Noumi Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

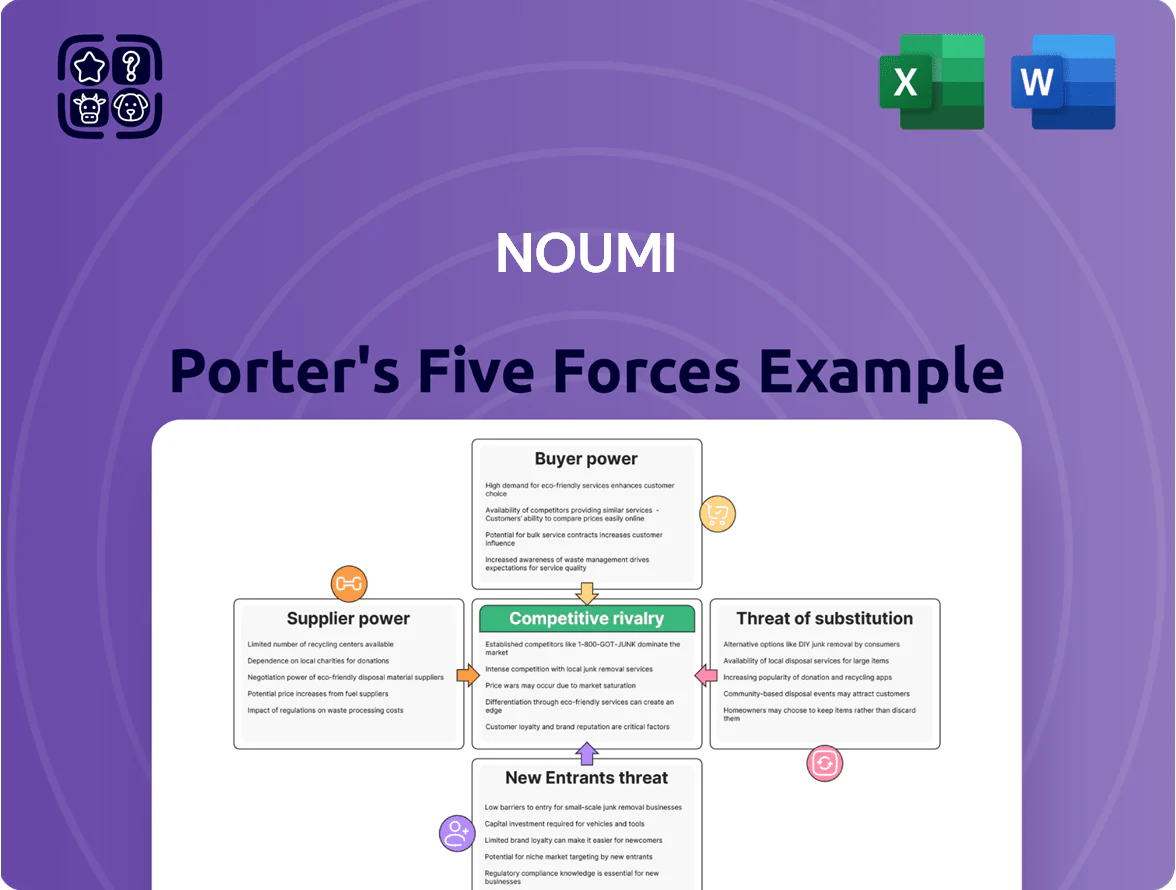

Noumi’s Porter's Five Forces snapshot highlights supplier bargaining, buyer sensitivity, competitive rivalry, entrant threats, and substitutes shaping its margins and growth prospects; core tensions stem from concentrated suppliers and evolving consumer preferences. This brief hints at where strategic vulnerability and opportunity lie—gain the full, consultant-grade Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable implications tailored to Noumi.

Suppliers Bargaining Power

Concentration of raw milk producers

The supply of raw milk is a critical input for Noumi’s nutritional and dairy snack divisions; Australia had about 5,800 dairy farms in 2024 but the top 10% of farms supply ~60% of milk, raising supplier concentration and bargaining power. Larger farming collectives negotiated higher farmgate prices—farmgate milk price averaged A$7.10/kg MS in 2024—so Noumi must secure long-term contracts and premiums for quality to stabilise supply and margins.

