NOS Boston Consulting Group Matrix

Download Your Competitive Advantage

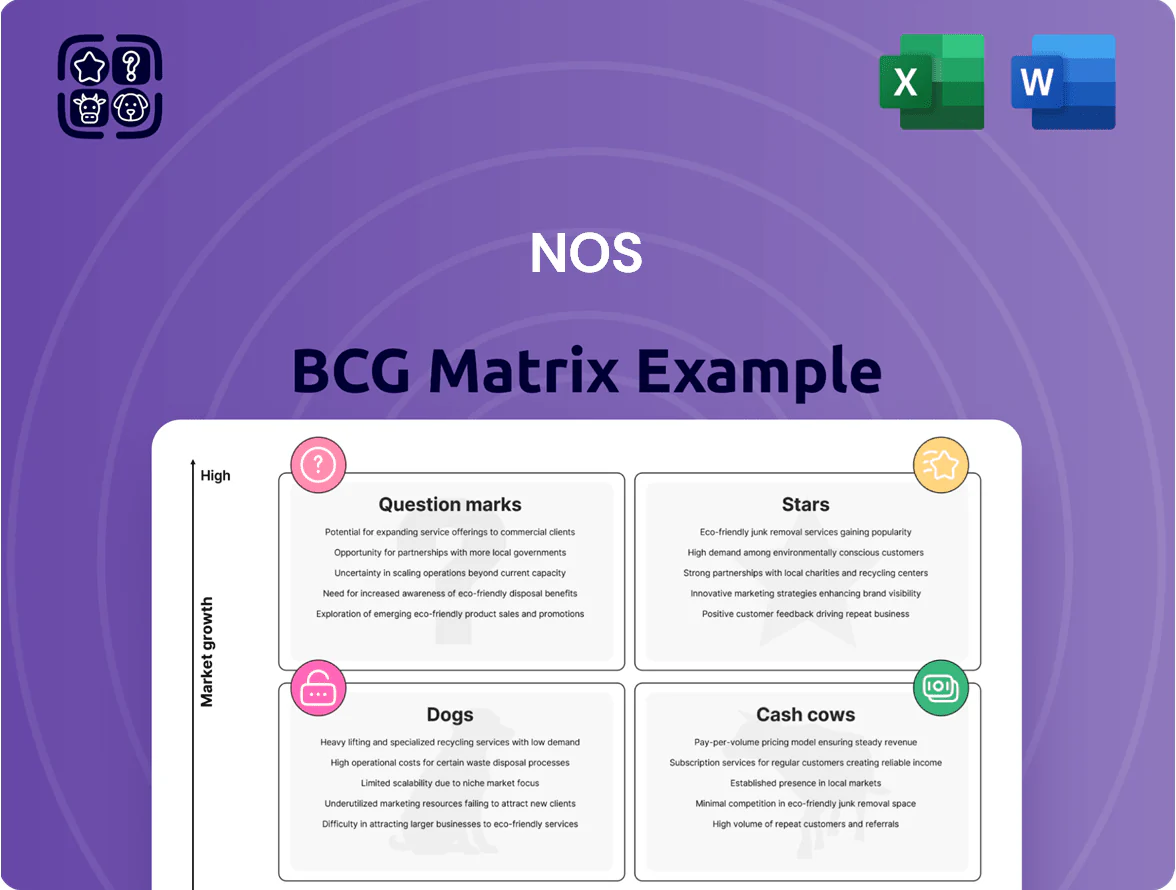

The NOS BCG Matrix snapshot highlights where key services may sit among Stars, Cash Cows, Question Marks, and Dogs—offering quick clarity on growth potential and resource efficiency. This preview teases quadrant placements and strategic implications; purchase the full BCG Matrix for a complete, data-driven breakdown, actionable recommendations, and polished Word + Excel deliverables you can use to prioritize investments and sharpen competitive strategy.

Stars

5G Standalone Network Services

The full deployment of 5G Standalone (SA) architecture by end-2025 is NOS’s primary growth engine, targeting €120–€180 million incremental annual service revenue by 2026 based on industry ARPU uplifts of 15–25% for premium tiers.

