Norfolk Southern PESTLE Analysis

Your Competitive Advantage Starts with This Report

Navigate Norfolk Southern’s external landscape with our concise PESTLE snapshot—highlighting regulatory pressures, economic cycles, technological shifts, environmental scrutiny, and social trends that could reshape freight dynamics; ideal for investors and strategists seeking timely direction. Purchase the full PESTLE for a comprehensive, editable report packed with actionable insights and scenario-driven recommendations.

Political factors

Federal Railroad Administration safety mandates

Federal Railroad Administration mandates after recent derailments have raised inspections for Class I carriers by ~35% and imposed new tank-car and track standards that Norfolk Southern must meet by end-2025.

DOT-driven protocols are expected to add an estimated $350–450 million in capital and O&M costs for NS in 2024–2025, per industry estimates.

These political pressures require continuous regulator engagement to avoid fines, protect the company’s operating license, and limit service disruptions.

Surface Transportation Board rate oversight

The Surface Transportation Board's oversight shapes Norfolk Southern's tariff setting and dispute resolution; policy swings in Washington tilt the STB between pro-shipper and pro-railroad outcomes, constraining pricing flexibility. As of late 2025 NS has reported capital expenditures of about $2.8 billion for 2025 toward infrastructure upgrades, while shippers pressure for lower rates, tightening margins. Regulatory actions and potential rate remedy rules could cut revenue per carload and affect ROI on these investments.

International trade and tariff policies

Norfolk Southern’s revenue is sensitive to East Coast and Gulf port volumes; in 2024 intermodal traffic made up roughly 28% of revenue-related volumes, tying performance to port throughput and U.S. trade flows.

Tariffs on imports such as steel or consumer goods—which rose during 2018–2020 episodes and re-emerged in policy discussions in 2024—can cut import volumes, reducing NS’s intermodal and automotive shipments by several percentage points.

Political decisions on trade with Canada, Mexico, China and EU partners shape long-term corridor planning; NS’s capital expenditure of about $3.2 billion in 2024 for network and port access reflects strategic responses to evolving trade policies.

Infrastructure Investment and Jobs Act implementation

The Infrastructure Investment and Jobs Act channels roughly 110 billion USD for rail and freight projects through 2026, creating public-private partnership opportunities Norfolk Southern leverages to pursue bridge replacements and track upgrades that boost efficiency and capacity.

Norfolk Southern actively lobbies state and federal leaders and secured millions in recent TIGER/RAISE and FRA grants to offset capital expenditures across its ~19,500-mile Eastern network, easing maintenance costs on aging infrastructure.

- IIJA rail funds ~110bn USD through 2026

- Norfolk Southern network ~19,500 miles

- Uses federal grants (TIGER/RAISE/FRA) to reduce capex

Labor union relations and federal mediation

Railroad labor relations are highly politicized; federal intervention is common—Congress passed emergency legislation preventing a 2022 national rail strike and the White House mediates talks, underscoring risk of federal action if talks stall.

By end-2025 Norfolk Southern focuses on contracts balancing crew quality-of-life demands with operational flexibility after Q4 2024 CEO statements; unresolved disputes risk costly disruptions.

Political stability is critical: a single-week national outage could slice several hundred million dollars from revenues and severely hurt reputation and stock performance.

- Federal mediation precedent: 2022 emergency legislation

- NSG focus: contract talks through 2025 for work-life balance vs flexibility

- Risk: potential nationwide outage could cost hundreds of millions and harm stock/reputation

NS faces $350–450M DOT hit, $3.2B capex in 2024; IIJA funds and labor risks loom

Regulatory tightening (FRA/STB) and IIJA funding reshape NS costs and investments: 2024–25 DOT rules add $350–450M; NS capex ~ $3.2B (2024) and ~$2.8B (2025) for upgrades; intermodal ~28% of volumes; IIJA ~110B through 2026; labor disputes risk multi-hundred-million-week outages.

