Nordex Porter's Five Forces Analysis

From Overview to Strategy Blueprint

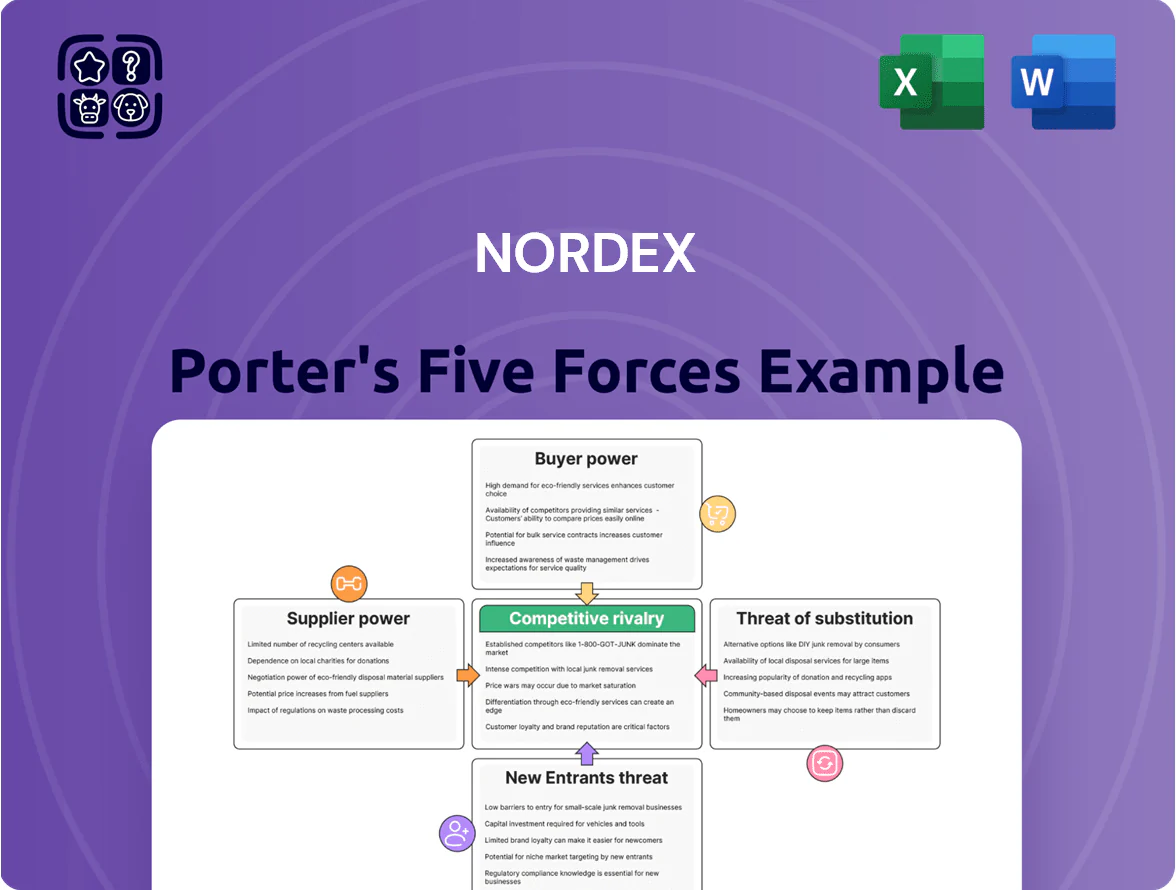

Nordex operates in a capital-intensive wind-turbine market where supplier concentration, technological differentiation, and regulatory shifts shape competitive intensity; while strong OEM relationships and scale help mitigate supplier and buyer pressures, rising new entrants and substitute technologies pose growing threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nordex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized component providers

The global supply of key wind-turbine components—gearboxes, main bearings, and LIDAR/sensor systems—is concentrated: the top 5 suppliers control roughly 70% of gearbox market capacity (2024 IEA/industry reports), giving them pricing and delivery leverage over Nordex during demand spikes linked to record 2023–25 offshore and onshore orders.

Volatility in raw material pricing

Nordex is highly exposed to steel, copper and carbon-fiber price swings—these inputs rose 12–18% in 2021–2022 and remained volatile through 2024, squeezing margins when suppliers pass costs along. Because these commodities trade on global markets, Nordex faces limited supplier price control and periodic input-driven margin compression; in 2024 COGS rose ~6% year-over-year for the sector. Nordex uses multi-year supply contracts and commodity hedges to limit volatility and protect EBITDA.

