NOS Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

NOS faces moderate buyer power and intense rivalry, while supplier influence and substitution risks hinge on tech advancements and regulatory shifts; barriers to entry remain significant but evolving. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore NOS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Infrastructure Vendors

NOS relies on a few global vendors—Ericsson, Nokia, and Huawei—for 5G and fiber gear, concentrating supply and giving these firms pricing and support leverage; Ericsson and Nokia accounted for ~45% of global 5G RAN revenue in 2024.

That supplier concentration forces NOS to accept longer vendor lock-in and stricter SLAs, raising negotiation risk and potential downtime costs; spare-part lead times exceeded 12 weeks in parts of 2024.

To keep network reliability while funding capex, NOS must balance vendor-dependent OPEX with planned capex of ~€500–€700m through 2025, seeking multi-vendor sourcing and volume discounts.

Premium Content Acquisition Costs

Global Semiconductor and Device Shortages

NOS relies on mobile handsets and set-top boxes from Apple, Samsung and niche OEMs; in 2024 global semiconductor shortages cut device shipments ~15% year-on-year, raising single-quarter fulfillment shortfalls to >10% for telco suppliers.

Disruptions in fabs (TSMC, Samsung Foundry) can delay NOS hardware upgrades and new-subscriber activations, so supplier allocation and wafer pricing hikes (chip cost up ~20% in 2023–24) directly squeeze margins.

Energy Provider Dependency

Operating massive data centres and a nationwide network makes NOS highly exposed to energy-price swings; in Q3 2025 European wholesale electricity prices averaged about 150 EUR/MWh, up ~35% vs 2022, a cost largely non-negotiable with utilities.

This supplier power drives NOS to invest in efficiency: NOS reported €42m capex on energy-saving projects in 2024 and targets 20% PUE improvement across its fleet by 2027 to blunt price shocks.

- Wholesale price ~150 EUR/MWh (Q3 2025)

- €42m energy capex in 2024

- Target 20% PUE improvement by 2027

Specialized Technical Labor Market

The scarcity of senior cloud architects, cybersecurity specialists, and 5G engineers in Portugal gives suppliers of specialized labor strong bargaining power, forcing NOS to match offers from global hubs like Dublin and London.

In 2025 Portugal had a 6.8% vacancy rate for ICT specialist roles and median tech salaries rose ~12% year-on-year, pushing NOS wage bills higher and compressing margins.

NOS responds with richer employee value propositions—remote work, training allowances, and signing bonuses—raising annual per-hire cost by an estimated €18–25k.

- 6.8% ICT vacancy rate (Portugal, 2025)

- Tech salaries +12% YoY (2025)

- Per-hire uplift ≈ €18–25k for retention

Supplier power, rising energy & talent costs squeeze NOS margins and force capex

Supplier power is high: concentrated network vendors (Ericsson/Nokia/Huawei ~45% 5G RAN share in 2024), exclusive sports rights (€300–€400m pa), energy price exposure (~150 EUR/MWh Q3 2025), and tight ICT labor (6.8% vacancy, tech pay +12% in 2025) squeeze NOS margins and force multi-vendor sourcing, efficiency capex (€42m energy capex 2024) and higher hiring costs (€18–25k per hire).

| Metric | Value |

|---|---|

| 5G RAN share (2024) | Ericsson+Nokia ≈45% |

| Football rights (annual) | €300–€400m |

| Wholesale electricity (Q3 2025) | ~150 EUR/MWh |

| Energy capex (2024) | €42m |

| ICT vacancy (Portugal, 2025) | 6.8% |

| Tech salary change (2025) | +12% YoY |

| Per-hire uplift | €18–25k |

What is included in the product

Tailored Porter's Five Forces for NOS, uncovering competitive drivers, buyer/supplier influence, entry barriers, substitutes, and disruptive threats with industry data and strategic commentary for investor and strategy use.

Interactive NOS Porter's Five Forces—quickly gauge competitive pressure with a single-sheet summary and customizable force levels to support fast, data-driven strategy decisions.

Customers Bargaining Power

Low Switching Costs for Consumers

Regulation in Portugal, including the 2019 European portability rules and ANACOM updates, cut mobile number porting times to under 1 business day, making switching cheap and fast for consumers. As of 2024, porting rose ~8% year-on-year, and NOS reported a 2.1% residential churn in H1 2025, reflecting deal-driven moves. NOS must spend more on retention: its 2024 commercial costs rose to €112m, partly for loyalty offers and subsidies. Lower switching costs force continuous promotional spend to protect market share.