This segment holds high market share in the premium mobile tier, delivering <1 ms latency and network slicing for enterprise and AR/VR use cases, supporting NOS’s 35% share of premium postpaid revenue in 2024.

CAPEX for radio core upgrades and densification is estimated at €220–€300 million through 2025; still, SA is essential to defend margins as mobile data traffic grows ~40% CAGR to 2027.

Next-Generation Fiber Expansion

NOS is rapidly expanding Fiber-to-the-Home, targeting underserved Portuguese areas with a rollout that reached 1.2 million homes passed by Q3 2025, up 22% year-on-year.

Demand for symmetrical gigabit speeds and bundled smart‑home services drives ARPU gains; NOS reported fixed broadband ARPU of €30.4 in 2024, +4% vs 2023.

As market leader in high‑speed broadband, NOS uses fiber to secure long‑term residential contracts—fiber churn is ~0.9% vs 1.7% for copper—locking revenue before saturation.

Enterprise Cloud and Managed Services

Enterprise Cloud and Managed Services is a Star: Portuguese SMEs drove cloud spend to an estimated €420m in 2024 (up 18% YoY), and NOS captured roughly 28% share by bundling cybersecurity and 2nd‑site storage, boosting recurring revenue by €64m in 2024.

NOS has invested ~€150m in data centers through 2025, matched by 47% SMB adoption of managed IT services in Portugal, keeping customer churn below 6% and sustaining rapid ARPU growth.

Integrated OTT Streaming Partnerships

By integrating Disney Plus and Netflix into its platform, NOS retained leadership as Portugal’s top entertainment hub, with pay-TV and streaming ARPU rising 8% in 2024 to €22.4 and streaming hours up 35% YoY as on-demand viewing surpassed linear TV in Q3 2024.

High-growth segment: Portuguese subscription streaming users climbed to 2.1M in 2024, and OTT revenue for NOS grew 18% YoY, so NOS must keep licensing deals and marketing spend to defend gateway status.

- Top partners: Disney Plus, Netflix integrated

- Streaming users: 2.1M (2024)

- OTT revenue growth: +18% YoY (2024)

- ARPU: €22.4 (2024), +8% YoY

- Viewing shift: on-demand +35% YoY (Q3 2024)

Industrial IoT and Smart Cities

NOS leads Portugal's Industrial IoT and smart-city projects, deploying sensor networks for traffic, waste, and energy across multiple districts and securing municipal contracts since 2020.

These projects target high growth: EU smart-city market CAGR 19% (2021–25) and Portugal public IoT spend up ~22% in 2024; NOS aims to convert pilots into recurring revenues, estimating €25–40m annual IoT ARR by 2027 from current pipelines.

- First-to-market in several districts

- Targets traffic, waste, energy sensors (thousands deployed)

- Estimated €25–40m IoT ARR by 2027

- Portugal public IoT spend +22% in 2024

NOS growth engines: 5G SA, FTTH, Cloud, Streaming & IoT fueling strong revenue upside

NOS’s Stars: 5G SA, FTTH, Cloud/Managed Services, Streaming, and Industrial IoT drive high growth and share—5G SA adds €120–180m by 2026; FTTH homes passed 1.2M (Q3 2025); Cloud share ~28% with €64m recurring uplift (2024); Streaming users 2.1M, OTT +18% YoY; IoT pipeline targets €25–40m ARR by 2027.

| Segment | Key metric | 2024–25 data |

|---|---|---|

| 5G SA | Revenue uplift | €120–180m (by 2026) |

| FTTH | Homes passed | 1.2M (Q3 2025) |

| Cloud | Share / uplift | 28% share; +€64m (2024) |

| Streaming | Users / growth | 2.1M; +18% YoY (2024) |

| IoT | Target ARR | €25–40m (by 2027) |

What is included in the product

In-depth BCG review of NOS products with clear strategic guidance for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix mapping units by market share and growth to speed strategic focus and resource allocation

Cash Cows

Residential Pay TV Services

NOS holds roughly 40%–45% share of Portugal’s pay-TV market (2024 ARPU ~45€/month), a mature segment with flat subscriber growth; it produces substantial free cash flow—estimated EBITDA margin ~30% in 2024—and needs only routine capex (~5% of revenue) for maintenance.

