Norcros Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Norcros faces moderate rivalry driven by established brands and fragmented channels, while supplier power is tempered by diversified sourcing and scale advantages; buyer power and substitutes pose selective pressure in value-sensitive segments, and barriers to entry—scale, distribution, and regulatory standards—limit new competitors. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Norcros’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

The manufacturing of tiles and adhesives depends on clay, specialty chemicals and energy, and global price swings hit margins; Norcros reported raw material and energy costs up 6% in FY 2024, pressuring gross margin to 28.7% in H2 2024. Energy spikes force tighter supplier terms and hedging for the energy‑intensive tile lines, so Norcros negotiates long‑term contracts and pass‑through clauses. By end‑2025 commodity volatility eased—UK CPI commodities index fell 9% year‑on‑year—yet suppliers of specialized chemicals retain strong leverage due to limited alternatives and longer lead times.

Specialized component dependency

For Triton and Vado, Norcros depends on specialized electronic modules and C3850-grade brassware from roughly 4–6 vetted suppliers, concentrating supply and raising supplier power.

Switching risks voiding UKCA/CE safety certifications and could cut product performance, so supplier leverage is high and switching costs exceed 5–8% of unit cost per SKU.

Since 2023 Norcros has formalised multi-year contracts covering ~60% of critical parts to secure lead times and capex predictability.

Logistics and shipping constraints

A large share of Norcros’s supply chain uses international shipping to serve the UK and South Africa, giving freight providers leverage; global container rates rose ~28% in 2021–22 and spot rates remained volatile into 2024, letting carriers add fuel surcharges that lifted landed costs by 5–12% for many manufacturers.

Suppliers set rates based on lane capacity and fuel: in 2023 bunker fuel averaged $620/ton, so logistics firms could flex margins rapidly, increasing supplier bargaining power.

Norcros reduced exposure by expanding local South African manufacturing—cutting imported volume by an estimated 15–25% in 2023—lowering transit lead times and sensitivity to ocean freight swings.

Supplier consolidation in the chemical industry

The global chemical industry saw 12 large mergers from 2018–2024, cutting mid-tier suppliers for tile adhesives and surface treatments by ~22%, boosting pricing power for top suppliers who now control ~65% of specialty binders supply.

Norcros must use its £215m 2024 UK revenue scale to secure priority allocations and negotiate fixed-price or volume-discount contracts to limit margin pressure.

- Supplier concentration up ~22% (2018–2024)

- Top suppliers control ~65% specialty binder market

- Norcros UK revenue £215m (2024) — bargaining leverage

- Action: pursue volume discounts, multi-year fixed pricing

Environmental and ESG compliance costs

Suppliers are passing environmental compliance and carbon-neutrality costs to buyers; industry data shows supplier ESG premium averages 5–8% in building-products as of 2024.

As Norcros targets higher sustainability by 2025, it must pay premiums for verified green inputs, raising COGS and squeezing margins unless it offsets via price or efficiency.

Fewer compliant vendors remain—about 30% of EU suppliers met ISO 14001/2023 ESG benchmarks in 2024—so compliant suppliers' bargaining power rises.

- Supplier ESG premium: 5–8% (2024)

- Norcros sustainability target: 2025

- Compliant supplier pool: ~30% EU (2024)

- Effect: higher COGS, stronger supplier leverage

High supplier power lifts costs; Norcros hedges via multi‑year contracts and UK scale

Supplier power is high: specialty chemicals and certified components are concentrated (top suppliers ≈65% share), raw materials/energy raised COGS (raw/energy +6% FY2024; gross margin H2 2024 28.7%), logistics volatility lifted landed costs 5–12%, and ESG premiums add 5–8%; Norcros uses multi‑year contracts for ~60% critical parts and £215m UK revenue to negotiate terms.