Volatility in agricultural commodity pricing

Suppliers of almonds, oats and soy exert moderate power: global commodity markets set prices and Noumi is price-taker in tight seasons. Australian droughts and water shortages cut almond and oat yields—Australia’s 2023 almond crop fell ~15%—raising input costs and squeezing margins. Specific quality specs for plant-based milk mean limited alternative sources, so low harvests force Noumi to pay spot premiums, sometimes +20% versus contract rates.

Specialized ingredient requirements for nutritionals

The production of high-protein nutritionals needs specialized ingredients like lactoferrin and pharma-grade vitamins, which only about 10–15 global suppliers meet as of 2025, raising supply concentration risk. Fewer qualified suppliers push up prices; lactoferrin spot prices rose ~22% in 2024, boosting input costs for makers like Noumi. This scarcity gives specialized chemical and nutrient suppliers stronger bargaining power over manufacturers.

Rising costs of sustainable packaging

- Bioplastic price rise ~18% (2024)

- Specialist suppliers hold ~65% capacity

- Premiums typically 10–25% higher

- Higher packaging spend raises COGS share

Energy and logistics provider influence

Manufacturing and distributing liquid dairy is energy-intensive and needs cold-chain or shelf-stable logistics; Australia’s commercial electricity rose ~12% in 2023–2024, raising input costs for Noumi.

Few nationwide logistics providers (3–5 major players) and limited cold-chain capacity give suppliers bargaining power; service outages directly stop Noumi serving domestic and export markets.

- Energy up ~12% (2023–24)

- 3–5 major national logistics providers

- Cold-chain disruptions = halted sales

Supplier concentration and input inflation squeeze Noumi’s margins—COGS risk rises

Suppliers hold moderate-to-high power: concentrated dairy farms (top 10% supply ~60%), scarce specialty nutrients (10–15 global lactoferrin suppliers), and packaging/cold-chain bottlenecks (65% specialist bioplastic capacity, 3–5 national logistics players) force Noumi into long-term contracts and spot premiums (lactoferrin +22% 2024; bioplastic +18% 2024; premium 10–25%), raising COGS and margin risk.

| Item | Key stat (year) |

|---|---|

| Top farm share | Top 10% → 60% (2024) |

| Lactoferrin suppliers | 10–15 global (2025) |

| Lactoferrin price | +22% (2024) |

| Bioplastic capacity | 65% specialist (2024) |

| Bioplastic price | +18% (2024) |

| Logistics providers | 3–5 national |

What is included in the product

Tailored exclusively for Noumi, this Porter’s Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to inform pricing, profitability, and strategic defense.

A concise Noumi Porter's Five Forces one-sheet that maps supplier, buyer, entrant, substitute, and rivalry pressures—ideal for fast strategic decisions and investor briefings.

Customers Bargaining Power

Dominance of the Australian grocery duopoly

The Australian grocery market is dominated by Woolworths and Coles, which together held about 67% of national supermarket sales in 2024, making them primary gatekeepers to consumers. These retailers exert strong bargaining power, routinely extracting lower wholesale prices and demanding promotional funding—Woolworths and Coles increased supplier rebates to roughly 3–5% of supplier revenue in recent contracts. Noumi’s dependence on these two chains for most domestic retail volume leaves its margins exposed to such price pressure and promotional costs.

Expansion of private label offerings

Major retailers like Woolworths and Coles expanded private-label plant-based lines 22% in 2024, grabbing premium shelf positions versus brands such as Milklab and Noumi.

Store brands undercut prices by 10–25%, forcing Noumi to fund R&D and limited editions to justify a 15–30% premium; R&D spend rose 12% in 2024 for Australian dairy players.

If retailers shift focus to own-labels, Noumi risks a 5–20% drop in national shelf facings and corresponding volume declines, based on category share movements in 2023–24.

Low switching costs for end consumers

Low switching costs mean US retail consumers can swap plant-based milk brands virtually free, and 62% of shoppers say price/promos drive their choice (2024 IRI). Milklab's cafe equity is strong, but retail buyers chase weekly discounts and shelf availability, so Noumi faces churn. Noumi must spend more on marketing: company reports show SG&A in 2024 rose 18% as loyalty and promo spend climbed to protect share.

Price sensitivity in international export markets

Influence of the professional barista channel

Noumi’s Milklab depends on professional baristas and café owners for adoption; this channel drove about 40% of Milklab’s 2024 revenue (≈AU$48m of AU$120m), so their preferences matter more than retail price sensitivity.

