Norwegian Air Shuttle Boston Consulting Group Matrix

See the Bigger Picture

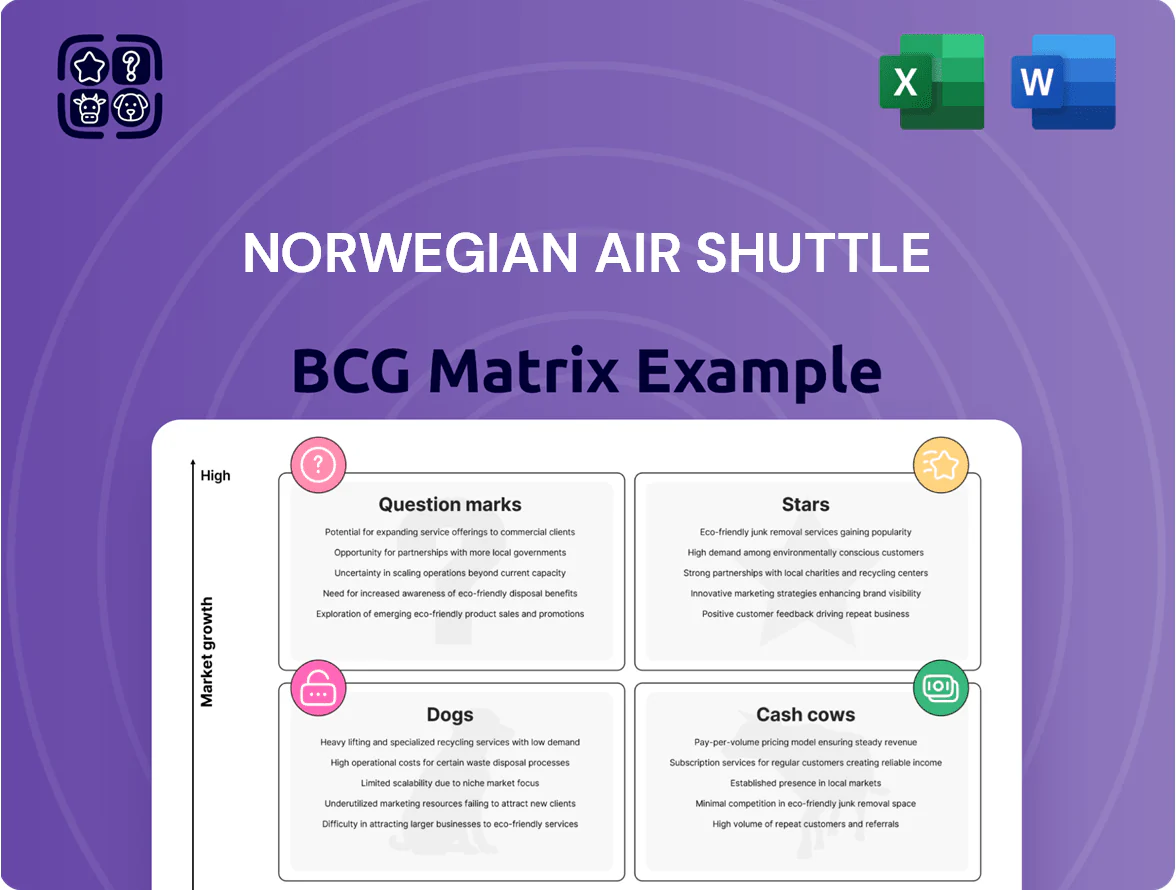

Norwegian Air Shuttle sits at a crossroads—legacy routes and fleet renewal create mixed market share signals, with potential Stars in leisure long-haul recovery and Question Marks around regional connectivity amid cost pressure. The full BCG Matrix unpacks quadrant placements, cash generation risks, and growth-investment priorities to guide fleet, route, and capital-allocation strategy. Purchase the complete report for data-driven recommendations, editable Word and Excel deliverables, and a ready-to-use strategic roadmap to optimize returns.

Stars

Short-Haul Nordic Routes

Short-Haul Nordic Routes: by late 2025 Norwegian Air Shuttle holds over 50% market share in Norway after integrating Widerøe, driving group passenger volumes to a record 27.3 million in 2025.