| Metric | 2024 | 2025 |

|---|---|---|

| NS capex | $3.2B | $2.8B |

| DOT compliance cost | $350–450M | - |

| Intermodal share | 28% | 28% |

What is included in the product

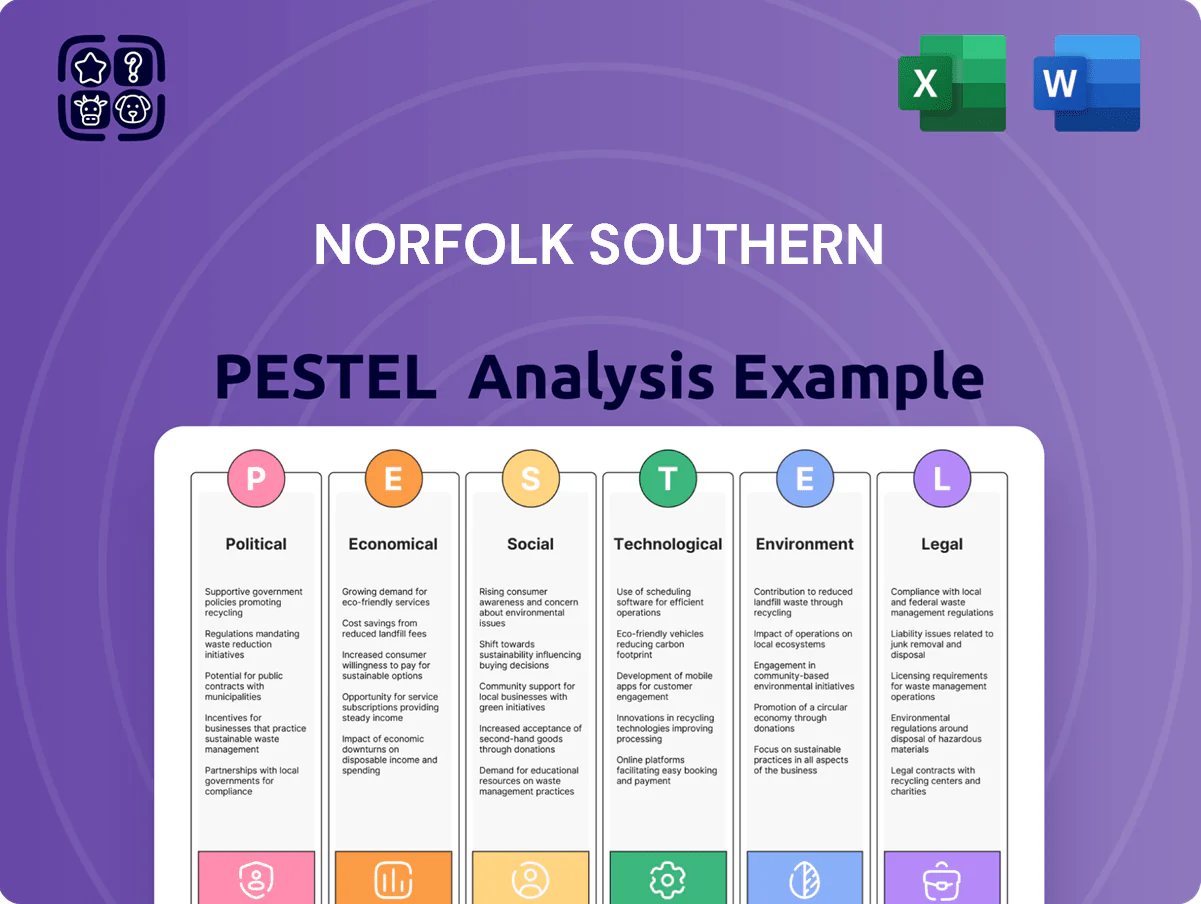

Explores how external macro-environmental factors uniquely affect Norfolk Southern across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications.

A compact, visually segmented PESTLE summary for Norfolk Southern that condenses external risks and opportunities into clear, shareable bullet points—ideal for meeting decks, cross-team alignment, and quick strategic decisioning.