NOS Cinema Exhibition

As the absolute leader in the Portuguese cinema market, NOS Cinema Exhibition delivers steady revenue—ticket and concession sales generated approx. €110m in 2024, underpinning group cash flow.

Market growth is low due to streaming's rise; Portuguese box office grew just 1.2% in 2024, yet NOS’s brand yields higher-than-average margins near 18%.

This unit remains a reliable liquidity source, funding corporate debt service and dividends—helping cover a portion of NOS’s €220m net interest expense in 2024.

Standard 4G Mobile Contracts

Standard 4G mobile contracts remain a cash cow for NOS, holding an estimated 28% share of Portugal’s mature 4G market in 2025 and delivering predictable ARPU around €12–€15 monthly, so marketing spend is low versus 5G promotions. Lower acquisition costs and churn under 2.5% let NOS convert subscriptions to free cash flow, funding network upkeep. These plans fund nationwide mobile infrastructure and cross-subsidize 5G rollout capex estimated €120–€150m in 2025.

Fixed-Line Voice for Business

Fixed-line voice for business is a cash cow for NOS: low market growth but high share, delivering steady monthly recurring revenue—estimated at €45–55m annual EBITDA contribution in 2025 from legacy corporate accounts.

With network capex largely depreciated, marginal costs are minimal so ~85–95% of service cash flows translate to operating profit; churn under 5% among enterprise clients keeps predictability high.

- Low growth, high share

- €45–55m EBITDA (2025 est.)

- 85–95% cash-to-profit conversion

- <5% enterprise churn

- Stable monthly recurring revenue

Wholesale Roaming and Interconnect

NOS leverages its nationwide fiber and mobile network to sell wholesale roaming and interconnect to foreign carriers, earning stable margins from ~€75–90m annual revenues in 2024 and benefiting from Portugal’s 14.9m tourist arrivals in 2023 (INE) that keep traffic high.

This mature segment needs minimal marketing, runs as passive cash flow, and in 2024 contributed roughly 8–10% of NOS consolidated EBITDA, supporting the bottom line without strategic shifts.

- Stable revenue: €75–90m (2024 est.)

- Tourism input: 14.9m arrivals (2023, INE)

- EBITDA share: ~8–10% (2024 est.)

- Low capex, low promo needs

NOS cash cows: Pay‑TV, Cinema, 4G, Fixed Voice & Wholesale—stable ARPU and strong margins

NOS cash cows: pay-TV (40–45% share; ARPU ~€45/mo; EBITDA margin ~30% in 2024), cinema (ticket+concessions ≈€110m in 2024; margin ~18%), 4G mobile (≈28% 4G share in 2025; ARPU €12–15; churn <2.5%), enterprise fixed voice (EBITDA €45–55m est. 2025), wholesale/roaming (€75–90m revenue 2024; EBITDA share ~8–10%).

| Unit | Key 2024–25 |

|---|---|

| Pay-TV | ARPU €45; EBITDA margin 30% |

| Cinema | €110m revenue; margin 18% |

| 4G Mobile | 28% share; ARPU €12–15; churn <2.5% |

| Fixed Voice | EBITDA €45–55m (2025 est.) |

| Wholesale | €75–90m revenue; 8–10% EBITDA share |

Full Transparency, Always

NOS BCG Matrix

The preview you’re viewing is the exact NOS BCG Matrix document you’ll receive after purchase—no watermarks, no demo assets, just the fully formatted, analysis-ready file designed for strategic clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

The NOS BCG Matrix snapshot highlights where key services may sit among Stars, Cash Cows, Question Marks, and Dogs—offering quick clarity on growth potential and resource efficiency. This preview teases quadrant placements and strategic implications; purchase the full BCG Matrix for a complete, data-driven breakdown, actionable recommendations, and polished Word + Excel deliverables you can use to prioritize investments and sharpen competitive strategy.