| Metric | Value (2024) |

|---|---|

| Top supplier share | ≈65% |

| Raw/energy cost change | +6% |

| Gross margin H2 | 28.7% |

| Logistics landed cost impact | 5–12% |

| ESG premium | 5–8% |

| Multi‑yr coverage | ~60% |

| UK revenue | £215m |

What is included in the product

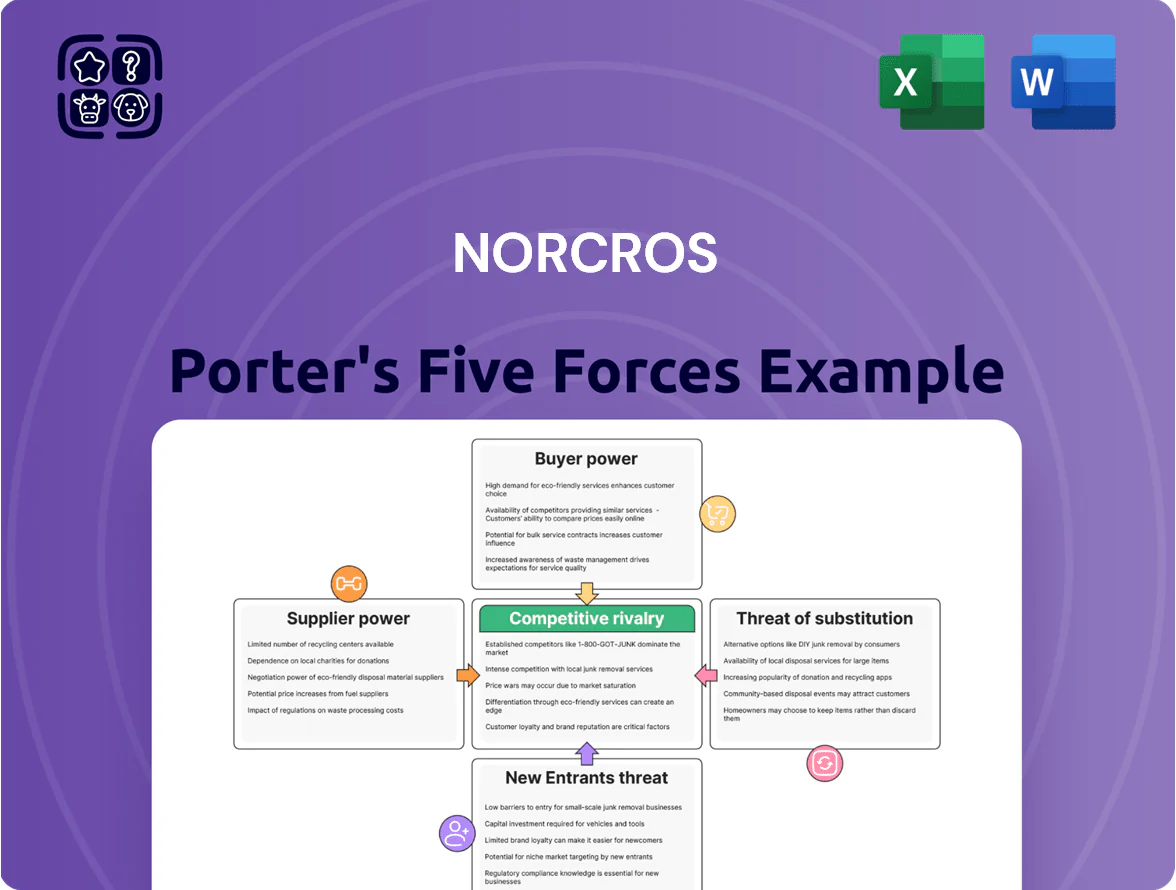

Uncovers Norcros’s competitive pressures by evaluating rival intensity, buyer and supplier power, threat of substitutes, and entry barriers to reveal strategic risks, pricing leverage, and opportunities to defend or grow market share.

Clear, one-sheet Porter’s Five Forces summary for Norcros—rapidly reveals competitive pressures and strategic levers for board-level decisions.

Customers Bargaining Power

Retailer concentration in the UK market

Trade customer loyalty and influence

Professional installers—plumbers and tilers—are key influencers who value ease of installation and reliability; Norcros reports 62% of trade sales in FY2024 tied to installer-preferred ranges.

Individually installers hold low bargaining power, but collectively their preference for brands like Triton or Johnson Tiles can shift market share; Triton held ~18% UK shower market in 2024.

Norcros spends ~£6m annually on trade loyalty programs and training (2024) to keep recommendations favoring its products over rivals.

Consumer price sensitivity in a high-interest environment

By end-2025, UK household spending on major renovations fell 6% year-on-year as mortgage rates averaged ~5.1%, keeping price-sensitive buyers cautious.

Retail customers hold high bargaining power: 78% research fixtures online and price-compare, enabling easy switching across bathroom and kitchen brands.

Norcros counters with product differentiation—water-saving tech reducing bills by up to 20% and 10-year warranties—shifting competition from price to value.

Low switching costs for accessories

Customers in bathroom accessories face almost zero switching costs, so Norcros brands like Croydex lose price power on impulse and replacement buys; UK retail data shows fenestration and fittings churn rates near 35% annually (2024 trade reports).

That forces Norcros to push design innovation and secure shelf-space—Croydex accounts for ~18% of Norcros group revenue (FY2024)—and rely on strong branding and aesthetics to deter moves to cheaper rivals.