Professionals demand consistent texture and taste; a competitor with better coffee performance can flip accounts quickly, shrinking Noumi’s high-margin B2B niche and cutting gross margin by an estimated 3–6 points if churn hits 10–20%.

Here’s the quick math: losing 15% of professional revenue (~AU$7.2m) at an 18% margin gap reduces annual gross profit by ~AU$1.3m; what this hides is rising customer switching costs and contract terms.

- 40% of 2024 revenue from pros (~AU$48m)

- Professionals less price-sensitive, demand consistency

- 10–20% churn could cut gross margin 3–6 pts

- 15% loss ≈AU$7.2m revenue → ~AU$1.3m gross profit hit

Retail giants squeeze Noumi: rising rebates, SG&A and export pressures threaten shelf space

Buyers (Woolworths/Coles: ~67% market share 2024) have strong leverage, pushing rebates ~3–5% and boosting private-labels (+22% plant-based SKUs 2024), which forces Noumi to raise R&D and promo spend (SG&A +18% 2024) and risks 5–20% shelf-facing loss; export markets (30–40% revenue) face 10–20% lower-priced rivals and FX swings ±6–8% (2023–24), with Noumi absorbing ~60% of cost rises.

| Metric | Value (2023–24) |

|---|---|

| Woolworths+Coles share | ~67% |

| Supplier rebates | 3–5% revenue |

| Private-label growth (plant) | +22% |

| Noumi exports | 30–40% revenue |

| Competitor price gap | 10–20% |

| FX volatility | ±6–8% |

| SG&A change | +18% |

Preview the Actual Deliverable

Noumi Porter's Five Forces Analysis

This preview shows the exact Noumi Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy, covering rivalry, threats of entry and substitutes, bargaining power of suppliers and buyers, and strategic implications.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Noumi’s Porter's Five Forces snapshot highlights supplier bargaining, buyer sensitivity, competitive rivalry, entrant threats, and substitutes shaping its margins and growth prospects; core tensions stem from concentrated suppliers and evolving consumer preferences. This brief hints at where strategic vulnerability and opportunity lie—gain the full, consultant-grade Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable implications tailored to Noumi.

Suppliers Bargaining Power

Concentration of raw milk producers

The supply of raw milk is a critical input for Noumi’s nutritional and dairy snack divisions; Australia had about 5,800 dairy farms in 2024 but the top 10% of farms supply ~60% of milk, raising supplier concentration and bargaining power. Larger farming collectives negotiated higher farmgate prices—farmgate milk price averaged A$7.10/kg MS in 2024—so Noumi must secure long-term contracts and premiums for quality to stabilise supply and margins.

Volatility in agricultural commodity pricing

Suppliers of almonds, oats and soy exert moderate power: global commodity markets set prices and Noumi is price-taker in tight seasons. Australian droughts and water shortages cut almond and oat yields—Australia’s 2023 almond crop fell ~15%—raising input costs and squeezing margins. Specific quality specs for plant-based milk mean limited alternative sources, so low harvests force Noumi to pay spot premiums, sometimes +20% versus contract rates.

Specialized ingredient requirements for nutritionals

The production of high-protein nutritionals needs specialized ingredients like lactoferrin and pharma-grade vitamins, which only about 10–15 global suppliers meet as of 2025, raising supply concentration risk. Fewer qualified suppliers push up prices; lactoferrin spot prices rose ~22% in 2024, boosting input costs for makers like Noumi. This scarcity gives specialized chemical and nutrient suppliers stronger bargaining power over manufacturers.

Rising costs of sustainable packaging

- Bioplastic price rise ~18% (2024)

- Specialist suppliers hold ~65% capacity

- Premiums typically 10–25% higher

- Higher packaging spend raises COGS share

Energy and logistics provider influence

Manufacturing and distributing liquid dairy is energy-intensive and needs cold-chain or shelf-stable logistics; Australia’s commercial electricity rose ~12% in 2023–2024, raising input costs for Noumi.

Few nationwide logistics providers (3–5 major players) and limited cold-chain capacity give suppliers bargaining power; service outages directly stop Noumi serving domestic and export markets.