These routes produce strong cash flow but face intense competition from Ryanair and SAS, forcing frequent capacity shifts for seasonal demand and high reinvestment in fleet and operations.

Widerøe Regional Integration

The Widerøe acquisition is a high-growth Star, supplying a unique feeder network that links remote Norwegian communities to major hubs and boosts group connectivity.

In 2025 Widerøe carried over 4.1 million passengers, helping drive Norwegian Air Shuttle’s record operating profit of NOK 3.7 billion and group load factor of 86% by year-end.

Demand for Nordic coolcations and Public Service Obligation (PSO) contracts lift revenue, but ongoing capital is needed for fleet upkeep and integrating operations to sustain synergies.

Modern Boeing 737 MAX Fleet

Norwegian’s modernisation makes the Boeing 737 MAX 8 a Star: 33 MAX 8 in service by late 2025 and 50 on order give clear operational efficiency gains.

MAX 8 cuts fuel burn ~14% vs older 737s, helping the airline aim for a 45% CO2 reduction by 2030 and lowering per-seat costs in growth markets.

Fleet renewal requires heavy cash for purchases and leases—capital outflow that pressures liquidity—but is vital to sustain a low-cost base.

MAX 8’s fuel savings underpin Program X, supporting management’s NOK 1 billion profitability target by 2026 via lower fuel and maintenance spend.

Ancillary Revenue Services

Ancillary revenue is a high-growth leader for Norwegian, rising 5.1% in 2025 to nearly NOK 4.8 billion as more passengers buy add-ons like seats, bags, and onboard sales.

These services grow faster than base fares and carry higher margins; with modest marketing spend to lift conversion, they can evolve into a cash cow under the no-frills model.

Norwegian is investing in digital distribution and interlining tech to boost upsell, distribution reach, and ancillary attach rates.

- 2025 ancillary revenue: ~NOK 4.8bn (up 5.1%)

- Key items: seat selection, extra baggage, in-flight sales

- Margin: higher than ticket revenue; marketing-dependent

- Capex: digital platforms for upsell and interlining

New Leisure Destination Expansion

The 17 new routes for summer 2025 and 12 for summer 2026, including Morocco and Italy, place Norwegian Air Shuttle in a high-growth Stars segment—driven by a 2024–25 Nordic leisure surge where seat bookings to southern Europe rose ~28% year-over-year.

These routes need heavy promotion and placement costs—expect higher unit marketing spend and lower load factors initially—but they diversify network risk beyond Scandinavia and target growing demand for sunny European and North African hotspots.

Successful Stars should mature into cash cows as brand recognition and yields improve; if routes hit 75% load factor within 12–18 months, they can become stable earners.

- 17 routes (2025) + 12 routes (2026)

- Key markets: Morocco, Italy

- Nordic leisure bookings up ~28% (2024–25)

- Target: 75% load factor in 12–18 months

- High initial promo costs, long-term yield diversification

Record 27.3M pax, NOK3.7bn op profit—MAX 8 fleet & NOK4.8bn ancillaries fuel growth

Stars: Short-haul Nordic routes, Widerøe feeder, Boeing 737 MAX 8, ancillary revenue, and new leisure routes drive high growth—record 27.3m passengers, NOK 3.7bn operating profit (2025); MAX 8: 33 in service, 50 on order; Widerøe: 4.1m pax; ancillary: NOK 4.8bn (2025).

| Metric | 2025 |

|---|---|

| Passengers | 27.3m |

| Op profit | NOK 3.7bn |

| Widerøe pax | 4.1m |

| Ancillary | NOK 4.8bn |

| MAX 8 | 33/50 |

What is included in the product

In-depth BCG review of Norwegian Air Shuttle: identifies Stars, Cash Cows, Question Marks, Dogs with strategic investment, hold, divest guidance.

One-page overview placing Norwegian Air Shuttle units in BCG quadrants for quick strategic clarity and investor briefing

Cash Cows

Domestic Norwegian Trunk Routes

The core domestic trunk routes—Oslo, Bergen, Trondheim—are Norwegian Air Shuttle’s primary cash cow, holding high market share in a mature market and delivering steady cash flow with average load factors of 86% in 2025.