- Near-zero switching costs; 35% churn (2024)

- Croydex ≈18% of Norcros revenue FY2024

- Focus: design, shelf-space, branding

Demand for energy and water efficiency

Modern buyers push for energy and water efficiency—electric showers and low-flow taps—to cut utility bills; 2024 UK household water use targets aim to reduce per-person use to 110 litres/day, raising demand for efficient fixtures.

Norcros shifted R&D toward sustainable solutions, reporting in FY2024 a 12% increase in sales of water-efficient products and targeting 20% of revenue from sustainable ranges by 2026.

- Buyers can reject legacy products

- Efficiency standards drive purchase decisions

- Norcros: +12% FY2024 efficient-product sales

- Target: 20% revenue from sustainable ranges by 2026

Norcros faces retailer leverage but boosts resilience with brands, Croydex and efficient ranges

Major UK retailers (B&Q, Wickes) drove ~35–45% of Norcros UK revenue in 2024, giving high buyer leverage; retail price comparison drives 78% online research and ~35% annual churn in fittings. Norcros offsets pressure with 70% branded sales, Croydex ~18% of group revenue (FY2024), £6m trade loyalty spend, and +12% FY2024 sales of water-efficient ranges targeting 20% revenue by 2026.

| Metric | 2024 / Target |

|---|---|

| Top-2 retailer share | 35–45% |

| Branded share UK sales | 70% |

| Croydex revenue share | ~18% |

| Trade loyalty spend | £6m |

| Efficient-product sales change | +12% (FY2024) |

| Efficient range revenue target | 20% by 2026 |

| Online research rate | 78% |

| Fittings churn | ~35% pa |

What You See Is What You Get

Norcros Porter's Five Forces Analysis

This preview shows the exact Norcros Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; it’s the same professionally formatted document ready for download and use the moment you buy, covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with concise insights and strategic implications.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Norcros faces moderate rivalry driven by established brands and fragmented channels, while supplier power is tempered by diversified sourcing and scale advantages; buyer power and substitutes pose selective pressure in value-sensitive segments, and barriers to entry—scale, distribution, and regulatory standards—limit new competitors. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Norcros’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

The manufacturing of tiles and adhesives depends on clay, specialty chemicals and energy, and global price swings hit margins; Norcros reported raw material and energy costs up 6% in FY 2024, pressuring gross margin to 28.7% in H2 2024. Energy spikes force tighter supplier terms and hedging for the energy‑intensive tile lines, so Norcros negotiates long‑term contracts and pass‑through clauses. By end‑2025 commodity volatility eased—UK CPI commodities index fell 9% year‑on‑year—yet suppliers of specialized chemicals retain strong leverage due to limited alternatives and longer lead times.

Specialized component dependency

For Triton and Vado, Norcros depends on specialized electronic modules and C3850-grade brassware from roughly 4–6 vetted suppliers, concentrating supply and raising supplier power.

Switching risks voiding UKCA/CE safety certifications and could cut product performance, so supplier leverage is high and switching costs exceed 5–8% of unit cost per SKU.

Since 2023 Norcros has formalised multi-year contracts covering ~60% of critical parts to secure lead times and capex predictability.

Logistics and shipping constraints

A large share of Norcros’s supply chain uses international shipping to serve the UK and South Africa, giving freight providers leverage; global container rates rose ~28% in 2021–22 and spot rates remained volatile into 2024, letting carriers add fuel surcharges that lifted landed costs by 5–12% for many manufacturers.

Suppliers set rates based on lane capacity and fuel: in 2023 bunker fuel averaged $620/ton, so logistics firms could flex margins rapidly, increasing supplier bargaining power.

Norcros reduced exposure by expanding local South African manufacturing—cutting imported volume by an estimated 15–25% in 2023—lowering transit lead times and sensitivity to ocean freight swings.

Supplier consolidation in the chemical industry

The global chemical industry saw 12 large mergers from 2018–2024, cutting mid-tier suppliers for tile adhesives and surface treatments by ~22%, boosting pricing power for top suppliers who now control ~65% of specialty binders supply.

Norcros must use its £215m 2024 UK revenue scale to secure priority allocations and negotiate fixed-price or volume-discount contracts to limit margin pressure.

- Supplier concentration up ~22% (2018–2024)

- Top suppliers control ~65% specialty binder market

- Norcros UK revenue £215m (2024) — bargaining leverage

- Action: pursue volume discounts, multi-year fixed pricing

Environmental and ESG compliance costs

Suppliers are passing environmental compliance and carbon-neutrality costs to buyers; industry data shows supplier ESG premium averages 5–8% in building-products as of 2024.

As Norcros targets higher sustainability by 2025, it must pay premiums for verified green inputs, raising COGS and squeezing margins unless it offsets via price or efficiency.

