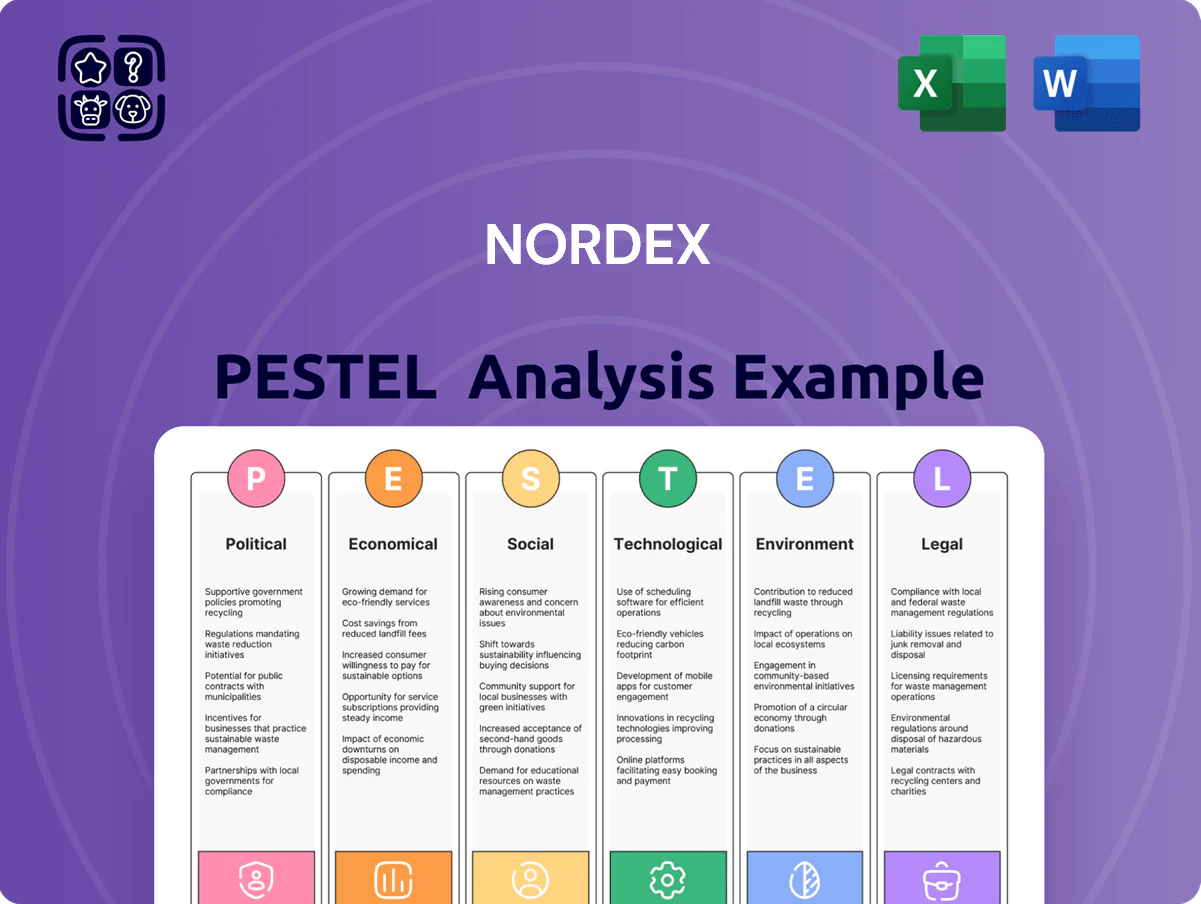

Nordex PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological advances are reshaping Nordex's trajectory with our concise PESTLE snapshot—designed for investors, strategists, and advisors who need actionable external insights fast; purchase the full PESTLE to access detailed risks, opportunities, and ready-to-use recommendations for immediate strategic impact.