- Energy up ~12% (2023–24)

- 3–5 major national logistics providers

- Cold-chain disruptions = halted sales

Supplier concentration and input inflation squeeze Noumi’s margins—COGS risk rises

Suppliers hold moderate-to-high power: concentrated dairy farms (top 10% supply ~60%), scarce specialty nutrients (10–15 global lactoferrin suppliers), and packaging/cold-chain bottlenecks (65% specialist bioplastic capacity, 3–5 national logistics players) force Noumi into long-term contracts and spot premiums (lactoferrin +22% 2024; bioplastic +18% 2024; premium 10–25%), raising COGS and margin risk.

| Item | Key stat (year) |

|---|---|

| Top farm share | Top 10% → 60% (2024) |

| Lactoferrin suppliers | 10–15 global (2025) |

| Lactoferrin price | +22% (2024) |

| Bioplastic capacity | 65% specialist (2024) |

| Bioplastic price | +18% (2024) |

| Logistics providers | 3–5 national |

What is included in the product

Tailored exclusively for Noumi, this Porter’s Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to inform pricing, profitability, and strategic defense.

A concise Noumi Porter's Five Forces one-sheet that maps supplier, buyer, entrant, substitute, and rivalry pressures—ideal for fast strategic decisions and investor briefings.

Customers Bargaining Power

Dominance of the Australian grocery duopoly

The Australian grocery market is dominated by Woolworths and Coles, which together held about 67% of national supermarket sales in 2024, making them primary gatekeepers to consumers. These retailers exert strong bargaining power, routinely extracting lower wholesale prices and demanding promotional funding—Woolworths and Coles increased supplier rebates to roughly 3–5% of supplier revenue in recent contracts. Noumi’s dependence on these two chains for most domestic retail volume leaves its margins exposed to such price pressure and promotional costs.

Expansion of private label offerings

Major retailers like Woolworths and Coles expanded private-label plant-based lines 22% in 2024, grabbing premium shelf positions versus brands such as Milklab and Noumi.

Store brands undercut prices by 10–25%, forcing Noumi to fund R&D and limited editions to justify a 15–30% premium; R&D spend rose 12% in 2024 for Australian dairy players.

If retailers shift focus to own-labels, Noumi risks a 5–20% drop in national shelf facings and corresponding volume declines, based on category share movements in 2023–24.

Low switching costs for end consumers

Low switching costs mean US retail consumers can swap plant-based milk brands virtually free, and 62% of shoppers say price/promos drive their choice (2024 IRI). Milklab's cafe equity is strong, but retail buyers chase weekly discounts and shelf availability, so Noumi faces churn. Noumi must spend more on marketing: company reports show SG&A in 2024 rose 18% as loyalty and promo spend climbed to protect share.

Price sensitivity in international export markets

Influence of the professional barista channel

Noumi’s Milklab depends on professional baristas and café owners for adoption; this channel drove about 40% of Milklab’s 2024 revenue (≈AU$48m of AU$120m), so their preferences matter more than retail price sensitivity.

Professionals demand consistent texture and taste; a competitor with better coffee performance can flip accounts quickly, shrinking Noumi’s high-margin B2B niche and cutting gross margin by an estimated 3–6 points if churn hits 10–20%.

Here’s the quick math: losing 15% of professional revenue (~AU$7.2m) at an 18% margin gap reduces annual gross profit by ~AU$1.3m; what this hides is rising customer switching costs and contract terms.

- 40% of 2024 revenue from pros (~AU$48m)

- Professionals less price-sensitive, demand consistency

- 10–20% churn could cut gross margin 3–6 pts

- 15% loss ≈AU$7.2m revenue → ~AU$1.3m gross profit hit

Retail giants squeeze Noumi: rising rebates, SG&A and export pressures threaten shelf space

Buyers (Woolworths/Coles: ~67% market share 2024) have strong leverage, pushing rebates ~3–5% and boosting private-labels (+22% plant-based SKUs 2024), which forces Noumi to raise R&D and promo spend (SG&A +18% 2024) and risks 5–20% shelf-facing loss; export markets (30–40% revenue) face 10–20% lower-priced rivals and FX swings ±6–8% (2023–24), with Noumi absorbing ~60% of cost rises.

| Metric | Value (2023–24) |

|---|---|

| Woolworths+Coles share | ~67% |

| Supplier rebates | 3–5% revenue |

| Private-label growth (plant) | +22% |

| Noumi exports | 30–40% revenue |

| Competitor price gap | 10–20% |

| FX volatility | ±6–8% |

| SG&A change | +18% |

Preview the Actual Deliverable

Noumi Porter's Five Forces Analysis

This preview shows the exact Noumi Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy, covering rivalry, threats of entry and substitutes, bargaining power of suppliers and buyers, and strategic implications.