Fewer compliant vendors remain—about 30% of EU suppliers met ISO 14001/2023 ESG benchmarks in 2024—so compliant suppliers' bargaining power rises.

- Supplier ESG premium: 5–8% (2024)

- Norcros sustainability target: 2025

- Compliant supplier pool: ~30% EU (2024)

- Effect: higher COGS, stronger supplier leverage

High supplier power lifts costs; Norcros hedges via multi‑year contracts and UK scale

Supplier power is high: specialty chemicals and certified components are concentrated (top suppliers ≈65% share), raw materials/energy raised COGS (raw/energy +6% FY2024; gross margin H2 2024 28.7%), logistics volatility lifted landed costs 5–12%, and ESG premiums add 5–8%; Norcros uses multi‑year contracts for ~60% critical parts and £215m UK revenue to negotiate terms.

| Metric | Value (2024) |

|---|---|

| Top supplier share | ≈65% |

| Raw/energy cost change | +6% |

| Gross margin H2 | 28.7% |

| Logistics landed cost impact | 5–12% |

| ESG premium | 5–8% |

| Multi‑yr coverage | ~60% |

| UK revenue | £215m |

What is included in the product

Uncovers Norcros’s competitive pressures by evaluating rival intensity, buyer and supplier power, threat of substitutes, and entry barriers to reveal strategic risks, pricing leverage, and opportunities to defend or grow market share.

Clear, one-sheet Porter’s Five Forces summary for Norcros—rapidly reveals competitive pressures and strategic levers for board-level decisions.

Customers Bargaining Power

Retailer concentration in the UK market

Trade customer loyalty and influence

Professional installers—plumbers and tilers—are key influencers who value ease of installation and reliability; Norcros reports 62% of trade sales in FY2024 tied to installer-preferred ranges.

Individually installers hold low bargaining power, but collectively their preference for brands like Triton or Johnson Tiles can shift market share; Triton held ~18% UK shower market in 2024.

Norcros spends ~£6m annually on trade loyalty programs and training (2024) to keep recommendations favoring its products over rivals.

Consumer price sensitivity in a high-interest environment

By end-2025, UK household spending on major renovations fell 6% year-on-year as mortgage rates averaged ~5.1%, keeping price-sensitive buyers cautious.

Retail customers hold high bargaining power: 78% research fixtures online and price-compare, enabling easy switching across bathroom and kitchen brands.

Norcros counters with product differentiation—water-saving tech reducing bills by up to 20% and 10-year warranties—shifting competition from price to value.

Low switching costs for accessories

Customers in bathroom accessories face almost zero switching costs, so Norcros brands like Croydex lose price power on impulse and replacement buys; UK retail data shows fenestration and fittings churn rates near 35% annually (2024 trade reports).

That forces Norcros to push design innovation and secure shelf-space—Croydex accounts for ~18% of Norcros group revenue (FY2024)—and rely on strong branding and aesthetics to deter moves to cheaper rivals.

- Near-zero switching costs; 35% churn (2024)

- Croydex ≈18% of Norcros revenue FY2024

- Focus: design, shelf-space, branding

Demand for energy and water efficiency

Modern buyers push for energy and water efficiency—electric showers and low-flow taps—to cut utility bills; 2024 UK household water use targets aim to reduce per-person use to 110 litres/day, raising demand for efficient fixtures.

Norcros shifted R&D toward sustainable solutions, reporting in FY2024 a 12% increase in sales of water-efficient products and targeting 20% of revenue from sustainable ranges by 2026.

- Buyers can reject legacy products

- Efficiency standards drive purchase decisions

- Norcros: +12% FY2024 efficient-product sales

- Target: 20% revenue from sustainable ranges by 2026

Norcros faces retailer leverage but boosts resilience with brands, Croydex and efficient ranges

Major UK retailers (B&Q, Wickes) drove ~35–45% of Norcros UK revenue in 2024, giving high buyer leverage; retail price comparison drives 78% online research and ~35% annual churn in fittings. Norcros offsets pressure with 70% branded sales, Croydex ~18% of group revenue (FY2024), £6m trade loyalty spend, and +12% FY2024 sales of water-efficient ranges targeting 20% revenue by 2026.

| Metric | 2024 / Target |

|---|---|

| Top-2 retailer share | 35–45% |

| Branded share UK sales | 70% |

| Croydex revenue share | ~18% |

| Trade loyalty spend | £6m |

| Efficient-product sales change | +12% (FY2024) |

| Efficient range revenue target | 20% by 2026 |

| Online research rate | 78% |

| Fittings churn | ~35% pa |

What You See Is What You Get

Norcros Porter's Five Forces Analysis

This preview shows the exact Norcros Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; it’s the same professionally formatted document ready for download and use the moment you buy, covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with concise insights and strategic implications.