Political factors

EU REPowerEU and Green Deal Industrial Plan

As of late 2025 Nordex benefits from the EU REPowerEU and Green Deal Industrial Plan: increased renewables targets raised EU 2030 wind capacity goals to ~510 GW, boosting demand for turbines and supporting Nordex order intake up 18% year-on-year in 2024–25.

Renewable Energy Directive III accelerated permitting cut average onshore project lead times from ~36 to ~18 months across member states, shortening time-to-revenue for Nordex projects in Germany and Spain.

Political tailwinds underpin a more stable European order book, with Nordex reporting a firm backlog of EUR 4.1bn by H2 2025 and sustained strong market share in core markets.

Geopolitical focus on energy sovereignty

The ongoing emphasis on energy security across a fragmented geopolitical landscape has elevated wind power to a strategic national asset; EMEA governments aim to raise domestic renewable share—EU target 42.5% renewables by 2030—to reduce reliance on imports. Governments in Poland, Spain and Turkey increased wind auction volumes by ~18% YoY in 2024, boosting local procurement. Nordex leverages this shift to secure multi-year contracts with state-backed utilities and private developers, contributing to its 2024 order backlog of €6.2bn.

Impact of US Inflation Reduction Act incentives

The Inflation Reduction Act’s incentives boost Nordex’s North American expansion, supporting projected wind installations of 28 GW in the US by 2025 and reinforcing demand for Delta4000 turbines, with tax credits (up to 30% ITC) improving project IRRs.

Production and investment credits have stabilized orders—US wind capacity additions rose 42% in 2024—yet evolving domestic content rules (tax credit tiers tied to US-made components) force Nordex to adapt sourcing and may raise near-term manufacturing costs.

Trade policies and protectionist measures

Political scrutiny over non-European wind technology has risen, prompting debates on trade barriers and fair competition after EU anti-subsidy probes; in 2024 the European Commission reported a 22% increase in safeguard investigations in clean tech sectors.

EU measures to shield local OEMs from subsidized competitors—including tariffs and stricter procurement rules—fortify Nordex’s market position in Europe, where it held ~12% wind turbine market share in 2024.

Procurement shifts prioritize qualitative criteria over lowest bid: public tenders now weight lifecycle cost and localization, with some member states increasing quality scoring by up to 30% in 2025.

- Rise in EU safeguard probes: +22% (2024)

- Nordex EU market share ~12% (2024)

- Quality weighting in tenders increased up to 30% (2025)

National grid expansion mandates

Government mandates to modernize aging grids are vital for integrating Nordex’s onshore wind; EU and US federal programs allocated about €160 billion (2024–2025) to grid upgrades, directly reducing curtailment risk for developers.

Political pressure has shifted toward streamlining interconnection queues—US FERC reforms in 2024 aimed to cut average wait times from 5–10 years toward under 2 years, easing project ramp-up.

These interventions ensure completed Nordex projects can deliver power promptly, lowering revenue disruption and improving asset utilization.

- €160bn public grid funding (EU/US, 2024–25)

- FERC 2024 reforms target <2-year interconnection

- Reduces curtailment and revenue downtime for Nordex

EU/US policy lifts wind build—510GW by 2030, Nordex backlog €4.1bn, US 28GW by 2025

Strong EU/US policy support raised wind targets (EU ~510 GW by 2030), boosted Nordex 2024–25 order intake +18% YoY and backlog €4.1bn (H2 2025); US IRA spurred 28 GW US installations by 2025 but domestic content rules increase sourcing costs; EU safeguard probes +22% (2024) protect local OEMs; €160bn allocated to grid upgrades (2024–25) and FERC reforms target <2-year interconnection.

| Metric | Value |

|---|---|

| EU 2030 wind target | ~510 GW |

| Nordex backlog | €4.1bn (H2 2025) |

| Order intake growth | +18% YoY (2024–25) |

| US installations | 28 GW (2025) |

| Grid funding | €160bn (2024–25) |

What is included in the product

Explores how macro-environmental factors uniquely affect Nordex across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific insights to identify threats and opportunities for executives, investors, and strategists.

