (2024) |

| Fish share of COGS | 28% |

| Certified input spend | 18% |

| Hedge coverage | ~60% |

| Diesel change | +18% (2025) |

| Refrig rates | +10–15% (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Nomad Foods that uncovers competitive drivers, supplier and buyer power, threat of substitutes and entrants, and highlights disruptive trends and strategic levers to protect margins and market share.

A concise Porter's Five Forces one-sheet for Nomad Foods—quickly gauge supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic decisions.

Customers Bargaining Power

High concentration of European grocery retailers

Europe’s grocery market is concentrated: in 2024 Tesco, Carrefour and Lidl each held ~5–10% market share in key countries, and the top 10 retailers accounted for roughly 60% of grocery sales, giving them strong leverage over suppliers like Nomad Foods. These chains routinely extract trade discounts of 10–25%, demand prime shelf space and force participation in promotions, squeezing supplier margins. Since Nomad earns over 70% of revenue via European retail channels, it faces constant pressure to cut wholesale prices to retain listings.

Expansion and quality of private label brands

Retailers have expanded private-label frozen ranges that sit beside Birds Eye and Iglo at lower prices; private labels grew to ~28% share of UK frozen meals by 2024, up from 21% in 2019 (Kantar).

By 2025 store-brand quality perception rose: 49% of shoppers now view own-label as equal or better for frozen veg/meals, making them viable for budget-conscious buyers.

This shift forces Nomad Foods to ramp brand investment—marketing, R&D, premium SKUs—after Nomad reported 2024 gross margin pressure of ~140 basis points vs. 2021.

Low switching costs for end consumers

Individual shoppers face virtually no cost switching from Nomad Foods to rivals or private labels; NielsenIQ data from 2024 shows private label share in European frozen foods at ~33%, up 2 percentage points year-over-year.

Increased price sensitivity due to economic pressures

Macroeconomic strain through 2025 left real household disposable income down ~1.5% in EU markets, pushing shoppers to hunt unit-price deals and larger packs; Nomad Foods saw U.K. frozen category volumes shift toward value SKUs by ~6% in 2024.

Consumers now steer trends, forcing Nomad to redesign pack sizes and price architecture to protect margin while matching demand for larger, lower-priced formats.

- Real household income −1.5% (EU, 2025)

- UK frozen value-SKU volume +6% (2024)

- Shift: unit-price comparisons, larger packs

- Action: adjust packaging/portion sizes

Influence of digital platforms and e-commerce

The rise of online grocery and quick-commerce apps lets consumers compare prices instantly; in 2024 online grocery penetration in Europe hit ~15% of grocery sales, raising price sensitivity for Nomad Foods.

Retailers use analytics and personalized promos—e.g., Ocado and Carrefour reported 20–30% uplift from targeted discounts—forcing brands into tighter digital promo cycles.

Nomad must keep share-of-shelf and promo elasticity on platforms, balancing visibility vs. margin in a transparent marketplace where Buy Box placement and fast delivery drive volume.

- Online grocery ~15% Europe (2024)

- Targeted promos: 20–30% uplift

- Focus: share-of-shelf, Buy Box, promo elasticity

Nomad squeezed: retailer power, private-label rise and promo-led margin erosion

Retailer concentration (top10 ≈60% sales) and private-label growth (~33% frozen share, 2024) give buyers high leverage; trade discounts 10–25% and promo pressure cut Nomad’s margins (~140bps decline since 2021). Online grocery ~15% (2024) raises price visibility; EU real disposable income −1.5% (2025) pushes value SKUs. Nomad must trade margin for shelf/promo share.

| Metric | Value |

|---|---|

| Top-10 retailer share | ~60% |

| Private-label frozen | ~33% (2024) |

| Online grocery | ~15% (2024) |

| EU real income | −1.5% (2025) |

| Margin impact | −140bps (since 2021) |

Same Document Delivered

Nomad Foods Porter's Five Forces Analysis

This preview shows the exact Nomad Foods Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the full, professionally formatted document is ready for instant download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Nomad Foods faces intense supplier negotiation for raw materials, moderate buyer power amid branded frozen-food loyalty, significant competition from private labels and global players, manageable threat of new entrants due to scale advantages, and evolving substitute risks from fresh-food trends; this snapshot hints at strategic pressures but omits force-by-force ratings and implications.