High switching costs for technical components

Switching specialized turbine suppliers demands extensive technical validation, re-engineering, and certification—processes that can take 12–24 months and cost tens of millions EUR per platform, according to industry benchmarks from 2024–2025. These high switching costs lock Nordex to key vendors across a turbine lifecycle (15–25 years), strengthening supplier bargaining power and limiting price leverage. Any supplier change risks production delays (reported up to 6–9 months in 2023 supply disruptions) and raises R&D and qualification spend, squeezing margins.

Logistical constraints and geographic dependencies

Nordex depends on supplier hubs for blades and towers—dominant clusters in Spain, Turkey, China and Brazil—so regional disruptions (eg, Turkey sanctions 2024; China lockdowns 2022) can halt supply and inflate costs; Nordex reported supply-chain related capex pressure in 2024, pushing working capital up ~15% vs 2023.

- Concentrated suppliers raise disruption risk

- Switching lead times often >12 weeks

- Working capital +15% YoY (2024) from logistics

- Limited on-short-notice alternatives

Forward integration threats from component makers

Some large component makers, like Siemens Gamesa suppliers and gearbox specialists, have the engineering capacity to forward integrate into assembly or servicing; this threat is moderate today but rising as modular designs lower entry barriers.

In 2025, turbine component firms represent about 20–25% of supply-chain value in onshore projects, so suppliers capturing assembly could shift margins away from OEMs like Nordex.

Nordex must keep innovating in system integration, R&D (Nordex spent ~EUR 188m on R&D in 2024), and service differentiation to stay the primary integrator.

- Moderate threat: expertise exists

- Modular designs: reduces integration costs

- 2024 R&D: EUR 188m (Nordex)

- Supply-chain value: ~20–25% to components (2025)

Gearbox oligopoly strengthens margins as costs rise; switching costly—Nordex boosts R&D

Suppliers are moderately strong: top‑5 gearbox makers hold ~70% capacity (2024), commodity-driven COGS rose ~6% YoY (2024), switching vendors takes 12–24 months and costs tens of M EUR, and Nordex R&D was EUR 188m (2024) to protect integration margin.

| Metric | Value |

|---|---|

| Top‑5 gearbox share | ~70% (2024) |

| Sector COGS change | +6% YoY (2024) |

| Switching time/cost | 12–24 months; tens M EUR |

| Nordex R&D | EUR 188m (2024) |

What is included in the product

Tailored Porter's Five Forces assessment for Nordex, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its wind-turbine market position.

A focused Porter's Five Forces snapshot for Nordex—clarifying competitive pressures and supplier/buyer dynamics to speed strategic decisions and investor assessments.

Customers Bargaining Power

Consolidation of large scale utility developers

Nordex faces concentrated buying power as utilities and global developers now account for a growing share of large turbine orders; for example, 2024 saw top 10 utility customers place ~40% of EU wind capacity tenders, pressuring OEM margins.

These sophisticated buyers demand lower prices and multi-year service contracts, negotiating discounts up to 10–15% on large lots and shifting risk to suppliers.

Their ability to select among Siemens Gamesa, Vestas, GE Renewable Energy and Nordex forces Nordex to compete on price, OPEX and delivery, compressing EBITDA margins—Nordex posted 3.8% adjusted EBITDA in FY2024, highlighting the squeeze.

Shift toward competitive auction models

Governments shifted from feed-in tariffs to competitive auctions, with over 70% of global renewable capacity awarded via auctions in 2024, forcing developers to cut capex and push savings onto manufacturers like Nordex.

Auctions compress margins—median winning bid declines of 18% from 2019–2023—so customers demand turbines optimized for cost per MWh, not just nameplate capacity.

Nordex faces buyer power as developers require lower LCOE, faster commissioning, and warranties tied to availability, pushing product cost and performance trade-offs onto suppliers.

High importance of Levelized Cost of Energy

Customers rank Levelized Cost of Energy (LCOE) as the decisive metric when choosing a turbine supplier; recent 2024 IEA and BNEF data show onshore wind LCOE ranges €20–€40/MWh, so a €5/MWh gap shifts deals. If Nordex cannot prove a competitive LCOE versus Vestas, Siemens Gamesa and Goldwind, buyers switch quickly to lower-cost bids. This strict, data-driven procurement—often tied to PPA pricing—keeps bargaining power with customers.

Low switching costs at the tender stage

During tendering, buyers face low switching costs, letting them pit turbine makers against each other to cut prices and demand advanced specs; in 2024 OEM bid competitiveness drove average contract price pressure of ~5–8% in EU onshore tenders.

Nordex therefore must win on service quality and proven turbine uptime—its 2024 fleet availability ~97.5% is a key selling point to lock orders early.