A concise Nordex PESTLE summary that’s visually segmented for quick meeting use, easily dropped into slides, shared across teams, and annotated per region or business line to support risk discussions and client reports.

Economic factors

Interest rate stabilization and financing costs

By end-2025 global policy rates had largely stabilized—ECB at 3.25%, US Fed at 5.25%—reducing financing volatility and cutting average project debt spreads for renewables by about 120 basis points versus 2022, improving developer IRRs by ~2–3 percentage points and boosting demand for Nordex turbines.

Raw material price volatility and inflation

Raw material costs like steel, copper and resins remain key for Nordex margins: steel prices averaged about $900/ton in 2025 vs $1,100/ton peak in 2022, while copper stood near $8,200/ton in 2025, pressuring input costs.

Hyperinflation has subsided, but Nordex uses hedging—commodity forwards and options—and reported a 2024 hedging cover reducing COGS volatility by ~12%.

Efficient supply-chain measures and indexed pricing in sales contracts are critical to preserve EBITDA amid commodity swings and 2024 global resin price volatility of ±18%.

Competitive pricing pressure from global OEMs

Nordex faces intense price competition from Chinese OEMs—China's turbine exports grew ~22% in 2024—pressuring margins as lower-cost alternatives enter Europe and Latin America.

To respond, Nordex emphasizes lowering Levelized Cost of Energy via higher-efficiency turbines and service-led offerings; FY2024 R&D spend rose to ~€150m to boost turbine efficiency.

Demonstrating superior lifecycle value and reducing operational risk through local service centers and longer warranties is crucial for Nordex to protect market share versus low-cost entrants.

Electricity market design and PPA trends

The rise of Corporate PPAs now accounts for about 40% of European corporate contracted renewable capacity in 2024, diversifying revenue for wind developers and benefiting Nordex through steady turbine orders and service agreements.

Corporates locking long-term green prices sustain demand for reliable onshore turbines—supporting Nordex even as national feed-in tariffs and auction outcomes fluctuate.

The market-driven PPA pipeline (≈60 GW Europe, 2024–2026) offers a buffer vs. policy shifts, underpinning project financing and aftermarket services.

- Corporate PPAs ≈40% of EU contracted capacity (2024)

- European PPA pipeline ≈60 GW (2024–2026)

- Market demand reduces exposure to feed-in tariff volatility

Logistics and global supply chain efficiency

By balancing local production with global sourcing, Nordex kept logistical overheads stable near 6–7% of COGS in 2024 despite surge in demand for wind installations.

- Ocean transit times down ~12% (2024)

- Transport cost reduction ~8% YoY

- Logistics ~6–7% of COGS (2024)

Lower rates, cheaper debt lift developer IRRs 2–3ppt; 60GW EU PPA pipeline fuels turbine demand

Lowered policy rates (ECB 3.25%, Fed 5.25% end-2025) cut project debt spreads ~120 bps vs 2022, improving developer IRRs ~2–3 ppt and boosting turbine demand; steel ~$900/t, copper ~$8,200/t (2025) press input costs; 2024 hedging reduced COGS volatility ~12%; European PPA pipeline ≈60 GW (2024–26) and corporate PPAs ≈40% of contracted capacity support orders.

| Metric | Value |

|---|---|

| ECB policy rate (end-2025) | 3.25% |

| Fed policy rate (end-2025) | 5.25% |

| Steel price (avg 2025) | $900/t |

| Copper price (2025) | $8,200/t |

| Hedging COGS volatility reduction (2024) | ~12% |

| EU PPA pipeline (2024–26) | ≈60 GW |

| Corporate PPAs share (2024) | ≈40% |

Same Document Delivered

Nordex PESTLE Analysis

The preview shown here is the exact Nordex PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological advances are reshaping Nordex's trajectory with our concise PESTLE snapshot—designed for investors, strategists, and advisors who need actionable external insights fast; purchase the full PESTLE to access detailed risks, opportunities, and ready-to-use recommendations for immediate strategic impact.