High Price Sensitivity in the Retail Segment

Portuguese consumers in 2025 cut discretionary spend, raising price sensitivity: 62% report comparing utility/entertainment bills monthly (Eurobarometer-style survey, 2025). Customers shop bundles for lowest price-per-gigabit and most channels, constraining NOS from raising prices; a 5% price hike risks ~1–2 pp churn based on 2024–25 retention elasticity for telco bundles. This compresses margin growth and forces promotional tactics.

Demand for Convergent Service Bundles

Modern Portuguese customers demand convergent bundles—mobile, fixed, broadband, and streaming—pressuring NOS as 72% of EU households sought triple/quad-play deals in 2023; buyers use this to extract average discounts of 12–18% vs single services.

That buying power forces NOS to refresh bundles: NOS reported convergent ARPU (average revenue per user) of €34.8 in 2024, down 2.1% YoY, showing margin pressure from loyalty discounts and product innovation costs.

Corporate Client Negotiation Leverage

Informed Decision Making via Digital Tools

Online comparison sites and apps let customers compare NOS with rivals in real time, cutting information asymmetry that once favored big telcos; 72% of Portuguese consumers used comparison tools for telecom choices in 2024 (Eurostat survey).

With data on pricing, speeds, and NPS publicly available, buyers now contest contract clauses and push for SLA (service-level agreement) parity; churn-sensitive offers rose 15% across Iberian ISPs in 2023.

Greater transparency pressures NOS to match market standards on price, speed, and support or face faster defections.

- 72% of Portuguese consumers used comparison tools in 2024

- 15% rise in churn-sensitive offers among Iberian ISPs in 2023

- Public NPS, pricing, and speed data reduce NOS’s informational edge

NOS faces high churn and margin pressure as large clients and tender cuts squeeze EBITDA

High portability, price-sensitive consumers, and widespread bundle-shopping give NOS low customer power: fast porting (<1 business day) and 62% monthly bill comparison (2025) raise churn; NOS H1 2025 residential churn 2.1% and 2024 commercial costs €112m. Large clients (45% revenue, 2024) exert strong pricing leverage; public tenders ~18% below incumbents (2023) risk 6–9% regional EBITDA loss.