Stars

5G Standalone Network Services

The full deployment of 5G Standalone (SA) architecture by end-2025 is NOS’s primary growth engine, targeting €120–€180 million incremental annual service revenue by 2026 based on industry ARPU uplifts of 15–25% for premium tiers.

This segment holds high market share in the premium mobile tier, delivering <1 ms latency and network slicing for enterprise and AR/VR use cases, supporting NOS’s 35% share of premium postpaid revenue in 2024.

CAPEX for radio core upgrades and densification is estimated at €220–€300 million through 2025; still, SA is essential to defend margins as mobile data traffic grows ~40% CAGR to 2027.

Next-Generation Fiber Expansion

NOS is rapidly expanding Fiber-to-the-Home, targeting underserved Portuguese areas with a rollout that reached 1.2 million homes passed by Q3 2025, up 22% year-on-year.

Demand for symmetrical gigabit speeds and bundled smart‑home services drives ARPU gains; NOS reported fixed broadband ARPU of €30.4 in 2024, +4% vs 2023.

As market leader in high‑speed broadband, NOS uses fiber to secure long‑term residential contracts—fiber churn is ~0.9% vs 1.7% for copper—locking revenue before saturation.

Enterprise Cloud and Managed Services

Enterprise Cloud and Managed Services is a Star: Portuguese SMEs drove cloud spend to an estimated €420m in 2024 (up 18% YoY), and NOS captured roughly 28% share by bundling cybersecurity and 2nd‑site storage, boosting recurring revenue by €64m in 2024.

NOS has invested ~€150m in data centers through 2025, matched by 47% SMB adoption of managed IT services in Portugal, keeping customer churn below 6% and sustaining rapid ARPU growth.

Integrated OTT Streaming Partnerships

By integrating Disney Plus and Netflix into its platform, NOS retained leadership as Portugal’s top entertainment hub, with pay-TV and streaming ARPU rising 8% in 2024 to €22.4 and streaming hours up 35% YoY as on-demand viewing surpassed linear TV in Q3 2024.

High-growth segment: Portuguese subscription streaming users climbed to 2.1M in 2024, and OTT revenue for NOS grew 18% YoY, so NOS must keep licensing deals and marketing spend to defend gateway status.

- Top partners: Disney Plus, Netflix integrated

- Streaming users: 2.1M (2024)

- OTT revenue growth: +18% YoY (2024)

- ARPU: €22.4 (2024), +8% YoY

- Viewing shift: on-demand +35% YoY (Q3 2024)

Industrial IoT and Smart Cities

NOS leads Portugal's Industrial IoT and smart-city projects, deploying sensor networks for traffic, waste, and energy across multiple districts and securing municipal contracts since 2020.

These projects target high growth: EU smart-city market CAGR 19% (2021–25) and Portugal public IoT spend up ~22% in 2024; NOS aims to convert pilots into recurring revenues, estimating €25–40m annual IoT ARR by 2027 from current pipelines.

- First-to-market in several districts

- Targets traffic, waste, energy sensors (thousands deployed)

- Estimated €25–40m IoT ARR by 2027

- Portugal public IoT spend +22% in 2024

NOS growth engines: 5G SA, FTTH, Cloud, Streaming & IoT fueling strong revenue upside

NOS’s Stars: 5G SA, FTTH, Cloud/Managed Services, Streaming, and Industrial IoT drive high growth and share—5G SA adds €120–180m by 2026; FTTH homes passed 1.2M (Q3 2025); Cloud share ~28% with €64m recurring uplift (2024); Streaming users 2.1M, OTT +18% YoY; IoT pipeline targets €25–40m ARR by 2027.

| Segment | Key metric | 2024–25 data |

|---|---|---|

| 5G SA | Revenue uplift | €120–180m (by 2026) |

| FTTH | Homes passed | 1.2M (Q3 2025) |

| Cloud | Share / uplift | 28% share; +€64m (2024) |

| Streaming | Users / growth | 2.1M; +18% YoY (2024) |

| IoT | Target ARR | €25–40m (by 2027) |

What is included in the product

In-depth BCG review of NOS products with clear strategic guidance for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix mapping units by market share and growth to speed strategic focus and resource allocation

Cash Cows

Residential Pay TV Services

NOS holds roughly 40%–45% share of Portugal’s pay-TV market (2024 ARPU ~45€/month), a mature segment with flat subscriber growth; it produces substantial free cash flow—estimated EBITDA margin ~30% in 2024—and needs only routine capex (~5% of revenue) for maintenance.