Political factors

EU REPowerEU and Green Deal Industrial Plan

As of late 2025 Nordex benefits from the EU REPowerEU and Green Deal Industrial Plan: increased renewables targets raised EU 2030 wind capacity goals to ~510 GW, boosting demand for turbines and supporting Nordex order intake up 18% year-on-year in 2024–25.

Renewable Energy Directive III accelerated permitting cut average onshore project lead times from ~36 to ~18 months across member states, shortening time-to-revenue for Nordex projects in Germany and Spain.

Political tailwinds underpin a more stable European order book, with Nordex reporting a firm backlog of EUR 4.1bn by H2 2025 and sustained strong market share in core markets.

Geopolitical focus on energy sovereignty

The ongoing emphasis on energy security across a fragmented geopolitical landscape has elevated wind power to a strategic national asset; EMEA governments aim to raise domestic renewable share—EU target 42.5% renewables by 2030—to reduce reliance on imports. Governments in Poland, Spain and Turkey increased wind auction volumes by ~18% YoY in 2024, boosting local procurement. Nordex leverages this shift to secure multi-year contracts with state-backed utilities and private developers, contributing to its 2024 order backlog of €6.2bn.

Impact of US Inflation Reduction Act incentives

The Inflation Reduction Act’s incentives boost Nordex’s North American expansion, supporting projected wind installations of 28 GW in the US by 2025 and reinforcing demand for Delta4000 turbines, with tax credits (up to 30% ITC) improving project IRRs.

Production and investment credits have stabilized orders—US wind capacity additions rose 42% in 2024—yet evolving domestic content rules (tax credit tiers tied to US-made components) force Nordex to adapt sourcing and may raise near-term manufacturing costs.

Trade policies and protectionist measures

Political scrutiny over non-European wind technology has risen, prompting debates on trade barriers and fair competition after EU anti-subsidy probes; in 2024 the European Commission reported a 22% increase in safeguard investigations in clean tech sectors.

EU measures to shield local OEMs from subsidized competitors—including tariffs and stricter procurement rules—fortify Nordex’s market position in Europe, where it held ~12% wind turbine market share in 2024.

Procurement shifts prioritize qualitative criteria over lowest bid: public tenders now weight lifecycle cost and localization, with some member states increasing quality scoring by up to 30% in 2025.

- Rise in EU safeguard probes: +22% (2024)

- Nordex EU market share ~12% (2024)

- Quality weighting in tenders increased up to 30% (2025)

National grid expansion mandates

Government mandates to modernize aging grids are vital for integrating Nordex’s onshore wind; EU and US federal programs allocated about €160 billion (2024–2025) to grid upgrades, directly reducing curtailment risk for developers.

Political pressure has shifted toward streamlining interconnection queues—US FERC reforms in 2024 aimed to cut average wait times from 5–10 years toward under 2 years, easing project ramp-up.

These interventions ensure completed Nordex projects can deliver power promptly, lowering revenue disruption and improving asset utilization.

- €160bn public grid funding (EU/US, 2024–25)

- FERC 2024 reforms target <2-year interconnection

- Reduces curtailment and revenue downtime for Nordex

EU/US policy lifts wind build—510GW by 2030, Nordex backlog €4.1bn, US 28GW by 2025

Strong EU/US policy support raised wind targets (EU ~510 GW by 2030), boosted Nordex 2024–25 order intake +18% YoY and backlog €4.1bn (H2 2025); US IRA spurred 28 GW US installations by 2025 but domestic content rules increase sourcing costs; EU safeguard probes +22% (2024) protect local OEMs; €160bn allocated to grid upgrades (2024–25) and FERC reforms target <2-year interconnection.

| Metric | Value |

|---|---|

| EU 2030 wind target | ~510 GW |

| Nordex backlog | €4.1bn (H2 2025) |

| Order intake growth | +18% YoY (2024–25) |

| US installations | 28 GW (2025) |

| Grid funding | €160bn (2024–25) |

What is included in the product

Explores how macro-environmental factors uniquely affect Nordex across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific insights to identify threats and opportunities for executives, investors, and strategists.