Economic factors

Interest rate environment and capital expenditure

The prevailing interest rate environment in late 2025—with the U.S. 10-year Treasury around 4.5% and the Federal Funds Rate near 5.25%—raises Norfolk Southern’s borrowing costs for its $2–3 billion annual capital program, increasing debt service on locomotive renewals and track expansion. Higher rates squeeze free cash flow and may delay projects, while a stabilizing or falling rate outlook would lower coupon costs and enable more aggressive long-term investments to boost network capacity and efficiency.

Fluctuations in global energy markets

Fluctuations in global energy markets affect Norfolk Southern via diesel costs and coal volumes; diesel averaged about $3.80/gal in 2024 US refiners' data, and fuel surcharges partially offset spikes but not immediate margin pressure. Sudden oil-driven volatility can compress quarterly operating ratios, as seen in 2023–2024 fuel-cost swings. Metallurgical coal demand for steel—global seaborne coking coal shipments rose ~4% in 2024—remains cyclical and crucial for NS export volumes.

Consumer spending and intermodal demand

U.S. consumer health drives Norfolk Southern’s intermodal volumes; 2024 retail sales rose 3.9% YoY through Q3 and real disposable personal income increased ~2.2% YTD, signaling steady demand for retail freight.

NS monitors disposable income and monthly retail sales to forecast container needs and adjust train schedules; intermodal accounted for ~26% of 2024 revenue.

With e-commerce still growing—U.S. e-commerce sales up ~8% in 2024—capturing truck-to-rail conversions through 2025 is a major economic upside for NS to increase utilization and lower unit costs.

Inflationary pressure on operating costs

Sustained mid-2020s inflation raised costs for steel rail, wooden ties and ballast by roughly 8–12% annually, pressuring Norfolk Southern’s maintenance capex and contributing to an FY2024 operating ratio near 59.5%.

To offset input inflation, NS emphasizes productivity—targeting network efficiency gains and precision scheduling—and is cutting labor cost growth via automation investments and crew-optimization programs into 2026.

Industrial production and manufacturing health

Norfolk Southern underpins U.S. manufacturing by hauling chemicals, automotive parts and construction materials; these segments accounted for roughly 40% of merchandise volume in 2024, with chemicals and auto parts among the highest margin categories.

A 2023–2024 lull in industrial production—U.S. industrial output down ~0.5% year-over-year in 2024—and a softer housing market (housing starts fell about 12% in 2024) can trigger immediate volume declines in these high-margin flows.

The railroad monitors regional manufacturing indices—Chicago Fed Midwest and Richmond Fed for the Southeast—and repositions crews and locomotives in near real-time to protect network fluidity and margin.

- ~40% of merchandise volume from manufacturing-related commodities (2024)

- U.S. industrial output −0.5% YoY (2024)

- Housing starts −12% (2024)

- Real-time allocation using Midwest and Southeast regional manufacturing indices

Higher rates and cost inflation squeeze NS FCF; intermodal and e‑commerce offer upside

Higher mid-2020s rates (10yr ~4.5%, Fed ~5.25%) lift NS borrowing costs for its $2–3B capex, squeezing FCF; diesel ~$3.80/gal (2024) and raw-material inflation +8–12% raise operating ratio (~59.5% FY2024); intermodal ~26% revenue with e-commerce +8% (2024) offering truck-to-rail upside; manufacturing ~40% merchandise volume amid industrial output −0.5% and housing starts −12% (2024).

| Metric | Value (2024) |

|---|---|

| 10yr Treasury | ~4.5% |

| Fed Funds | ~5.25% |

| Diesel | $3.80/gal |

| Raw-material inflation | +8–12% p.a. |

| Operating ratio | ~59.5% |

| Intermodal rev | ~26% |

| E-commerce growth | +8% |

| Manufacturing volume | ~40% |

| Industrial output | −0.5% YoY |

| Housing starts | −12% |

What You See Is What You Get

Norfolk Southern PESTLE Analysis

The preview shown here is the exact Norfolk Southern PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get immediately after checkout—no placeholders, no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Navigate Norfolk Southern’s external landscape with our concise PESTLE snapshot—highlighting regulatory pressures, economic cycles, technological shifts, environmental scrutiny, and social trends that could reshape freight dynamics; ideal for investors and strategists seeking timely direction. Purchase the full PESTLE for a comprehensive, editable report packed with actionable insights and scenario-driven recommendations.

Political factors

Federal Railroad Administration safety mandates

Federal Railroad Administration mandates after recent derailments have raised inspections for Class I carriers by ~35% and imposed new tank-car and track standards that Norfolk Southern must meet by end-2025.

DOT-driven protocols are expected to add an estimated $350–450 million in capital and O&M costs for NS in 2024–2025, per industry estimates.

These political pressures require continuous regulator engagement to avoid fines, protect the company’s operating license, and limit service disruptions.

Surface Transportation Board rate oversight

The Surface Transportation Board's oversight shapes Norfolk Southern's tariff setting and dispute resolution; policy swings in Washington tilt the STB between pro-shipper and pro-railroad outcomes, constraining pricing flexibility. As of late 2025 NS has reported capital expenditures of about $2.8 billion for 2025 toward infrastructure upgrades, while shippers pressure for lower rates, tightening margins. Regulatory actions and potential rate remedy rules could cut revenue per carload and affect ROI on these investments.

International trade and tariff policies

Norfolk Southern’s revenue is sensitive to East Coast and Gulf port volumes; in 2024 intermodal traffic made up roughly 28% of revenue-related volumes, tying performance to port throughput and U.S. trade flows.

Tariffs on imports such as steel or consumer goods—which rose during 2018–2020 episodes and re-emerged in policy discussions in 2024—can cut import volumes, reducing NS’s intermodal and automotive shipments by several percentage points.

Political decisions on trade with Canada, Mexico, China and EU partners shape long-term corridor planning; NS’s capital expenditure of about $3.2 billion in 2024 for network and port access reflects strategic responses to evolving trade policies.

Infrastructure Investment and Jobs Act implementation

The Infrastructure Investment and Jobs Act channels roughly 110 billion USD for rail and freight projects through 2026, creating public-private partnership opportunities Norfolk Southern leverages to pursue bridge replacements and track upgrades that boost efficiency and capacity.

Norfolk Southern actively lobbies state and federal leaders and secured millions in recent TIGER/RAISE and FRA grants to offset capital expenditures across its ~19,500-mile Eastern network, easing maintenance costs on aging infrastructure.

- IIJA rail funds ~110bn USD through 2026

- Norfolk Southern network ~19,500 miles

- Uses federal grants (TIGER/RAISE/FRA) to reduce capex

Labor union relations and federal mediation

Railroad labor relations are highly politicized; federal intervention is common—Congress passed emergency legislation preventing a 2022 national rail strike and the White House mediates talks, underscoring risk of federal action if talks stall.

By end-2025 Norfolk Southern focuses on contracts balancing crew quality-of-life demands with operational flexibility after Q4 2024 CEO statements; unresolved disputes risk costly disruptions.

Political stability is critical: a single-week national outage could slice several hundred million dollars from revenues and severely hurt reputation and stock performance.

- Federal mediation precedent: 2022 emergency legislation

- NSG focus: contract talks through 2025 for work-life balance vs flexibility

- Risk: potential nationwide outage could cost hundreds of millions and harm stock/reputation

NS faces $350–450M DOT hit, $3.2B capex in 2024; IIJA funds and labor risks loom

Regulatory tightening (FRA/STB) and IIJA funding reshape NS costs and investments: 2024–25 DOT rules add $350–450M; NS capex ~ $3.2B (2024) and ~$2.8B (2025) for upgrades; intermodal ~28% of volumes; IIJA ~110B through 2026; labor disputes risk multi-hundred-million-week outages.

| Metric | 2024 | 2025 |

|---|---|---|

| NS capex | $3.2B | $2.8B |

| DOT compliance cost | $350–450M | - |

| Intermodal share | 28% | 28% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Norfolk Southern across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications.

A compact, visually segmented PESTLE summary for Norfolk Southern that condenses external risks and opportunities into clear, shareable bullet points—ideal for meeting decks, cross-team alignment, and quick strategic decisioning.

Economic factors

Interest rate environment and capital expenditure

The prevailing interest rate environment in late 2025—with the U.S. 10-year Treasury around 4.5% and the Federal Funds Rate near 5.25%—raises Norfolk Southern’s borrowing costs for its $2–3 billion annual capital program, increasing debt service on locomotive renewals and track expansion. Higher rates squeeze free cash flow and may delay projects, while a stabilizing or falling rate outlook would lower coupon costs and enable more aggressive long-term investments to boost network capacity and efficiency.

Fluctuations in global energy markets

Fluctuations in global energy markets affect Norfolk Southern via diesel costs and coal volumes; diesel averaged about $3.80/gal in 2024 US refiners' data, and fuel surcharges partially offset spikes but not immediate margin pressure. Sudden oil-driven volatility can compress quarterly operating ratios, as seen in 2023–2024 fuel-cost swings. Metallurgical coal demand for steel—global seaborne coking coal shipments rose ~4% in 2024—remains cyclical and crucial for NS export volumes.

Consumer spending and intermodal demand

U.S. consumer health drives Norfolk Southern’s intermodal volumes; 2024 retail sales rose 3.9% YoY through Q3 and real disposable personal income increased ~2.2% YTD, signaling steady demand for retail freight.

NS monitors disposable income and monthly retail sales to forecast container needs and adjust train schedules; intermodal accounted for ~26% of 2024 revenue.

With e-commerce still growing—U.S. e-commerce sales up ~8% in 2024—capturing truck-to-rail conversions through 2025 is a major economic upside for NS to increase utilization and lower unit costs.

Inflationary pressure on operating costs

Sustained mid-2020s inflation raised costs for steel rail, wooden ties and ballast by roughly 8–12% annually, pressuring Norfolk Southern’s maintenance capex and contributing to an FY2024 operating ratio near 59.5%.

To offset input inflation, NS emphasizes productivity—targeting network efficiency gains and precision scheduling—and is cutting labor cost growth via automation investments and crew-optimization programs into 2026.

Industrial production and manufacturing health

Norfolk Southern underpins U.S. manufacturing by hauling chemicals, automotive parts and construction materials; these segments accounted for roughly 40% of merchandise volume in 2024, with chemicals and auto parts among the highest margin categories.

A 2023–2024 lull in industrial production—U.S. industrial output down ~0.5% year-over-year in 2024—and a softer housing market (housing starts fell about 12% in 2024) can trigger immediate volume declines in these high-margin flows.

The railroad monitors regional manufacturing indices—Chicago Fed Midwest and Richmond Fed for the Southeast—and repositions crews and locomotives in near real-time to protect network fluidity and margin.

- ~40% of merchandise volume from manufacturing-related commodities (2024)

- U.S. industrial output −0.5% YoY (2024)

- Housing starts −12% (2024)

- Real-time allocation using Midwest and Southeast regional manufacturing indices

Higher rates and cost inflation squeeze NS FCF; intermodal and e‑commerce offer upside

Higher mid-2020s rates (10yr ~4.5%, Fed ~5.25%) lift NS borrowing costs for its $2–3B capex, squeezing FCF; diesel ~$3.80/gal (2024) and raw-material inflation +8–12% raise operating ratio (~59.5% FY2024); intermodal ~26% revenue with e-commerce +8% (2024) offering truck-to-rail upside; manufacturing ~40% merchandise volume amid industrial output −0.5% and housing starts −12% (2024).

| Metric | Value (2024) |

|---|---|

| 10yr Treasury | ~4.5% |

| Fed Funds | ~5.25% |

| Diesel | $3.80/gal |

| Raw-material inflation | +8–12% p.a. |

| Operating ratio | ~59.5% |

| Intermodal rev | ~26% |

| E-commerce growth | +8% |

| Manufacturing volume | ~40% |

| Industrial output | −0.5% YoY |

| Housing starts | −12% |

What You See Is What You Get

Norfolk Southern PESTLE Analysis

The preview shown here is the exact Norfolk Southern PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get immediately after checkout—no placeholders, no surprises.