Suppliers Bargaining Power

Fragmented agricultural and seafood supply base

Nomad Foods sources raw materials from thousands of independent European and global farmers and fisheries, so supplier concentration is low and the firm shifted ~65% of procurement volumes across suppliers in 2024 to optimise costs; this fragmentation limits individual supplier power. Still, suppliers of sustainably certified fish (MSC/ASC) or organic vegetables command higher leverage given limited certified supply—these account for ~18% of input spend in 2024.

Volatility in global commodity pricing

Nomad Foods is highly exposed to volatility in fish, vegetable and energy costs; fish accounts for ~28% of COGS and energy/cold storage added ~6% in 2024, so price swings hit margins quickly.

The firm uses forward contracts covering ~60% of near-term purchases to hedge spikes, but long-term inflation (EU food CPI up 5.1% in 2024) strengthens suppliers in renegotiations.

Environmental shifts and EU/North Atlantic fishing quotas through late 2025 have tightened supply elasticity for cod and haddock, keeping spot prices elevated and supplier bargaining power higher.

Strict adherence to sustainability and ESG standards

Nomad Foods’ strict MSC (Marine Stewardship Council) and ASC (Aquaculture Stewardship Council) requirements shrink its supplier pool, raising supplier bargaining power as certified producers are scarce; globally, only about 15% of seafood producers held such certifications by 2024. This certification reliance lets suppliers demand premiums—often 5–15% higher prices—since other ESG-focused firms like Unilever and Nestlé compete for the same vendors. To secure supply, Nomad commonly signs multi-year contracts and vertical partnership deals covering 3–7 years, locking in volumes and quality.

Impact of logistics and cold chain costs

Suppliers of specialized refrigerated logistics hold strong leverage over Nomad Foods because frozen supply chains need tight temperature control and have high switching costs.

In 2025 rising fuel prices (average diesel up ~18% vs 2024) and a 6–8% transport labor shortfall pushed refrigerated transport rates up 10–15%, squeezing margins.

Nomad has limited short-term partner flexibility; any switch risks spoilage and service gaps that cost millions in lost product and sales.

- Specialized logistics = high switching cost

- Diesel +18% YoY in 2025

- Refrigerated rates +10–15% in 2025

- Labor shortfall 6–8% in transport

Limited threat of forward integration

Most agricultural and seafood suppliers lack the capital and brand expertise to build consumer frozen-meal businesses, so they rely on large processors like Nomad Foods, lowering supplier bargaining power.

Flash-freezing technology and global cold-chain logistics are complex and costly—CapEx and operating scale needed act as a barrier to forward integration; Nomad reported €3.6bn revenue in 2024, highlighting scale advantage.

- Suppliers dependent on processors

- High CapEx for freezing/distribution

- Branding/marketing gaps for suppliers

- Nomad scale: €3.6bn revenue (2024)

Nomad Foods: Moderate Supplier Power, Cost Pressure from Fish, Diesel & Cold-Chain

Supplier power for Nomad Foods is moderate: fragmented raw-material base lowers power, but certified seafood/organic inputs (≈18% spend) and specialized cold-logistics increase leverage; fish = ~28% of COGS, energy/cold = ~6% (2024). Hedging covers ~60% near-term buys; multi-year contracts (3–7 yrs) mitigate but rising diesel (+18% in 2025) and refrigerated rates (+10–15%) keep supplier pressure.

| Metric | 2024/2025 |

|---|---|

| Revenue | €3.6bn (2024) |

| Fish share of COGS | 28% |

| Certified input spend | 18% |

| Hedge coverage | ~60% |

| Diesel change | +18% (2025) |

| Refrig rates | +10–15% (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Nomad Foods that uncovers competitive drivers, supplier and buyer power, threat of substitutes and entrants, and highlights disruptive trends and strategic levers to protect margins and market share.