A concise Nordex PESTLE summary that’s visually segmented for quick meeting use, easily dropped into slides, shared across teams, and annotated per region or business line to support risk discussions and client reports.

Economic factors

Interest rate stabilization and financing costs

By end-2025 global policy rates had largely stabilized—ECB at 3.25%, US Fed at 5.25%—reducing financing volatility and cutting average project debt spreads for renewables by about 120 basis points versus 2022, improving developer IRRs by ~2–3 percentage points and boosting demand for Nordex turbines.

Raw material price volatility and inflation

Raw material costs like steel, copper and resins remain key for Nordex margins: steel prices averaged about $900/ton in 2025 vs $1,100/ton peak in 2022, while copper stood near $8,200/ton in 2025, pressuring input costs.

Hyperinflation has subsided, but Nordex uses hedging—commodity forwards and options—and reported a 2024 hedging cover reducing COGS volatility by ~12%.

Efficient supply-chain measures and indexed pricing in sales contracts are critical to preserve EBITDA amid commodity swings and 2024 global resin price volatility of ±18%.

Competitive pricing pressure from global OEMs

Nordex faces intense price competition from Chinese OEMs—China's turbine exports grew ~22% in 2024—pressuring margins as lower-cost alternatives enter Europe and Latin America.

To respond, Nordex emphasizes lowering Levelized Cost of Energy via higher-efficiency turbines and service-led offerings; FY2024 R&D spend rose to ~€150m to boost turbine efficiency.

Demonstrating superior lifecycle value and reducing operational risk through local service centers and longer warranties is crucial for Nordex to protect market share versus low-cost entrants.

Electricity market design and PPA trends

The rise of Corporate PPAs now accounts for about 40% of European corporate contracted renewable capacity in 2024, diversifying revenue for wind developers and benefiting Nordex through steady turbine orders and service agreements.

Corporates locking long-term green prices sustain demand for reliable onshore turbines—supporting Nordex even as national feed-in tariffs and auction outcomes fluctuate.

The market-driven PPA pipeline (≈60 GW Europe, 2024–2026) offers a buffer vs. policy shifts, underpinning project financing and aftermarket services.

- Corporate PPAs ≈40% of EU contracted capacity (2024)

- European PPA pipeline ≈60 GW (2024–2026)

- Market demand reduces exposure to feed-in tariff volatility

Logistics and global supply chain efficiency

By balancing local production with global sourcing, Nordex kept logistical overheads stable near 6–7% of COGS in 2024 despite surge in demand for wind installations.

- Ocean transit times down ~12% (2024)

- Transport cost reduction ~8% YoY

- Logistics ~6–7% of COGS (2024)

Lower rates, cheaper debt lift developer IRRs 2–3ppt; 60GW EU PPA pipeline fuels turbine demand

Lowered policy rates (ECB 3.25%, Fed 5.25% end-2025) cut project debt spreads ~120 bps vs 2022, improving developer IRRs ~2–3 ppt and boosting turbine demand; steel ~$900/t, copper ~$8,200/t (2025) press input costs; 2024 hedging reduced COGS volatility ~12%; European PPA pipeline ≈60 GW (2024–26) and corporate PPAs ≈40% of contracted capacity support orders.

| Metric | Value |

|---|---|

| ECB policy rate (end-2025) | 3.25% |

| Fed policy rate (end-2025) | 5.25% |

| Steel price (avg 2025) | $900/t |

| Copper price (2025) | $8,200/t |

| Hedging COGS volatility reduction (2024) | ~12% |

| EU PPA pipeline (2024–26) | ≈60 GW |

| Corporate PPAs share (2024) | ≈40% |

Same Document Delivered

Nordex PESTLE Analysis

The preview shown here is the exact Nordex PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.