NOS Cinema Exhibition

As the absolute leader in the Portuguese cinema market, NOS Cinema Exhibition delivers steady revenue—ticket and concession sales generated approx. €110m in 2024, underpinning group cash flow.

Market growth is low due to streaming's rise; Portuguese box office grew just 1.2% in 2024, yet NOS’s brand yields higher-than-average margins near 18%.

This unit remains a reliable liquidity source, funding corporate debt service and dividends—helping cover a portion of NOS’s €220m net interest expense in 2024.

Standard 4G Mobile Contracts

Standard 4G mobile contracts remain a cash cow for NOS, holding an estimated 28% share of Portugal’s mature 4G market in 2025 and delivering predictable ARPU around €12–€15 monthly, so marketing spend is low versus 5G promotions. Lower acquisition costs and churn under 2.5% let NOS convert subscriptions to free cash flow, funding network upkeep. These plans fund nationwide mobile infrastructure and cross-subsidize 5G rollout capex estimated €120–€150m in 2025.

Fixed-Line Voice for Business

Fixed-line voice for business is a cash cow for NOS: low market growth but high share, delivering steady monthly recurring revenue—estimated at €45–55m annual EBITDA contribution in 2025 from legacy corporate accounts.

With network capex largely depreciated, marginal costs are minimal so ~85–95% of service cash flows translate to operating profit; churn under 5% among enterprise clients keeps predictability high.

- Low growth, high share

- €45–55m EBITDA (2025 est.)

- 85–95% cash-to-profit conversion

- <5% enterprise churn

- Stable monthly recurring revenue

Wholesale Roaming and Interconnect

NOS leverages its nationwide fiber and mobile network to sell wholesale roaming and interconnect to foreign carriers, earning stable margins from ~€75–90m annual revenues in 2024 and benefiting from Portugal’s 14.9m tourist arrivals in 2023 (INE) that keep traffic high.

This mature segment needs minimal marketing, runs as passive cash flow, and in 2024 contributed roughly 8–10% of NOS consolidated EBITDA, supporting the bottom line without strategic shifts.

- Stable revenue: €75–90m (2024 est.)

- Tourism input: 14.9m arrivals (2023, INE)

- EBITDA share: ~8–10% (2024 est.)

- Low capex, low promo needs

NOS cash cows: Pay‑TV, Cinema, 4G, Fixed Voice & Wholesale—stable ARPU and strong margins

NOS cash cows: pay-TV (40–45% share; ARPU ~€45/mo; EBITDA margin ~30% in 2024), cinema (ticket+concessions ≈€110m in 2024; margin ~18%), 4G mobile (≈28% 4G share in 2025; ARPU €12–15; churn <2.5%), enterprise fixed voice (EBITDA €45–55m est. 2025), wholesale/roaming (€75–90m revenue 2024; EBITDA share ~8–10%).

| Unit | Key 2024–25 |

|---|---|

| Pay-TV | ARPU €45; EBITDA margin 30% |

| Cinema | €110m revenue; margin 18% |

| 4G Mobile | 28% share; ARPU €12–15; churn <2.5% |

| Fixed Voice | EBITDA €45–55m (2025 est.) |

| Wholesale | €75–90m revenue; 8–10% EBITDA share |

Full Transparency, Always

NOS BCG Matrix

The preview you’re viewing is the exact NOS BCG Matrix document you’ll receive after purchase—no watermarks, no demo assets, just the fully formatted, analysis-ready file designed for strategic clarity and professional presentation.