| Metric | Value |

|---|---|

| Porting time | <1 business day (2019 rules) |

| Consumer comparison | 62% monthly (2025) |

| Residential churn | 2.1% H1 2025 |

| Commercial costs | €112m (2024) |

| Large-client revenue | 45% (2024) |

| Public tender discount | ~18% (2023) |

What You See Is What You Get

NOS Porter's Five Forces Analysis

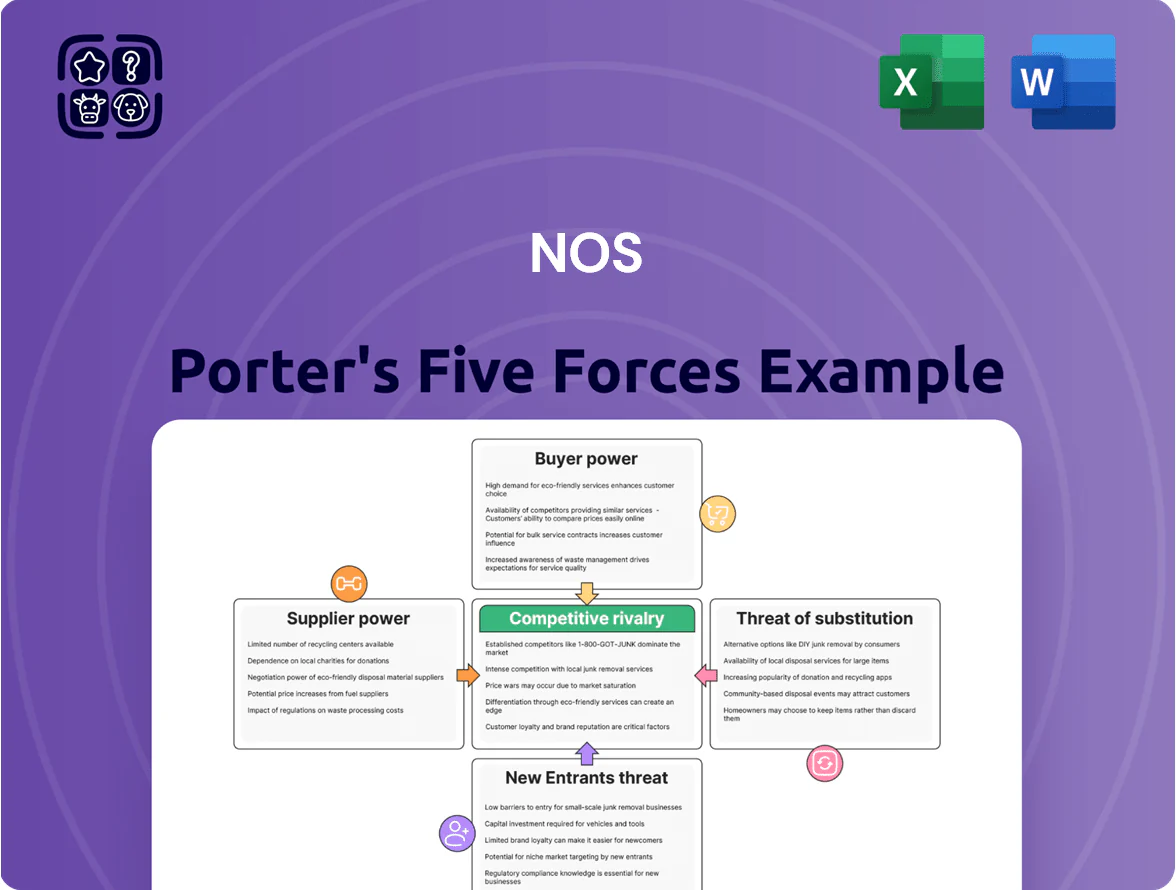

This preview shows the exact NOS Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is the final, professionally formatted file, covering threat of new entrants, bargaining power of suppliers and buyers, threat of substitutes, and competitive rivalry with actionable insights. Once you buy, you’ll get instant access to this same ready-to-use analysis.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

NOS faces moderate buyer power and intense rivalry, while supplier influence and substitution risks hinge on tech advancements and regulatory shifts; barriers to entry remain significant but evolving. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore NOS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Infrastructure Vendors

NOS relies on a few global vendors—Ericsson, Nokia, and Huawei—for 5G and fiber gear, concentrating supply and giving these firms pricing and support leverage; Ericsson and Nokia accounted for ~45% of global 5G RAN revenue in 2024.

That supplier concentration forces NOS to accept longer vendor lock-in and stricter SLAs, raising negotiation risk and potential downtime costs; spare-part lead times exceeded 12 weeks in parts of 2024.

To keep network reliability while funding capex, NOS must balance vendor-dependent OPEX with planned capex of ~€500–€700m through 2025, seeking multi-vendor sourcing and volume discounts.

Premium Content Acquisition Costs

Global Semiconductor and Device Shortages

NOS relies on mobile handsets and set-top boxes from Apple, Samsung and niche OEMs; in 2024 global semiconductor shortages cut device shipments ~15% year-on-year, raising single-quarter fulfillment shortfalls to >10% for telco suppliers.

Disruptions in fabs (TSMC, Samsung Foundry) can delay NOS hardware upgrades and new-subscriber activations, so supplier allocation and wafer pricing hikes (chip cost up ~20% in 2023–24) directly squeeze margins.

Energy Provider Dependency

Operating massive data centres and a nationwide network makes NOS highly exposed to energy-price swings; in Q3 2025 European wholesale electricity prices averaged about 150 EUR/MWh, up ~35% vs 2022, a cost largely non-negotiable with utilities.

This supplier power drives NOS to invest in efficiency: NOS reported €42m capex on energy-saving projects in 2024 and targets 20% PUE improvement across its fleet by 2027 to blunt price shocks.

- Wholesale price ~150 EUR/MWh (Q3 2025)

- €42m energy capex in 2024

- Target 20% PUE improvement by 2027

Specialized Technical Labor Market

The scarcity of senior cloud architects, cybersecurity specialists, and 5G engineers in Portugal gives suppliers of specialized labor strong bargaining power, forcing NOS to match offers from global hubs like Dublin and London.

In 2025 Portugal had a 6.8% vacancy rate for ICT specialist roles and median tech salaries rose ~12% year-on-year, pushing NOS wage bills higher and compressing margins.

NOS responds with richer employee value propositions—remote work, training allowances, and signing bonuses—raising annual per-hire cost by an estimated €18–25k.