- Low switching cost enables price/tech leverage

- 2024 price pressure ~5–8% in EU onshore tenders

- Nordex fleet availability ~97.5% in 2024 as differentiator

Demand for comprehensive long term service packages

Modern buyers press for integrated offers that pair turbines with 20–30 year service contracts; institutional buyers now demand availability guarantees often >97%, shifting lifetime margin to service fees—Nordex reported service revenue growth of 18% in 2024, showing this leverage.

To win bids, Nordex accepts strict KPIs (availability, AEP) and penalties; a 1% availability shortfall can cut lifetime cash flow by mid-single digits, so customers extract pricing and warranty concessions.

- 20–30 year service terms common

- Customers seek >97% availability

- Nordex service revenue +18% in 2024

- 1% availability shortfall trims lifetime cash flow mid-single digits

Buyers squeezing margins: top-10 drive 40% tenders, Nordex EBITDA 3.8%, service growth

Customers (utilities, developers) hold strong bargaining power—top 10 buyers drove ~40% EU tenders in 2024, forcing 10–15% discounts on large orders and 5–8% price pressure in EU onshore tenders; Nordex’s 3.8% adjusted EBITDA (FY2024) and €?5/MWh LCOE gaps matter. Service revenue +18% (2024) and ~97.5% fleet availability help, but 20–30y contracts with >97% uptime shift risk and margin to suppliers.

| Metric | 2024 value |

|---|---|

| Top10 share EU tenders | ~40% |

| Price discounts on large lots | 10–15% |

| EU onshore tender price pressure | 5–8% |

| Nordex adj. EBITDA | 3.8% |

| Service revenue growth | +18% |

| Fleet availability | ~97.5% |

What You See Is What You Get

Nordex Porter's Five Forces Analysis

This preview shows the exact Nordex Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed here is the full, professionally formatted file you can download and use the moment you buy, covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Nordex operates in a capital-intensive wind-turbine market where supplier concentration, technological differentiation, and regulatory shifts shape competitive intensity; while strong OEM relationships and scale help mitigate supplier and buyer pressures, rising new entrants and substitute technologies pose growing threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nordex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized component providers

The global supply of key wind-turbine components—gearboxes, main bearings, and LIDAR/sensor systems—is concentrated: the top 5 suppliers control roughly 70% of gearbox market capacity (2024 IEA/industry reports), giving them pricing and delivery leverage over Nordex during demand spikes linked to record 2023–25 offshore and onshore orders.

Volatility in raw material pricing

Nordex is highly exposed to steel, copper and carbon-fiber price swings—these inputs rose 12–18% in 2021–2022 and remained volatile through 2024, squeezing margins when suppliers pass costs along. Because these commodities trade on global markets, Nordex faces limited supplier price control and periodic input-driven margin compression; in 2024 COGS rose ~6% year-over-year for the sector. Nordex uses multi-year supply contracts and commodity hedges to limit volatility and protect EBITDA.

High switching costs for technical components

Switching specialized turbine suppliers demands extensive technical validation, re-engineering, and certification—processes that can take 12–24 months and cost tens of millions EUR per platform, according to industry benchmarks from 2024–2025. These high switching costs lock Nordex to key vendors across a turbine lifecycle (15–25 years), strengthening supplier bargaining power and limiting price leverage. Any supplier change risks production delays (reported up to 6–9 months in 2023 supply disruptions) and raises R&D and qualification spend, squeezing margins.

Logistical constraints and geographic dependencies

Nordex depends on supplier hubs for blades and towers—dominant clusters in Spain, Turkey, China and Brazil—so regional disruptions (eg, Turkey sanctions 2024; China lockdowns 2022) can halt supply and inflate costs; Nordex reported supply-chain related capex pressure in 2024, pushing working capital up ~15% vs 2023.

- Concentrated suppliers raise disruption risk

- Switching lead times often >12 weeks

- Working capital +15% YoY (2024) from logistics

- Limited on-short-notice alternatives

Forward integration threats from component makers

Some large component makers, like Siemens Gamesa suppliers and gearbox specialists, have the engineering capacity to forward integrate into assembly or servicing; this threat is moderate today but rising as modular designs lower entry barriers.

In 2025, turbine component firms represent about 20–25% of supply-chain value in onshore projects, so suppliers capturing assembly could shift margins away from OEMs like Nordex.

Nordex must keep innovating in system integration, R&D (Nordex spent ~EUR 188m on R&D in 2024), and service differentiation to stay the primary integrator.