Low promotional spend lets Norwegian milk profits from these routes to fund growth and service corporate debt; cash from operations supported the board’s 2025 proposal of a NOK 0.80 per share dividend.

Norwegian Reward Loyalty Program

Norwegian Reward is a mature, high-market-share cash cow for Norwegian Air Shuttle, generating steady revenue with low incremental investment; by late 2025 it reported ~4.3 million members and contributed an estimated NOK 650–700 million in partner commission revenue in 2024–25.

It drives retention and repeat bookings—members account for ~55% of revenue passengers—while high-margin partner fees fund digital CX R&D and shore up group liquidity.

Widerøe integration expanded reach across Nordic regional routes, boosting Reward redemptions by ~18% year-on-year and reinforcing the program as a cornerstone of Nordic market strength.

Established European Capital Connections

Routes linking Nordic capitals to hubs like London Gatwick and Berlin are mature markets where Norwegian holds ~30–40% share on key city pairs and sustained load factors of ~82% in 2025, giving reliable yields and high regularity.

London was the network’s top non‑Nordic destination in 2025, generating ~12% of group revenue and steady unit revenue, so these lanes need less marketing and support than launches.

Lower promo spend lets Norwegian focus on unit cost control; steady cash flow from these routes covered ~15% of 2025 administrative expenses and funded deposits for five A320neo-family aircraft ordered in 2024.

Ground Handling and Third-Party Services

Through subsidiary Widerøe Ground Handling the group controls ground services at 41 Norwegian airports, operating in a mature, low‑growth market while delivering steady 'other revenue' of several hundred million NOK in 2025.

The unit serves both Norwegian Air Shuttle flights and third‑party carriers and generates more cash than it consumes, making it a classic Cash Cow in the BCG matrix.

That stable cash flow underpinned group liquidity of NOK 7.4 billion at year‑end 2025, supporting operations and investment flexibility.

- Widerøe Ground Handling: 41 airports

- Other revenue: several hundred million NOK (2025)

- Net cash generator: services own and third‑party flights

- Group liquidity: NOK 7.4 billion (YE 2025)

Winter Seasonal Sun Routes

Established winter routes to the Canary Islands and Southern Spain became reliable cash cows for Norwegian Air Shuttle (NAS) in winter 2025, delivering average load factors near 89% and ancillary revenue uplift of ~12% versus Q4 2024.

These mature markets show high repeat bookings, low promo spend, and year-over-year yield stability; NAS trimmed capacity 8% in Jan–Mar 2025 and converted a typical loss quarter into positive EBIT for the network winter trunk.

Profits from these sun routes helped offset broader seasonality, contributing an estimated NOK 450–520 million to winter 2025 operating profit, stabilizing group cash flow.

- Load factor ~89% winter 2025

- Ancillary +12% vs Q4 2024

- Capacity cut 8% Jan–Mar 2025

- Estimated NOK 450–520m contribution

NAS cash cows: high-load domestic, Nordic‑UK & sun routes fuel strong yields and dividend

Core domestic trunk routes, Norwegian Reward, Widerøe Ground Handling, Nordic‑UK city pairs and winter sun routes are NAS cash cows, delivering high load factors (domestic 86%, Nordic‑UK ~82%, sun ~89% in 2025), steady ancillary income, and funded a NOK 0.80/share dividend and YE liquidity NOK 7.4bn.

| Asset | Key 2025 metric |

|---|---|

| Domestic routes | Load 86% |

| Reward | 4.3m members |

| WGH | 41 airports |

| Sun routes | Load 89% |

Preview = Final Product

Norwegian Air Shuttle BCG Matrix

The file you're previewing is the exact Norwegian Air Shuttle BCG Matrix report you'll receive after purchase—fully formatted, no watermarks or demo content, and ready for presentation or analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Norwegian Air Shuttle sits at a crossroads—legacy routes and fleet renewal create mixed market share signals, with potential Stars in leisure long-haul recovery and Question Marks around regional connectivity amid cost pressure. The full BCG Matrix unpacks quadrant placements, cash generation risks, and growth-investment priorities to guide fleet, route, and capital-allocation strategy. Purchase the complete report for data-driven recommendations, editable Word and Excel deliverables, and a ready-to-use strategic roadmap to optimize returns.

Stars

Short-Haul Nordic Routes

Short-Haul Nordic Routes: by late 2025 Norwegian Air Shuttle holds over 50% market share in Norway after integrating Widerøe, driving group passenger volumes to a record 27.3 million in 2025.

These routes produce strong cash flow but face intense competition from Ryanair and SAS, forcing frequent capacity shifts for seasonal demand and high reinvestment in fleet and operations.

Widerøe Regional Integration

The Widerøe acquisition is a high-growth Star, supplying a unique feeder network that links remote Norwegian communities to major hubs and boosts group connectivity.

In 2025 Widerøe carried over 4.1 million passengers, helping drive Norwegian Air Shuttle’s record operating profit of NOK 3.7 billion and group load factor of 86% by year-end.

Demand for Nordic coolcations and Public Service Obligation (PSO) contracts lift revenue, but ongoing capital is needed for fleet upkeep and integrating operations to sustain synergies.

Modern Boeing 737 MAX Fleet

Norwegian’s modernisation makes the Boeing 737 MAX 8 a Star: 33 MAX 8 in service by late 2025 and 50 on order give clear operational efficiency gains.

MAX 8 cuts fuel burn ~14% vs older 737s, helping the airline aim for a 45% CO2 reduction by 2030 and lowering per-seat costs in growth markets.

Fleet renewal requires heavy cash for purchases and leases—capital outflow that pressures liquidity—but is vital to sustain a low-cost base.

MAX 8’s fuel savings underpin Program X, supporting management’s NOK 1 billion profitability target by 2026 via lower fuel and maintenance spend.

Ancillary Revenue Services

Ancillary revenue is a high-growth leader for Norwegian, rising 5.1% in 2025 to nearly NOK 4.8 billion as more passengers buy add-ons like seats, bags, and onboard sales.

These services grow faster than base fares and carry higher margins; with modest marketing spend to lift conversion, they can evolve into a cash cow under the no-frills model.

Norwegian is investing in digital distribution and interlining tech to boost upsell, distribution reach, and ancillary attach rates.

- 2025 ancillary revenue: ~NOK 4.8bn (up 5.1%)

- Key items: seat selection, extra baggage, in-flight sales

- Margin: higher than ticket revenue; marketing-dependent

- Capex: digital platforms for upsell and interlining

New Leisure Destination Expansion

The 17 new routes for summer 2025 and 12 for summer 2026, including Morocco and Italy, place Norwegian Air Shuttle in a high-growth Stars segment—driven by a 2024–25 Nordic leisure surge where seat bookings to southern Europe rose ~28% year-over-year.

These routes need heavy promotion and placement costs—expect higher unit marketing spend and lower load factors initially—but they diversify network risk beyond Scandinavia and target growing demand for sunny European and North African hotspots.

Successful Stars should mature into cash cows as brand recognition and yields improve; if routes hit 75% load factor within 12–18 months, they can become stable earners.

- 17 routes (2025) + 12 routes (2026)

- Key markets: Morocco, Italy

- Nordic leisure bookings up ~28% (2024–25)

- Target: 75% load factor in 12–18 months

- High initial promo costs, long-term yield diversification

Record 27.3M pax, NOK3.7bn op profit—MAX 8 fleet & NOK4.8bn ancillaries fuel growth

Stars: Short-haul Nordic routes, Widerøe feeder, Boeing 737 MAX 8, ancillary revenue, and new leisure routes drive high growth—record 27.3m passengers, NOK 3.7bn operating profit (2025); MAX 8: 33 in service, 50 on order; Widerøe: 4.1m pax; ancillary: NOK 4.8bn (2025).

| Metric | 2025 |

|---|---|

| Passengers | 27.3m |

| Op profit | NOK 3.7bn |

| Widerøe pax | 4.1m |

| Ancillary | NOK 4.8bn |

| MAX 8 | 33/50 |

What is included in the product

In-depth BCG review of Norwegian Air Shuttle: identifies Stars, Cash Cows, Question Marks, Dogs with strategic investment, hold, divest guidance.

One-page overview placing Norwegian Air Shuttle units in BCG quadrants for quick strategic clarity and investor briefing

Cash Cows

Domestic Norwegian Trunk Routes

The core domestic trunk routes—Oslo, Bergen, Trondheim—are Norwegian Air Shuttle’s primary cash cow, holding high market share in a mature market and delivering steady cash flow with average load factors of 86% in 2025.

Low promotional spend lets Norwegian milk profits from these routes to fund growth and service corporate debt; cash from operations supported the board’s 2025 proposal of a NOK 0.80 per share dividend.

Norwegian Reward Loyalty Program

Norwegian Reward is a mature, high-market-share cash cow for Norwegian Air Shuttle, generating steady revenue with low incremental investment; by late 2025 it reported ~4.3 million members and contributed an estimated NOK 650–700 million in partner commission revenue in 2024–25.

It drives retention and repeat bookings—members account for ~55% of revenue passengers—while high-margin partner fees fund digital CX R&D and shore up group liquidity.

Widerøe integration expanded reach across Nordic regional routes, boosting Reward redemptions by ~18% year-on-year and reinforcing the program as a cornerstone of Nordic market strength.

Established European Capital Connections

Routes linking Nordic capitals to hubs like London Gatwick and Berlin are mature markets where Norwegian holds ~30–40% share on key city pairs and sustained load factors of ~82% in 2025, giving reliable yields and high regularity.

London was the network’s top non‑Nordic destination in 2025, generating ~12% of group revenue and steady unit revenue, so these lanes need less marketing and support than launches.

Lower promo spend lets Norwegian focus on unit cost control; steady cash flow from these routes covered ~15% of 2025 administrative expenses and funded deposits for five A320neo-family aircraft ordered in 2024.

Ground Handling and Third-Party Services

Through subsidiary Widerøe Ground Handling the group controls ground services at 41 Norwegian airports, operating in a mature, low‑growth market while delivering steady 'other revenue' of several hundred million NOK in 2025.

The unit serves both Norwegian Air Shuttle flights and third‑party carriers and generates more cash than it consumes, making it a classic Cash Cow in the BCG matrix.

That stable cash flow underpinned group liquidity of NOK 7.4 billion at year‑end 2025, supporting operations and investment flexibility.

- Widerøe Ground Handling: 41 airports

- Other revenue: several hundred million NOK (2025)

- Net cash generator: services own and third‑party flights

- Group liquidity: NOK 7.4 billion (YE 2025)

Winter Seasonal Sun Routes

Established winter routes to the Canary Islands and Southern Spain became reliable cash cows for Norwegian Air Shuttle (NAS) in winter 2025, delivering average load factors near 89% and ancillary revenue uplift of ~12% versus Q4 2024.

These mature markets show high repeat bookings, low promo spend, and year-over-year yield stability; NAS trimmed capacity 8% in Jan–Mar 2025 and converted a typical loss quarter into positive EBIT for the network winter trunk.

Profits from these sun routes helped offset broader seasonality, contributing an estimated NOK 450–520 million to winter 2025 operating profit, stabilizing group cash flow.

- Load factor ~89% winter 2025

- Ancillary +12% vs Q4 2024

- Capacity cut 8% Jan–Mar 2025

- Estimated NOK 450–520m contribution

NAS cash cows: high-load domestic, Nordic‑UK & sun routes fuel strong yields and dividend

Core domestic trunk routes, Norwegian Reward, Widerøe Ground Handling, Nordic‑UK city pairs and winter sun routes are NAS cash cows, delivering high load factors (domestic 86%, Nordic‑UK ~82%, sun ~89% in 2025), steady ancillary income, and funded a NOK 0.80/share dividend and YE liquidity NOK 7.4bn.

| Asset | Key 2025 metric |

|---|---|

| Domestic routes | Load 86% |

| Reward | 4.3m members |

| WGH | 41 airports |

| Sun routes | Load 89% |

Preview = Final Product

Norwegian Air Shuttle BCG Matrix

The file you're previewing is the exact Norwegian Air Shuttle BCG Matrix report you'll receive after purchase—fully formatted, no watermarks or demo content, and ready for presentation or analysis.