- 6.8% ICT vacancy rate (Portugal, 2025)

- Tech salaries +12% YoY (2025)

- Per-hire uplift ≈ €18–25k for retention

Supplier power, rising energy & talent costs squeeze NOS margins and force capex

Supplier power is high: concentrated network vendors (Ericsson/Nokia/Huawei ~45% 5G RAN share in 2024), exclusive sports rights (€300–€400m pa), energy price exposure (~150 EUR/MWh Q3 2025), and tight ICT labor (6.8% vacancy, tech pay +12% in 2025) squeeze NOS margins and force multi-vendor sourcing, efficiency capex (€42m energy capex 2024) and higher hiring costs (€18–25k per hire).

| Metric | Value |

|---|---|

| 5G RAN share (2024) | Ericsson+Nokia ≈45% |

| Football rights (annual) | €300–€400m |

| Wholesale electricity (Q3 2025) | ~150 EUR/MWh |

| Energy capex (2024) | €42m |

| ICT vacancy (Portugal, 2025) | 6.8% |

| Tech salary change (2025) | +12% YoY |

| Per-hire uplift | €18–25k |

What is included in the product

Tailored Porter's Five Forces for NOS, uncovering competitive drivers, buyer/supplier influence, entry barriers, substitutes, and disruptive threats with industry data and strategic commentary for investor and strategy use.

Interactive NOS Porter's Five Forces—quickly gauge competitive pressure with a single-sheet summary and customizable force levels to support fast, data-driven strategy decisions.

Customers Bargaining Power

Low Switching Costs for Consumers

Regulation in Portugal, including the 2019 European portability rules and ANACOM updates, cut mobile number porting times to under 1 business day, making switching cheap and fast for consumers. As of 2024, porting rose ~8% year-on-year, and NOS reported a 2.1% residential churn in H1 2025, reflecting deal-driven moves. NOS must spend more on retention: its 2024 commercial costs rose to €112m, partly for loyalty offers and subsidies. Lower switching costs force continuous promotional spend to protect market share.

High Price Sensitivity in the Retail Segment

Portuguese consumers in 2025 cut discretionary spend, raising price sensitivity: 62% report comparing utility/entertainment bills monthly (Eurobarometer-style survey, 2025). Customers shop bundles for lowest price-per-gigabit and most channels, constraining NOS from raising prices; a 5% price hike risks ~1–2 pp churn based on 2024–25 retention elasticity for telco bundles. This compresses margin growth and forces promotional tactics.

Demand for Convergent Service Bundles

Modern Portuguese customers demand convergent bundles—mobile, fixed, broadband, and streaming—pressuring NOS as 72% of EU households sought triple/quad-play deals in 2023; buyers use this to extract average discounts of 12–18% vs single services.

That buying power forces NOS to refresh bundles: NOS reported convergent ARPU (average revenue per user) of €34.8 in 2024, down 2.1% YoY, showing margin pressure from loyalty discounts and product innovation costs.

Corporate Client Negotiation Leverage

Informed Decision Making via Digital Tools

Online comparison sites and apps let customers compare NOS with rivals in real time, cutting information asymmetry that once favored big telcos; 72% of Portuguese consumers used comparison tools for telecom choices in 2024 (Eurostat survey).

With data on pricing, speeds, and NPS publicly available, buyers now contest contract clauses and push for SLA (service-level agreement) parity; churn-sensitive offers rose 15% across Iberian ISPs in 2023.

Greater transparency pressures NOS to match market standards on price, speed, and support or face faster defections.

- 72% of Portuguese consumers used comparison tools in 2024

- 15% rise in churn-sensitive offers among Iberian ISPs in 2023

- Public NPS, pricing, and speed data reduce NOS’s informational edge

NOS faces high churn and margin pressure as large clients and tender cuts squeeze EBITDA

High portability, price-sensitive consumers, and widespread bundle-shopping give NOS low customer power: fast porting (<1 business day) and 62% monthly bill comparison (2025) raise churn; NOS H1 2025 residential churn 2.1% and 2024 commercial costs €112m. Large clients (45% revenue, 2024) exert strong pricing leverage; public tenders ~18% below incumbents (2023) risk 6–9% regional EBITDA loss.

| Metric | Value |

|---|---|

| Porting time | <1 business day (2019 rules) |

| Consumer comparison | 62% monthly (2025) |

| Residential churn | 2.1% H1 2025 |

| Commercial costs | €112m (2024) |

| Large-client revenue | 45% (2024) |

| Public tender discount | ~18% (2023) |

What You See Is What You Get

NOS Porter's Five Forces Analysis

This preview shows the exact NOS Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is the final, professionally formatted file, covering threat of new entrants, bargaining power of suppliers and buyers, threat of substitutes, and competitive rivalry with actionable insights. Once you buy, you’ll get instant access to this same ready-to-use analysis.