- Moderate threat: expertise exists

- Modular designs: reduces integration costs

- 2024 R&D: EUR 188m (Nordex)

- Supply-chain value: ~20–25% to components (2025)

Gearbox oligopoly strengthens margins as costs rise; switching costly—Nordex boosts R&D

Suppliers are moderately strong: top‑5 gearbox makers hold ~70% capacity (2024), commodity-driven COGS rose ~6% YoY (2024), switching vendors takes 12–24 months and costs tens of M EUR, and Nordex R&D was EUR 188m (2024) to protect integration margin.

| Metric | Value |

|---|---|

| Top‑5 gearbox share | ~70% (2024) |

| Sector COGS change | +6% YoY (2024) |

| Switching time/cost | 12–24 months; tens M EUR |

| Nordex R&D | EUR 188m (2024) |

What is included in the product

Tailored Porter's Five Forces assessment for Nordex, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its wind-turbine market position.

A focused Porter's Five Forces snapshot for Nordex—clarifying competitive pressures and supplier/buyer dynamics to speed strategic decisions and investor assessments.

Customers Bargaining Power

Consolidation of large scale utility developers

Nordex faces concentrated buying power as utilities and global developers now account for a growing share of large turbine orders; for example, 2024 saw top 10 utility customers place ~40% of EU wind capacity tenders, pressuring OEM margins.

These sophisticated buyers demand lower prices and multi-year service contracts, negotiating discounts up to 10–15% on large lots and shifting risk to suppliers.

Their ability to select among Siemens Gamesa, Vestas, GE Renewable Energy and Nordex forces Nordex to compete on price, OPEX and delivery, compressing EBITDA margins—Nordex posted 3.8% adjusted EBITDA in FY2024, highlighting the squeeze.

Shift toward competitive auction models

Governments shifted from feed-in tariffs to competitive auctions, with over 70% of global renewable capacity awarded via auctions in 2024, forcing developers to cut capex and push savings onto manufacturers like Nordex.

Auctions compress margins—median winning bid declines of 18% from 2019–2023—so customers demand turbines optimized for cost per MWh, not just nameplate capacity.

Nordex faces buyer power as developers require lower LCOE, faster commissioning, and warranties tied to availability, pushing product cost and performance trade-offs onto suppliers.

High importance of Levelized Cost of Energy

Customers rank Levelized Cost of Energy (LCOE) as the decisive metric when choosing a turbine supplier; recent 2024 IEA and BNEF data show onshore wind LCOE ranges €20–€40/MWh, so a €5/MWh gap shifts deals. If Nordex cannot prove a competitive LCOE versus Vestas, Siemens Gamesa and Goldwind, buyers switch quickly to lower-cost bids. This strict, data-driven procurement—often tied to PPA pricing—keeps bargaining power with customers.

Low switching costs at the tender stage

During tendering, buyers face low switching costs, letting them pit turbine makers against each other to cut prices and demand advanced specs; in 2024 OEM bid competitiveness drove average contract price pressure of ~5–8% in EU onshore tenders.

Nordex therefore must win on service quality and proven turbine uptime—its 2024 fleet availability ~97.5% is a key selling point to lock orders early.

- Low switching cost enables price/tech leverage

- 2024 price pressure ~5–8% in EU onshore tenders

- Nordex fleet availability ~97.5% in 2024 as differentiator

Demand for comprehensive long term service packages

Modern buyers press for integrated offers that pair turbines with 20–30 year service contracts; institutional buyers now demand availability guarantees often >97%, shifting lifetime margin to service fees—Nordex reported service revenue growth of 18% in 2024, showing this leverage.

To win bids, Nordex accepts strict KPIs (availability, AEP) and penalties; a 1% availability shortfall can cut lifetime cash flow by mid-single digits, so customers extract pricing and warranty concessions.

- 20–30 year service terms common

- Customers seek >97% availability

- Nordex service revenue +18% in 2024

- 1% availability shortfall trims lifetime cash flow mid-single digits

Buyers squeezing margins: top-10 drive 40% tenders, Nordex EBITDA 3.8%, service growth

Customers (utilities, developers) hold strong bargaining power—top 10 buyers drove ~40% EU tenders in 2024, forcing 10–15% discounts on large orders and 5–8% price pressure in EU onshore tenders; Nordex’s 3.8% adjusted EBITDA (FY2024) and €?5/MWh LCOE gaps matter. Service revenue +18% (2024) and ~97.5% fleet availability help, but 20–30y contracts with >97% uptime shift risk and margin to suppliers.

| Metric | 2024 value |

|---|---|

| Top10 share EU tenders | ~40% |

| Price discounts on large lots | 10–15% |

| EU onshore tender price pressure | 5–8% |

| Nordex adj. EBITDA | 3.8% |

| Service revenue growth | +18% |

| Fleet availability | ~97.5% |

What You See Is What You Get

Nordex Porter's Five Forces Analysis

This preview shows the exact Nordex Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed here is the full, professionally formatted file you can download and use the moment you buy, covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry.