Norisol A/S PESTLE Analysis

Skip the Research. Get the Strategy.

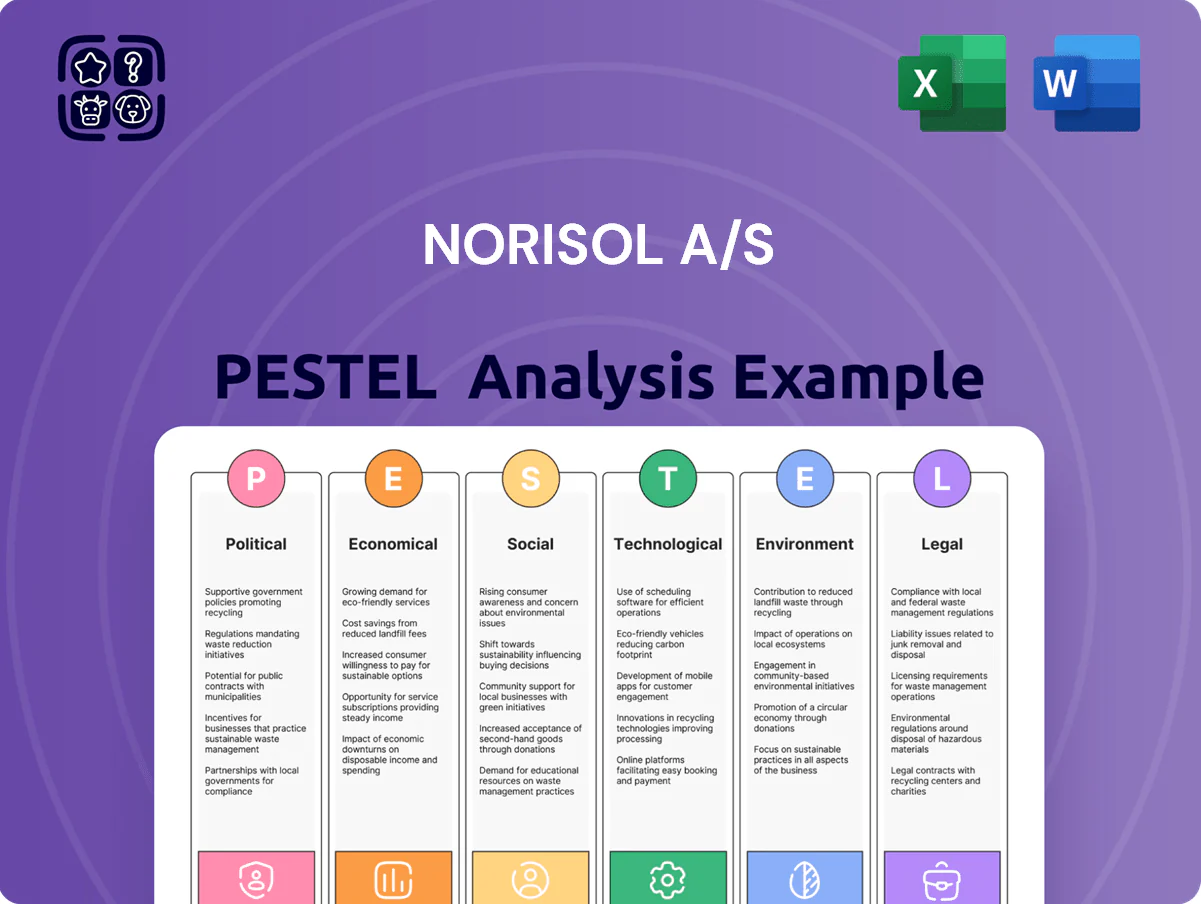

Unlock strategic clarity with our PESTLE Analysis of Norisol A/S—examine political regulations, economic cycles, social trends, technological shifts, legal risks, and environmental pressures that could alter its trajectory; buy the full report to receive the complete, editable analysis and actionable recommendations for investors and strategists.

Political factors

EU Energy Efficiency Directive implementation

The EU’s tightened Energy Efficiency Directive raises insulation performance requirements for commercial and industrial buildings, aiming for 32.5% primary energy savings by 2030 and accelerating retrofits across member states.

As a Danish technical insulation provider, Norisol must adapt product specs and services to meet stricter U-values and reporting obligations to keep clients compliant and avoid fines tied to national transpositions.

Policy-driven retrofit demand supports market growth—EU estimates additional annual investments of €100–150 billion in building efficiency to 2030—sustaining revenue opportunities for Norisol in industrial insulation projects.

Scandinavian offshore energy policy

Government backing for North Sea offshore wind and CCS—Denmark, Norway and Sweden committed to expanding offshore capacity to reach 70+ GW by 2030 across the region—secures a multi-decade project pipeline for Norisol's marine and offshore divisions; stable Northern European politics lowers policy risk for investments exceeding €10bn in regional infrastructure, while state-led programs (e.g., Danish Energy Agency local content targets) favor Norisol's local technical expertise and supply contracts.

Geopolitical energy security priorities

European energy independence policies have driven a 2024–25 surge in domestic infrastructure investment—EU funding for grid and asset upkeep rose ~12% to €47bn in 2024—boosting demand for maintenance and insulation services where Norisol operates. Norisol’s role in improving thermal efficiency of plants helps reduce fuel imports; lifespan-extension decisions for coal, gas and nuclear units (postponements adding 5–15 years) directly increase contract volumes and annual maintenance revenues.

Public infrastructure spending programs

Government-funded construction projects in Denmark and Sweden increasingly mandate high energy performance and safety standards, benefiting established contractors like Norisol A/S that specialize in HVAC and turnkey construction.

Denmark's 2025 budget allocates about DKK 12 billion to public facility upgrades and green retrofits while Sweden earmarked SEK 20 billion for 2025–2026 sustainable building initiatives, creating predictable demand for Norisol's services.

- Stable public contracts due to stringent energy/safety specs

- Denmark 2025: ~DKK 12bn for upgrades

- Sweden 2025–26: ~SEK 20bn for green buildings

- Reliable revenue stream for construction & HVAC

Trade relations and material availability

Political tensions or trade agreements affecting imports of mineral wool and specialized coatings can disrupt Norisol A/S supply chains; EU imports of mineral wool rose 6% in 2024 while China-EU trade frictions pushed regional lead times up 12%.

Changes in tariffs between the EU and external markets—tariff adjustments of 2–8% on construction inputs in 2024—require agile procurement and alternative sourcing to protect margins.

Diplomacy on industrial standards, e.g., updated EU marine coating regs in 2025 raising compliance costs by an estimated 1.5% of project value, dictates technical specs Norisol must meet abroad.

- 2024: EU mineral wool imports +6%

- Lead times +12% amid China-EU tensions

- Tariff shifts 2–8% on construction inputs (2024)

- 2025 EU marine coating regs ≈ +1.5% project cost

EU retrofit surge and offshore buildout boost Norisol demand amid supply constraints

Stronger EU energy rules and national retrofit funding (EU building efficiency investments €100–150bn/yr to 2030; DK 2025 DKK 12bn; SE 2025–26 SEK 20bn) boost demand for Norisol’s insulation and HVAC services; offshore wind/CCS expansions (70+ GW regional target by 2030) secure long-term projects. Supply risks persist: mineral wool imports +6% (2024), lead times +12%, tariff shifts 2–8%, and 2025 marine-coating regs ≈ +1.5% project cost.

| Metric | Value |

|---|---|

| EU retrofit investment need | €100–150bn/yr to 2030 |

| Denmark 2025 budget | DKK 12bn |

| Sweden 2025–26 | SEK 20bn |

| Regional offshore target | 70+ GW by 2030 |

| Mineral wool imports (2024) | +6% |

| Lead times (China-EU tensions) | +12% |

| Tariff shifts (2024) | 2–8% |

| 2025 marine coating impact | ≈+1.5% project cost |

What is included in the product

Explores how external macro-environmental factors uniquely affect Norisol A/S across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking scenarios to identify threats and opportunities for executives, consultants, and investors.

A concise PESTLE snapshot for Norisol A/S that highlights external risks and opportunities by category, ready to drop into presentations or planning sessions for quick team alignment and strategic decision-making.

Economic factors

Industrial energy price volatility

Rising industrial energy prices—European gas up ~40% in 2024 vs 2020 and average industrial electricity tariffs near €0.18–0.22/kWh—boost demand for Norisol’s insulation and HVAC optimization, as clients achieve payback periods often under 3–5 years through reduced heat loss. High energy costs increase approval rates for CAPEX on large-scale insulation projects to protect margins, making efficiency a core financial strategy rather than just sustainability.

Labor market tightness in technical trades

Scarcity of certified scaffolders and insulation technicians in Northern Europe—vacancy rates for construction specialists hit 3.7% in 2024—pushes wages up; Norisol faces average wage inflation of 5–8% for technical staff, raising recruitment costs and margins pressure.

Norisol must invest in retention and training: industry benchmarks show firms spending 1.5–3% of payroll on upskilling; for Norisol this implies €2–4m annually to maintain service quality.

Competition for technical talent from energy retrofit and offshore sectors remains acute, limiting rapid scaling and increasing project delivery risk.

Offshore decommissioning market growth

The North Sea decommissioning market is forecast at USD 41–50 billion cumulative 2024–2035, driving demand for Norisol’s surface protection and scaffolding as platforms retire; UK decommissioning spend hit £4.7bn in 2023 and UK OGA expects increased activity through 2030, creating counter-cyclical revenue that offsets volatility in new-build offshore projects and supports steady margin recovery.

Inflationary pressure on raw materials

Persistent inflation in metals, chemicals and insulation raised input costs by about 9-12% annually in 2023–2024, pressuring Norisol A/S’s long-term service contract margins and forcing upward adjustments to pricing models.

To protect profitability, Norisol must adopt robust cost-plus pricing or indexation clauses tied to commodity indices such as LME and ICE, and pass-through mechanisms to clients.

Volatile global commodity markets—copper up ~15% and petrochemical feedstocks up ~10% in 2024—require continuous monitoring to keep project bids competitive and profitable.

- Implement indexation/cost-plus clauses linked to LME/ICE

- Quarterly commodity monitoring and bid adjustment

- Hedge key metal/chemical exposures where feasible

Interest rate impact on construction investment

Higher interest rates in 2025 reduced new-build starts across Denmark and Norway by about 8–12% year-on-year, pushing Norisol A/S to prioritize maintenance and repair work over new construction contracts.

Private-sector project slowdowns shifted revenue mix toward essential maintenance and government-backed infrastructure projects, which remained more stable despite tighter credit.

Rising cost of capital raised borrowing costs by roughly 1.5–2 percentage points versus 2024, constraining Norisol’s capacity to finance fleet upgrades and new equipment purchases.

- 2025 new-build starts down ~8–12%

- Shift toward maintenance and public projects

- Borrowing costs +1.5–2 pp vs 2024

Costs Surge: Gas +40%, Inputs +9–12%, Higher Rates—Index, Hedge, Monitor

Energy costs up ~40% (gas 2024 vs 2020); industrial electricity €0.18–0.22/kWh; wage inflation 5–8% for technicians; input costs +9–12% (2023–24); North Sea decommissioning USD 41–50bn (2024–35); 2025 new-build starts -8–12%; borrowing costs +1.5–2pp vs 2024; recommend indexation, quarterly commodity monitoring, hedging.

| Metric | Value |

|---|---|

| Gas change (2024 vs 2020) | +~40% |

| Industrial electricity | €0.18–0.22/kWh |

| Wage inflation (tech) | 5–8% |

| Input costs (2023–24) | +9–12% |

| North Sea decommissioning (2024–35) | USD 41–50bn |

| New-build starts 2025 | -8–12% |

| Borrowing cost change | +1.5–2 pp vs 2024 |

What You See Is What You Get

Norisol A/S PESTLE Analysis

The preview shown here is the exact Norisol A/S PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Norisol A/S—examine political regulations, economic cycles, social trends, technological shifts, legal risks, and environmental pressures that could alter its trajectory; buy the full report to receive the complete, editable analysis and actionable recommendations for investors and strategists.

Political factors

EU Energy Efficiency Directive implementation

The EU’s tightened Energy Efficiency Directive raises insulation performance requirements for commercial and industrial buildings, aiming for 32.5% primary energy savings by 2030 and accelerating retrofits across member states.

As a Danish technical insulation provider, Norisol must adapt product specs and services to meet stricter U-values and reporting obligations to keep clients compliant and avoid fines tied to national transpositions.

Policy-driven retrofit demand supports market growth—EU estimates additional annual investments of €100–150 billion in building efficiency to 2030—sustaining revenue opportunities for Norisol in industrial insulation projects.

Scandinavian offshore energy policy

Government backing for North Sea offshore wind and CCS—Denmark, Norway and Sweden committed to expanding offshore capacity to reach 70+ GW by 2030 across the region—secures a multi-decade project pipeline for Norisol's marine and offshore divisions; stable Northern European politics lowers policy risk for investments exceeding €10bn in regional infrastructure, while state-led programs (e.g., Danish Energy Agency local content targets) favor Norisol's local technical expertise and supply contracts.

Geopolitical energy security priorities

European energy independence policies have driven a 2024–25 surge in domestic infrastructure investment—EU funding for grid and asset upkeep rose ~12% to €47bn in 2024—boosting demand for maintenance and insulation services where Norisol operates. Norisol’s role in improving thermal efficiency of plants helps reduce fuel imports; lifespan-extension decisions for coal, gas and nuclear units (postponements adding 5–15 years) directly increase contract volumes and annual maintenance revenues.

Public infrastructure spending programs

Government-funded construction projects in Denmark and Sweden increasingly mandate high energy performance and safety standards, benefiting established contractors like Norisol A/S that specialize in HVAC and turnkey construction.

Denmark's 2025 budget allocates about DKK 12 billion to public facility upgrades and green retrofits while Sweden earmarked SEK 20 billion for 2025–2026 sustainable building initiatives, creating predictable demand for Norisol's services.

- Stable public contracts due to stringent energy/safety specs

- Denmark 2025: ~DKK 12bn for upgrades

- Sweden 2025–26: ~SEK 20bn for green buildings

- Reliable revenue stream for construction & HVAC

Trade relations and material availability

Political tensions or trade agreements affecting imports of mineral wool and specialized coatings can disrupt Norisol A/S supply chains; EU imports of mineral wool rose 6% in 2024 while China-EU trade frictions pushed regional lead times up 12%.

Changes in tariffs between the EU and external markets—tariff adjustments of 2–8% on construction inputs in 2024—require agile procurement and alternative sourcing to protect margins.

Diplomacy on industrial standards, e.g., updated EU marine coating regs in 2025 raising compliance costs by an estimated 1.5% of project value, dictates technical specs Norisol must meet abroad.

- 2024: EU mineral wool imports +6%

- Lead times +12% amid China-EU tensions

- Tariff shifts 2–8% on construction inputs (2024)

- 2025 EU marine coating regs ≈ +1.5% project cost

EU retrofit surge and offshore buildout boost Norisol demand amid supply constraints

Stronger EU energy rules and national retrofit funding (EU building efficiency investments €100–150bn/yr to 2030; DK 2025 DKK 12bn; SE 2025–26 SEK 20bn) boost demand for Norisol’s insulation and HVAC services; offshore wind/CCS expansions (70+ GW regional target by 2030) secure long-term projects. Supply risks persist: mineral wool imports +6% (2024), lead times +12%, tariff shifts 2–8%, and 2025 marine-coating regs ≈ +1.5% project cost.

| Metric | Value |

|---|---|

| EU retrofit investment need | €100–150bn/yr to 2030 |

| Denmark 2025 budget | DKK 12bn |

| Sweden 2025–26 | SEK 20bn |

| Regional offshore target | 70+ GW by 2030 |

| Mineral wool imports (2024) | +6% |

| Lead times (China-EU tensions) | +12% |

| Tariff shifts (2024) | 2–8% |

| 2025 marine coating impact | ≈+1.5% project cost |

What is included in the product

Explores how external macro-environmental factors uniquely affect Norisol A/S across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking scenarios to identify threats and opportunities for executives, consultants, and investors.

A concise PESTLE snapshot for Norisol A/S that highlights external risks and opportunities by category, ready to drop into presentations or planning sessions for quick team alignment and strategic decision-making.

Economic factors

Industrial energy price volatility

Rising industrial energy prices—European gas up ~40% in 2024 vs 2020 and average industrial electricity tariffs near €0.18–0.22/kWh—boost demand for Norisol’s insulation and HVAC optimization, as clients achieve payback periods often under 3–5 years through reduced heat loss. High energy costs increase approval rates for CAPEX on large-scale insulation projects to protect margins, making efficiency a core financial strategy rather than just sustainability.

Labor market tightness in technical trades

Scarcity of certified scaffolders and insulation technicians in Northern Europe—vacancy rates for construction specialists hit 3.7% in 2024—pushes wages up; Norisol faces average wage inflation of 5–8% for technical staff, raising recruitment costs and margins pressure.

Norisol must invest in retention and training: industry benchmarks show firms spending 1.5–3% of payroll on upskilling; for Norisol this implies €2–4m annually to maintain service quality.

Competition for technical talent from energy retrofit and offshore sectors remains acute, limiting rapid scaling and increasing project delivery risk.

Offshore decommissioning market growth

The North Sea decommissioning market is forecast at USD 41–50 billion cumulative 2024–2035, driving demand for Norisol’s surface protection and scaffolding as platforms retire; UK decommissioning spend hit £4.7bn in 2023 and UK OGA expects increased activity through 2030, creating counter-cyclical revenue that offsets volatility in new-build offshore projects and supports steady margin recovery.

Inflationary pressure on raw materials

Persistent inflation in metals, chemicals and insulation raised input costs by about 9-12% annually in 2023–2024, pressuring Norisol A/S’s long-term service contract margins and forcing upward adjustments to pricing models.

To protect profitability, Norisol must adopt robust cost-plus pricing or indexation clauses tied to commodity indices such as LME and ICE, and pass-through mechanisms to clients.

Volatile global commodity markets—copper up ~15% and petrochemical feedstocks up ~10% in 2024—require continuous monitoring to keep project bids competitive and profitable.

- Implement indexation/cost-plus clauses linked to LME/ICE

- Quarterly commodity monitoring and bid adjustment

- Hedge key metal/chemical exposures where feasible

Interest rate impact on construction investment

Higher interest rates in 2025 reduced new-build starts across Denmark and Norway by about 8–12% year-on-year, pushing Norisol A/S to prioritize maintenance and repair work over new construction contracts.

Private-sector project slowdowns shifted revenue mix toward essential maintenance and government-backed infrastructure projects, which remained more stable despite tighter credit.

Rising cost of capital raised borrowing costs by roughly 1.5–2 percentage points versus 2024, constraining Norisol’s capacity to finance fleet upgrades and new equipment purchases.

- 2025 new-build starts down ~8–12%

- Shift toward maintenance and public projects

- Borrowing costs +1.5–2 pp vs 2024

Costs Surge: Gas +40%, Inputs +9–12%, Higher Rates—Index, Hedge, Monitor

Energy costs up ~40% (gas 2024 vs 2020); industrial electricity €0.18–0.22/kWh; wage inflation 5–8% for technicians; input costs +9–12% (2023–24); North Sea decommissioning USD 41–50bn (2024–35); 2025 new-build starts -8–12%; borrowing costs +1.5–2pp vs 2024; recommend indexation, quarterly commodity monitoring, hedging.

| Metric | Value |

|---|---|

| Gas change (2024 vs 2020) | +~40% |

| Industrial electricity | €0.18–0.22/kWh |

| Wage inflation (tech) | 5–8% |

| Input costs (2023–24) | +9–12% |

| North Sea decommissioning (2024–35) | USD 41–50bn |

| New-build starts 2025 | -8–12% |

| Borrowing cost change | +1.5–2 pp vs 2024 |

What You See Is What You Get

Norisol A/S PESTLE Analysis

The preview shown here is the exact Norisol A/S PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment, with no placeholders or surprises.