A concise Porter's Five Forces one-sheet for Nomad Foods—quickly gauge supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic decisions.

Customers Bargaining Power

High concentration of European grocery retailers

Europe’s grocery market is concentrated: in 2024 Tesco, Carrefour and Lidl each held ~5–10% market share in key countries, and the top 10 retailers accounted for roughly 60% of grocery sales, giving them strong leverage over suppliers like Nomad Foods. These chains routinely extract trade discounts of 10–25%, demand prime shelf space and force participation in promotions, squeezing supplier margins. Since Nomad earns over 70% of revenue via European retail channels, it faces constant pressure to cut wholesale prices to retain listings.

Expansion and quality of private label brands

Retailers have expanded private-label frozen ranges that sit beside Birds Eye and Iglo at lower prices; private labels grew to ~28% share of UK frozen meals by 2024, up from 21% in 2019 (Kantar).

By 2025 store-brand quality perception rose: 49% of shoppers now view own-label as equal or better for frozen veg/meals, making them viable for budget-conscious buyers.

This shift forces Nomad Foods to ramp brand investment—marketing, R&D, premium SKUs—after Nomad reported 2024 gross margin pressure of ~140 basis points vs. 2021.

Low switching costs for end consumers

Individual shoppers face virtually no cost switching from Nomad Foods to rivals or private labels; NielsenIQ data from 2024 shows private label share in European frozen foods at ~33%, up 2 percentage points year-over-year.

Increased price sensitivity due to economic pressures

Macroeconomic strain through 2025 left real household disposable income down ~1.5% in EU markets, pushing shoppers to hunt unit-price deals and larger packs; Nomad Foods saw U.K. frozen category volumes shift toward value SKUs by ~6% in 2024.

Consumers now steer trends, forcing Nomad to redesign pack sizes and price architecture to protect margin while matching demand for larger, lower-priced formats.

- Real household income −1.5% (EU, 2025)

- UK frozen value-SKU volume +6% (2024)

- Shift: unit-price comparisons, larger packs

- Action: adjust packaging/portion sizes

Influence of digital platforms and e-commerce

The rise of online grocery and quick-commerce apps lets consumers compare prices instantly; in 2024 online grocery penetration in Europe hit ~15% of grocery sales, raising price sensitivity for Nomad Foods.

Retailers use analytics and personalized promos—e.g., Ocado and Carrefour reported 20–30% uplift from targeted discounts—forcing brands into tighter digital promo cycles.

Nomad must keep share-of-shelf and promo elasticity on platforms, balancing visibility vs. margin in a transparent marketplace where Buy Box placement and fast delivery drive volume.

- Online grocery ~15% Europe (2024)

- Targeted promos: 20–30% uplift

- Focus: share-of-shelf, Buy Box, promo elasticity

Nomad squeezed: retailer power, private-label rise and promo-led margin erosion

Retailer concentration (top10 ≈60% sales) and private-label growth (~33% frozen share, 2024) give buyers high leverage; trade discounts 10–25% and promo pressure cut Nomad’s margins (~140bps decline since 2021). Online grocery ~15% (2024) raises price visibility; EU real disposable income −1.5% (2025) pushes value SKUs. Nomad must trade margin for shelf/promo share.

| Metric | Value |

|---|---|

| Top-10 retailer share | ~60% |

| Private-label frozen | ~33% (2024) |

| Online grocery | ~15% (2024) |

| EU real income | −1.5% (2025) |

| Margin impact | −140bps (since 2021) |

Same Document Delivered

Nomad Foods Porter's Five Forces Analysis

This preview shows the exact Nomad Foods Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the full, professionally formatted document is ready for instant download and use the moment you buy.